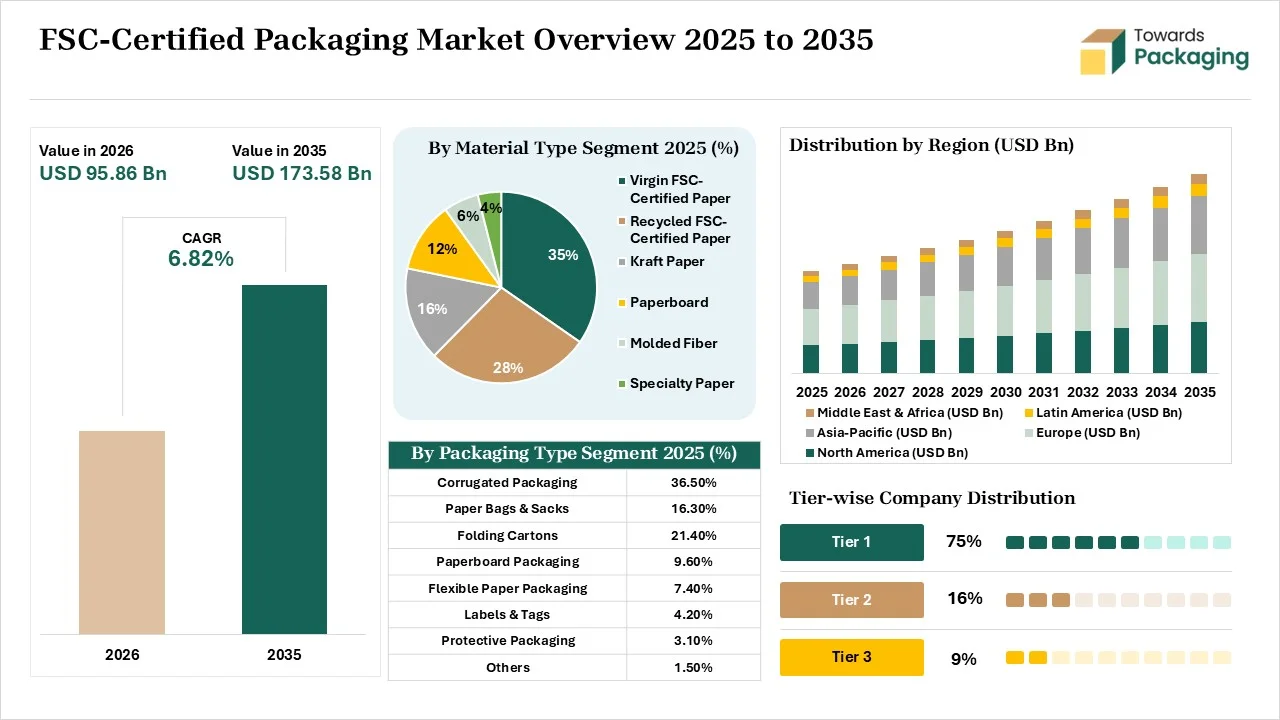

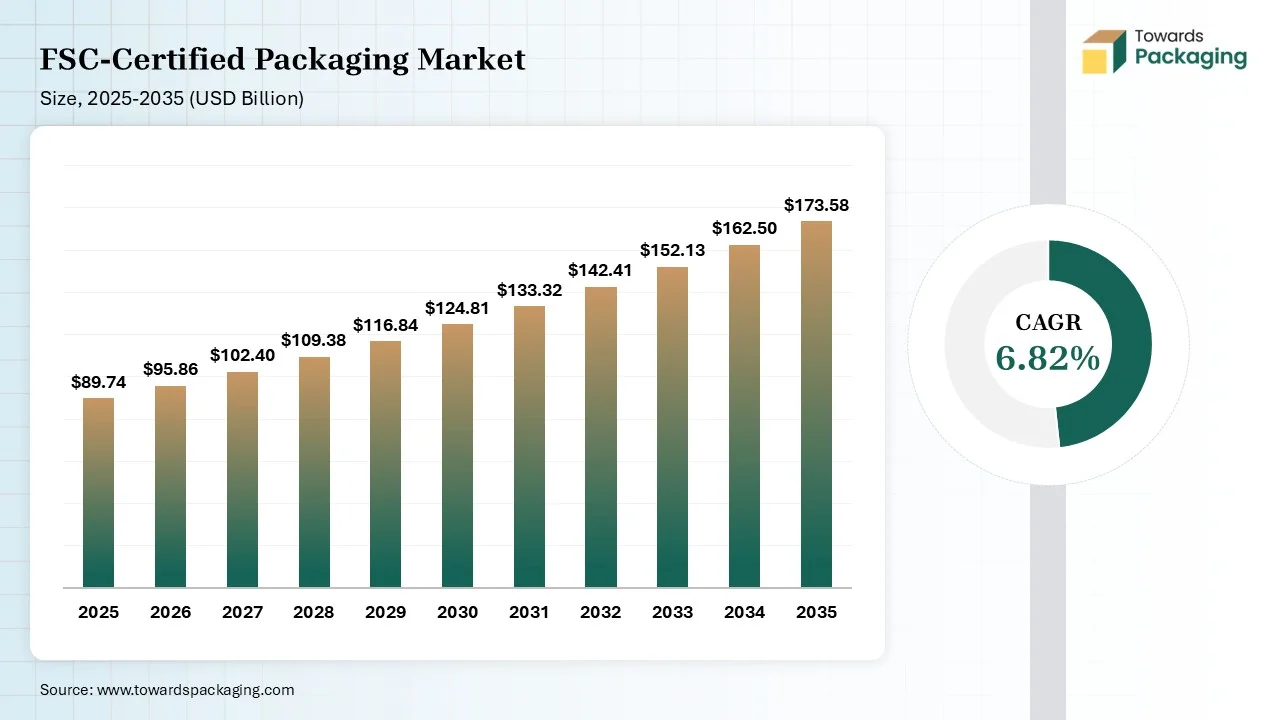

The FSC-certified packaging market is projected to grow from USD 95.86 billion in 2026 to USD 173.58 billion by 2035, registering a CAGR of 6.82% during the forecast period. The report covers detailed market size analysis, revenue forecasts, segment-wise performance, regional insights, market trends, competitive analysis, company profiles, value chain analysis, trade statistics, manufacturers and suppliers analysis, pricing trends, production and consumption data, import-export analysis, distribution channels, and growth opportunities. It also examines how rising corporate sustainability initiatives, increasing demand for plastic alternatives, and the growing preference for ethical supply chains are shaping market expansion.

FSC-certified packaging is the process of sourcing packaging materials from responsibly managed forests. It supports building brand trust and protecting biodiversity. The types of FSC packaging are FSC recycled, FSC 100%, and FSC Mix. It offers characteristics like CoC traceability, brand transparency, sustainable sourcing, and high recyclability. It offers benefits like premium consumer appeal, supply chain transparency, environmental preservation, circular economy support, and social responsibility. The common applications are paper coffee cups, cosmetic product boxes, juice cartons, mailing boxes, takeaway trays, and retail boxes.

For instance, in November 2025, UFP Packaging Corrugated Division acquired SFI and FSC Chain of Custody Certifications. The certification ensures fiber derived from sustainably managed sources. The certification supports environmental stewardship and responsible sourcing.

The FSC-certified packaging market growth is driven by the burgeoning consumer eco-consciousness, high e-commerce deliveries, corporate CSR goals, shifting circular economy, popularity of certified paper packaging in FMCG products, transition away from waste-generating packaging, demand for CoC traceability, and the growing green public procurement policies.

The FSC-certified packaging market is going through technological developments like software integration, blockchain, integration of intelligent indicators, robotics, and embedded codes. The technological developments are growing due to the demand for optimizing layouts, enabling lightweighting, and maintaining transparent records. The strong development in the market is the incorporation of AI, which helps in verifying sourcing claims.

AI identifies flag inconsistencies and supports the sustainable design of packaging. AI guarantees green claims and supply chain traceability. AI inspects packaging lines and verifies forestry origins. AI supports material optimization and measures carbon footprint. AI helps in aggregating supplier certificates and supports minimal material use. Overall, AI helps in corporate value creation and eco-design.

The stage acquires raw materials such as FSC Mix, FSC 100%, and FSC Recycled.

The stage includes steps like certified forest management, pulping & paper manufacturing, board conversion, printing, cutting, finishing, packing, labeling, and fulfilment.

Design includes material selection, minimizing waste, and eco-friendly finishes. Prototyping involves developing digital models, creating physical models, functionality testing, and stress testing.

The corrugated packaging segment dominated the market with 36.5% share in 2025. The growing outbound shipping and the strong growth in FMCG increase the use of corrugated packaging. The thriving online sales market and the huge interest in lightweight packaging increase the adoption of corrugated packaging. The exceptional circularity and high corporate demand help with expansion. The superior stacking strength, structural integrity, and low shipping costs of corrugated packaging drive the segment growth.

The flexible paper packaging segment held the 7.40% market share in 2025 and is expected to grow at the fastest CAGR of 8.2% during the forecast period. The focus on mitigating carbon-neutrality targets and the brand's interest in packaging accountability increase the adoption of flexible paper packaging. The focus on retail space efficiency and the availability of compostable barrier coatings increases the adoption of flexible paper packaging. The increased packaging of fresh produce and the interest in lightweight paper cushioning increase the use of flexible paper packaging, supporting the segment growth.

The virgin FSC-certified paper segment dominated the market with 34.6% share in 2025. The pharmaceutical safety regulations and the demand for highly detailed branding increase the adoption of FSC-certified paper. The high use of FSC Mix labels and the focus on avoiding food contact with chemical traces increase the adoption of virgin FSC-certified paper. The protection of heavy loads and the strong paper recycling infrastructure increase the adoption of virgin FSC-certified paper. The premium aesthetics, bright white surface, and exceptional structural strength of virgin FSC-certified paper drive the segment growth.

The recycled FSC-certified paper segment held the 27.80% market share in 2025 and is expected to grow at the fastest CAGR of 7.8% during the forecast period. The focus on lowering the harvest of virgin trees and the presence of major global brands increase the adoption of recycled FSC-certified paper. The focus on pre-consumer waste and the need to reduce the processing of virgin wood pulp increases the adoption of recycled FSC-certified paper. The growing carbon emissions in the development of new paper and the growing independent sourcing increase the adoption of recycled FSC-certified paper, supporting the segment growth.

The FSC Mix segment dominated the market with 51.4% share in 2025. The growing mass-market packaging and the huge interest in paper-based packaging increase the demand for FSC Mix. The focus on avoiding human rights violations and the development of molded fiber trays increases the use of FSC Mix. The focus on transparent traceability and material supply flexibility increases the adoption of FSC Mix. The optimal cost and the stricter sourcing integrity of FSC Mix drive the segment growth.

The FSC 100% segment held the 31.20% market share in 2025 and is expected to grow at the fastest CAGR of 7.5% during the forecast period. The exploding luxury brands and the brands' focus on reputational risks increase the use of FSC 100%. The brand's focus on preserving biological diversity and uncompromising green claims increases the adoption of FSC 100%. The expanding global retailers and the focus on enhancing social benefits increase the use of FSC 100%. The high consumer trust on FSC100% supports the segment growth.

The flexographic printing segment dominated the market with 38.8% share in 2025. The explosion of e-retail and the growing continuous print runs in FMCG increase the adoption of flexographic printing. The focus on enhancing final product sustainability and the increased development of micro-flue corrugated board increase the adoption of flexographic printing. The substrate versatility, brand provenance, inline manufacturing efficiency, and superior economics of flexographic printing drive the segment growth.

The digital printing segment held the 18.90% market share in 2025 and is expected to grow at the fastest CAGR of 8.6% during the forecast period. The shift away from time-consuming setup and the growing demand for identical boxes increase the adoption of digital printing. The rise in small batch production and the interest in eco-friendly inks increases the use of digital printing. The growing hyper-personalization of packaging and the expansion of modern sustainable substrates increase the adoption of digital printing. The supply chain agility, minimal waste, and hyper-customization of digital printing support the segment growth.

The food & beverage segment dominated the market with 42.7% share in 2025. The growing label demand on takeout boxes and the adoption of fiber-based packaging in F&B companies increase the use of FSC-certified packaging. The food industry's focus on meeting health standards and the surging online meal-kit services increase the adoption of FSC-certified packaging. The strong beverage producers and the eco-aware consumers increase the adoption of FSC-certified packaging, driving the segment growth.

The e-commerce segment held the 18.60% market share in 2025 and is expected to grow at the fastest CAGR of 8.5% during the forecast period. The brand's focus on providing an unravelling unboxing experience to their customers increases the use of FSC-certified packaging. The e-commerce company's transition towards corrugated board helps with expansion. The burgeoning e-commerce shoppers and the focus on providing a premium e-commerce experience increase the use of FSC-certified packaging. The focus on lowering business risk supports the segment growth.

The direct sales segment dominated the market with 59.8% share in 2025. The demand for independently verified guarantees and the interest in green unboxing experiences increase the adoption of direct sales. The waste-reduction laws and the focus on avoiding middleman communication increase the use of direct sales. The rise of direct shipping and the expanding premium retail channels increases the use of direct sales. The focus on eliminating third-party verification increases adoption of direct sales, driving the segment growth.

The online/B2B platforms segment held the 11.70% market share in 2025 and is expected to grow at the fastest CAGR of 8.8% during the forecast period. The demand for transparent supply chains and the increased acquisition of eco-friendly options increase the adoption of online sales. The need to eliminate regional intermediaries and focus on scalable raw material sourcing increases the use of B2B platforms. The preference for certified suppliers and the rise in bulk ordering of custom packages increase the use of B2B platforms. The simplified compliance management in online marketplaces supports the segment growth.

Europe dominated the market with 35.6% share in 2025. The EUDR regulation and the stringent waste reduction policies increase the use of FSC-certified packaging. The focus on product transparency and the protection of brand credibility increases the use of FSC-certified packaging. The major FMCG giants and the advanced waste management infrastructure increase the use of FSC-certified packaging. The interest in FSC-certified kraft paper drives the market growth.

North America held the 27.40% market share in 2025. The state regulations in countries like Canada and the higher demand for verifiable sourcing increase the adoption of FSC-certified packaging. The focus on zero-deforestation forests and the internal sustainability targets of major brands increases the use of FSC-certified packaging. The robust integrated forestry resources and the explosive e-commerce increase the use of FSC-certified packaging, supporting the market growth.

Asia Pacific held the 25.80% share in the market in 2025 and is expected to grow at the fastest CAGR of 8.1% during the forecast period. The phase-out of complex multilayer plastics and the rise in live-stream sales increase the adoption of FSC-certified packaging. The interest in FSC-sourced paper packaging helps with expansion. The consumer shift to transparent packaging and the rising online shopping have increased the use of FSC-certified packaging. The hyper-growth in food delivery boosts the market growth.

Latin America held the 6.10% market share in 2025. The anti-plastic legislation and the burgeoning online retail increase the adoption of FSC-certified packaging. The growing government partnerships with forestry institutes help with expansion. The green packaging mandates and the growing consumer goods export increase the adoption of FSC-certified packaging. The explosion of fast-food franchises supports the market growth.

The Middle East & Africa held the 5.10% market share in 2025. The plastic curbing initiatives and the stringent environmental laws increase the adoption of FSC-certified packaging. The growing cosmetics export and the rising parcel volumes increase the use of FSC-certified packaging. The strong personal care companies and the increasing adoption of eco-friendly substrates increase the use of FSC-certified packaging, boosting the market growth.

| Rank | Company | Headquarters | Country | Major Contribution to FSC-Certified Packaging Market | Key Packaging Products and Services |

| 1. | Smurfit Westrock | Dublin, Ireland | Ireland | The company focuses on sustainable forest management and the Chain of Custody tracking. The company focuses on creating deforestation-free packaging. | Heavy Duty Boxes, NatraLock Ultra Seal, Bag-in-Box Solutions, Retail Ready Packaging |

| 2. | Tetra Pak | Pully, Switzerland, and Lund, Sweden | Switzerland/Sweden | The company focuses on 100% responsible sourcing of raw materials. The company supplied FSC-labelled packages above 500 billion. | Tetra Pak Aseptic, Tetra Brik Aseptic, Tetra Fino Aseptic, Tetra Top, Tetra Pak Chilled, Tetra Rex Plan-based |

| 3. | Amcor | Zurich, Switzerland | Switzerland | The company acquires feedstocks from FSC-certified forests and develops custom paperboard solutions. | AmFiber Performance Paper, AmFiber Packpyrus, AmFiber Functional Paper, Custom Paperboard Solutions |

| 4. | International Paper | Memphis, Tennessee, United States | United States | The company acquires raw materials from third-party certified forests and focuses on certified forest management. | Corrugated Containers, Food & Beverage Packaging, Specialty Paperboard, Corrugated Sheets, Retail Displays |

| 5. | Mondi Group | Weybridge, England, United Kingdom | United Kingdom | The company focuses on responsible fiber sourcing, and it invested €200 million in the upgradation of Duino Mill. | Containerboard, Sack Papers, Flexible Papers, Corrugated Board, Paper Bags |

By Packaging Type

By Material

By Certification Type

By Printing Technology

By End-Use Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarFSC-Certified Packaging Market