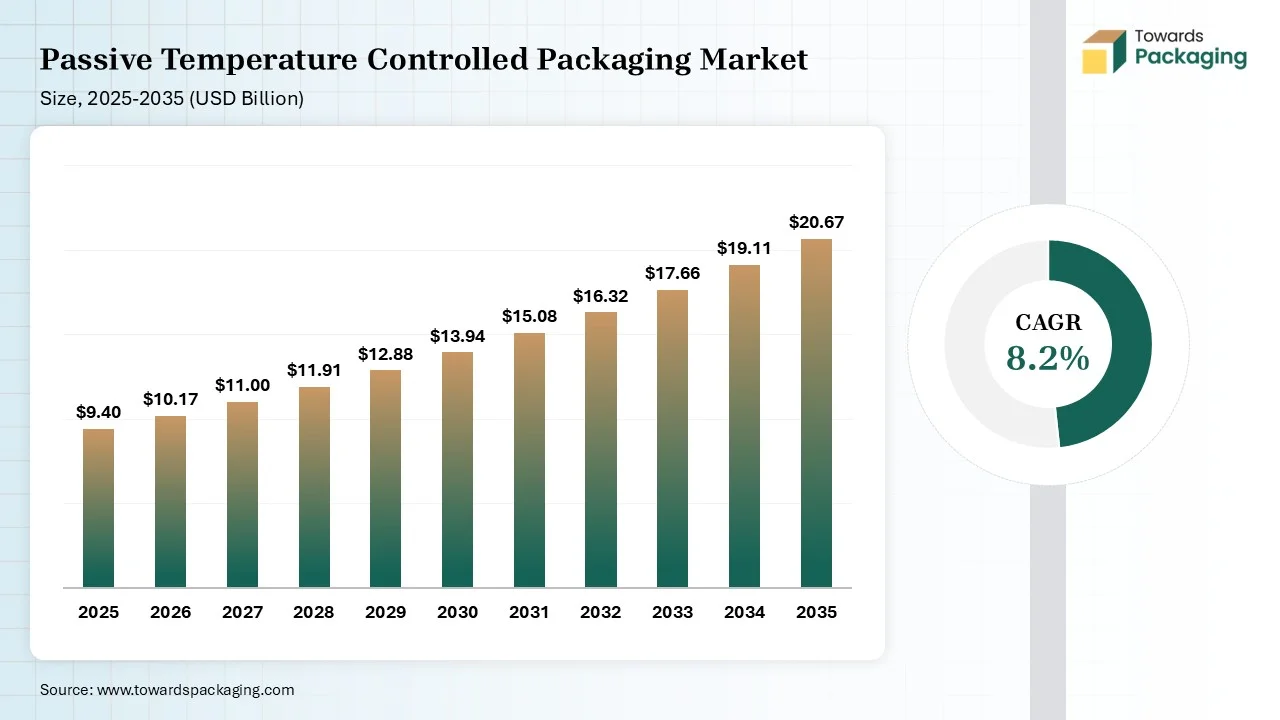

The passive temperature-controlled packaging market is projected to grow from USD 10.17 billion in 2026 to USD 20.67 billion by 2035, registering a CAGR of 8.2% during the forecast period. The report provides detailed insights into market size, segment-wise data by product type and application, and regional analysis across North America, Europe, Asia-Pacific, and other key regions. It also covers leading companies, manufacturers, and suppliers, along with competitive analysis, value chain evaluation, and trade data, offering a complete view of industry dynamics.

Market Size (2025): USD 9.4 Billion

CAGR (2025–2035): 8.2%

Market Volume (2025): 6.8 Billion Units (Shipments)

Passive temperature controlled packaging racks and a particular temperature series without any external power. Rather, it applies insulated materials and refrigerants, such as phase change materials, to make sure products stay fresh with the assistance of logistics and transport. By making sure stable temperatures in terms of cold chain passive temperature-controlled packaging for food delivery are maintained, it is crucial to protect the products and serve high-quality products.

The technological growth in passive temperature-controlled packaging is perfect in coordination and communication via technology that can lower flows and delays in the complete supply chain. For instance, high-level coordination lowers transport time and develops inventory management. Technology allows an effective shipment path and fast delivery times. Additionally, data analytics also enables us to personalize any business services and communication to align with particular end-user choices. On the other hand, energy-effective logistics and route optimization have led to lower carbon emissions, which are similar to smaller eco–friendly footsteps. Environment-friendly shipping solutions and packaging can meet any corporate social responsibility programs.

The insulated shippers segment dominated the market with 28% share in 2025 because it has refrigerants and vacuum-insulated panels depending on phase-change materials that have captured industry share from regular expanded polystyrene (EPS) and polyurethane designs, dry ice, and gel packs. Advanced result shippers highlight vacuum-insulated panels, controlled compression lids, and +5 degrees Celsius material, which delivers accurate and constant melt-freeze transformation for temperature control. The shippers have a proximate weight of 50% less than regular insulated shippers and the cut distribution amount.

The phase change materials (PCM) packaging segment held the 18% market share in 2025, and it is also expected to grow at the fastest CAGR of 10.50% during the forecast period. They absorb and release heat at defined temperatures. PCMs can be designed to track particular ranges between 2 degrees Celsius and 8 degrees Celsius or 20 degrees Celsius. They finalize or melt at such complicated settled points by ensuring thermal stability. PCM packs are reusable in nature and generally recognized as non-toxic ones. This lowers disposal and shipping limitations.

Insulated containers segment held the 20% market share in 2025 because such boxes are pointed as non-operational reefer containers, which are here to be a solution for various issues, since they can protect temperature pollutants during logistics. These containers frequently have double walls that are vacuumed to mitigate the actual movement of cold and heat between the interior and exterior, which are packed to prevent moisture and condensation.

The expanded polystyrene (EPS) segment dominated the market with 30% share in 2025 because of its potential to provide constant thermal insulation while being lightweight and convenient to handle. The closed -cell structure of an EPS grabs air that behaves as a productive barrier against heat transfer.

Such a design enables EPS thermal insulation packaging to track internal temperature over an expanded time when they are used along with coolants such as dry ice or gel packs. EPS packaging for healthcare is predominantly crafted as insulated containers, which are ideal for contents from external temperature changes.

Cardboard/Paper-based insulated segment held the 18% market share in 2025, and it is also expected to grow at the fastest CAGR of 10.80% during the forecast period. Paper-based cellulose operates on the exact principle, which is fixed into air to reduce heat transfer, by making a deep network of air pockets that opposes the exchange between the outside surroundings and payload. They are technically recyclable in nature, which results in less landfill.

The polyurethane (PU) foam segment held the 20% market share in 2025 because they play a crucial role in making durable and insulated storage systems, like containers, tanks, and packaging materials. Such coatings prevent pollutants that are caused by physical effects, temperature changes, and chemical exposure that affect pharmaceutical products during distribution. Cold chain logistics frequently use polyurethane foam coatings as thermal insulators to track low temperatures for temperature-sensitive vaccines and biologics.

The 2-8 degrees Celsius (Chilled) segment dominated the market with 40% share in 2025. Temperature-fragile biopharmaceuticals, allergenics, medicinal products, and vaccines are mostly less in physical volume but high in terms of monetary value, which need the protection of a specified temperature range from 2 to 8 degrees Celsius. Such temperature capability of such products will be reduced, or overall lost, if the 2–8-degree Celsius temperature series are not tracked at any point from production until the exact time period they have been admitted to patients.

The -80 degree Celsius (Ultra-Low/Deep Frozen) segment held the 10% market share in 2025 and is also expected to grow at the fastest CAGR of 10.20% during the forecast period. Ultra-low temperature freezers typically running at negative 80 degrees Celsius; however, they are capable of temperatures that come to negative 90 degrees in terms of advanced designs, which deliver as the pharmaceutical sector’s initial long-term biological storage solution. The initial compressors get chills at an intermediate-temperature refrigerant, as it cools down as a secondary refrigerant that has the potential of reaching ultra-low temperatures.

The -20-degree Celsius (Frozen) segment held the 30% market share in 2025 because it runs at sub-zero temperatures, which are generally between 18 degrees Celsius and -25 degrees Celsius, as such warehouses are for products that should stay frozen solid. Seafood, ice cream, and frozen meals have stayed in terms of microbial activity, which protects products for several months.

Cold storage prevents businesses and patients by making sure medicines stay effective. Non-compliance can point to cost checking, product loss, and the regulatory searches, such as EU GMP and GDP Annex 15, which give importance to brands that should check storage spaces and tracking systems to ensure integrity.

The pharmaceuticals segment dominated the market with 45% share in 2025 because passive temperature-controlled packaging assists in storing temperature-sensitive medicines securely while transport and storage by tracking products inside their checked temperature range. Such packaging are a crucial part of the pharmaceutical cold chain that prevents the quality of medicines from being compromised from manufacturing to patients. It plays a crucial role in the pharmaceutical cold chain along with transport, logistics, and tracking.

The healthcare & diagnostics/biotech segment held the 15% market share in 2025, and it is also expected to grow at the fastest CAGR of 9.80% during the forecast period. Like regular drug distribution, precision medicine counts smaller batch sizes, which are unmatched, and counts manufacturing models, and is strong in delivery windows. Such highly tailored procedures cannot be assisted by static or strong logistics designs. It needs flexible cold chain solutions, real-time management, live communication, and constant planning to make sure therapies reach the patients in optimal surroundings.

The food & beverages segment held the 30% market share in 2025, as temperature control packaging commonly uses insulated walls. Such walls are designed from corrugated cardboard, foam, or thermal liners. They protect the heat from the current entering or leaving the box. A sealed bag or box does not enable external air to push the internal surroundings. This manages food fresh and is constant during logistics. Gel packs, ice packs, or dry ice are kept inside boxes that manage the coldness of the food. Such cooling agents maintain the essential temperature for many hours. Particularly businesses use smart sensors inside boxes. They manage temperature in real time.

The single-use packaging segment dominated the market with 70% share in 2025, as reusable passive shippers count durable boxes, which frequently have hollow walls that have insulation. PCM packs are kept around the center point of the payload. Single-use shippers count Styrofoam boxes and insulated cardboard cartons. Passive temperature-controlled packaging is a complicated part of the cold chain. Such packaging solutions are generally the outcome of system engineering and materials.

The reusable packaging systems segment held the 30% market share in 2025, and it is also expected to grow at the fastest CAGR of 9.80% during the forecast period. It serves different environmental and economic benefits. By allowing several uses, they lower waste and lower the carbon footprint. They are frequently crafted to be more stackable, which updates storage and lowers space demands. Such an update includes more effective logistics, updates inventory management, and develops complete operational smoothness.

Asia Pacific dominated the market with 30% share in 2025 and is expected to have the fastest growth in the market with 9.50% CAGR during the forecast period. Current demand is totally developed for acceptance of IoT-allowed smart packaging that delivers real-time temperature tracking and predictive tracking. The move towards biodegradable, eco-friendly materials meets with worldwide sustainability goals. Robotics integration and automation are packaging procedures that lower costs and develop reliability. Additionally, regulatory frameworks are becoming strong around cold chain reliability, which markets products to update secure packaging and tamper-evident solutions.

India Passive Temperature Controlled Packaging Market Trends:

In India, counterfeit medications have remained a main threat to brand equity and patient safety, especially in developing industries. To use this, the sector is giving importance from passive enclosures to active, which is smart packaging. Regular static QR codes have proven reliable against standard counterfeiters who just copy them. Products are excessively mixing Radio Frequency Identification (RFID) and Near-Field Communication (NFC) into secondary packaging.

North America held the 32% market share in 2025, as it points to tailored packaging that pushes products, specifically biologics, pharmaceuticals, and sensitive products that stay within a particular temperature range during storage and transportation. This industry has become excessively important as the urge for fragile products develops, which is linked with the growth of healthcare logistics and e-commerce. At current times, the North American market is experiencing a positive development, which is driven by growing user awareness, regulatory requirements, and advancements in packaging technologies. The growing importance of vaccines and biopharmaceuticals proposes further demand for relevant temperature control solutions.

The current scenario of U.S. passive temperature-controlled packaging is officially marked by fast technological growth, growing regulatory pressures, and a flexible supply chain design. In the biotechnology and pharmaceutical sphere, the importance of cold chain reliability is growing, as pointed out by the fast growth of vaccines, biologics, and gene therapies. The complications of tracking strong temperature series while transportation have led to inventions in active-cooling systems, phase-change materials, and real-time tracking technologies. This segment is also excessively encouraged by regulatory frameworks such as EMA and FDA, which have compulsion and traceability, which has further market development.

By Product Type:

By Material Type:

By Temperature Range:

By End-Use Industry:

By Duration/Usage Type:

By Regions:

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPassive Temperature Controlled Packaging Market