Market Overview 2025 to 2035")

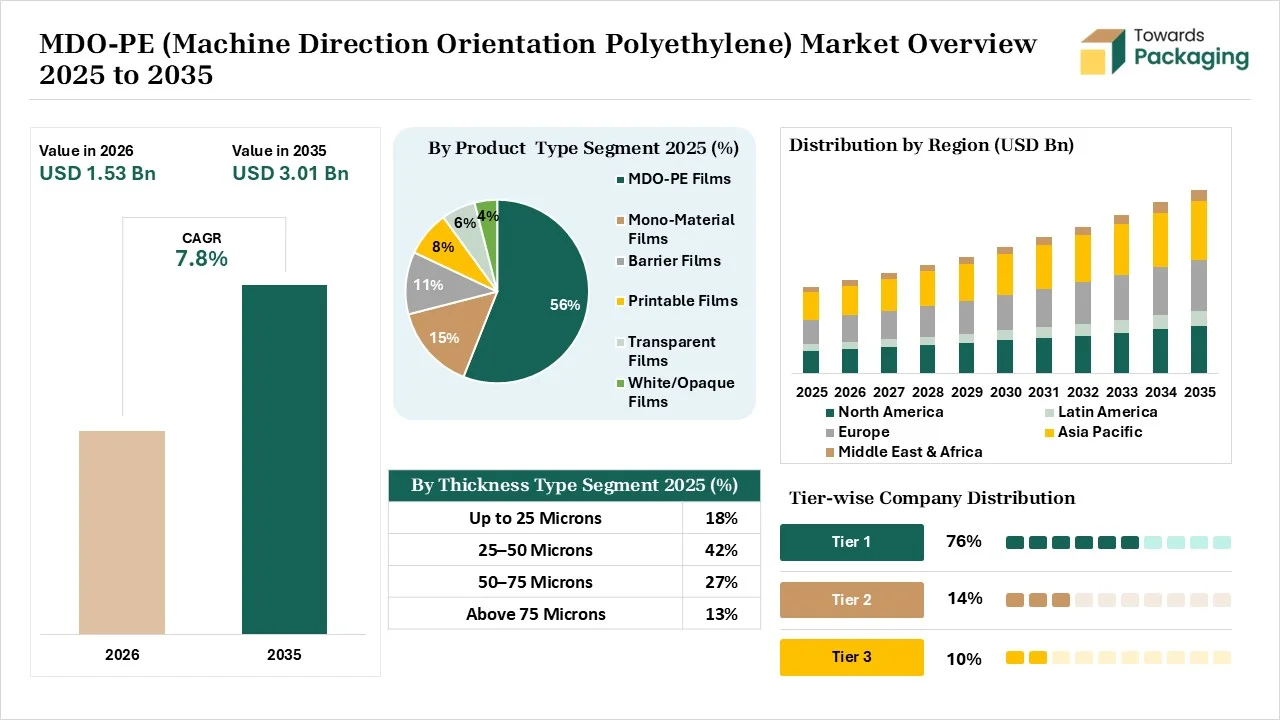

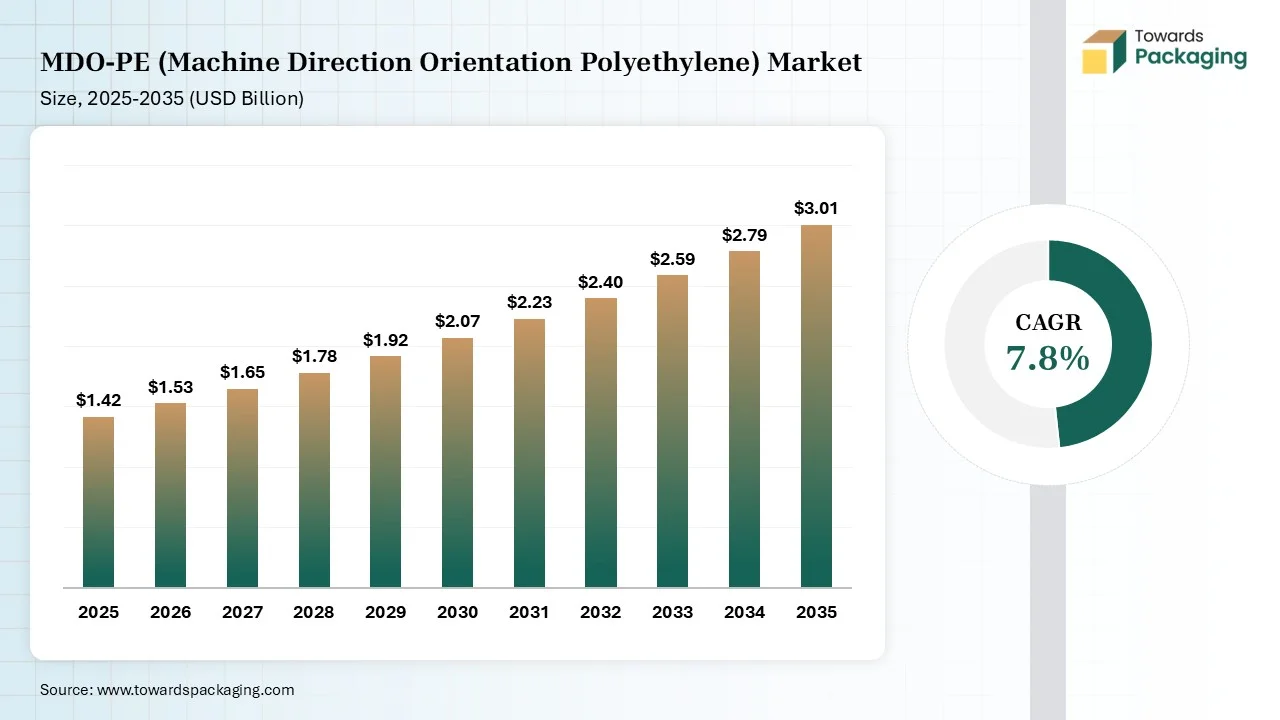

The MDO-PE (Machine Direction Orientation Polyethylene) market is projected to grow from USD 1.53 billion in 2026 to USD 3.01 billion by 2035, registering a CAGR of 7.8% during the forecast period. The report provides detailed market size and forecast analysis, segment-wise insights, regional performance, company profiles, competitive analysis, manufacturers and suppliers data, value chain analysis, import-export trade data, pricing trends, technological developments, sustainability initiatives, and key growth opportunities shaping the global market.

Market Size 2025 to 2035")

MDO-PE is a specialized PE film developed while heating in the machine direction. It is manufactured using steps like preheating, stretching, annealing, and cooling. The benefits of MDO-PE are cost savings, excellent printability, improved optics, material reduction, sustainability, improved optics, and excellent tear resistance. It has downgauging potential and offers 100% recyclability. MDO-PE is widely used in stand-up pouches, detergent pouches, collation shrink films, snack wrappers, and refill bags.

For instance, LG Chem collaborated with Reifenhauser to manufacture innovative MDO-PE films. The main aim of collaboration is downgauging MDO-PE films and optimizing production efficiency. The collaboration focuses on developing cost-effective solutions and uses cutting-edge extrusion technology.

The MDO-PE market growth is driven by the surging mono-material packaging, delivery boom, focus on excellent film properties, burgeoning healthcare industry, focus on improving heat resistance, regulations on traditional plastic use, thriving flexible packaging demand, expanding downgauging capabilities, and the surge in organized retail.

In July 2025, Constantia Flexibles invested 6.5 million euros in Hosokawa Alpine MDO technology at the Constantia Pirk site. The investment offers 12 rollers and supports improving film quality. The technology improves the stretched film homogeneity and manufactures EcoLamHighplus. The technology protects packaged products for a longer time and enhances optical properties.

The MDO-PE market is going through technological developments driven by demand for sustainability, intelligent operations, and material downgauging. Technological developments like digital twinning, smart automation, predictive maintenance, PLC integration, machine learning, and robotics are fueled by demand for optimized film stiffness and prevention of film tearing. The market’s major development is the incorporation of AI technology, which helps in enhancing barrier properties.

AI optimizes the stretching process and easily conducts virtual production. AI creates thinner films and lowers the scrap rates. AI predicts the prices of PE resins and develops polyolefin blends. AI analyzes the production line speeds and detects gauge bands. AI predicts the failures of the machine part and prevents the film from tearing. AI supports inline defect detection and prevents unscheduled shutdowns of the production lines.

The stage acquires feedstocks like HDPE, VLDPE, specialty resins, MDPE, and POP.

The material processing includes preheating, stretching, annealing, and cooling. The conversion includes coating, printing, lamination, and pouch making.

Design focuses on molecular alignment, layer formulation, down-gauging, and aesthetic additions. Prototyping focuses on simulations, lamination, testing, and recyclability goals.

The MDO-PE films segment dominated the market with 68% share in 2025. The growing personal care packaging and the shift to recyclable packaging materials increase the use of MDO-PE films. The brands' move away from non-recyclable substrates and the focus on shrinking raw material usage increase the adoption of MDO-PE films. The high penalties on multi-polymer packaging and the high volume of food packaging increase the adoption of MDO-PE films. The excellent mechanical enhancements and resource efficiency of MDO-PE films drive the segment growth.

The MDO-PE labels segment held the 11% market share in 2025 and is expected to grow at the fastest CAGR of 8.9% during the forecast period. The interest in no-label look and the focus on maintaining packaging durability increase the adoption of MDO-PE labels. The development of curved cosmetic bottles and the growing ESG pressures increase the use of MDO-PE labels. The rise in packaging, lightweighting, and expanding automated application lines increases the use of MDO-PE labels. The superior die-cutting performance and exceptional ink adhesion of MDO-PE labels support the segment growth.

The 25-50 microns segment dominated the market with 43% share in 2025. The focus on packaging lines' high performance and the expansion of all-PE pouches increases the use of 25-50 microns. The focus on aesthetic clarity of packaging and the sensitive food protection increases the adoption of 25-30 microns. The need to optimize material efficiency increases the adoption of 25-50 microns. The superior machinability, enhanced barrier properties, and perfect downgauging potential of 25-50 microns drive the segment growth.

The above 75 microns segment held the 11% market share in 2025 and is expected to grow at the fastest CAGR of 8.5% during the forecast period. The growing demand for heavy-duty packaging protection and the increased need for stronger films increase the use of films above 75 microns. Its compatibility with standard PE streams and seamless line conversion helps with expansion. The need for industrial packaging helps with growth. The exceptional machinability, lightweighting, superior tensile strength, complete recyclability, and excellent flexibility of above 75 microns support the segment growth.

The sequential orientation segment dominated the market with 44% share in 2025. The need to enhance packaging performance and the presence of high-speed printing lines increase the use of sequential orientation. The high mono-material circularity and the demand for thinner films increase the adoption of sequential orientation. The established processing expertise helps with the expansion. The high throughput, superior equipment versatility, and downgauging capability of sequential orientation drive the segment growth.

The offline orientation segment held the 13% market share in 2025 and is expected to grow at the fastest CAGR of 8.7% during the forecast period. The growing specific packaging needs and the interest in high-performance substrates increase the adoption of offline orientation. The focus on flexible production scheduling and the burgeoning specialty packaging market increases the adoption of offline orientation. The manufacturing of highly customized films increases the use of offline orientation. The superior precision, enhanced down gauging, and improved performance of offline orientation support the segment growth.

The HDPE-based MDO-PE segment dominated the market with 41% share in 2025. The global packaging regulations and the rise in manufacturing of stand-up packaging increase the adoption of HDPE-based MDO-PE. The growth in cost-efficient downgauging and the focus on enhancing film’s clarity increase the adoption of HDPE-based MDO-PE. The thriving recyclable packaging structures increase the use of HDPE-based MDO-PE. The excellent stiffness and the high dimensional stability of HDPE-based MDO-PE drive the segment growth.

The blended polyethylene grades segment held the 15% market share in 2025 and is expected to grow at the fastest CAGR of 8.9% during the forecast period. The creation of a perfect polymer microstructure and the demand for performance like traditional laminates increase the use of blended polyethylene. The high utilization of multi-material pouches and the growing detergent packaging increase the use of blended polyethylene grades. The growing gauge optimization and the focus on preventing film breakage increase the use of blended polyethylene grades. The customized performance and advanced formulations of blended polyethylene grades support the segment growth.

The pouches segment dominated the market with 34% share in 2025. The growing demand for easy-to-recycle packaging and the focus on packaging puncture resistance increase the use of MDO-PE pouches. The rise in direct PET replacement and the high production efficiency increase the production of MDO-PE pouches. The expanding frozen food brands and the focus on saving material cost increase the MDO-PE pouches development. The brand convenience, superior strength, and high sealability of MDO-PE pouches drive the segment growth.

The labels segment held the 8% market share in 2025 and is expected to grow at the fastest CAGR of 9% during the forecast period. The rising creation of single-family packages and the focus on cutting transportation costs increase the adoption of MDO-PE labels. The rising demand for flawless finishes and the high-performance durability in the home care industry increases the adoption of MDO-PE labels. The high-quality aesthetic packaging demand and the growing label recycling issues increase the adoption of MDO-PE labels, supporting the segment growth.

The food & beverage segment dominated the market with 49% share in 2025. The rise in perishable beverages and the expansion of flexible food packaging formats increase the use of MDO-PE. The focus on enhancing the transparency of food on retail shelves and the cost-saving demand in the F&B industry increases the adoption of MDO-PE. The interest in snack pouches and the thriving beverage packaging increases the use of MDO-PE. The need for superior barriers in the dairy industry and the expanding use of food stand-up bags drive the segment growth.

The e-commerce & logistics segment held the 7% market share in 2025 and is expected to grow at the fastest CAGR of 9.2% during the forecast period. The need for extended transit protection and the rise in hyperlocal logistics increase the use of MDO-PE. The exploding D2C shipments and the burgeoning e-commerce logistics increase the adoption of MDO-PE. The high-scale e-commerce deliveries and focus on last-mile handling increase the adoption of MDO-PE. The growing e-commerce automation and demand for lightweight solutions support segment growth.

The flexible packaging segment dominated the market with 54% share in 2025. The changing habits of consumers and the demand for BOPP-like performance increase the adoption of MDO-PE flexible packaging. The focus on protecting packaging functional performance and the rising use of flat pouches increase the adoption of MDO-PE flexible packaging. The expanding bag formats and the rising packaging of pharmaceutical products increase the adoption of MDO-PE flexible packaging. The superior aesthetics of flexible packaging drive the segment growth.

The specialty applications segment held the 5% market share in 2025 and is expected to grow at the fastest CAGR of 9.1% during the forecast period. The focus on protecting items like coffee and the need to enhance the shelf presence of premium products increases the use of MDO-PE. The exploding personal care brands and the growing consumer interest in lightweight travel pouches increase the use of MDO-PE. The thriving modern D2C shipping and the growing digital printing technologies increase the use of MDO-PE. The expanding advanced applications support the segment growth.

The direct sales segment dominated the market with 46% share in 2025. The growing demand for work hand-in-hand and the rise in massive volume commitments increase the adoption of direct sales. The focus on ensuring stable prices and the higher demand for immediate engineering support increase the adoption of direct sales. The need for direct consultations and on-site troubleshooting increases the use of direct sales. The reliable delivery in direct sales drives the segment growth.

The online procurement platforms segment held the 6% market share in 2025 and is expected to grow at the fastest CAGR of 10.2% during the forecast period. The focus on monitoring certifications and the rise in integration of ESG metrics increases the use of online procurement platforms. The demand for instant vendor access and the focus on simple digital processes increase the use of online procurement platforms. The need to mitigate market volatility and expand medium-sized enterprises increases the use of online procurement platforms. The exceptional operational efficiency of online platforms supports the segment growth.

Asia Pacific dominated the market with 34% share in 2025 and is expected to grow at the fastest CAGR of 9.1% during the forecast period. The rise in RTE food delivery and the strong presence of film converters increase the demand for MDO-PE. The brand's focus on meeting recycling guidelines and the high pharmaceutical consumption increases the use of MDO-PE. The expansion of modern supermarket chains and the well-developed flexible packaging hubs increases the use of MDO-PE. The focus on protecting perishables and the shift away from multi-material laminates increase the use of MDO-PE, driving the market growth.

Europe held the 29% market share in 2025. Europe's focus on lowering plastic waste and the development of mono-PE structures increases the adoption of MDO-PE. The focus on maintaining packaging’s protective qualities and the interest in green alternatives increase the adoption of MDO-PE. The rise in home deliveries and the expansion of flexible food packaging increase the adoption of MDO-PE. The shifting away from traditional packaging drives the market growth.

North America held the 24% market share in 2025. The regional brands focus on meeting eco-friendly goals, and the higher demand for polyethylene mailers increases the use of MDO-PE. The rise of food packaging and the robust recyclability policies increases the use of MDO-PE. The growing demand for convenience products and the CPG companies' commitment towards sustainable packaging increase the adoption of MDO-PE, supporting the market growth.

Latin America held the 7% market share in 2025. The growing middle-class incomes and the heavy consumption of home care products increase the adoption of MDO-PE. The expansion of eco-conscious brands and the burgeoning packaging modernization increases the adoption of MDO-PE. The exploding processed beverages industry and the focus on shortening packaging lead times increase the use of MDO-PE, boosting the overall market growth.

The Middle East & Africa held the 6% market share in 2025. The availability of cost-effective resin and the interest in modern retail increase the use of MDO-PE. The focus on replacing multi-layer plastics and the focus on reducing imported packaging increase the adoption of MDO-PE. The growing medical distribution and the high demand for medical-grade films increase the adoption of MDO-PE, supporting the overall market growth.

| Rank | Company | Headquarters | Country | Major Contribution to MDO-PE (Machine Direction Orientation Polyethylene) Market | Key Packaging Products and Services |

| 1 | Dow | Midland, Michigan, United States | United States | The company develops mono-material matte MDO-PE pouches and has invested in expanding the MDO unit in the Pack Studios. | ELITE AT 6900 Polyethylene Resin, REVOLOOP Recycled Plastic Resins, INNATE Precision Packaging Resins, AFFINITY Polyolefin Plastomers |

| 2 | Borealis AG | Vienna, Austria | Austria | The company manufactures full PE laminate solutions and focuses on using recycled content in packaging solutions. | BorShape FX1001, BorShape FX1002, BorShape FX1003, Borstar FB5560 |

| 3 | Nowofol | Siegsdorf, Bavaria, Germany | Germany | The company manufactures mono-material packaging solutions and has heavily invested in sustainable product development. | NOWOSTRAIGHT, NOWOLABEL, NOWOPAQUE, NOVOCARRY |

| 4 | ExxonMobi | Spring, Texas | Texas | The company focuses on the development of cheese packaging, freezer pouches, and barrier packaging. | Exceed Stiff+, Exceed Flow+, Vistamaxx, Exceed HD/ ExxonMobil HDPE, Exxtra Seal |

| 5 | NOVA Chemicals Corporation | Calgary, Alberta, Canada | Canada | The company focuses on MDO-HDPE resin development and manufacturing MDO-LLDPE solutions. | ASTUTE Plastomers, MDO-HDPE Films, MDO-LLDPE Films |

Market Companies")

By Product Type

By Thickness

By Manufacturing Technology

By Resin Type

By Packaging Format

By End-Use Industry

By Application

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarMDO-PE (Machine Direction Orientation Polyethylene) Market