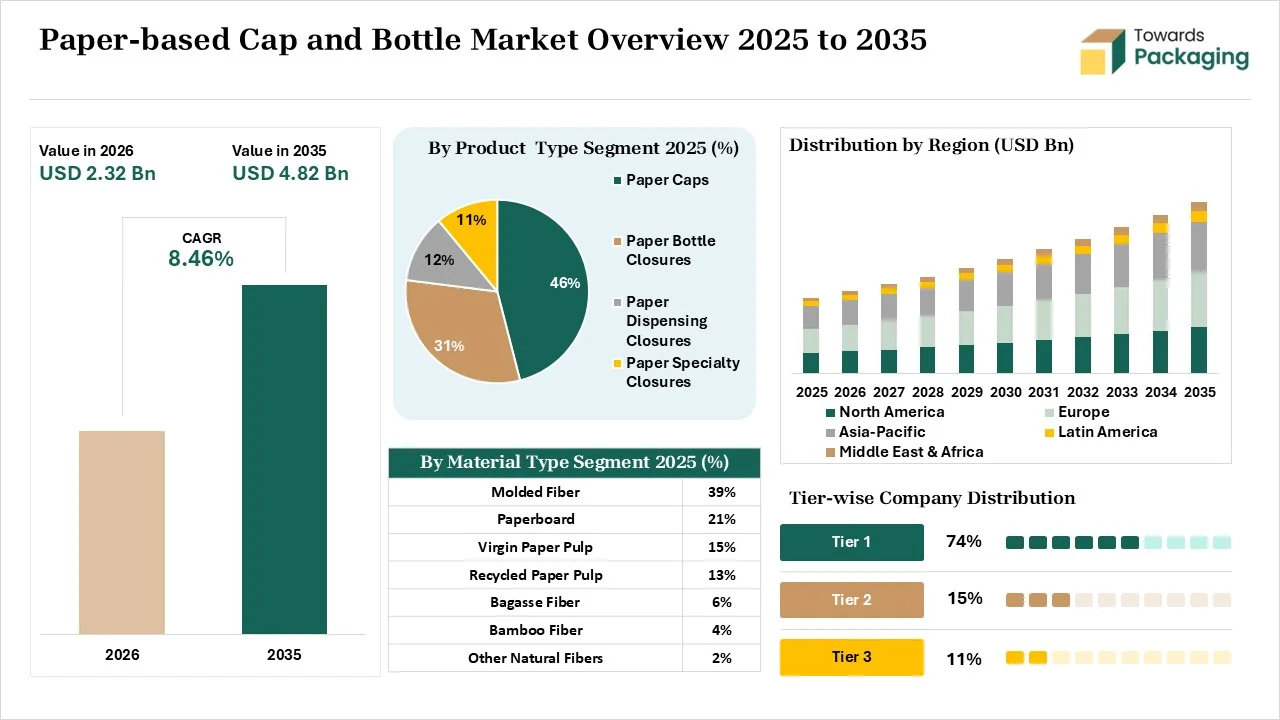

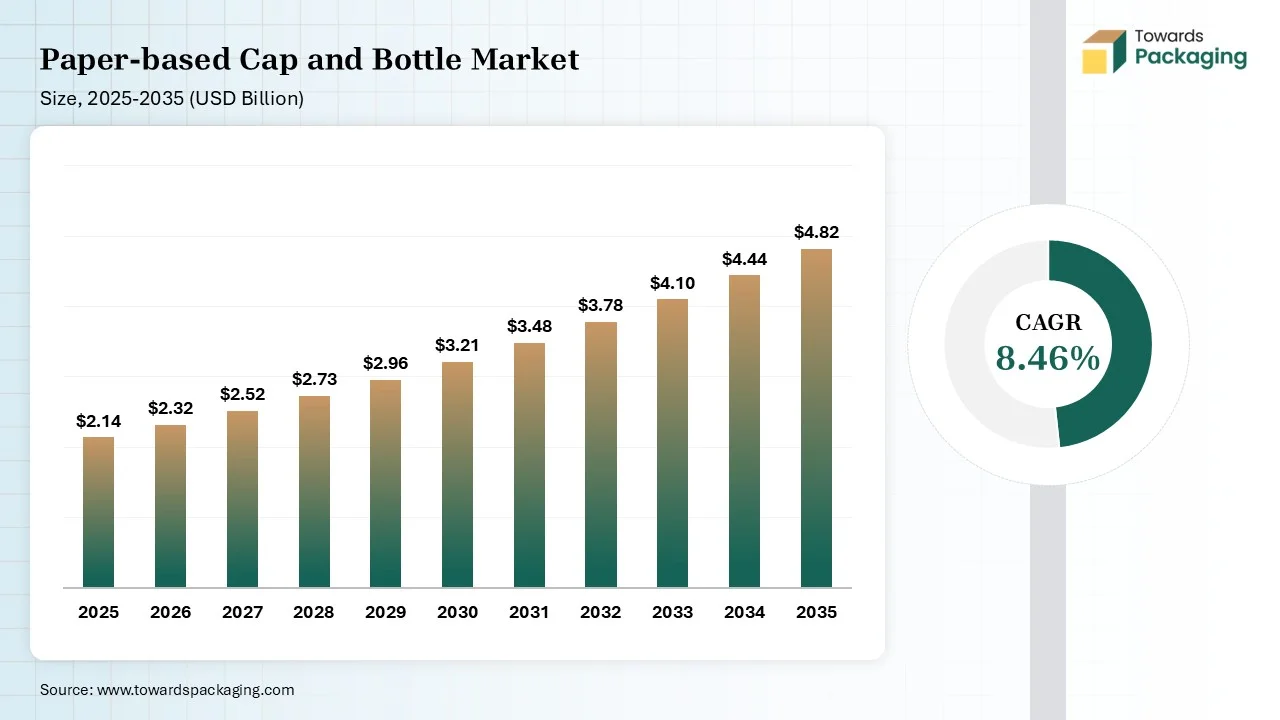

The paper-based cap and bottle market is projected to grow from USD 2.32 billion in 2026 to USD 4.82 billion by 2035, expanding at a CAGR of 8.46% during the forecast period. The report provides detailed insights into market size, growth forecasts, segment analysis, regional performance, competitive analysis, company profiles, manufacturers and suppliers, value chain analysis, import-export trade data, pricing trends, technological advancements, sustainability initiatives, and key market developments shaping the industry.

The paper-based cap and bottle are a sustainable packaging solution made from paper. The paper-based cap is a sustainable closure, and the paper-based bottle is a sustainable container manufactured from plant fibers. They offer benefits like high recyclability, eco-friendly aesthetics, minimized carbon footprint, functional integrity, and lightweight efficiency. They feature excellent customizability, a lightweight design, and protected contents. Paper-based caps and bottles are used across spirits, broths, juices, FMCG liquids, condiments, wine, soups, sauces, and milk packaging. For instance, the Absolute Vodka company uses screwable paper caps for its vodka bottles.

For instance, in October 2025, Cremaura cream liqueur adopted Frugal bottles developed by Frugalpac. The paper bottles are useful for products like Tequila-based Rose flavors and Tequila-based Caramel flavors. The shift to paper bottles increases the global reach and lowers the company’s environmental impact.

For instance, in March 2026, REWE introduced olive oil in a Frugalpac paper bottle. The Jordan Olivenol is packed using a paper bottle. The bottle protects product quality and is available in REWE stores. The olive oil is available in a 750 ml bottle, and the Frugal bottle offers protection against photo-oxidation.

The paper-based caps and bottle market growth is driven by the continuous expansion of advanced barrier coatings, modern consumers' commitment to eco-friendly products, focus on lowering logistic costs, rise in brand marketing, growing water packaging, bans on single-use plastics, CPG companies' sustainability commitments, and innovations in molded fiber technologies.

In February 2025, Pulpex raised investment of $78 million to increase the production of paper-based bottles. The investment raised in Series D funding, and the bottles are made of wood pulp. The bottles are compatible with the household waste stream recycling. The funding round is led by Scottish National Investment Bank and NWF.

The paper-based cap and bottle market is going through several technological developments, like dry molded fiber technology, nanotechnology, IoT-enabled packaging, machine vision, and digital product passports. Technological developments driven by lowering water usage and precision manufacturing. The AI integration is a major transformation in the industry. AI helps in data-driven design and speeding up material R&D.

AI tests numerous barrier combinations and supports advanced quality control. AI helps in sustainable material optimization and detects misaligned paperboard seals. AI predicts the structural failures and enhances plant efficiency. AI incorporates interactive elements in the paper-based cap & bottles. AI easily adjusts visual assets and predicts seasonal trends. Overall, AI supports design optimization and waste optimization.

Raw materials like plant-based fibers, PLA barriers, plant-based waxes, solid bleached sulfate, certified wood pulp, PHA barrier, and coated unbleached kraft.

Material processing involves steps like fiber preparation, molded fiber forming, hot pressing, barrier liner integration, assembly, and finishing. Conversion includes material processing, hybrid core integration, and top-seal barrier.

Design focuses on cap evolution, outer shell, and barrier linings. Prototyping focuses on pressure tests, iterative refinement, and functional trials.

The paper caps segment dominated the market with 45.8% share in 2025. The shift away from fossil-based caps and the growing recycling challenges in plastic caps increase the adoption of paper caps. The expanding spirit companies and the high demand for leak-proof seals increase the use of paper caps. The interest in eco-friendly caps helps with expansion. The seamless integration of paper caps in existing manufacturing lines drives the segment growth.

The paper bottle closures segment held the 30.70% market share in 2025 and is expected to grow at the fastest CAGR of 8.9% during the forecast period. The focus on cutting overall bottle weight and the focus on maximizing the use of renewable fiber increase the adoption of paper bottle closures. The real-world durability and enhanced recyclability of paper bottle closures help with expansion. The major beverage brands shift to paper-based alternatives, and the transition away from aluminum closures increases the adoption of paper bottle closures, supporting the market growth.

The molded fiber segment dominated the market with 38.6% share in 2025. The focus on preventing liquid leaking and the manufacturing of complex caps increases the use of molded fiber. The need to lower shipping damage and the rising development of intricate shape caps increase the use of molded fiber. The excellent crush resistance, coating advancements, liquid barriers, high repulpability, and excellent aesthetics of molded fiber help with expansion. The growing modern manufacturing drives the segment growth.

The recycled paper pulp segment held the 13.40% market share in 2025 and is expected to grow at the fastest CAGR of 9.3% during the forecast period. The focus on minimizing emissions and transportation savings during distribution increases the adoption of recycled paper pulp. The robust local recycling networks and the advancements in closures increase the use of recycled paper pulp. The focus on offering a unique tactile experience and the need to cut deforestation increase the use of recycled paper pulp. The cost optimization and supply chain accessibility in recycled paper pulp drive the segment growth.

The uncoated segment dominated the market with 29.5% share in 2025. The brand's focus on creating eco-friendly aesthetics and the need to lower manufacturing footprint increases the use of uncoated paper. The high raw material efficiency and focus on avoiding extra lamination increase the use of uncoated paper. The integration of aqueous dispersion technologies in uncoated paper helps with expansion. The maximum recyclability and lower production cost of uncoated paper drive the segment growth.

The bio-based coating segment held the 17.10% market share in 2025 and is expected to grow at the fastest CAGR of 9.7% during the forecast period. The high interest in easily recyclable materials and the shift away from hazardous PFAS coatings increase the adoption of bio-based coatings. The preference for non-toxic packaging and focus on comparable performance increases the use of bio-based coating. The creation of premium brand reputation and the innovations in bio-formulations increase the use of bio-based coating, supporting the segment growth.

The threaded closures segment dominated the market with 42.8% share in 2025. The focus on preventing caps from stripping and the need for a measurable mechanical bond increase the adoption of threaded closures. The rise in non-food items and the focus on preserving freshness increase the use of threaded closures. The functional convenience, unmatched resealability, and excellent mechanical integrity of threaded closures help with the expansion. The rising water packaging drives the segment growth.

The snap-fit closures segment held the 24.60% market share in 2025 and is expected to grow at the fastest CAGR of 9% during the forecast period. The high fiber content and the focus on tethered cap designs increase the adoption of snap-fit closures. The need for press-and-seal convenience and the interest in leak-proof locks increase the use of snap-fit closures. The growing gel use and the need for zero-torque sealing are increasing the adoption of the snap-fit closures. The one-handed convenience, lightweightness, and high performance of snap-fit closures support the segment growth.

The wet molding segment dominated the market with 46.7% share in 2025. The rising development of high-density shells and the focus on developing smooth exterior finishes increase the use of wet molding. The interest in tactile branding and the need for barrier integration increase the use of wet molding. The development of caps and bottles that withstand internal pressure increases the use of wet molding. The permanent branding and high density of wet molding drive the segment growth.

The dry molding segment held the 25.60% market share in 2025 and is expected to grow at the fastest CAGR of 9.5% during the forecast period. The focus on lowering energy spent and the shift away from long drying cycles increase the use of dry molding. The creation of screw threads and the focus on creating unique experiences increase the use of dry molding. The shift away from drying ovens and the demand for high manufacturing speeds increase the use of dry molding. The premium functionality and high industrial scalability of dry molding support the market growth.

The 251-500 ml segment dominated the market with 37.9% share in 2025. The growing everyday use of the products and the focus on structural engineering of bottles increase the use of 251-500 ml. The expansion of liquid hand soaps and the need to maintain portion control increase the use of 251-500 ml bottles. The rise in surface cleaners and the consumption of single-serve juices increases the use of 251-500 ml bottles. The cylindrical structures and eco-awareness increase the adoption of 251-500 ml bottles, driving the overall segment growth.

The 501-1000 ml segment held the 28.30% market share in 2025 and is expected to grow at the fastest CAGR of 9.1% during the forecast period. The consumer's strong focus on fridge-fit convenience and high interest in spirits increases the use of 501-1000 ml bottles. The focus on maintaining liquid structural integrity and the increased premiumization of beverages increases the adoption of the growing multi-person households and need for everyday hydration increase the use of 501-1000 ml bottles. The growing eco-conscious Gen Z supports the segment growth.

The food & beverage segment dominated the market with 58.4% share in 2025. The thriving cloud kitchen platforms and the growth in multinational food producers increase the adoption of paper-based caps and bottles. The innovations in the food-grade barrier coatings help with expansions. The rise in on-the-go dairy and the growing everyday dairy consumption increases the use of paper-based caps and bottles. The expanding single-use liquid packaging and massive water demand drive the segment growth.

The pharmaceuticals segment held the 11.30% market share in 2025 and is expected to grow at the fastest CAGR of 9.2% during the forecast period. The expanding OTC industry and the need for lightweight packaging in pharmaceuticals increase the adoption of paper-based caps and bottles. The focus on brand differentiation in the pharmaceutical industry and the presence of major pharma giants increase the use of paper-based caps and bottles. The exploding nutraceutical spaces and the focus on plastic-reduction in pharma infrastructure increase the adoption of paper-based bottles and caps, supporting the segment growth.

The direct sales (OEM) segment dominated the market with 63.2% share in 2025. The rise in complex technology and the focus on seamless design integration increase the use of direct sales. The high initial manufacturing expenses and the management of return logistics increase the use of direct sales. The customization of corporate orders and the focus on proper material handling increase the adoption of direct sales. The strong B2B supply relationships of direct sales drive the segment growth.

The online/B2B platforms segment held the 11.30% market share in 2025 and is expected to grow at the fastest CAGR of 10.2% during the forecast period. The rise in comparison of barrier coatings and the growing demand for market-ready bottles increases the adoption of online/B2B platforms. The rise in specialized innovations and the increasing need for requesting custom quotes increases the use of online/B2B platforms. The higher need for centralized delivery and high space-saving packaging demand increases the adoption of online/B2B platforms, supporting the segment growth.

Europe dominated the market with 32.4% share in 2025. The high taxes on disposable plastics and the consumers' focus on prioritizing circularity increase the adoption of paper-based caps and bottles. The strong recycling rates of paper and the increased manufacturing of bio-based coatings increase the adoption of paper-based caps and bottles. The huge development of low-carbon packages and the focus on systematic sustainability mandates increases the use of paper-based caps and bottles. The strong R&D infrastructures drive the market growth.

Asia Pacific held the 29.30% share in the market in 2025 and is expected to grow at the fastest CAGR of 9.6% during the forecast period. The circular economy mandates across APAC countries, and the high parcel intensity increases the demand for paper-based caps and bottles. The well-developed integrated pulp mills and the shift to green products increase the use of paper-based caps and bottles. The quick model's presence and the availability of advanced manufacturing techniques increase the use of paper-based caps and bottles. The rapidly expanding premium food supports the market growth.

North America held the 26.80% market share in 2025. The aggressive plastic reduction targets and the customer loyalty towards eco-packaging increase the use of paper-based caps & bottles. The interest in eco-friendly closure systems and the global brands' transformation to compostable packaging increases the use of paper-based caps & bottles. The plastic pollution awareness and the focus on holding liquids safely increase the use of paper-based caps & bottles, supporting the market growth.

Latin America held the 6.30% market share in 2025. The transition to bio-based containers and the strong paper industry increases the adoption of paper-based caps and bottles. The shift away from plastic bottles and the abundance of high-quality kraft paper increase the adoption of paper-based caps and bottles. The increased green materials adoption in domestic FMCG brands and the focus on preventing ocean pollution increase the use of paper-based caps and bottles, boosting the market growth.

The Middle East & Africa held the 5.20% market share in 2025. The regulatory mandates on single-use plastic containers and the massive online shopping by urban populations increase the adoption of paper-based caps and bottles. The rise in sustainable tourism and the expanding hospitality industry increases the use of paper-based caps and bottles. The surging cosmetic productions and the high consumer interest in biodegradable caps increase the adoption of paper-based caps and bottles, boosting the market growth.

| Rank | Company | Headquarters | Country | Major Contribution to Paper-based Cap and Bottle Market | Key Packaging Products and Services |

| 1 | Paboco | Slangerup, Denmark | Denmark | The company manufactures integrated plant-based barriers and focuses on scaling sustainable production. |

Fiber-Based Caps , Next Gen Paper Bottle |

| 2 | Amcor | Zurich, Switzerland | Switzerland | The company provides thin-film barriers and focuses on the development of paper wraps on existing packaging machinery. | Plastic-Free Foils, AmFiber Performance Paper, EcoGuard Range |

| 3 | Mondi Group | Weybridge, Surrey, United Kingdom | United Kingdom | The company manufactures fiber-based plugs and manufactures various types of high-barrier papers. The company also developed specialized kraft paper, SpringPack Plus. | Hug&Hold, PerFORMing, Corrugated Wraparound, Corrugated Trays |

| 4 | Pulpex | Sawston, Cambridgeshire, England, United Kingdom | United Kingdom | The company provides 100% PET-free materials and food-safe barriers. The company's bottles reduce carbon emissions up to 90%. | Paper-Based Closures, Customized Single-Mould Bottles, Paper-based Caps |

| 5 | Tetra Pak | Pully, near Lausanne, Switzerland | Switzerland | The company offers plant-based polymers and paper-based barriers for aseptic cartons. | Tetra Top, Tethered Caps, Tetra Top with Bio-based Top |

By Product Type

By Material

By Coating Type

By Closure Mechanism

By Manufacturing Process

By Bottle Size Compatibility

By End-use Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPaper-based Cap and Bottle Market