The U.S. cold chain packaging market is projected to grow from USD 20.68 billion in 2026 to USD 53.77 billion by 2035, registering a CAGR of 11.2% during the forecast period. The report provides detailed market size evaluation, revenue forecast, and comprehensive segment analysis by packaging type, material, product format, application, and end-use industry. It also covers regional demand patterns, trade statistics, import-export analysis, production trends, competitive landscape assessment, company profiling, value chain analysis, and extensive manufacturers and suppliers data across the United States.

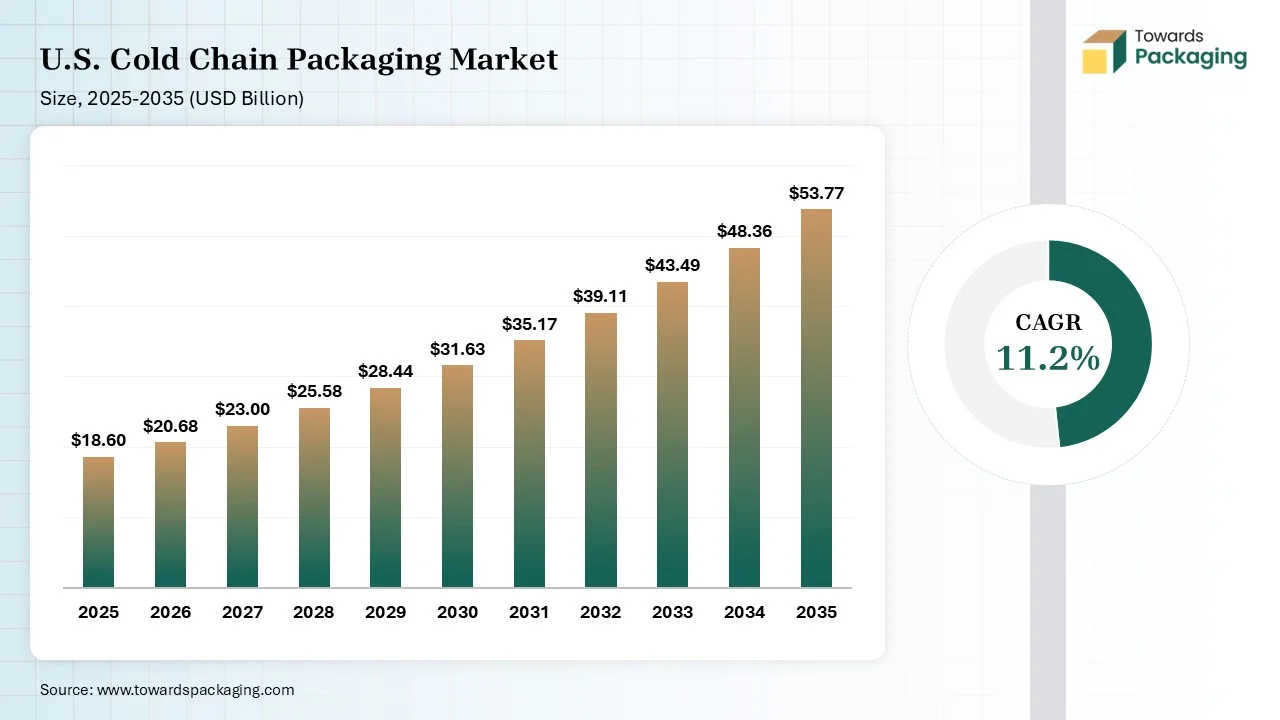

Market Size (2025): USD 18.6 Billion

CAGR (2025–2035): 11.2%

Market Volume (2025): 4.9 million Tons

Volume CAGR (2025–2035): 10.4%

Pricing Data (2025):

A cold chain is a tailored supply chain that is crafted for sensitive goods, drugs, vaccines, chemicals, and other temperature-fragile products, which should be stored at a controlled temperature from production to outcome delivery. This procedure includes tracking constant refrigeration within both transport and logistics; that makes sure temperature-sensitive products stay within the demanded humidity and temperature levels. Cold chain technology, by using procedures like dry ice, gel packs, reefers, and liquid nitrogen, ensures accurate temperature control.

Trends in the U.S. Cold Chain Packaging Market

Sustainability: Brands are substituting regular EPS foam that has curbside biodegradable and recyclable materials. Insulated packaging created from starch-based foams, molded fiber, and mycelium is receiving attention.

E-Commerce and DTC Growth: The growth of meal-kit deliveries and online pharmacy services is encouraging cold chain packaging to develop. Users predict pharmaceutical-grade temperature control in such deliveries, as its life-saving gourmet seafood or insulin are well aligned with industry standards.

IoT-Driven Tracking and AI: Smart technology is updating cold chain logistics. IoT-enabled tracking systems and AI-linked sensors now deliver real-time visibility into humidity, temperature, and the shipment facility. Predictive analysis also assists in updating packaging outcomes, lowering extra materials during periods of managing secured standards.

Standardization and Regulatory Compliance: As the worldwide supply chains stretch, regulatory needs are becoming stronger. The pharmaceutical sector is experiencing strong Good Distribution Practice (GDP) standards, while food security regulations are undergoing developments in packaging reliability.

Blockchains are being distributed in digital ledger technology, which marks transactions across computers. Every amount or communication is collected into blocks and connected in chronological order to make a fixed and immutable series of records. Each communication with a product is being tracked on the blockchain, which delivers an overall and transparent history of transport. This makes the management system of the product’s location, status, and surroundings more manageable. Additionally, energy-efficient refrigeration systems lower electricity usage, which lessens the operational costs for cold chain shipping brands. Such procedures frequently use environmentally friendly refrigerants that have lower climate effects than regular refrigerants.

Managing temperature inside checked restrictions needs not only insulation but also continuous monitoring. EPS vaccine boxes are primarily crafted to use temperature monitoring technologies, such as temperature sensors, electronic data loggers, and time-temperature indicators.

Logistics and Distribution: Minimalist cold chain packaging has further benefited from lower manufacturing and logistics costs while travelling and collaborating with sustainable logistics practices. Such strategies count by using reusable packaging, circular packaging, and recyclable packaging, so as to market closed-loop systems that match the creation of waste while assisting responsible resource links.

Recycling and Waste Management: Bioplastics have the added benefit of being a recyclable option with a lesser carbon footprint while being sourced from renewable sources. Paper-based packaging is conveniently thoughtful and recyclable for sustainable logistics, for instance, compostable materials like plant-based films, which serve solutions in the packaging waste minimization.

The insulated containers segment dominated the U.S. cold chain packaging market with 48% share in 2025, as these units' lower temperature changes prevent devices and supplies from cold or heat without any complete refrigeration. Shippers make use of valid insulated containers, dry ice, gel packs, or phase-change materials to track temperature during logistics. Packaging is managed to store ingredients within the focused range.

The refrigerants segment held 37% of the market share in 2025, as storing the contents of any meal kit chilled and fresh is essential. They operate with insulation elements to deliver a constant temperature in the interior part of the box. Additionally, water-soluble gel is frozen inside plastic packs to store products cold. The current ingredients in terms of gel packs are sodium polyacrylate. When they are integrated with frozen water, it is mainly lower than ice.

The temperature monitoring devices segment held 15% of the market share in 2025 because cold chain monitoring depends on the link of temperature monitoring machines that pass with a cargo during logistics, kept at a location. These points are whether any product is present in shipping containers, processing plants, refrigerated trucks, freezers, and cold storage facilities at any local supermarket, in which it has a cold chain tracking device that follows it. Such sensors have constantly managed and recorded temperatures, and several other transmitting data, product conditions to a main system.

The plastic segment dominated the U.S. cold chain packaging market with a 52% share in 2025, as plastics are utilized in the cold chain sector and they solve issue fold witness each day. For biologics, vaccines, and lab samples, every small temperature change matters. This points out the environmental materials that demand to remain relying in the cold and not lower down from disinfectants. Temperature-reliant plastics in the pharmaceutical sector are prevalently used for trays for syringes and vials, insulated medical shippers, and interior parts for the medical transport vehicles.

The paper & paperboard segment held 28% of the market share in 2025 because molded fiber begins with the correct raw material mixture for the technology used in the cold chain packaging sector. In the current scenario, commercial spaces use recycled paperboard, which gets mixed with wheat straw, sugarcane bagasse, or bamboo pulp as an extra-fiber source. These fiber-dependent designs are frequently compostable or biodegradable in matched systems, as they fit perfectly into current sustainable packaging methods.

The metal segment held 8% market share in 2025 because aluminium foil is widely used as a metal material in terms of packaging materials. It has the benefit of odorless, non-toxic, and light-protecting elements. Hence, pharmaceutical aluminium foil blister packaging is widely used in cold chain packaging material. Health-grade aluminium foil packaging is a packaging material which are available in direct link with edible drugs.

The single-use packaging segment dominated the U.S. cold chain packaging market with 61% share in 2025, as they are also known as disposable packaging, as such basic containers shift batches of medicine and are being disposed of after one application. Passive temperature control is utilized with such packaging. Such containers have mainly less upfront cost as compared to a reusable solution with respect to sourcing, buying, and then the actual buying, sourcing, and management of stock surfaces.

The reusable packaging segment held 39% market share in 2025 because the eco-friendly advantages of reusable packaging solutions stretch a long way from simple waste avoidance to overall lifecycle developments, which solve climate update, secure ecosystems, and market resource protection. Such systems mainly change the eco-friendly equation by substituting linear “take-create-dispose” designs with a circular starry which develops resource usage while lowering eco-friendly effect.

The pharmaceuticals segment dominated the U.S. cold chain packaging market with 46% share in 2025 as freezing biologics is almost an unavoidable method in the procedure of protecting and keeping them for an extended period. Biologics use a huge range of therapeutic items that come from living organisms. They include protein solutions, monoclonal antibodies, and other vaccines that are complicated formulations crafted to diagnose different medical conditions and diseases. The freeze-thaw procedure needs proximate attention to cooling rates, formulation, and cryoprotective methods to manage the efficacy and stability of drug items among cold chains.

The food & beverages segment held 42% of the market share in 2025 because cold chain packaging points to secured materials utilized to manage temperature while transport, distribution, and delivery. It stores food secured from moisture that points to box leaks or damage and bacteria development because of growing temperatures. Long-distance service issues and handling pressure during transport. If we run with fresh produce, specifically meat, fish, chilled ready-to-eat foods, and poultry, cold chain security is a milestone for both product quality and hygiene.

The chemicals segment held 7% of the market share in 2025 because materials can respond, lower, or transform into toxic substances if they are exposed to the incorrect conditions, which creates managed essentials for both compliance and safety. Chemical materials should stay at temperatures to stay effective and constant. Storing the correct eco-friendly conditions and fixing temperature tracking are complicated during storage and transportation for such products.

The chilled (2oC to 8oC) segment dominated the U.S. cold chain packaging market with 44% share in 2025 as several vaccines (specifically inactivated vaccines and the live nasal spray for influenza vaccine) need to be stored in lower temperatures, which is suggested in refrigerator temperature. Such vaccines can temporarily be stored in terms if refrigerator for approximately 72 hours before application. Once such vaccines have been kept in the refrigerator, they should not be refrozen at this temperature.

The frozen (-20oC and below) segment held the market with 34% share in 2025 because they are also known as frozen warehouses, which points to tailored storage facilities that are crafted to track constant low temperatures (sub-zero) for the official storage of frozen food items. Such facilities play an important role in protecting the safety and quality of frozen foods within the supply chain. Frozen cold rooms are crafted to maintain temperatures that generally range from -18 oC to as low as -22 oC.

The controlled room temperature segment held the market with 22% share in 2025, as CRTs are being defined by the United States Pharmacopeia (USP) as temperatures present between 20oC and 25oC. The USP does not give official permission for the expanded temperature range, as the complete mean kinetic temperature must be 25oC. This points out that while the temperature should change over time as materials are kept.

The direct sales (B2B) segment dominated the U.S. cold chain packaging market with 49% share in 2025 as pharma’s regular design of selling within PBMs, wholesalers, and pharmacies depends excessively on adjusted rebates, which points to unique pricing. But as the MFN rules, IRA and remaining discounts get squeezed between calls for developed producers, who are discovering alternative channels to protect the amount and control, as the patient witnesses. The DTC program, with a model as a manufacturer, makes a stage that brings together various solutions in a pharma-branded digital ecosystem.

The third-party logistics (3PL) segment held the market with 33% share in 2025 as the top 3PL providers give importance to investments in state-of-the-art infrastructure and technology, which are specialized for smooth cold chain management. This overall strategy includes a series of well-established factors, which include refrigerated transportation, warehouses, and fleets filled with high-level tracking systems and real-time management potential.

The e-commerce distribution segment held the market with 18% share in 2025 as the development of online grocery and meal-kit-delivery services urges strong cold chain logistics for home deliveries. For example, banana exporters are discovering paths to track the fruit ripening procedure differently, so they make sure quality and freshness when the fruit is delivered directly to homes. It has the capability to manage and control atmospheres in refrigerated containers that are known as reefers or board vessels, as shippers can actively track the number of bananas.

The U.S. cold chain packaging industry concentrates on temperature-fragile packaging solutions, which are necessary for protecting the safety and quality of sensitive goods. Main focused markets include food and beverages, pharmaceuticals, and biotechnology industries. Income growth is being driven by a growing urge for temperature-controlled warehouses, strict rules on pharmaceutical shipments, and food safety. Some of the significant product types include insulated containers, refrigerants, and temperature tracking tools, catering to demands for managing temperature-fragile products.

By Product Type

By Material Type

By Packaging Format

By End-use Industry

By Temperature Range

By Distribution Channel

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarU.S. Cold Chain Packaging Market