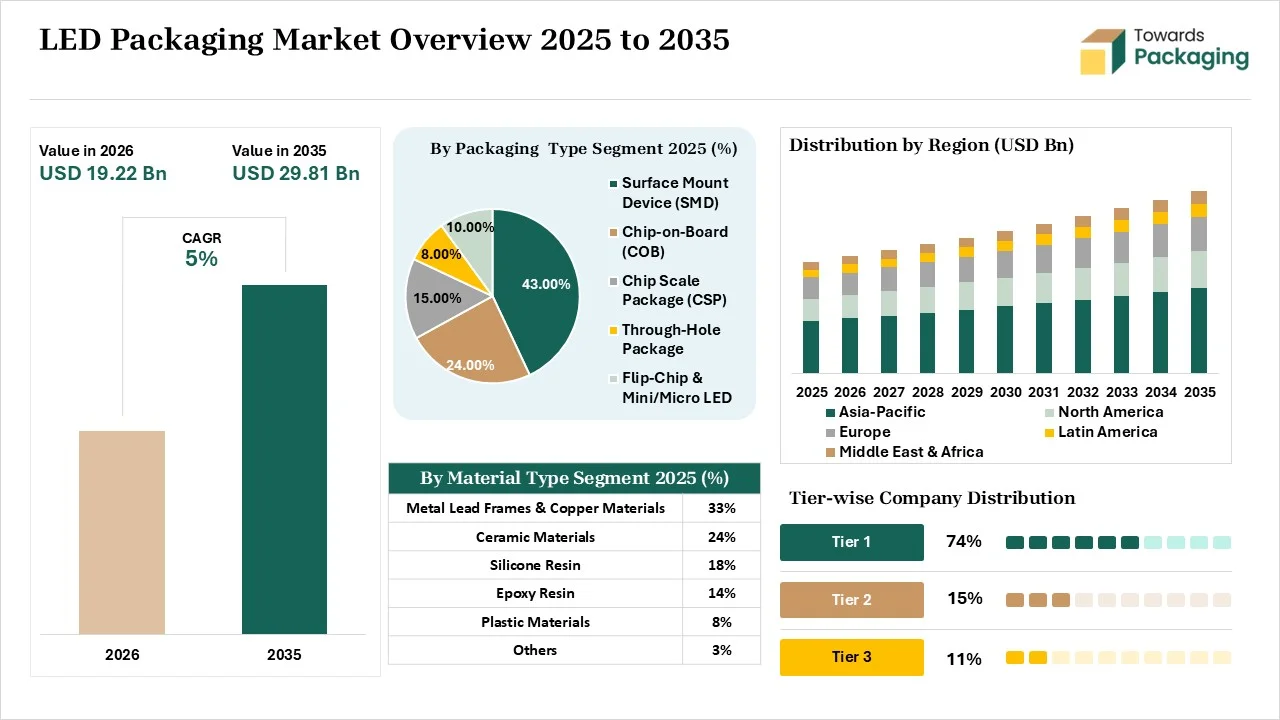

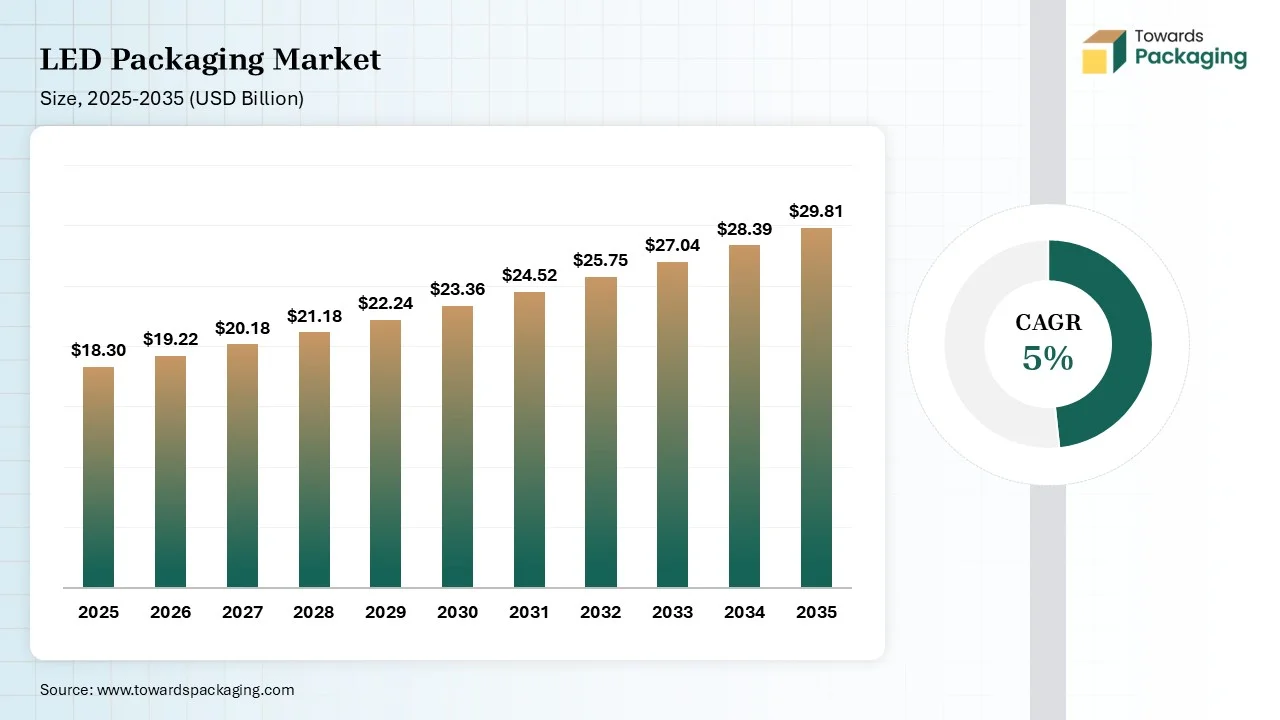

The LED packaging market is projected to grow from USD 19.22 billion in 2026 to USD 29.81 billion by 2035, registering a 5% CAGR during the forecast period. The report covers market size, growth forecasts, segment analysis, regional insights, competitive analysis, company profiles, manufacturers and suppliers, value chain analysis, import-export trade data, technological developments, and key market trends shaping the industry.

LED packaging is the integration of an LED chip onto a protected unit. The key components of packaging are the LED die, substrate, wire bonds, and encapsulant. The key functionalities are chip protection, heat dissipation, electrical connection, optical control, light extraction, and color conversion. Common technologies like COB, Dual In-line Package, and SMD are used. LED packaging offers benefits like environmental shielding, high-power support, improved visual experience, automated production, and better beam control. LED packaging is used across large screens, public lighting, interior automotive lighting, dental tools, LCD televisions, indicator lights, and many more.

For instance, In May 2026, Crystal Matrix Limited will develop an ATMP and compound semiconductor fabrication facility in Dholera, Gujarat. The facility focuses on developing mini/micro-LED display modules and mini-micro-LED GaN Epitaxy Wafers. The manufactured products are used in applications like commercial displays, smartphones, XR glasses, TVs, tablets, smart watches, and in-car displays.

The LED packaging market growth is driven by the miniaturization in electronics, automotive electrification, government regulations, expanding UV LED technology, rise in cross-licensing, growing regional electronics manufacturing hubs, display advancements, interest in IoT-connected lighting, rise in production automation, and the expansion of horticultural lighting.

The LED packaging market is undergoing technological developments like the integration of IoT in factory automation, simulation software, machine learning, miniaturization, algorithmic thermal management, and computer vision. Factors like optimizing chip design, compact form factors, and improved optical efficiency are drivers for the ongoing technological developments. The integration of AI is gaining traction in the market.

AI easily analyzes wire-bonding errors and develops advanced encapsulation materials. AI optimizes the architecture of LED packaging and analyzes performance metrics. AI helps in expediting production timelines and spots phosphor coating irregularities. AI easily tests thermal management structures of LED packaging and minimizes factory downtime. Overall, AI supports smart integration and accelerates the design of LED packaging.

The stage acquires raw materials like lead frames, bonding wires, LED chips, encapsulation materials, die attach adhesives, and lens materials.

Key Players:- ams-OSRAM AG, Samsung Electronics, Shin-Etsu Chemical, Ablestik, Sanan Optoelectronics, Nichia Corporation, Dow Chemical, Toray Industries

Material processing involves die attach, wire bonding, and encapsulation. Conversion includes phosphor application and wavelength shifting.

Design focuses on die attach, wire bonding, encapsulation, lens attachment, lead trimming, optical testing, binning, taping, and final inspection. Prototyping involves digital design, rapid fabrication, and validation testing.

The surface mount device (SMD) segment dominated the market with 43% share in 2025. The growing automated manufacturing in consumer electronics and the development of sleek general lighting fixtures increase the use of SMD. The production of compact lightbulbs and the rise in general residential lighting have increased the use of SMD. The adoption of high-power automotive headlights increases the use of SMD. The lightweight design, application versatility, superior color uniformity, and optimized heat dissipation of SMD drives the segment growth.

The chip scale package (CSP) segment held the 15% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% during the forecast period. The popularity of high-resolution displays and the focus on improving product yield increase the adoption of CSP. The heavy use of smart lighting systems and the creation of shorter interconnect distance increases use of CSP. The interest in energy-efficient general illumination increases CSP adoption. The enhanced optical flexibility, superior thermal management, and extreme miniaturization of CSP support the segment growth.

The metal lead frames & copper materials segment dominated the market with 33% share in 2025. The rising large-scale LED production and the burgeoning consumer electronics industry increase the use of metal lead frames & copper materials. The need for sturdy structural foundation and focus on cost-efficient manufacturing increases the adoption of metal lead frames & copper materials. The high electrical conductivity, exceptional heat dissipation, and the excellent mechanical stability of metal lead frames drive the segment growth.

The ceramic materials segment held the 24% market share in 2025 and is expected to grow at the fastest CAGR of 6.2% during the forecast period. The increased display manufacturing and the development of micro-LEDs increase the use of ceramic materials. The focus on preventing short circuits and the rise in complex component designs increase the use of ceramic materials. The optical efficiency and outstanding thermal management of ceramic materials help with expansion. The environmental stability, optical reliability, and dimensional stability of ceramic materials support the segment growth.

The general lighting segment dominated the market with 35% share in 2025. The growing bans on older lighting technologies and the rise in large-scale construction projects increase demand for general lighting, which requires LED packaging. The expanding public infrastructure and the focus on consuming less power increase the use of LED-based general lighting. The retrofitting activities in residential construction and the rise of automated offices drive the segment growth.

The automotive lighting segment held the 18% market share in 2025 and is expected to grow at the fastest CAGR of 6.8% during the forecast period. The growing ADAS integration and the consumer interest in luxury vehicles increase demand for LED-based automotive lighting. The focus on thermal management in the automotive ecosystem and the rising development of animated light signatures increase the use of automotive lighting. The expanding EV range and the interest in ultra-thin OLED technologies support the overall growth of the segment.

The chip-on-board (COB) segment dominated the market with 32% share in 2025. The increased manufacturing of high-power illumination and focus on homogenous lighting panels increases the use of COB technology. The focus on the reduction of assembly cost and the highly compact designs increases the use of COB technology. The uniform illumination, high lumen density, seamless light uniformity, and enhanced durability of COB drives the segment growth.

The flip-chip technology segment held the 18% market share in 2025 and is expected to grow at the fastest CAGR of 6.9% during the forecast period. The increased development of commercial displays and the innovations in lighting solutions increase the use of flip-chip technology. The demand for higher brightness and the extreme miniaturization of components increases the use of flip-chip technology. The high energy savings, higher efficiency, and excellent luminous efficacy of flip-flop technology support the segment growth.

The mid power (0.5W-1W) segment dominated the market with 38% share in 2025. The growing general lighting use in residential retrofits and the focus on even light distribution increase demand for mid power LED packaging. The rise in street lighting programs and the explosion of residential bulbs increase the use of mid power LED packaging. The easier thermal management, diffused illumination, uniformity, and excellent cost efficiency of mid power LED packaging drive the segment growth.

The high power (1W-3W) segment held the 27% market share in 2025 and is expected to grow at the fastest CAGR of 5.8% during the forecast period. The expansion of luxury cars and the advancements in wearables increase the use of high power LED packaging. The explosion of stadium lighting and the need for high-quality image capture have increased the adoption of high power LED packaging. The interest in adaptive matrix headlamps and the growing bans on incandescent bulbs increase the use of high power LED packaging. The advanced thermal management of high power LED packaging drives the segment growth.

The residential segment dominated the market with 33% share in 2025. The growing mercury lamp bans and the increased use of general lighting in homes increase the adoption of LED packaging. The burgeoning LED retrofitting in the residential sector helps with expansion. Household consumers focus on reducing utility bills, and the rise in replacing incandescent fixtures in houses increases the use of LED packaging. The smart home integration drives the segment growth.

The commercial segment held the 24% market share in 2025 and is expected to grow at the fastest CAGR of 5.5% during the forecast period. The replacement of older lighting in large office spaces increases demand for LED packaging. The focus on lowering the maintenance costs of commercial buildings and the integration of IoT-based lighting systems in retail spaces increases the adoption of LED packaging. The expansion of modern commercial architectures and the interest in connected lighting networks in commercial properties support the overall segment growth.

Asia Pacific dominated the market with a 47% share in 2025 and is expected to grow fastest at a 5.80% CAGR during the forecast period due to the high-volume manufacturing hub. The interest in compact packaging technologies and the rise in smart street lighting increase the use of LED packaging. The heavy investment in miniaturization and the rise in state-sponsored initiatives increase the adoption of LED packaging. The expanding next-generation displays and the strong industry-leading OEMs increase the adoption of LED packaging. The shift to energy-efficient lighting drives the market growth.

North America held the 20% market share in 2025. The government rebates credits, and the rise in smart building automation increases the use of LED packaging. The interest in adaptive headlights in the automotive industry and the adoption of high-end healthcare devices increase the use of LED packaging. The expansion of connected vehicle systems and the growing smart urban infrastructure increases the use of LED packaging. The interest in premium digital signage supports the market growth.

Europe held the 19% market share in 2025 due to the shift away from inefficient lighting. The growing intelligent mobility applications and the green building investments increase the adoption of LED packaging. The rise in public infrastructure retrofits and the expansion of interior vehicle displays increase the use of LED packaging. The eco-design mandates and the interest in chip-scale packages boost the market growth.

The growing streetlight retrofits and the rising automakers' investment in the advanced optical-electronic platforms increase the use of LED packaging.

The growing EV advancements and the focus on energy sobriety targets increase the use of LED packaging.

Latin America held the 7% market share in 2025. The preference for energy conservation and the growing smart infrastructure modernization increases the use of LED packaging. The presence of government subsidies and the growing lighting demand increases the use of LED packaging. The growing use of energy-efficient technology in the residential industry increases the adoption of LED packaging, boosting the market growth.

The Middle East & Africa held the 7% market share in 2025. The expansion of smart streetlight and the thriving next-generation displays increases the use of LED packaging. The growing off-grid integration and regulatory efficiency standards increase the adoption of LED packaging. The rise in smart infrastructure projects and the intelligent lighting budget support the market growth.

| Rank | Company | Headquarters | Country | Major Contribution to the LED Packaging Market | Key Packaging Products and Services |

| 1. | Nichia Corporation | Anan, Tokushima, Japan | Japan | The company offers 3-in-1 LED packaging and focuses on the sustainabLED initiative. The company expanded MicroLED production capacity. | Chip-on-Board, Direct Mountable Chip, Chip Scale Package, Multi-Chip & RGB Packages, Through-Hole LEDs |

| 2. | Samsung Electronics | Suwon, South Korea | South Korea | The company is a leading developer of chip-scale packages and focuses on providing advanced display packaging. The company focuses on Phosphor-on-Wafer innovation. | Chip-Scale Packaging, Mid-Power LED Packages, High-Power LED Packages, Chip-on-Board |

| 3. | Seoul Semiconductor Co., Ltd. | Ansan-si, Gyeonggi Province, South Korea | South Korea | The company developed products like Acrich, Violeds, SunLike LEDs, and nPola. The company focuses on supplying Mini LEDs for the production of automotive displays. | SunLike Series, Standard Mid/High-Power Packages, Filament LEDs Packaging, WICOP |

| 4. | Everlight Electronics Co., Ltd. | New Taipei City, Taiwan | Taiwan | The company has a high production capacity for LED packaging. The company focuses on automotive lighting innovations and sensor packaging. | High Power LEDs, SMD LEDs, LED Lamps |

| 5. | Epistar Corporation | Hsinchu City, Taiwan | Taiwan | The company is a major supplier of Flip-Chip packaging. The Ennostar company invested approximately US$122 million to expand the production capacity of Epistar company of 150mm micro-LED epitaxial wafers. | High-Voltage LEDs, Standard Surface Mount Devices, Mini LED Packaging, Micro LED Packaging |

By Packaging Type

By Material

By Application

By Technology

By Power Range

By End User

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarLED Packaging Market