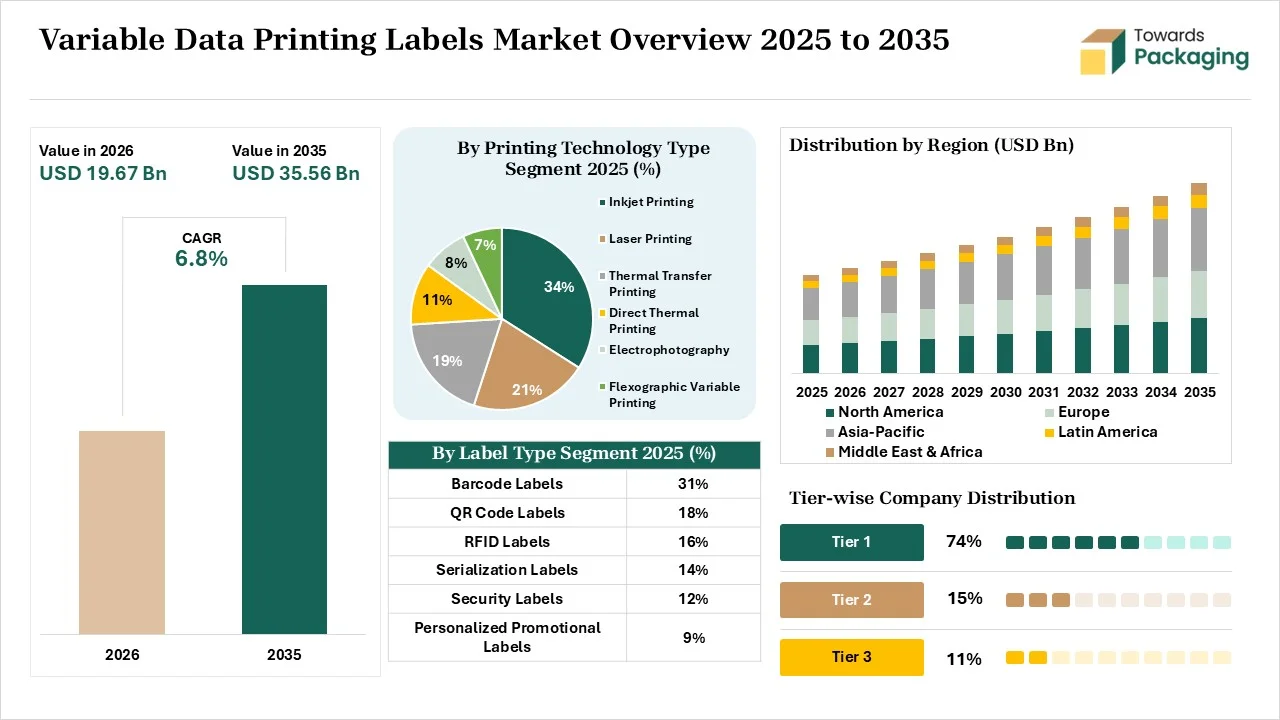

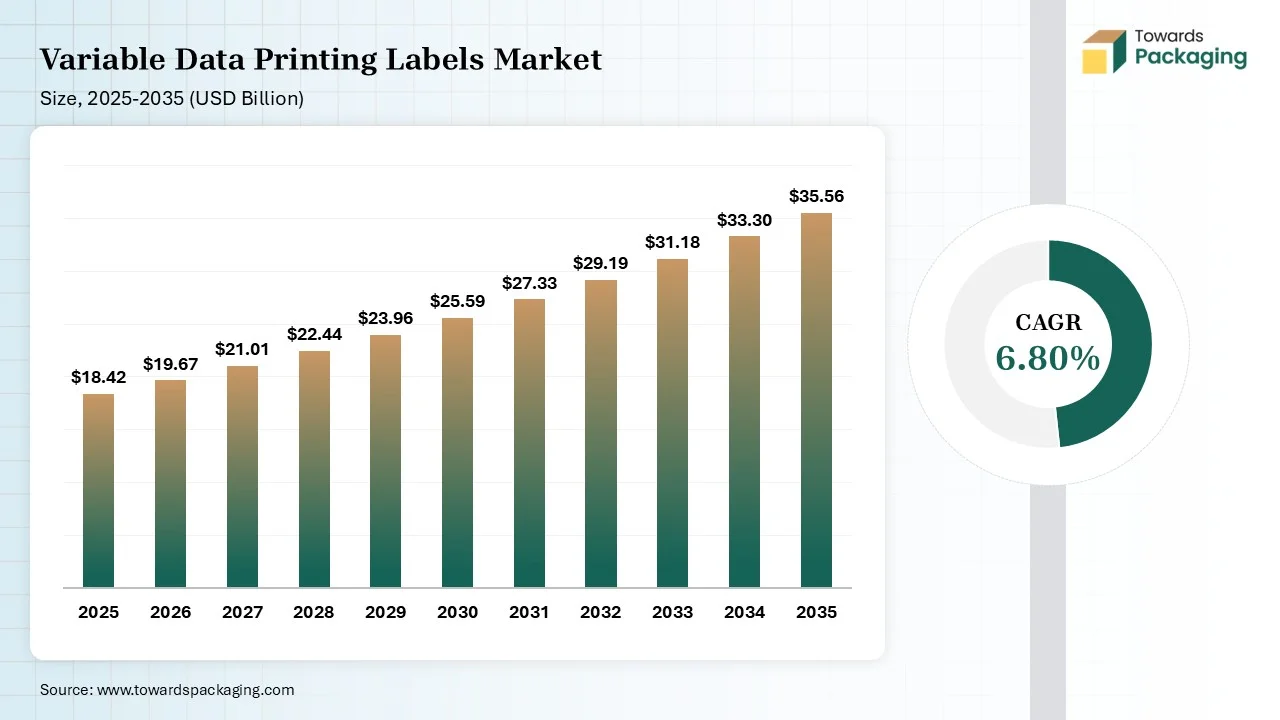

The variable data printing labels market is projected to grow from USD 19.67 billion in 2026 to USD 35.56 billion by 2035, registering a CAGR of 6.80% during the forecast period. The report provides comprehensive coverage of market size, revenue forecasts, segment-wise analysis by printing technology, label type, substrate, application, and end-use industry. It delivers detailed regional insights, competitive landscape assessment, company profiling, market share analysis, value chain evaluation, trade flow statistics, and extensive data on manufacturers, suppliers, distributors, and emerging market participants. The study also examines how digital printing advancements, increasing demand for personalized labels, linerless label adoption, and the growing popularity of smart packaging are shaping industry growth.

Variable data printing (VDP) labels are tailored-printed labels manufactured using digital printing methods. The main components of VDP labels are the database and print run. The various variable elements are traceability codes, product details, sequential numbers, barcodes, personalization, and QR codes. It provides benefits like counterfeit protection, hyper-personalization, enhanced compliance, inventory efficiency, automated traceability, and cost efficiency. VDP labels are used in property tagging, DTC campaigns, GS1 barcodes, unique serial numbers, QR codes, hidden sweepstakes text, and equipment tagging.

The variable data printing labels market growth is driven by the e-commerce growth, the innovation of electrophotographic presses, the rise in item-level serialization, the expansion of targeted content in brands, the interest in dynamic labeling solutions, the shift away from large label inventories, the burgeoning mass product customization, and the expansion of digital VDP.

The variable data printing labels market is experiencing technological developments driven by strict traceability regulations, scalable customization, and real-time tracking. Technological developments like 3D visualizations, cloud integration, and data automation are driven by demand for enhancing press speeds and supply chain compliance. AI plays a key role in the market by offering real-time personalization.

AI creates custom marketing messages and supports the development of localized packaging campaigns. AI easily processes variable data files and inspects printed labels. AI prevents unexpected repair costs and generates unique designs. AI easily verifies unique barcodes and other variable data. AI easily detects alignment issues and adjusts ink drops. Overall, AI helps in mass personalization and enhancing operational efficiency.

Raw materials like thermal paper, BOPP, polyolefin, kraft paper, thermal transfer ribbons, PET, varnish, and PET film liner are required.

Material processing focuses on surface coating, adhesive application, and lamination. Conversion focuses on rotary die-cutting, matrix stripping, and slitting.

Package design focuses on the static layer, the variable layer, and automated merging. Prototyping focuses on design, software merging, short-run printing, and adjustment.

The inkjet printing segment dominated the market with 34% share in 2025 due to its high-speed production. The production of short-run labels and the manufacturing of high-contrast barcodes increase the use of inkjet printing. The increased use of item-level serialization and the increased printing of sequential information increases the adoption of inkjet printing. The mass customization, lower setup costs, and exceptional scannability of inkjet printing drive the segment growth.

The laser printing segment held the 21% market share in 2025 due to the demand for high-resolution output. The focus on supply chain management and the minimization of consumables costs increases the adoption of laser printing. The focus on printing expiration dates in pharmaceuticals and the expansion of high-volume jobs increase the use of laser printing. The high-volume efficiency and exceptional sharpness of laser printing support the segment growth.

The thermal transfer printing segment held the 19% market share in 2025 due to its high-definition scannability. The long-term storage and the regulations for labeling hazardous materials in pharmaceuticals increase the use of thermal transfer printing. The rise in product tracing and the presence of long-lasting barcodes on drugs increase the use of thermal transfer printing. The incorporation of automated labeling with thermal transfer printing boosts the segment growth.

The barcode labels segment dominated the market with 31% share in 2025 due to the growing use in modern inventory management. The focus on tracking patient safety and the management of logistics increases the use of barcode labels. The e-commerce fulfilment and the use of batch-coded labels in healthcare increase the adoption of barcode labels. The growing automated inventory tracking increases the use of barcode labels. The excellent machine readability and cost-effectiveness of barcode labels drive the segment growth.

The QR code labels segment held the 18% market share in 2025 due to the growing use in short-run promotions. The development of customized discount codes and the focus on valuable consumer analytics increase the adoption of QR codes. The simplification of warranty management and the hyper-personalised marketing increases demand for QR codes. The burgeoning eco-friendly initiatives support the segment growth.

The RFID labels segment held the 16% market share in 2025 due to the focus on streamlining inventory management. The focus on interactive promotions and the need for serialized tracking increases the adoption of RFID labels. The thriving warehouse automation and the focus on streamlining returns increase the use of RFID labels. The growing fast-paced product launch and the utilization of mass encoding increase the use of RFID labels, boosting the segment growth.

The plastic films segment dominated the market with 39% share in 2025 due to its high-quality printability. The rigorous handling in the pharmaceutical industry and the rise in high-resolution graphics printing increase the adoption of plastic films. The robust mass-personalization and the production of squeezable bottles increase the use of plastic films. The high-quality printability, extreme durability, and excellent flexibility of plastic films drive the segment growth.

The paper segment held the 37% market share in 2025 due to the growing use of electrophotography technologies. The printing of variable information and the major retail brands increases the use of paper. The drug safety mandates and the focus on eliminating plastic increase the use of paper. The rise in production of shipping labels and the increased printing of customized messaging increases the use of paper, supporting the segment growth.

The synthetic paper segment held the 9% market share in 2025 due to the increased use in digital presses. The focus on unique brand management and the shifting away from conventional wood-based products increases the use of synthetic paper. The growth in interactive packaging and the expansion of customized printing increase the adoption of synthetic paper. The print sharpness and excellent color vibrancy of synthetic paper support the segment growth.

The roll-to-roll printing segment dominated the market with 58% share in 2025 due to rising use in the food sector. The need for high-speed serialization and the development of RFID-enabled labels increases the use of roll-to-roll printing. The focus on limiting ink waste and the increasing bulk runs of customized variable labels enhance the use of roll-to-roll printing. The finishing integration and compatibility with modern materials of roll-to-roll printing drive the segment growth.

The sheet-fed printing segment held the 24% market share in 2025 due to the increasing localized messages of brands. The focus on frequent SKU changes and track-and-trace mandates increases the use of sheet-fed printing. The rise in customization of individual labels and the development of label stocks increases the use of sheet-fed printing. The substrate flexibility, cost-efficiency, & personalization of sheet-fed printing drives the growth the segment.

The hybrid printing systems segment held the 18% market share in 2025 due to the growing use of high-quality embellishments. The development of durable finishes and premium decorations increases the use of hybrid printing systems. The focus on reducing turnaround times and the innovations in low-migration LED inks increase the adoption of hybrid printing systems. The automation efficiency and reduced waste of hybrid printing systems boost the segment growth.

The product identification segment dominated the market with 27% share in 2025 due to its brand security. The development of individualized customer experiences and real-time inventory tracking increases the use of VDP labels. The encryption of QR codes and the expanding logistics increase the use of VDP labels. The improvement in inventory accuracy and the focus on SKU management increase the use of VDP labels, driving the segment growth.

The track & trace segment held the 18% market share in 2025 due to strong regulatory compliance across several countries. The installation of the warehouse management systems and the focus on monitoring unauthorized tampering increase the use of track & trace. The growing equipment upgradation and demand for genuine products across the automotive industry increase the use of track & trace labels.

The inventory management segment held the 15% market share in 2025 due to the focus on handling SKUs. The high-speed production operations and the focus on streamlining ordering patterns increase the use of VDP labels. The growing on-demand printing and the growing product variations increase the use of VDP labels. The expansion of real-time tracking boosts the segment growth.

The food & beverage segment dominated the market with 24% share in 2025 due to the growing limited-edition runs in F&B. The focus on integrating expiration dates and other factors on F&B products increases the use of VDP labels. The generation of food invoices and the integration of freshness codes on F&B products increases the use of VDP labels. The focus on maintaining the authenticity of products like organic goods, wines, and others drives the segment growth.

The pharmaceuticals segment held the 18% market share in 2025 due to the focus on combating counterfeit drugs. The production of new drugs and the rise in patient-specific labeling increase the use of VDP labels. The focus on verifying drug authenticity and the interest in specialized drugs increase the adoption of VDP labels. The focus on scanning pharmaceutical inventory supports the segment growth.

The consumer goods segment held the 14% market share in 2025 due to the rising number of modern shoppers. The focus on securing serialized numbering and real-time ingredient tracking increases the use of VDP labels. The robust beverage companies and the increasing smart packaging in consumer goods accelerate the adoption of VDP labels. The geo-targeted variations boost the segment growth.

Asia Pacific dominated the market with a 33% share in 2025 and is expected to grow at the fastest CAGR of 8.3% during the forecast period. The burgeoning shopping on the e-commerce platform across Asian countries and the investment in the automated printing machinery increase demand for variable data printing labels. The brand protection demand and the exploding consumer goods increase the use of variable data printing labels. The consumer's strong focus on dynamic parcel tracking and the rise in targeted product packaging increase the use of variable data printing labels, driving the overall market growth.

China

India

North America held the 29% market share in 2025. The stringent regulations for product counterfeiting prevention and the expansion of D2C fulfilment increase demand for variable data printing labels. The high availability of electrophotography presses and the expansion of personalised packaging in brands increase demand for variable data printing labels. The localized marketing campaigns of brands support the overall market growth.

United States

Canada

Europe held the 25% market share in 2025. The robust anti-counterfeiting measures in the food industry and the focus on inventory management increase the use of variable data printing labels. The brands' shift to smart packaging and advancing digital printing technologies increases the adoption of VDP labels. The robust serialization requirements across the pharmaceutical sector and the focus on tracking goods increase the use of VDP labels, supporting the overall market growth.

Germany

The stringent pharmaceutical directives and the high volume of parcel shipping increase the adoption of VDP labels.

The focus on minimizing inventory waste and the requirement for advanced track-and-trace help with expansion.

United Kingdom

Latin America held the 7% market share in 2025. The regulations for pharmaceutical serialization and the interest in tailored local marketing campaigns increase the adoption of VDP labels. The stringent agriculture export regulations and the well-established production base in Mexico increase demand for VDP labels. The high utilization of track-and-trace labeling drives the market growth.

Brazil

Argentina

The Middle East & Africa held the 6% market share in 2025. The explosion of counterfeit goods and the stricter beverage labeling rules increases the use of VDP labels. The need for covert security features in the healthcare industry and supermarket expansion increases the adoption of VDP labels. The expanding regional logistics hubs and stricter labeling standards support the overall market growth.

UAE

Saudi Arabia

| Rank | Company | Headquarters | Country | Major Contribution to Variable Data Printing Labels Market | Key Packaging Products and Services |

| 1. | HP Inc. | California, United States | United States | The company focuses on algorithmic mass customization and creates smart labels. The company offers AI-driven automation. | HP Indigo V12 Digital Press HP Indigo 200K Digital Press HP Indigo Secure TIJ 2.5 PrintOS TIJ 1.0 |

| 2. | Xerox Corporation | Norwalk, Connecticut, United States | United States | The company invested $20 million in digital label printing expansion. The company focuses on Native VDP scripting and ultra-fast workflow. | XMPie Solutions Xerox FreeFlow VI Suite Xerox PrimeLink & Iridesse Production Press |

| 3. | Canon Inc. | Tokyo, Japan | Japan | The company focuses on hyper-customization of single labels and integrates workflow software. | LabelStream 4000 Series LabelStream LS2000 varioPRINT 140 Series |

| 4. | Avery Dennison Corporation | Mentor, Ohio, United States | United States | The company offers linerless labeling & specialty adhesives for developing labels. The company also provides intelligent labels and an industry-leading printer. | Direct Thermal Labels AD XeroLinr DT TT Labels DT Film Options |

| 5. | 3M Company | Saint Paul suburb of Maplewood, Minnesota, United States | United States | The company offers thermal transfer technologies and premium acrylic adhesives for the production of labels. | 3M Thermal Transfer Printable Labels 3M Press Printable Label Materials 3M Versatile Print Label Material |

By Printing Technology

By Label Type

By Material

By Printing Format

By Application

By End-use Industry

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarVariable Data Printing Labels Market