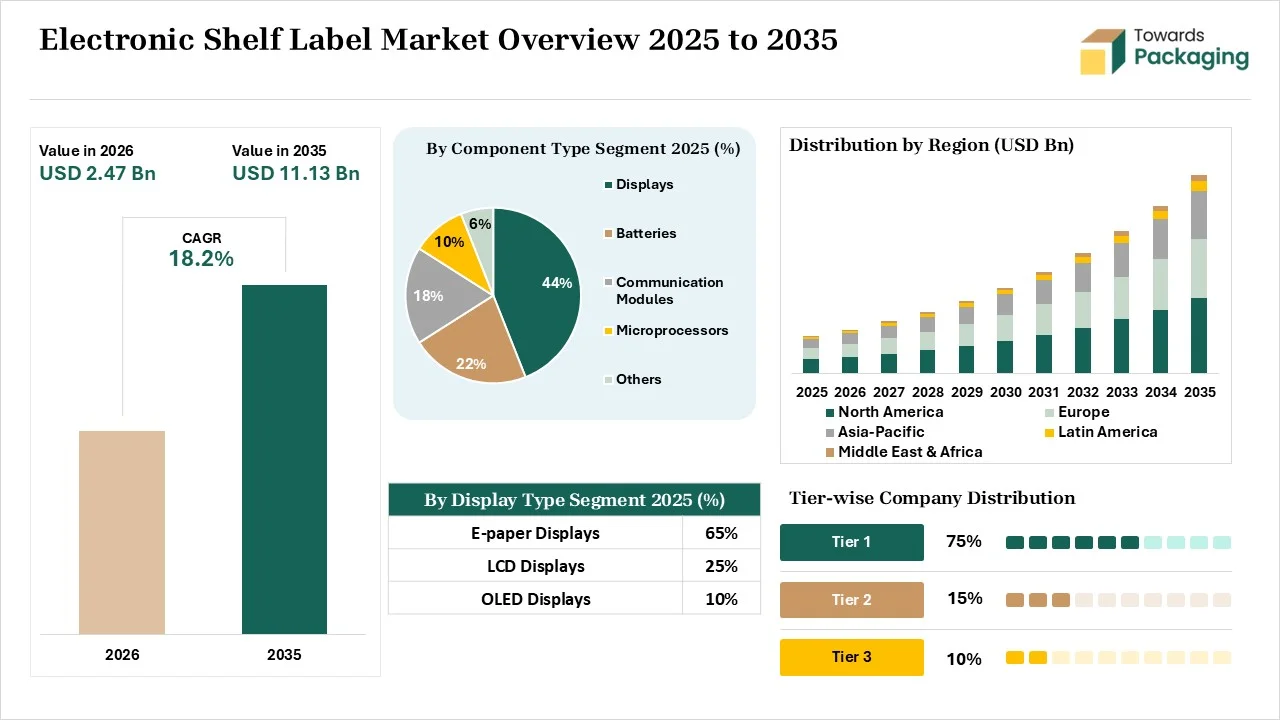

The Electronic Shelf Label market is projected to grow from USD 2.47 billion in 2026 to USD 11.13 billion by 2035, registering a robust CAGR of 18.2% during the forecast period. The report provides comprehensive coverage of market size, revenue forecasts, segment-wise performance, regional market trends, and growth opportunities. It includes detailed analysis of technology, product type, component, communication technology, store format, and end-use segments. The study also covers company profiles, competitive benchmarking, market share analysis, value chain assessment, trade statistics, pricing trends, manufacturer analysis, supplier landscape, distribution network evaluation, and strategic developments shaping the industry. Growth is supported by increasing focus on enhancing in-store customer experiences, sustainability initiatives, omnichannel retail expansion, and labor optimization strategies.

An electronic shelf label (ESL) is a replacement for traditional paper price tags. It is a type of digital display system that is used across retail shelves. It integrates wireless connectivity and display technology. It provides benefits like pricing accuracy, sustainability, massive labor savings, operational efficiency, and dynamic pricing. It features E-ink technology, omnichannel synchronization, inventory support, centralized updates, and interactive customer features. An electronic shelf label is used in applications like inventory management, customer interaction, expiration date management, medical, warehouse, omnichannel order fulfilment, and others.

For instance, the Canadian supermarket Sobeys plans to invest $51M in the electronic shelf labels. The company is collaborating with JRTech to install the latest technology of electronic shelf labels. The collaboration focuses on delivering a high-quality solution for retail infrastructure.

The electronic shelf label market growth is driven by shifting away from paper price tags, a rise in online e-commerce pricing, a focus on omnichannel alignment, expanding semiconductor components, growing major deployments of ESL, enhancing display technology, regulatory pressures, and the rise in retail giant endorsements.

The technological developments, such as machine learning algorithms, computer vision, edge computing, NFC integration, IoT integration, and cloud management, are taking place in the electronic shelf label market. Factors like optimization of store operations, personalized customer experiences, and elimination of paper waste are drivers for the ongoing technological developments. The AI adoption is a robust technological development driven by demand for real-time adjustments.

AI increases the profit margins and monitors the shelf-level stock. AI supports targeted promotions and automates label formatting. AI analyzes competitor pricing and easily predicts hardware failures. AI eliminates the need for manual tag changes and helps in hyper-personalised promotions. AI adjusts prices of near-expiration inventory and prevents operational disruptions. AI easily detects weak batteries and automatically showcases discounts. Overall, AI supports intelligent inventory management.

The stage sources raw materials like plastics, microcontrollers, biomaterials, display panels, printed circuit boards, batteries, radio, and semiconductors.

Material processing involves microcapsule preparation, circuit printing, and system-on-panel. Conversion includes lamination, die-cutting, and encapsulation.

Package design involves material selection, battery integration, and electronics placement. Prototyping involves 3D modeling, 3D printing, and testing.

The displays segment dominated the market with 44% share in 2025 due to the increased utilization of the centralized dashboard. The instant price updates and the focus on vibrant color capabilities increase the use of displays. The preference for better brand communication and the interest in high-contrast screens increase the adoption of displays. The interest in liquid crystal displays drives the segment growth.

The batteries segment held the 22% market share in 2025 due to the shift away from manual printing. The expansion of high-value tasks and the strong physical retail stores increases the adoption of batteries. The focus on store inventory systems and the robust green initiatives increases the use of batteries. The extended label lifespans and cost-efficiency of batteries support the segment growth.

The communication modules segment held the 18% market share in 2025 due to a focus on tracking assets in real-time. The cost-efficiency of automated pricing networks and the focus on time-sensitive promotions increase the use of communication models. The consumer demand for accessing digital coupons and the reduction of costly pricing errors increase the use of communication modules, boosting the overall segment growth.

The e-paper displays segment dominated the market with 65% share in 2025 due to its minimal power consumption. The need for real-time price updates and focus on brand storytelling increases the use of e-paper displays. The green retail initiatives and the display of complex characters increase the use of e-paper displays. The superior wide-angle viewing, multi-color displays, and high contrast of e-paper display drive the segment growth.

The LCD displays segment held the 25% market share in 2025 due to the increased display of rich media. The focus on updating the label wirelessly and the need for advanced display technology increase the use of LCD displays. The interest in vibrant promotional graphics and the need to display inventory locations increases the use of LCD displays. The excellent accuracy, rich display, agile pricing, and seamless automation of LCD displays support the segment growth.

The OLED displays segment held the 10% market share in 2025 due to growing use in in-store marketing. The expansion of modern supermarkets and the growth in showing quick animations increases the adoption of OLED displays. The retail stores' preference for displaying dynamic media and the focus on interactive shopping increase the use of OLED displays. The curved displays, superior readability, and vibrant marketing of OLED displays boost the segment growth.

The radio frequency (RF) segment dominated the market with 68% share in 2025 due to its compatibility with enterprise software networks. The massive retail spaces and the focus on eliminating the use of complex transmitter grids increase the adoption of RF. The growing demand for two-way communication and the focus on reducing metal shelving increase the use of RF. The superior coverage, high reliability, improved battery life, and superior penetration of RF drive the segment growth.

The Bluetooth Low Energy (BLE) segment held the 17% market share in 2025 due to the growing use in large-scale replacements. The focus on securing the backend of the retail systems and the indoor navigation activities increases the adoption of BLE. The demand for bi-directional communication and the need to preserve battery life span increase the use of BLE. The unprecedented scalability, enhanced security, and standardized interoperability of BLE support the segment growth.

The infrared (IR) segment held the 10% market share in 2025 due to the growing use in big-box supermarkets. The growing demand for interference-free communication and focus on low power utilization increases the use of IR. The preference for promotional updates increases IR adoption. The high network security, excellent scalability, and high security of IR support the overall growth of the segment.

The 3 to 7 inches segment dominated the market with 42% share in 2025 due to the optimal promotional space. The expansion of standard grocery and the diverse hypermarket store formats increases the use of 3 to 7 inches display. The growing general grocery labeling and the focus on catching customer attention increase the adoption of 3 to 7 inches display. The enhanced visibility and excellent shelf compatibility of 3 to 7 inches display drives the segment growth.

The less than 3 inches segment held the 36% market share in 2025 due to the growing use in grocery stores. The focus on remotely updating prices and a clearer display of promotional information increases adoption of less than 3 inches. The expanding convenience stores increase the adoption of displays of less than 3 inches. The operational automation, optimal space management, and affordability of less than 3 inches support the segment growth.

The 7 to 10 inches segment held the 15% market share in 2025 due to its high-resolution graphics. The expanding electronic stores and the advancements in merchandising strategies increase the use of 7 to 10 inches display. The growing premium retail use and the increased display of promotional videos increase the use of 7 to 10 inches display. The interactive experiences and enhanced customer engagement of 7 to 10 inches display boost the segment growth.

The retail segment dominated the market with 88% share in 2025 due to the preference for running dynamic promotions. The focus on saving time from tedious tasks and the growing human errors in traditional tags increases the use of ESL. The identification of empty shelf space and retail digitalization increases the adoption of ESL. The reduction of customer dissatisfaction and the large retail environments increase the use of ESL, driving the overall segment growth.

The industrial segment held the 12% market share in 2025 due to the demand for automated order picking. The growing communication in restock alerts and the rising need for displaying picking instructions increase the use of ESL. The growing number of industrial picking mistakes and the development of industrial-grade labels increase the adoption of ESL. The integration of ESL in major industrial hubs for tasks like margin protection, inventory efficiency, and others supports the segment growth.

The supermarkets & hypermarkets segment dominated the market with 42% share in 2025 due to the growing SKU volume. The frequent promotions and the minimization of errors increase the use of ESL. The massive price synchronization and the automation of inventory stocking increase the use of ESL. The growing e-commerce competition and investment in large chains increase the adoption of ESL. The stock management drives the segment growth.

The convenience stores segment held the 18% market share in 2025 due to the availability of happy hour discounts. The growing localized demand and the seamless pricing focus in convenience stores increase the adoption of ESL. The presence of a small staff and the multi-buy offers in convenience stores increases ESL use. The focus on streamlining restocking and efficient price management increases ESL use, supporting the segment growth.

The specialty retail stores segment held the 16% market share in 2025 due to the demand for real-time stock updates. The growing supplier fluctuations and the focus on building customer trust increase the use of ESL. The focus on reducing labor-intensive specialty store operations and the rise in smarter inventory tracking increase the use of ESL. The dynamic pricing and inventory automation of specialty retail stores boost the segment growth.

North America dominated the market with a 38% share in 2025. The massive retail chains and the scarcity of retail labor increase the adoption of ESL. The high availability of IoT solutions and the large e-commerce wings increase the use of ESL. The retailers' shift to digital solutions and the focus on automating price updates increase ESL use. The expensive grocery chains and the growing e-commerce pressures increase the use of ESL. The paperless initiatives drive the market growth.

Europe held the 30% market share in 2025. The high minimum wages and the retail industry's focus on matching online store prices increase the use of ESL. The expansion of mobile shopping and the large chain rollouts increases the adoption of ESL. The interest in paperless tags and the automation of operations in the retail sector increases ESL use. The focus on updating omnichannel pricing and the major tech companies' presence support the market growth.

Asia Pacific held the 24% share in the market and is growing at a fastest CAGR of 19.2% in the market during the forecast period. The rising labor cost in Asian countries and the expansion of smart store initiatives increase the adoption of ESL. The robustly growing modern trade and the increased deployment of technological solutions increase the use of ESL. The supply chain fluctuations in the retail sector and the interest in full-graphic e-paper tags support the market growth.

Latin America held the 5% market share in 2025. The focus on reducing operational costs and the omnichannel integration in physical shelves increases demand for ESL. The explosion of commercial shopping complexes and the rising penetration of cloud-based infrastructures increase the use of ESL. The focus on reducing requirements for manual price markdowns and the growth in physical stores increase the adoption of ESL, supporting the market growth.

The Middle East & Africa held the 3% market share in 2025. The presence of luxury retail stores and the elimination of human errors increase the use of ESL. The digital transformation agendas and the penetration of high-speed internet increase the use of ESL. The government focuses on building a smart city, and dynamic pricing execution increases the adoption of ESL. The presence of large shopping malls boosts the market growth.

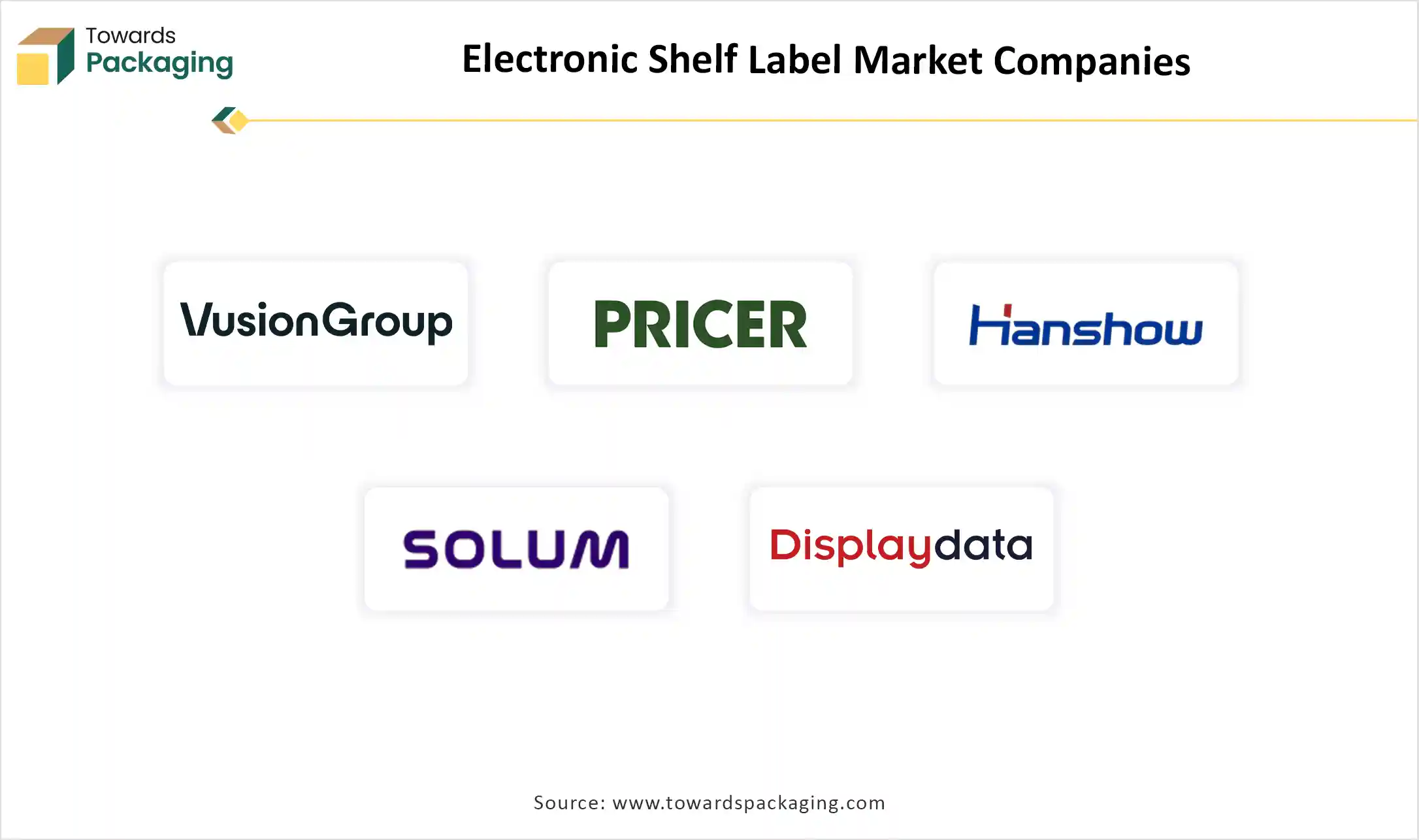

| Rank | Company Name | Headquarters | Country | Major Contribution to the Electronic Shelf Label Market | Key Packaging Products and Services |

| 1 | VusionGroup | Nanterre, France | France | The company offers low-power e-ink technology and integrates built-in LED indicators on the labels. The company deployed ESL in nearly 500 supermarkets in Morrisons. | ESL Hardware Series:- V700 Series, VSway Series, V300 Series, and V100 Series |

| 2 | Pricer | Stockholm, Sweden | Sweden | The company focuses on continuous ESL color innovation and offers optical wireless communication. The company provides next-generation displays. | SmartTAG HD & S, SmartTAG Color Family, and Pricer Avenue |

| 3 | Hanshow Technology Co. Ltd | Jiaxing, Zhejiang Province, China | China | The company focuses on developing ultra-durable ESL hardware and supports smart retail systems. | Nebular Pro Series, Polaris Pro Series, Nebular Series, and Stellar Pro Series |

| 4 | SOLUM | Yongin-si, Gyeonggi-do, Republic of South Korea | South Korea | The company collaborated with WHSmith to install ESL in the United Kingdom travel stores. The company offers solar-based shelf rails in collaboration with Epishine. | Newton Industrial & Special ESLs, Newton Pro, and Newton CORE & CORE |

| 5 | Displaydata Ltd. | Woodley, Reading, Berkshire, England, United Kingdom | United Kingdom | The company offers three-color ESLs and focuses on manufacturing dynamic cloud solutions. | Endcap & Island Displays, Aura 29, Chroma Aeon 16, Aura Aeon 42, Chroma Aeon 21 |

By Component

By Display Type

By Communication Technology

By Display Size

By Application

By End User

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarElectronic Shelf Label Market