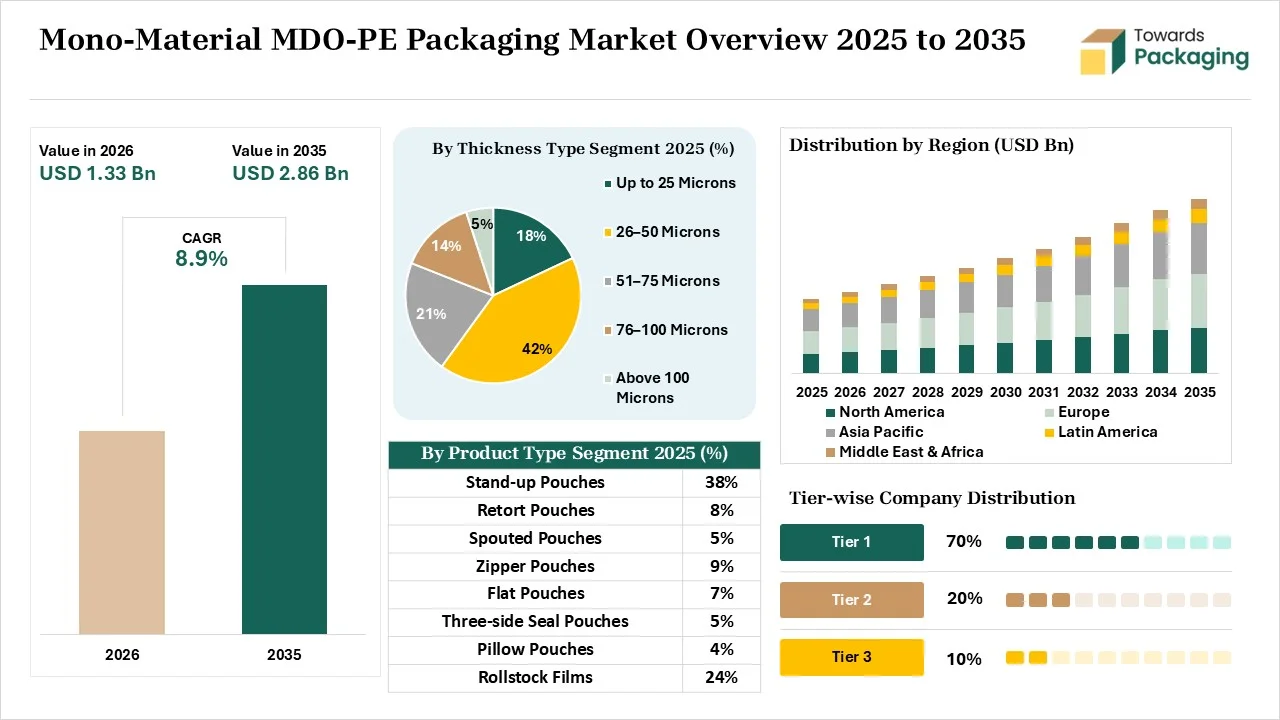

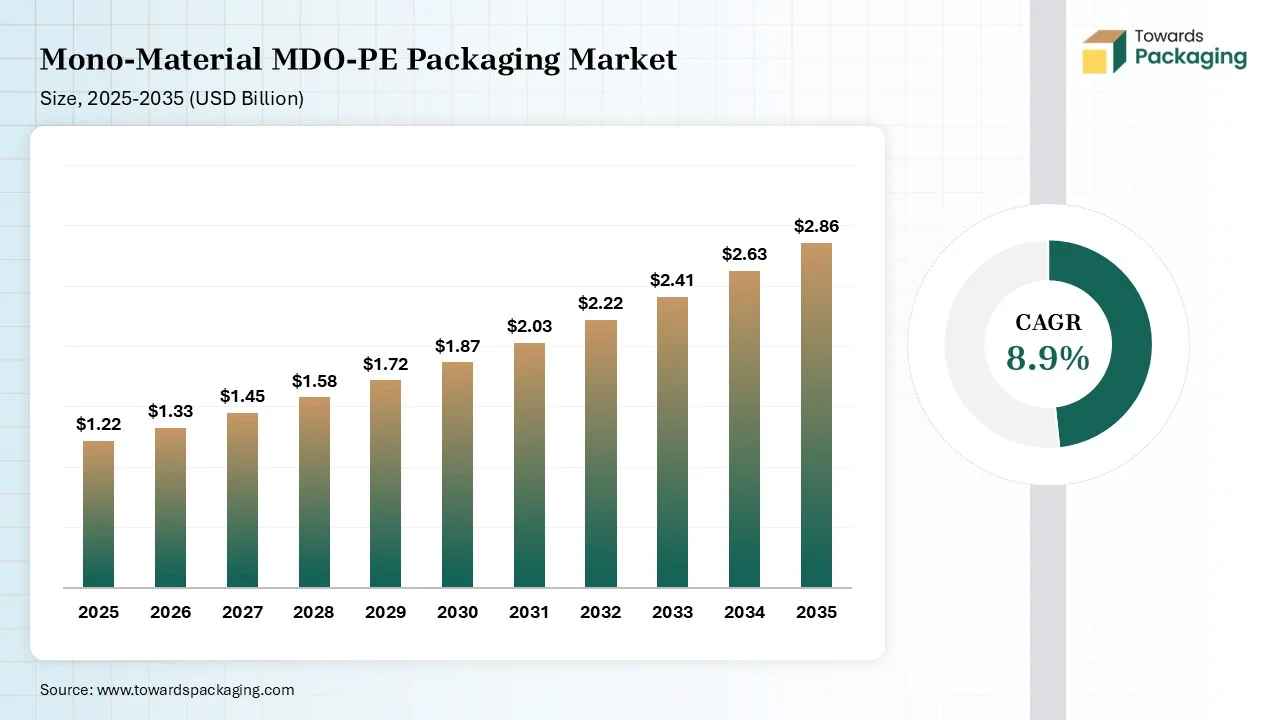

The mono-material MDO-PE packaging market is projected to grow from USD 1.33 billion in 2026 to USD 2.86 billion by 2035, registering a CAGR of 8.9% during 2026–2035. The report covers market size, share, growth trends, segmentation by product type, application, end-use industry, and region, along with detailed regional analysis, competitive landscape, company profiles, manufacturers and suppliers, value chain analysis, trade statistics, pricing trends, demand-supply analysis, and emerging market opportunities shaping the industry.

Mono-material MDO-PE packaging is a type of sustainable flexible packaging developed fully from a single polymer material. The major features are high barrier protection, lightweight, high shock absorption, full recyclability, and superior optics. The mono-material MDO-PE packaging offers benefits like material reduction, excellent printability, and ambitious sustainability. The manufacturing includes film extrusion, machine direction orientation, lamination, and printing. Mono-material MDO-PE packaging is widely used in frozen foods, dry pet food, wet wipes, personal hygiene items, confectionery, pet treats, liquid detergents, and medical packaging.

The mono-material MDO-PE packaging market growth is driven by corporate environment pledges, innovations in downgauging, exploding flexible packaging options, logistical efficiency needs, convenience food growth, pressures on the packaging sectors, burgeoning single polymer packaging, advancements in high-barrier films, and the demand for improved packaging printability.

In July 2025, Hosokawa Alpine MDO technology received an investment of 6.5 million euros from Constantia Flexibles. The technology installed at Constantia Pirk Site and the helps in enhancing film quality. The new investment provides a total of 12 rollers and supports the development of EcoLamHighplus. The investment focuses on expanding Constantia Flexibles' range of services.

The mono-material MDO-PE packaging market is undergoing technological developments like digital twin simulations, structural design software, smart manufacturing, virtual commissioning, and polymer simulation. The technological developments help in predictive polymer modelling, replacing laminates, and digital simulations. The AI incorporation is the major technological shift in the market, which helps in line control.

AI predicts the seal strength of mono-material MDO-PE packaging and identifies flaws in packaging. AI predicts the pressure on production lines and supports automated sorting. AI lowers the requirement for trial-and-error and automatically adjusts roller speeds. AI spots uneven stretches and supports material simulation. Overall, AI supports process control and lifecycle analysis.

Raw materials like base PE resins, barrier materials, sealant films, and additives are required.

Material processing includes steps like extrusion, preheating, stretching, annealing, and cooling. Conversion includes printing, lamination, and bagging.

Design focuses on structural design, barrier strategies, closures, and printing. Prototyping focuses on lab-scale extrusion, pouch conversion, and recyclability certifications.

The stand-up pouches segment dominated the market with 38% share in 2025. The transition away from rigid containers and the growing liquid storage increases the adoption of stand-up pouches. The need for packaging with enhanced mechanical properties and the focus on lowering the flopping over of pouches increase the adoption of stand-up pouches. The optimized shipping capacity, high stiffness, and enhanced convenience of stand-up pouches drive the segment growth.

The rollstock films segment held the 24% market share in 2025 and is expected to grow at the fastest CAGR of 9.8% during the forecast period. The rise in high-speed rollstock printing and expanded automated packaging increases the adoption of rollstock films. The surging downgauging initiatives and the shift away from print-web films increase the adoption of rollstock films. The rise in FFS lines and the development of premium aesthetics increase the use of rollstock films. The high printing capability, unmatched recyclability, and perfect runnability of rollstock films support the segment growth.

The 26-50 microns segment dominated the market with 42% share in 2025. The interest in heavy-duty wraps and the rise in high-speed conversion increase the adoption of 26-50 microns. The focus on limiting the consumption of resin and the explosion of standard flexible packaging increases the adoption of 26-50 microns. The need to lower plastic volume and the burgeoning of material waste optimization increase the adoption of 26-50 microns. The optimal mechanical strength and superior machinability of 26-50 microns drive the segment growth.

The above 100 microns segment held the 5% market share in 2025 and is expected to grow at the fastest CAGR of 9.7% during the forecast period. The rise in the development of a strong pouch and the expansion of large-format pet food pouches increases the adoption of those above 100 microns. The rise in packaging of sensitive medications and the growing logistics requirements increase the adoption of above 100 microns. The growth in high-speed packaging lines helps with expansion. The superior barrier protection and enhanced packaging durability of above 100 microns support the segment growth.

The medium barrier segment dominated the market with 34% share in 2025. The rising frozen food packaging and the focus on avoiding premium costs increase the adoption of medium barrier. The need to preserve dry goods and the demand for increasing product freshness increase the use of a medium barrier. The rise in packaging of dry goods and the burgeoning daily consumption of goods increases the use of medium barrier. The medium barrier format's compatibility with existing recycling streams drives the segment growth.

The ultra-high barrier segment held the 17% market share in 2025 and is expected to grow at the fastest CAGR of 10.4% during the forecast period. The focus on preserving packaging recyclability and the focus on saving raw materials increase the adoption of ultra-high barrier packaging. The heavy meat consumption and the brand's focus on lowering film thickness increase the use of ultra-high barrier. The need for advanced preservation and expanding sensitive items increases the use of ultra-high barrier packaging. The growing use of tamper-evident packaging in diverse industrial applications supports the segment growth.

The machine direction orientation (MDO) segment dominated the market with 41% share in 2025 and is expected to grow at the fastest CAGR of 10.1% during the forecast period. The expansion of stand-up pouches and the focus on maintaining packaging integrity increase the adoption of MDO. The focus on enhancing PE gloss and the smooth working of converting lines increases the adoption of MDO. The premium graphics printing and the strategies for mono-material replacements increase the adoption of MDO. The improved stiffness, optical clarity, and enhanced puncture resistance of MDO drive the segment growth.

The blown film extrusion segment held the 22% market share in 2025. The manufacturing of customized packaging layer designs and the focus on staying economically competitive increase the use of blown film extrusion. The focus on easy reprocessing of packaging and the need to enhance the tensile strength of packaging increase the adoption of blown film extrusion. The exploding industrial packaging uses blown film extrusion. The improved film durability and enhanced strength of blown film extrusion support the segment growth.

The flexible packaging segment dominated the market with 87% share in 2025 and is expected to grow at the fastest CAGR of 9.2% during the forecast period. The increased development of packaging from a single polymer family and the rising use of high-speed machinery are increasing the development of flexible packaging. The need for a rigid print layer alternative and the established sealing process increases the use of flexible packaging. The growing pressures on brands and the rising number of household goods companies increase the use of flexible packaging. The low transportation cost of flexible formats drives the segment growth.

The semi-rigid packaging segment held the 13% market share in 2025. The well-developed PE recycling ecosystem and the focus on maintaining structural integrity increase the use of semi-rigid packaging. The storing of complex food items and the high penalty on mixed polymers increase the use of semi-rigid packaging. The need for flat-bottom shaping in packaging helps with expansion. The thriving packaging versatility and the rising specialty applications support the segment growth.

The food & beverages segment dominated the market with 56% share in 2025. The focus on keeping dairy products fresh and the massive global F&B brands increases the use of mono-material MDO-PE packaging. The expansion of RTE aisles and the rising wrapper demand increase the adoption of mono-material MDO-PE packaging. The food waste reduction demand and the excellent shelf-life requirements in F&B increase the use of mono-material MDO-PE packaging. The frozen food premiumization drives the segment growth.

The healthcare & pharmaceuticals segment held the 8% market share in 2025 and is expected to grow at the fastest CAGR of 10.2% during the forecast period. The stricter medical standards and the pharmaceutical device protection increase the use of mono-material MDO-PE packaging. The high interest in heat-sealable closures and the manufacturing of medical device pouches increases the use of mono-material MDO-PE packaging. The expanded sensitive drug infrastructure and thriving medical-grade pouches support the overall growth of the segment.

The direct sales segment dominated the market with 44% share in 2025. The complex research & development, and the management of packaging specifications, increase the adoption of direct sales. The brand's focus on guaranteed compliance and quality assurance increases the adoption of direct sales. The specific products' demand and the high-volume contracts increase the use of direct sales. The technical collaboration availability in direct sales drives the segment growth.

The e-commerce procurement segment held the 8% market share in 2025 and is expected to grow at the fastest CAGR of 11.4% during the forecast period. The focus on streamlining inventory and the demand for exceptional logistics performance increase the use of e-commerce procurement. The corporate environmental mandates and the modernized online shopping increase the adoption of e-commerce procurement. The increased transparency of purchasing and the minimization of void-fill increase the use of e-commerce procurement. The simplified procurement process supports the segment growth.

Europe dominated the market with a 31% share in 2025. The growing redesigning of packaging in many consumer brands and the strong mechanical recycling systems increase the adoption of mono-material MDO-PE packaging. The increased replacement of conventional laminates and the EPR tariffs increase the use of mono-material MDO-PE packaging. The technologically advanced sorting infrastructure and the pharma companies' commitments towards mono-material packaging drive the overall market growth.

Asia Pacific held the 29% share in 2025 and is expected to grow at the fastest CAGR of 10.2% during the forecast period. The implementation of EPR policies across the APAC countries and the demand for superior performance packaging increase the adoption of mono-material MDO-PE packaging. The skyrocketed demand for e-commerce goods and regulatory crackdowns increases the adoption of mono-material MDO packaging. The massive production base of mono-material MDO packaging helps with expansion. The explosion of smart packaging supports the market growth.

North America held the 27% market share in 2025. The Plastic Pact initiatives across North American countries and the growing medical device packaging increase the adoption of mono-material MDO-PE packaging. The strong infrastructure of multinational packaging converters and the growth in packaging re-engineering increase the adoption of mono-material MDO-PE packaging. The growing demand for high-barrier quality packaging supports the market growth.

Latin America held the 7% market share in 2025. The focus on recycled-content quotas in the Latin American countries and the rise in the updation of labeling increase the demand for mono-material MDO-PE packaging. The growing demand for metallized foil alternatives and the burgeoning online retail increases the use of mono-material MDO-PE packaging. The growing demand for frozen items supports the market growth.

The Middle East & Africa held the 6% market share in 2025. The high pressure on the export market and the abundance of regional feedstocks increase the adoption of mono-material MDO-PE packaging. The growth in modern retail networks and the need for crystal-clear transparency in packaging increase the use of mono-material MDO-PE packaging. The advancements in film technology and local sustainability initiatives support the market growth.

| Rank | Company | Headquarters | Country | Major Contribution to Mono-material MDO-PE Packaging Market | Key Packaging Products and Services |

| 1 | Mondi Group | Weybridge, England, United Kingdom | United Kingdom | The company offers medium-to-high barrier protection and offers MDO PE-based triplex laminates. The company collaborates with Pet Food brands to provide MDO-PE packaging. | Re/cycle FlexiBag, Mono-material StandUpPouch, Retortable mono-material Pouch, Re/loop FlexiBag Reinforced |

| 2 | Berry Global | Evansville, Indiana | Indiana | The company focuses on expanding mono-material PE pouches production in the United States. The company focuses on increasing recyclability and sustainable collaborations. | Entour Bold, Omni Xtra, Entour Shield, Clarity Guard |

| 3 | Sonoco | South Carolina, 29550, USA | United States | The company manufactures mono-material PE structures and offers the EnviroFlex PE portfolio. The company offers the EnviroSense Initiative. | EnviroFlex PE Bags, EnviroFlex PE Permade Pouches & Rollstock, EnviroFlex PE Flow Wrap |

| 4 | UFlex Limited | Noida, Uttar Pradesh, India | India | The company develops high-purity barrier films and manufactures large-format MDO-PE bags. | Heavy-Duty Export Pouches, Reclosable Pouch Formats, Sustainable Tube Packaging |

| 5 | Amcor | Zurich, Switzerland | Switzerland | The company expanded its high-barrier films production capacity in Italy. The company offers MDO-PE solutions to pharmaceutical applications and focuses on AmPrima Scaling. | AmPrima PE Plus, Amcor HealthCare Recycle-Ready Medical Laminates, Stand-up Pouches, AmPrima Forming Films |

By Product Type

By Thickness

By Barrier Type

By Processing Technology

By Packaging Format

By End-use Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarMono-Material MDO-PE Packaging Market