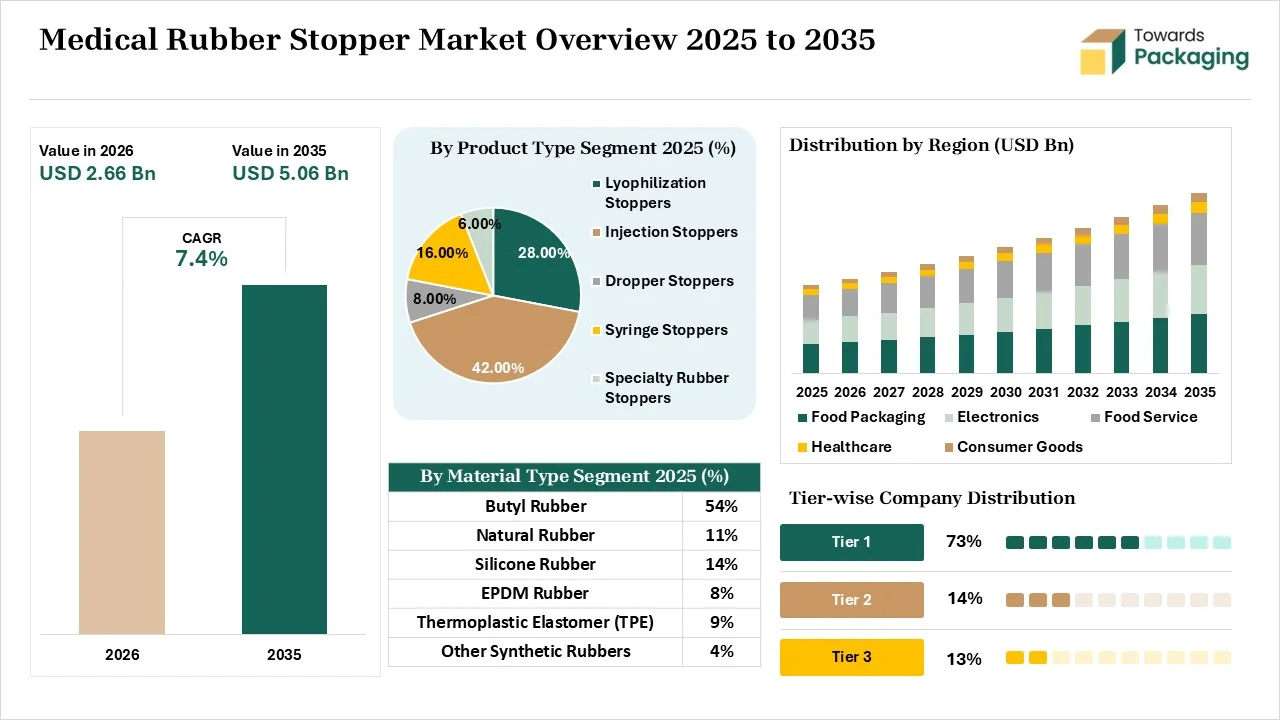

The Medical Rubber Stopper Market is projected to grow from USD 2.66 billion in 2026 to USD 5.06 billion by 2035, registering a CAGR of 7.40%. The report provides detailed market size forecasts, segment-wise analysis, regional performance, competitive landscape, company profiles, value chain analysis, trade insights, and comprehensive data on manufacturers, suppliers, growth opportunities, and key industry trends.

A medical rubber stopper is a non-toxic seal used in the packaging of pharmaceutical products. It has a self-healing design and offers moisture control. It possesses characteristics like chemical inertness, superior gas barrier, low extractables, superior purity, and resealability. The materials like bromobutyl rubber, butyl rubber, natural rubber, and chlorobutyl rubber are used in the development of medical rubber stoppers. It offers benefits like contamination protection, high thermal stability, and tamper evidence. The applications of medical rubber stoppers are vaccines, IV fluid systems, sterile pharmaceutical vials, prefilled syringes, and others.

The medical rubber market growth is driven by the thriving chronic diseases, expanding veterinary healthcare, transition to RTU components, growing vaccination drives, worldwide pharmaceutical manufacturing expansion, rise in biosimilars, popularity of therapeutics, rigorous expectations in drug contamination, and innovations in coated materials.

The medical rubber stopper market is going through several technological developments driven by material innovation, stringent regulatory standards, and contamination reduction. Technological developments like automated manufacturing, computer vision, predictive analytics, and smart packaging help in high-speed manufacturing and ensure exact consistency. The prominent development in the market is that AI helps in precise stopper design.

AI supports advanced material design and prevents drug contamination. AI supports high-volume production and flags deformities in medical rubber stoppers. AI prevents expensive production downtime and easily analyzes complex sterilization cycles. AI automates traceability tracking and prevents critical shortages of stoppers. AI checks seal imperfections and monitors factory sensors. Overall, AI supports precision manufacturing and vision inspection in medical rubber stoppers.

Raw materials like halobutyl rubbers, plasticizers, curing systems, pigments, fluoropolymer coatings, synthetic polyisoprene, fillers, and antioxidants are required.

Material processing steps are compounding, calendering, trimming, surface treatment, and washing. Conversion focuses on calendering, vulcanization, and trimming.

Design focuses on material chemistry, surface coatings, and geometric optimization. Prototyping includes low-fidelity proof-of-concept, functional prototyping, and pre-production pre-testing.

The injection stoppers segment dominated the market with 42% share in 2025 due to the preference for injectable therapies. The focus on drug contamination prevention and the rise in complex chemical medical formulations increase the use of injection stoppers. The interest in pre-validated closures and the robust growth in vaccines increases the adoption of injection stoppers. The high sterility and unmatched sealing integrity of injection stoppers drive the segment growth.

The syringe stoppers segment held the 16% market share in 2025 and is expected to grow at the fastest CAGR of 9.3% during the forecast period due to the rising use of prefilled syringes. The interest in self-administered therapies and the need to maintain medication stability increase the use of syringe stoppers. The rise in monoclonal antibodies and the prevention of extractables from drugs increases the use of syringe stoppers. The high heat resistance, excellent purity, and leachables control in syringe stoppers support the segment growth.

The butyl rubber segment dominated the market with 54% share in 2025. The degradation prevention of sensitive drugs and the development of modern biologics increase the adoption of butyl rubber. The high-temperature sterilization methods and the presence of international pharmaceutical guidelines increase the adoption of butyl rubber. The use of parenteral drugs and the need for protection in sensitive medications increases the adoption of butyl rubber. The zero permeability, needle puncture integrity, and exceptional gas barrier of butyl rubber drive the segment growth.

The thermoplastic elastomer (TPE) segment held the 9% market share in 2025 and is expected to grow at the fastest CAGR of 9.6% during the forecast period. The focus on reducing chemical leachable risks in vaccines and the high utilization of multi-dose vials increase the use of TPE. The robust healthcare standards and the prevention of altering drug chemistry increase the adoption of TPE. The rise in single-use applications and the expanding multi-component designs increases the adoption of TPE. The high purity, excellent sealing, and biocompatibility of TPE support the segment growth.

The fluoropolymer coated segment dominated the market with 38% share in 2025 and is expected to grow at the fastest CAGR of 9.1% during the forecast period. The interest in mRNA therapies and the focus on reducing friction in pre-filled syringes increase the adoption of fluoropolymer-coated medical rubber stoppers. The prevention of chemical leaching in medicines and the growing aseptic manufacturing of medicines increases the use of fluoropolymer-coated medical rubber stoppers. The silicone-free gliding, zero permeability, and superior chemical inertness of fluoropolymer-coated medical rubber stoppers drive the segment growth.

The uncoated segment held the 31% market share in 2025. The growing pharmaceutical industries and the development of specific medical formulations increase the use of uncoated medical rubber stoppers. The development of non-aggressive medications and the focus on lowering oral medication risk have increased the use of uncoated medical rubber stoppers. The regulatory stability, exceptional CCI, and cost-effectiveness of uncoated medical rubber stoppers support the segment growth.

The steam sterilization compatible segment dominated the market with 36% share in 2025. The growing use of autoclave processing and the focus on destroying biological contaminants increase the use of steam sterilization. The surge in commercial drug manufacturing and the focus on improving sealing performance in vial assembly increase the use of steam sterilization. The unmatched penetration, material compatibility, cost-effectiveness, and excellent reliability of steam sterilization drive the segment growth.

The multiple sterilization compatible segment held the 27% market share in 2025 and is expected to grow at the fastest CAGR of 9% during the forecast period. The production of high-volume medications and the development of animal injectables increase the use of multiple sterilization methods. The rising protein-based therapies and the need to provide supply-chain flexibility increase the use of multiple sterilization methods. The advanced material technologies and the CDMO expansion support the segment growth.

The injectable drugs segment dominated the market with 57% share in 2025. The expansion of modern injectables and the tightening of safety standards in injectable drugs increases the use of medical rubber stoppers. The rise in autoimmune disorders and the strong focus on contamination prevention in injectable medications increase the use of medical rubber stoppers. The growing immunization initiatives and the thriving general injectable industry increase the adoption of medical rubber stoppers, driving the segment growth.

The cell & gene therapy products segment held the 7% market share in 2025 and is expected to grow at the fastest CAGR of 11.4% during the forecast period. The requirement for ultra-low temperature storage and the prevention of trace materials reaction with cell therapy increases the use of medical rubber stoppers. The high utilization of CGT products and the rising commercial approvals of CGT increase the use of medical rubber stoppers. The surging active clinical trials of CGT and the huge investment in regenerative medicines boost the overall segment growth.

The pharmaceutical companies segment dominated the market with 48% share in 2025. The regulatory compliance in pharmaceutical packaging and the production of sensitive parenteral drugs increases the use of medical rubber stoppers. The rapid development of low-leachable stoppers and the rise in defect-free operations increase the use of medical rubber stoppers. The development of high-volume sterile injectables and the thriving vaccine industry increases the use of medical rubber stoppers. The popularity of auto-injectors drives the segment growth.

The biotechnology companies segment held the 18% market share in 2025 and is expected to grow at the fastest CAGR of 9.5% during the forecast period. The growing sensitivity of biologics and the advancements in biotech increase the use of medical rubber stoppers. The development of pre-sterilized RTU stoppers helps with expansion. The shift to biosimilars and the expansion of bioprocessing capacities increase demand for medical rubber stoppers. The interest in silicone-free stoppers and the preference for specialized elastomeric closures support the segment growth.

North America dominated the market with a 33% share in 2025. The high consumption of complex biologics and the high demand for chemically inert closures increase the adoption of medical rubber stoppers. The availability of pre-validated rubber components and the focus on preventing drug leaching increase the production of medical rubber stoppers. The surging temperature-sensitive biologics and the strong pharmaceutical packaging companies drive the market growth.

Asia Pacific held the 29% market share in 2025 and is expected to grow at the fastest CAGR of 9.5% during the forecast period due to the strong contract manufacturing organizations. The surging sterile injectable drugs and the burgeoning healthcare access increase demand for medical rubber stoppers. The favorable local manufacturing ecosystem and the sterilization compliance increase the use of medical rubber stoppers. The transition to advanced coated stoppers and the high requirements for medical packaging solutions support the market growth.

Europe held the 27% market share in 2025. The stricter guidelines for managing packaging integrity and the expansion of chronic care therapeutics increase the adoption of medical rubber stoppers. The European companies' investment in biodegradable compounds and the rise in smart packaging increase the development of innovative medical rubber stoppers. The surge in patient-centric packaging boosts the market growth.

Latin America held the 6% market share in 2025 due to the generics expansion. The presence of major pharmaceutical companies and the demand for affordable healthcare increases the adoption of medical rubber stoppers. The expanding biosimilar drug industry and the regulations for drug approvals increase the use of medical rubber stoppers. The expanding injectable medical supplies and the focus on medicine sovereignty support the market growth.

The Middle East & Africa held the 5% market share in 2025 due to the rise in injectable drug packaging. The rise in foreign medical imports and the focus on preventing drug-container interactions increase the use of medical rubber stoppers. The prevalence of communicable diseases and the presence of large biotech distributors increase the use of medical rubber stoppers. The upgradation of vaccine storage facilities supports the market growth.

| Rank | Company | Headquarters | Country | Major Contribution to the Medical Rubber Stopper Market | Key Packaging Products and Services |

| 1. | West Pharmaceutical Services, Inc. | Pennsylvania, 19341, United States | United States | The company heavily invests in expanding the manufacturing of medical rubber stopper components, such as Ready-to-Sterilize. The company offers LyoTec Technology and FluoroTec Barrier Film. | LyoTec Stoppers, FluroTec Coated Stoppers, NovaPure Stoppers, AccelTRA Components |

| 2. | Datwlyer Holding Inc. | Aldorf, Switzerland | Switzerland | The company developed a second plant of complex fluropolymer-coated stoppers in Pune. The company offers UltraShield Film Coating and OmniFlex Coating Technology for the development of medical rubber stoppers. | UltraShield Stoppers, OmniFlex Stoppers, NeoFlex Plungers |

| 3. | Sumitomo Rubber Industries, Ltd. | Kobe, Hyogo, Japan | Japan | The company uses advanced polymer technology for the development of advanced medical rubber parts. | Vial Stoppers, Prefilled Syringe Stoppers |

| 4. | AptarGroup, Inc. | Crystal Lake, Illinois, United States | United States | The company expanded its elastomer component capacity in the United States and France. The company focuses on developing specialized rubber formulations. | PremiumFill, PremiumCoat |

| 5. | Daikyo Seiko, Ltd. | Sano, Tochigi, Japan | Japan | The company mainly invests in Daikyo RUV and Daikyo RSV elastomer stoppers. The company offers advanced lubricity coatings and Ultra-Clean D Sigma Elastomer Components. | Laminated Rubber Stoppers, Daikyo D Sigma |

By Product Type

By Material

By Coating Type

By Sterilization Compatibility

By Application

By End User

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarMedical Rubber Stopper Market