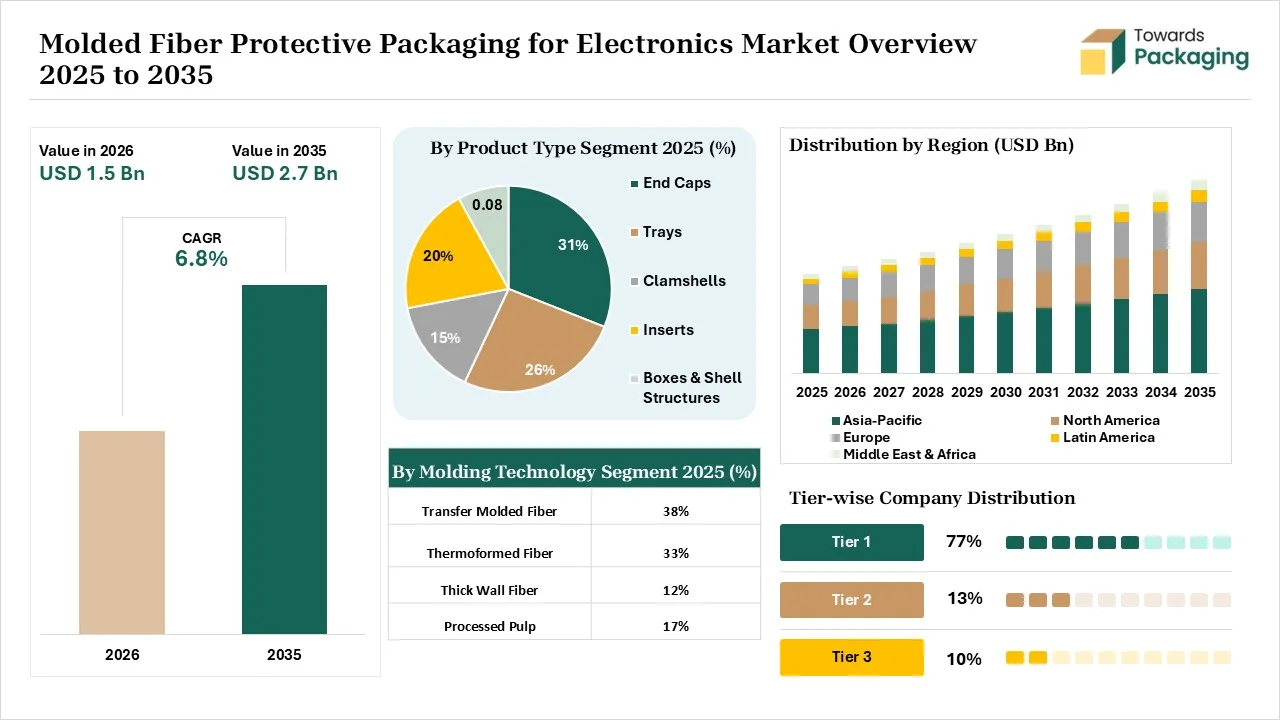

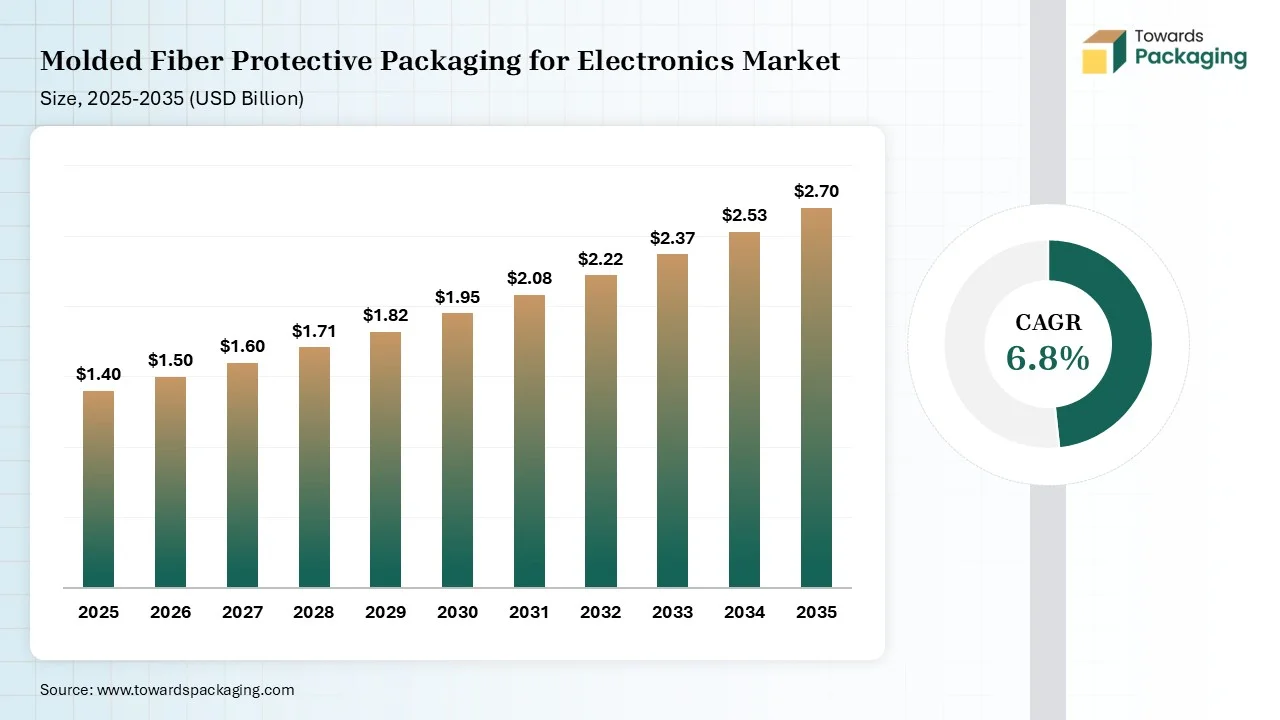

The molded fiber protective packaging for electronics market is projected to grow from USD 1.5 billion in 2026 to USD 2.7 billion by 2035, registering a CAGR of 6.8% during the forecast period. The market is benefiting from the increasing replacement of Styrofoam packaging, rising demand for sustainable electronics packaging, and stronger corporate ESG commitments. This report provides comprehensive market size forecasts, segment-level revenue analysis, regional demand trends, competitive benchmarking, company market share assessment, manufacturer and supplier profiling, value chain evaluation, trade and import-export analysis, production capacity insights, pricing trends, and strategic developments shaping the industry.

Molded fiber protective packaging for electronics is a sustainable cushioning material used to protect sensitive electronic devices. Its features are superior shock absorption, 100% biodegradability, stackability, custom-fit cradling, anti-static properties, excellent strength-to-weight ratio, and premium aesthetics. The highly used molded fiber protective packaging in electronics is thick-walled, transfer molded, and thermoformed. It offers benefits like high customizability and space efficiency. It is widely used in chargers, smartphones, laptops, smart home devices, and others.

The molded fiber protective packaging for the electronics market growth is driven by the focus on cost optimization, innovations in molding machinery, preference for online shopping, rise in securing delicate components, prohibitions on plastic use, focus on logistics efficiency, increased use of compostable packaging materials, and aesthetic advancements.

The molded fiber protective packaging for electronics market is witnessing technological developments like smart manufacturing, digital 3D modeling, precision engineering, and robotics. These developments are driven by demand for high-performance solutions and automated precision molding. The adoption of AI is the key technological development in the market, driven by demand for cost-effective packaging and increasing shock absorption.

AI creates the tailored shapes of molded fiber and analyzes the stress points of diverse pulp. AI reduces the use of excess material and analyzes the correct biodegradable matrix. AI detects surface irregularities and predicts maintenance needs for molding machines. AI easily adjusts packaging designs and detects structural weaknesses. Overall, AI helps from material selection to inventory management.

The stage acquires raw materials like old corrugated containers, mixed paper, bagasse, rice straw, oil-proofing agents, old newsprint, bamboo, wood cellulose, and anti-static additives.

Material Processing and conversion include steps like pulp preparation, vacuum forming, pressing, thermoforming, precision finishing, trimming, and custom coatings.

Package design focuses on custom cradling, structural engineering, and sustainability. Prototyping focuses on 3D printed molds, drop testing, and material iteration.

The end caps segment dominated the market with 31% share in 2025 due to the superior shock absorption. The focus on enhancing brand optics and the need to lower freight costs increases the adoption of end caps. The growing demand for highly efficient nesting and the sustainability goals in electronics companies increase the use of end caps. The anti-static properties, space optimization, custom-tailored fit, and logistics cost-efficiency of end caps drive the segment growth.

The trays segment held the 26% market share in 2025 due to the excellent drop protection. The focus on minimizing logistics costs and the preference for improving brand credibility increase the adoption of trays. The focus on protecting sensitive electronic components and the need to minimize electronic device transit damage increase the adoption of trays. The design flexibility, excellent shock absorption, and weight efficiency of trays support the segment growth.

The transfer molded fiber segment dominated the market with 38% share in 2025 due to its 100% recyclability. The growing mass production of electronics and the higher demand for electronic inserts increase the adoption of transfer molded fiber. The focus on preventing scratches on displays and the irregular device geometries increases the use of transfer molded fiber. The dimensional accuracy, exceptional shock absorption, excellent surface finish, and tailored fit of transfer molded fiber drives the segment growth.

The thermoformed fiber segment held the 33% market share in 2025 due to its unmatched sustainability and protective properties. The growing demand for plastic-like precision in packaging and the need for custom-fit cushioning increase the use of thermoformed fiber. The protection of sensitive circuit boards increases the adoption of thermoformed fiber. The premium aesthetics, 100% circularity, and chemical-enhanced durability of thermoformed fiber support the segment growth.

The recycled paper pulp segment dominated the market with 57% share in 2025 due to its manufacturing scalability. The growing demand for low-cost feedstocks and the focus on surface protection of electronic screens increase the adoption of recycled paper pulp. The electronics brands focus on enhancing environmental credentials, and the stringent global taxes increase the adoption of recycled paper pulp. The high customizability and excellent transit protection of recycled paper pulp drive the segment growth.

The virgin wood pulp segment held the 24% market share in 2025 due to the focus on a cleaner supply chain. The rise in banning foam plastics and the focus on low impurities increases the adoption of virgin wood pulp. The expansion of premium packaging applications increases the utilization of virgin wood pulp. The precise thermoforming, excellent mechanical strength, premium branding, and excellent purity of virgin wood pulp support the segment growth.

The smartphones & tablets segment dominated the market with 28% share in 2025 due to the rising global shipping volume of tablets &smartphones. The higher usage of touch-screen devices and the focus on exact fit in tablet models increase the use of molded fiber protective packaging. The need for sleek packaging and the expansion of smartphone brands increase the adoption of molded fiber protective packaging. The smartphone brands' move to eco-friendly materials drives the segment growth.

The consumer electronics segment held the 20% market share in 2025 due to the rise in online gadgets sales. Consumer electronics shift away from plastic clamshells, and the focus on protecting internal components increases the adoption of molded fiber protective packaging. The focus on saving warehouse space and the irregular device shapes increases the utilization of molded fiber protective packaging. The focus on avoiding regulatory penalties in consumer electronics supports the segment growth.

The cushioning protection segment dominated the market with 34% share in 2025 due to the growing demand for protecting product against vibration. The growing thinning of electronic devices and the rise in chemical enhancements increase the adoption of cushioning protection. The global growth in electronics shipments increases demand for cushioning protection. The need for perfect custom-fit plastic replacement drives the segment growth.

The shock & impact protection segment held the 24% market share in 2025 due to the demand for exceptional plastic replacement. The rise in e-commerce logistics and the focus on cost-effectiveness in reverse logistics increases demand for shock & impact resistance. The protection of brand reputation and the surge in advanced molded designs help with expansion. The burgeoning D2C electronics transition supports the segment growth.

The consumer electronics manufacturers segment dominated the market with 39% share in 2025 due to the electronics companies' focus on avoiding the utilization of single-use plastics. The growing demand for excellent shock absorption and the electronics brands' focus on zero-waste initiatives increase the use of molded fiber protective packaging. The large production volume and higher demand for premium packaging drive the segment growth.

The electronics OEMs segment held the 24% market share in 2025 due to the OEMs' focus on avoiding EPS use. The expansion of global manufacturing activity and the brand reputation focus increases the adoption of molded fiber protective packaging. The development of complex electronics and the need for exceptional product protection increase the use of molded fiber protective packaging, supporting the overall segment growth.

The direct sales segment dominated the market with 46% share in 2025 due to the demand for custom engineering. The increasing use of custom-molded inserts and the rise in specialized manufacturing increase the adoption of direct sales. The focus on collaboration with clients and the development of consistent finishes increases the adoption of direct sales. The supply chain security and high-volume contracts of direct sales drive the segment growth.

The packaging converters segment held the 27% market share in 2025 due to the growing demand for tailored molded solutions. The focus on excellent structural rigidity and corporate commitments increases the adoption of packaging converters. The increased use of highly lightweight materials and the development of customized fit increase the adoption of packaging converters. The OEM outsourcing trends support the segment growth.

Asia Pacific dominated the market in 2025 with a 44% share and is expected to grow at the fastest CAGR of 7.9% in the market during the forecast period due to the well-established consumer electronics manufacturing centers. The strong availability of agricultural residues and the presence of deep automation capabilities increase the adoption of molded fiber protective packaging for electronics. The burgeoning logistics networks and the focus on cushioning fragile devices increase the use of molded fiber protective packaging for electronics. The cost-effective manufacturing drives the segment growth.

China

India

North America held the 24% market share in 2025. The bans on the use of expanded polystyrene and the carbon footprint reduction goals in major electronic brands increase the adoption of molded fiber protective packaging for electronics. The development of smart home devices & the expansion of DTC online shopping enhances the use of molded fiber protective packaging for electronics. The green metrics in the region and the presence of advanced manufacturing techniques support the market growth.

United States

Canada

Europe held the 21% market share in 2025. The high recycling rates and restrictions on microplastic use increase the adoption of molded fiber protective packaging for electronics. The expansion of online electronics shopping and the consumer preference for packaging that eliminates unboxing waste increase the use of molded fiber protective packaging for electronics. The high investment in manufacturing machinery and the miniaturization of medical devices increase the use of molded fiber protective packaging for electronics, supporting the overall market growth.

Germany

United Kingdom

Latin America held the 6% share in 2025. The growing online shopping of sensitive electronics products and the focus on electronics supply chain optimization increase the adoption of molded fiber protective packaging for electronics. The strong electronics assembly hubs and the waste-management reforms increase the use of molded fiber protective packaging for electronics. The electronics brand's strong focus on a green image boosts the overall market growth.

Brazil

Argentina

The Middle East & Africa held the 5% market share in 2025. The region focuses on meeting global sustainability standards, and the presence of leading electronics retailers increases the use of molded fiber protective packaging for electronics. The focus on protecting fragile electronic items and manufacturing advancements increases the adoption of molded fiber protective packaging for electronics. The rising manufacturing of component-dense consumer electronics fuels the overall market growth.

United Arab Emirates

South Africa

In February 2026, AGY collaborated with JPS Composite Materials to launch domestic production of low-CTE glass fiber fabrics. The new fiber fabrics are ideal for next-gen semiconductor packaging and advanced IC substrates. The manufacturing facility of new fiber fabrics is present in Aiken, South Carolina.

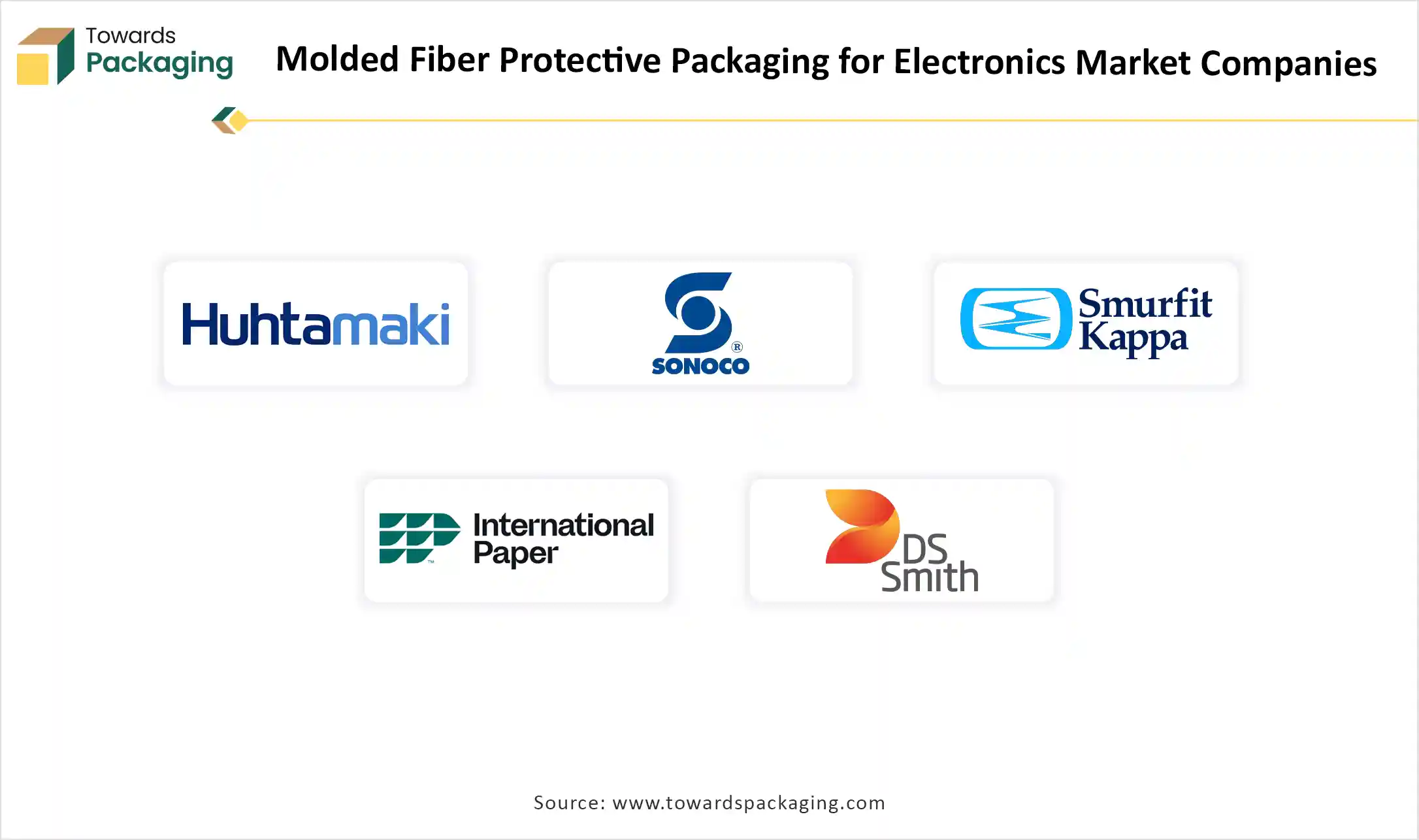

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products and Services |

| 1. | Huhtamaki Oyj | Espoo, Finland | Finland | Focuses on high-precision manufacturing, and the company invested $100 million to expand production of advanced fiber solutions in Hammond, Indiana. | Electronic Trays, End Caps, and Corners |

| 2. | Sonoco Products Company | Hartsville, South Carolina, United States | United States | The company focuses on developing sustainable foam alternatives and using circular-ready materials. | Paper Honeycomb, SonoPost Structural Posts & Corners, Edge Boards, and Custom Molded Cushions |

| 3. | Smurfit Kappa Group | Dublin, Ireland | Ireland | The company develops form-fitting packaging and performs rigorous transit validation. | Clamshells, Custom Inserts, Cushioning, Trays, and End Caps |

| 4. | International Paper Company | Memphis, Tennessee, United States | United States | The company is developing sustainable design and custom corrugated packaging solutions. | Molded Pulp Inserts, ESD Protection, Retail-Ready Packaging, Molded Pulp Nests, Custom Die-Cut Partitioning, and End Caps |

| 5. | DS Smith plc | London, England, UK | United Kingdom | The company develops specialized buffers and manufactures recyclable molded fiber packaging. | Buffers, ESD Packaging, Electronics Trays, Kit Packaging, Inserts, and Multi-Material Solutions |

By Product Type

By Molding Technology

By Raw Material

By Electronics Product Type

By Protection Function

By End User

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarMolded Fiber Protective Packaging for Electronics Market