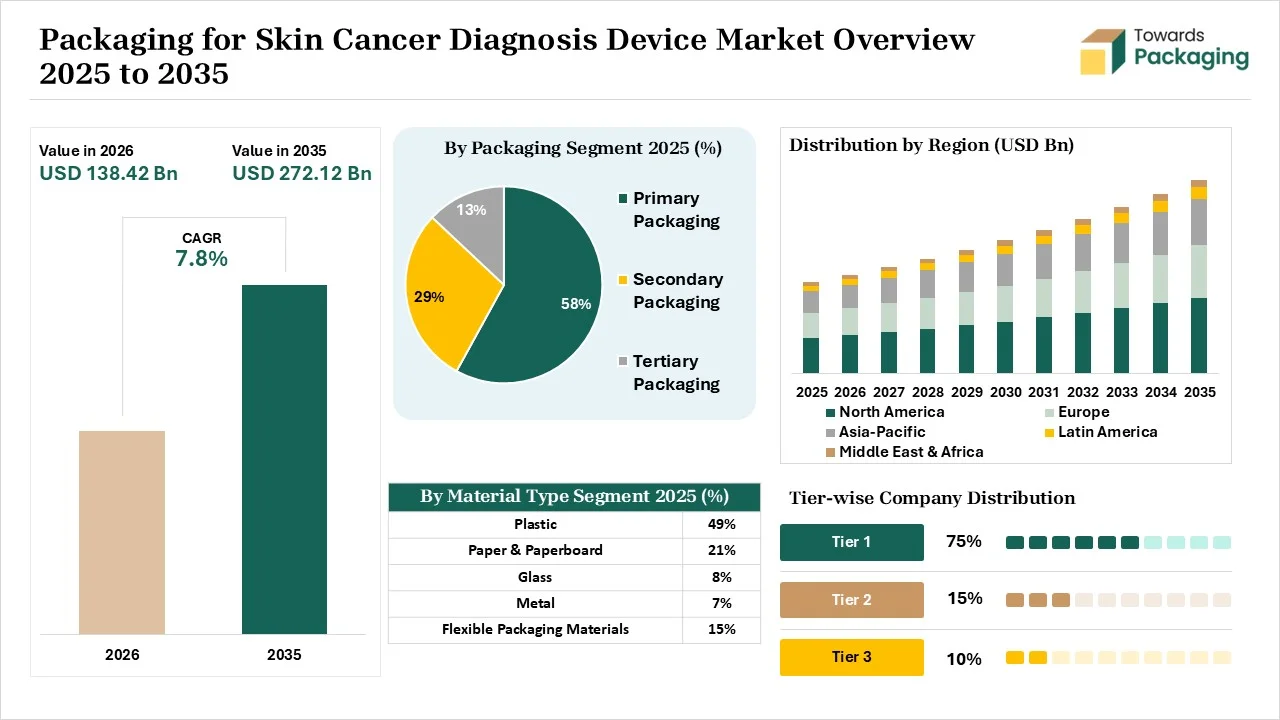

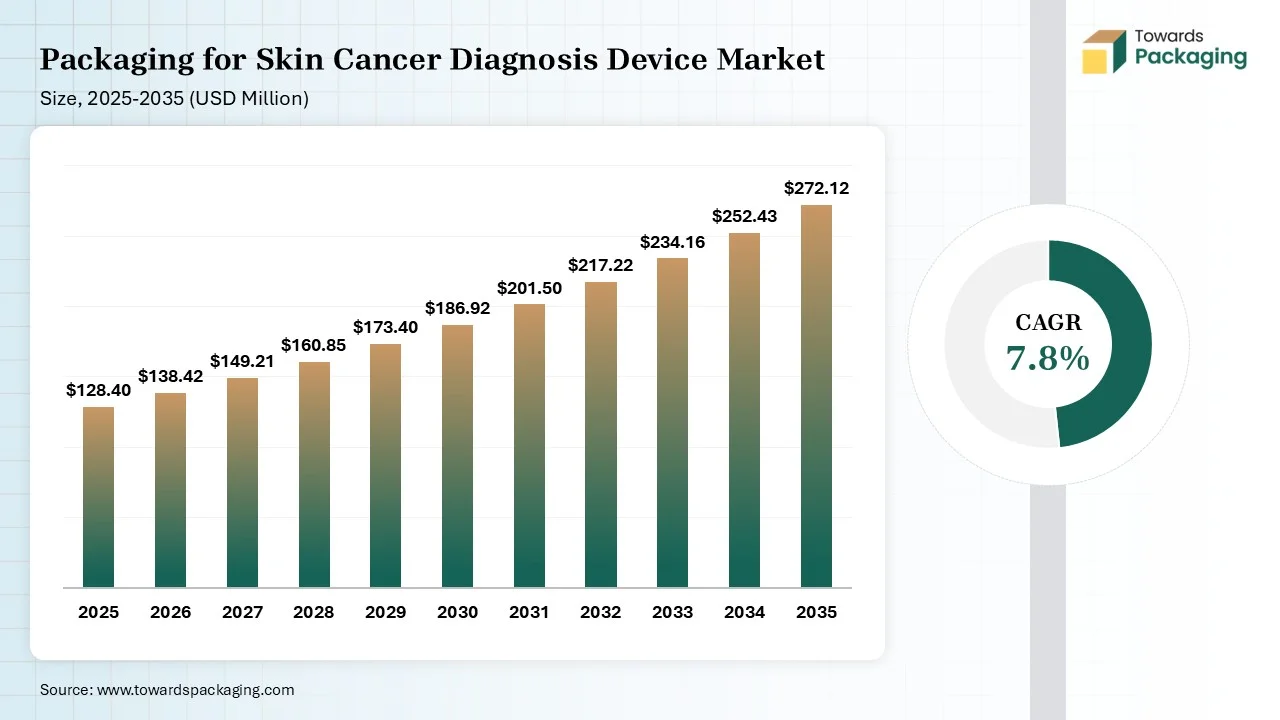

The Packaging for Skin Cancer Diagnosis Device Market is projected to grow from USD 138.42 million in 2026 to USD 272.12 million by 2035, registering a CAGR of 7.8% during the forecast period. This report provides detailed market size forecasts, segment-wise analysis by packaging type, material, application, and end user, regional and country-level insights, company profiles, competitive landscape, value chain assessment, import-export (trade) analysis, manufacturers and suppliers data, pricing trends, regulatory overview, and key market developments. It also highlights how the increasing prevalence of skin cancer, rising adoption of AI-enabled dermatoscopes, and growing use of UDI-compliant packaging solutions are supporting market growth.

Packaging for skin cancer diagnosis device is a specialized physical enclosure developed to protect various skin cancer diagnostic tools during storage and transportation. The key components are tamper-evident materials, shock-absorption materials, recyclable design, and regulatory labeling. The packaging offers benefits like hardware protection, reassurance, traceability, environmental shielding, supply chain efficiency, and ease of use. The packaging formats, like clinic-ready desktop packaging, sliding rigid packs, and bespoke carry packs, are used for the packaging of skin cancer diagnosis devices. Devices like dermatoscopes, confocal microscopes, AI-powered spectroscopy devices, and digital total body photography systems are used for screening skin cancer. The packaging provides excellent device protection and an enhanced at-home testing experience.

The packaging for skin cancer diagnosis device market growth is driven by the worldwide increase in non-melanoma, expansion of non-invasive techniques, rise in teledermatology, growing use of handheld devices, favorable insurance coverage, machine learning integration, innovations in the imaging modalities, rise in annual skin screenings, growth in genomic assays, and sterile packaging innovations.

The packaging for skin cancer diagnosis device market is going through technological developments due to the demand for smart delivery systems and user-friendly handling. Developments like cloud connectivity, AI-based diagnostics, wearable biosensors, machine learning, and 3D imaging help in providing portability, early detection, and tracking individual moles. The major development in the market is smartphone diagnostics, which accelerates the speed of image analysis.

Smartphone diagnostics offers affordable self-screening of skin cancer and provides a remote review of the patient's condition, which creates demand for a portable diagnosis device. The smartphone diagnostics provide patient empowerment and algorithmic analysis. The rising use of pocket-sized dermatoscopes and sensor integration in packaging increases demand for packaging for skin cancer diagnosis devices. The growing teledermatology packaging and cost-effective scalability help with expansion. Overall, increased accessibility and instant AI processing in smartphone diagnostics drive the market growth.

Raw materials like medical-grade paper, HDPE, foil laminated films, cross-linked PE films, DuPont Tyvek, PETG, corrugated cardboard, medical-grade films, and foam inserts are required.

Material processing includes cleanroom manufacturing, sterilization compatibility, integrity validation, and environmental simulation. Conversion includes precision rotary die-cutting, multi-layer laminating, and slitting.

Design focuses on the tamper evidence, mechanical protection, and intuitive unboxing. Prototyping includes concept development, F3 testing, and transit simulation.

Logistics focuses on temperature control, real-time monitoring, and chain of custody. Distribution focuses on distribution testing, ISO 11607 compliance, regulatory controls, and labeling.

The primary packaging segment dominated the packaging for skin cancer diagnosis device market with 58% share in 2025. The demand for bio-burden control and the integration of sensitive optics in packaging increases the adoption of primary packaging. The protection of the diagnostic device from extreme temperatures and the innovations in medical-grade plastics increase the use of primary packaging. The stringent tracing demand in the diagnostic industry and the focus on preventing infection increase the use of primary packaging. The device protection and sterile barrier maintenance of primary packaging drives the segment growth.

The secondary packaging segment held the 29% market share in 2025. The rise in focus on medical device authentication and the demand for protective barriers during transit increases the use of secondary packaging. The incorporation of track-and-trace labels and the need for highly printable packaging increase the use of secondary packaging. The demand for Unique Device Identification and the expansion of delicate diagnostic instruments increase the use of secondary packaging. The expansion of tamper-evident secondary boxes and the rising transportation of clinical kits support the overall segment growth.

The tertiary packaging segment held the 13% market share in 2025 and is expected to grow at the fastest CAGR of 8.4% during the forecast period. The growing exports of molecular testing kits and the focus on monitoring temperature during logistics increase the use of tertiary packaging. The expansion of decentralized testing and the growth in global kit consolidations increase the use of tertiary packaging. The thriving blockchain-ready parcel labels and the higher focus on supply chain security increase the use of tertiary packaging. The rise in last-mile hospital delivery supports the overall segment growth.

The plastic segment dominated the packaging for skin cancer diagnosis device market with 49% share in 2025. The demand for a highly effective barrier in a diagnostic device and mass production capabilities increases the use of plastics. The growing development of rigid clamshells and the need to safeguard device integrity increase the adoption of plastic. The increased creation of sterile barriers and the popularity of tamper-evident seals increase the use of plastic. The high visibility, design versatility, and low manufacturing cost of plastic drives the segment growth.

The paper & paperboard segment held the 21% market share in 2025. The expansion of group purchasing organizations and the popularity of primary sterile packaging increase the adoption of paper & paperboard. The development of sterilization wraps and the serialization laws in medical devices increases the use of paper & paperboard. The increased replacement of legacy plastics and the need for volume reduction increase the use of paper & paperboard. The explosion of digital printing and the tracking mandates increases the use of paper & paperboard, boosting the overall segment growth.

The flexible packaging materials segment held the 15% market share in 2025 and is expected to grow at the fastest CAGR of 8.8% during the forecast period. The protection of sensitive diagnostic tools and the focus on lowering the physical shifting of devices increase the use of flexible packaging materials. The focus on minimizing shipping weight and the advanced seal integration increases the adoption of flexible packaging materials. The popularity of digital authentication and the thriving skin cancer detection base increases the use of flexible packaging materials. The customizability and high moisture protection in flexible packaging materials support the segment growth.

The glass segment held the 8% market share in 2025. The need for superb optical transmission and the dermatologists' demand for deeper illumination penetration increase the adoption of glass. The popularity of non-reactive primary packaging and the net-zero goals in national healthcare systems increases the use of glass. The explosion of in vitro diagnostics and the rising use of laser components increases the use of glass. The smart packaging capabilities, chemical inertness, true color rendering, and zero-gas permeability of glass support the overall segment growth.

The dermatoscopes segment dominated the packaging for skin cancer diagnosis device market with 26% share in 2025. The demand for accuracy in melanoma detection and the rise in non-invasive procedures increase the adoption of dermatoscopes. The demand for high-resolution digital imaging and interest in point-of-care imaging increases the adoption of dermatoscopes. The focus on evaluating small details of skin lesions and the growing number of rural healthcare providers increase the adoption of dermatoscopes. The FDA approvals and high portability of dermatoscopes drive the segment growth.

The imaging systems segment held the 23% market share in 2025. The focus on enhancing the evaluation of skin lesions and the interest in fast risk assessment increase the use of imaging systems. The major need for total body photography and the advancements in remote screening increase the use of imaging systems. The focus on lowering patient pain and the checking of new mole developments increases the use of imaging systems. The remote analysis of high-quality images increases the use of imaging systems, supporting the overall segment growth.

The biopsy devices segment held the 22% market share in 2025. The increased global burden of skin cancer and the transition to punch biopsy instruments increase the use of biopsy devices. The reduction of cross-contamination risk and the need for the protection of specialized needles increase the use of biopsy devices. The shift away from conventional hospital settings and the rise in tissue biopsies increase the use of biopsy devices. The popularity of the ambulatory clinic setting and the rise in definitive cancer diagnoses increase the use of biopsy devices, boosting the overall segment growth.

The AI-assisted diagnostic devices segment held the 17% market share in 2025 and is expected to grow at the fastest CAGR of 10.1% during the forecast period. The need to spot anomalies in dermoscopic images and the higher interest in non-invasive detection increase the adoption of AI-assisted diagnostic devices. The shift away from painful surgical biopsies and the thriving healthcare burden increases demand for AI-assisted diagnostic devices. The growing demand for expert-level diagnostics and increased awareness about superior early detection increase the adoption of AI-assisted diagnostic devices. The 3D visualization, high accuracy, and easy accessibility of AI-assisted diagnostic devices support the segment growth.

The sterile packaging segment dominated the packaging for skin cancer diagnosis device market with 72% share in 2025 and is expected to grow at the fastest CAGR of 8.2% during the forecast period. The growing use of pre-sterilized devices and the need for breathable barriers in diagnostic devices increase the use of sterile packaging. The demand for terminal sterilization compatibility and focus on avoiding complexity in shipping of devices increases the use of sterile packaging. The preference for thermoformed blister trays and the expansion of excision tools increases the use of sterile packaging. The increased use of durable plastics in sterile packaging drives the segment growth.

The non-sterile packaging segment held the 28% market share in 2025. The expanding use of AI-based optical scanners and the need for equipment durability during worldwide shipping increase the adoption of non-sterile packaging. The cost-effective packaging in the skin cancer diagnostic device and the rise in clinic-level disinfection increase the adoption of non-sterile packaging. The complex sterilization process and the explosion of digital skin analysis cameras increase the use of non-sterile packaging, supporting the segment growth.

The hospitals segment dominated the packaging for skin cancer diagnosis device market with 41% share in 2025. The demand for comprehensive cancer services and the rise in immediate therapeutic intervention increases demand for packaging for skin cancer diagnosis devices. The expansion of non-invasive diagnostic platforms and the stricter protocols of infection prevention increases the use of packaging for skin cancer diagnosis devices. The high skin cancer procedure volumes and the availability of multidisciplinary care teams increase the use of packaging for skin cancer diagnosis devices, driving the segment growth.

The dermatology clinics segment held the 29% market share in 2025 and is expected to grow at the fastest CAGR of 8.7% during the forecast period. The demand for focused expertise for detecting irregular moles and the demand for cellular-level visualization increase the use of packaging for skin cancer diagnosis devices. The patients' focus on faster appointments and the expansion of early-stage cancer screening increases the use of packaging for skin cancer diagnosis devices. The personalised care demand and the need to improve patient throughput help with the expansion. The expansion of outpatient screening results supports the segment growth.

The diagnostic laboratories segment held the 14% market share in 2025. The growth in molecular testing and the expansion of liquid-biopsy platforms increase the demand for diagnostic laboratories. The explosion of private diagnostic centers and the interest in non-invasive testing increases the use of diagnostic laboratories. The expansion of complex testing services and the focus on safe distribution of samples increase the use of diagnostic laboratories. The expanding digital pathology and the expansion of specialized consumables support the segment growth.

The ambulatory surgical centers segment held the 9% market share in 2025. The rise in sterile barrier innovations and the growing demand for same-day diagnostic tests increase the adoption of ambulatory surgical centers. The focus on lowering out-of-pocket expenses and the interest in value-based care increase the use of ambulatory surgical centers. The low-complexity procedures and better infection control in ambulatory surgical centers help with the expansion. The ambulatory surgical centers' expansion and the high patient preference support the overall growth of the segment.

The direct sales segment dominated the packaging for skin cancer diagnosis device market with 38% share in 2025. The demand for clinical demonstrations and the need for tailored financial planning increase the adoption of direct sales. The continuous demand for software updates and the need for seamless integration with other platforms increase the use of direct sales. The development of high-value B2B relationships, the need for customization, and the demand for product education increase the adoption of direct sales, driving the segment growth.

The medical device distributors segment held the 32% market share in 2025. The growing utilization of single-use components and the rising transportation of sterile items increase the adoption of medical device distributors. The advanced traceability requirements and the increased logistics of sensitive diagnostic equipment increase the use of medical device distributors. The rising development of hybrid diagnostic consoles and the surge in portable imaging units increase the adoption of medical device distributors. The buyer focuses on minimizing overhead costs, which supports the overall growth of the segment.

The contract packaging providers segment held the 18% market share in 2025. The prevention of contamination in primary packaging and the global healthcare mandates increase the use of contract packaging providers. The development of cleanroom-ready packaging and the need to minimize capital expenditure increase the use of contract packaging providers. The complexity of skin cancer smart devices and the interest in resilient supply chains increase the use of contract packaging providers, supporting the overall growth of the segment.

The e-commerce & online procurement segment held the 12% market share in 2025 and is expected to grow at the fastest CAGR of 10.4% during the forecast period. The need for enhanced supply chain visibility and the rise in tracking packaging inventories increase the adoption of e-commerce & online procurement. The convenient procurement demand and increased use of verified diagnostic tools increase the adoption of e-commerce & online procurement. The demand for smartphone-compatible diagnostic devices and the management of bulk orders increases the use of e-commerce & online procurement. The cost control and digital traceability of e-commerce & online procurement support the segment growth.

North America dominated the packaging for skin cancer diagnosis device market with a 39% share in 2025. The prevalence of melanoma skin cancers and the integrated hospital networks increase the demand for packaging for skin cancer diagnosis devices. The huge burden of non-melanoma skin cancer patients and the stricter sterility guidelines increase the demand for packaging. The expansion of teledermatology devices and the presence of sun-exposed areas increase the use of skin cancer diagnosis. The availability of employer-based insurance plans and the expanding awareness campaigns drive the market growth.

Europe held the 27% market share in 2025. The EU Medical Device Regulation and the thriving diagnosis of skin cancer increase the demand for packaging for skin cancer diagnosis devices. The growth in AI-assisted teledermatology and the use of bio-based polymers in medical device packaging help with the expansion. The growing cumulative UV exposure and the burgeoning primary-care diagnostics increase the use of packaging for skin cancer diagnosis devices. The EU guidelines for tamper-evidence and the huge investment in preventive healthcare support the market growth.

Asia Pacific held the 24% share in the market and is expected to grow at the fastest CAGR of 9.6% during the forecast period. The growing integration of non-invasive imaging systems and the rise in digital health frameworks increase the use of packaging for skin cancer diagnosis devices. The growing sun exposure and the burgeoning wellness tourism industry increase the adoption of packaging for skin cancer diagnosis devices. The larger geriatric demographics and the transition to AI-based diagnostic devices help with the expansion. The secure packaging mandates and the availability of production-linked incentives boost the market growth.

Latin America held the 6% market share in 2025. The high VU radiation and the early detection initiatives increase the adoption of packaging for skin cancer diagnosis devices. The interest in non-invasive diagnostics and the expanding medical device packaging helps with the expansion. The growing skin cancer incidence and the rise in public screening programs increase the use of packaging for skin cancer diagnosis devices. The incorporation of cloud-based mobile diagnostics supports the market growth.

The Middle East & Africa held the 4% market share in 2025. The growing skin-related conditions and the growth of modern medical cities increase the use of packaging for skin cancer diagnosis devices. The expansion of handheld diagnostic tools and the popularity of specialized dermatology equipment increase the use of packaging. The growing early screening of cancer and the availability of specialized medical treatments support the market growth.

| Rank | Name | Headquarters | Country | Major Contribution to Packaging for Skin Cancer Diagnosis Device Market | Key Packaging Products and Services |

| 1 | Amcor Plc | Zurich, Switzerland | Switzerland | The company provides SureForm Pro ICE Forming Films for the packaging of medical products. It also offers ACT2100 Heat Seal Coatings to maintain the sterile barrier integrity. | Recycle-Ready High Shield Medical Laminates, Healthcare Coated Tyvek ACT2100, Dessiflex Technology, Am Secure Thermoformed Trays & Rollstock, SureForm Forming Films |

| 2 | Sonoco Products Company | Hartsville, South Carolina, United States | United States | The company offers high-precision injection molding and offers flow wrapping solutions for the medical delivery and diagnostics industries. | Medical Plastics & Injection Molding, GreenCan, Thermoformed Packaging, Sterile Barrier Packaging |

| 3 | Oliver Healthcare Packaging | Grand Rapids, Michigan, United States | United States | The company creates Oliver design for diagnostic and medical devices. The company creates sterile barrier pouches for medical device sterility. | Tyvek Pouches, Laminate Film Pouches, Die-Cut Lids & Roll Stock, Barrier Foil Pouches, HDPE CleanCut Cards |

| 4 | Berry Global Inc. | Evansville, Indiana, 47710, United States | United States | The company provides rigid plastic components for the packaging of diagnostic tools. The company also offers packaging products for skin care packaging | Flexible Microbial Barrier Packaging, DuraMed & DirectSeal Films, Component Films & Overwraps |

| 5 | DuPont de Nemours Inc. | 974 Centre Road, Building 730, Wilmington, Delaware, 19805, United States | United States | The company offers microbial protection for diagnostic device packaging and focuses on preventing package damage. | Tyvek Peel Pouches, DuPont Liveo Healthcare Materials, DuPont Tyvek Medical & Pharmaceutical Packaging |

| 6 | SteriPack Group | Mullingar, County Westmeath, Ireland | Ireland | The company offers moisture-resistant protective inserts and offers end-to-end supply chain services for sterilization management. | PeelVent Pouch, Sterile Berrier System Packing, Primary & Secondary Packing |

| 7 | Tekni-Plex, Inc. | Wayne, Pennsylvania, United States | United States | The company offers coated medical-grade paper and thermoformable blister films for the packaging of diagnostic devices. | Thermoformable Medical Tray Films, Medical Grade Laminates, Single- and Multi-Dose Containers, Breathable Lidding & Papers |

By Packaging Type

By Material

By Device Type

By Sterility Requirement

By End User

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPackaging for Skin Cancer Diagnosis Device Market