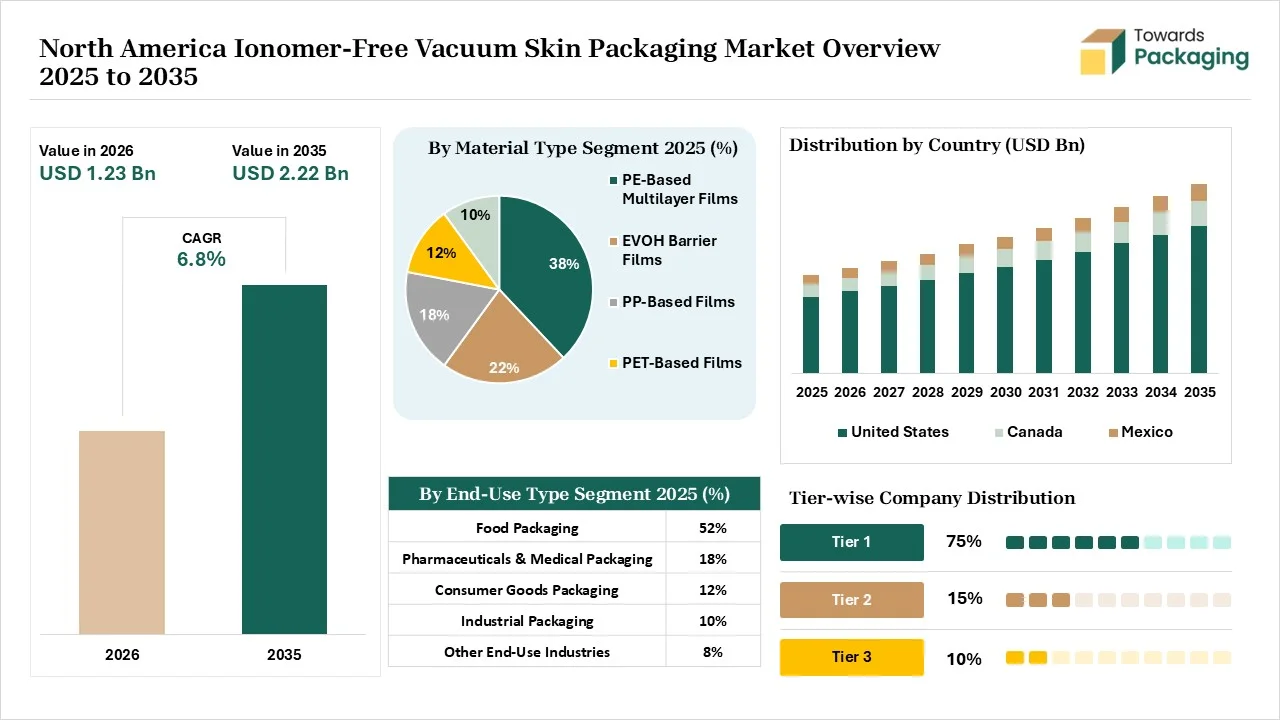

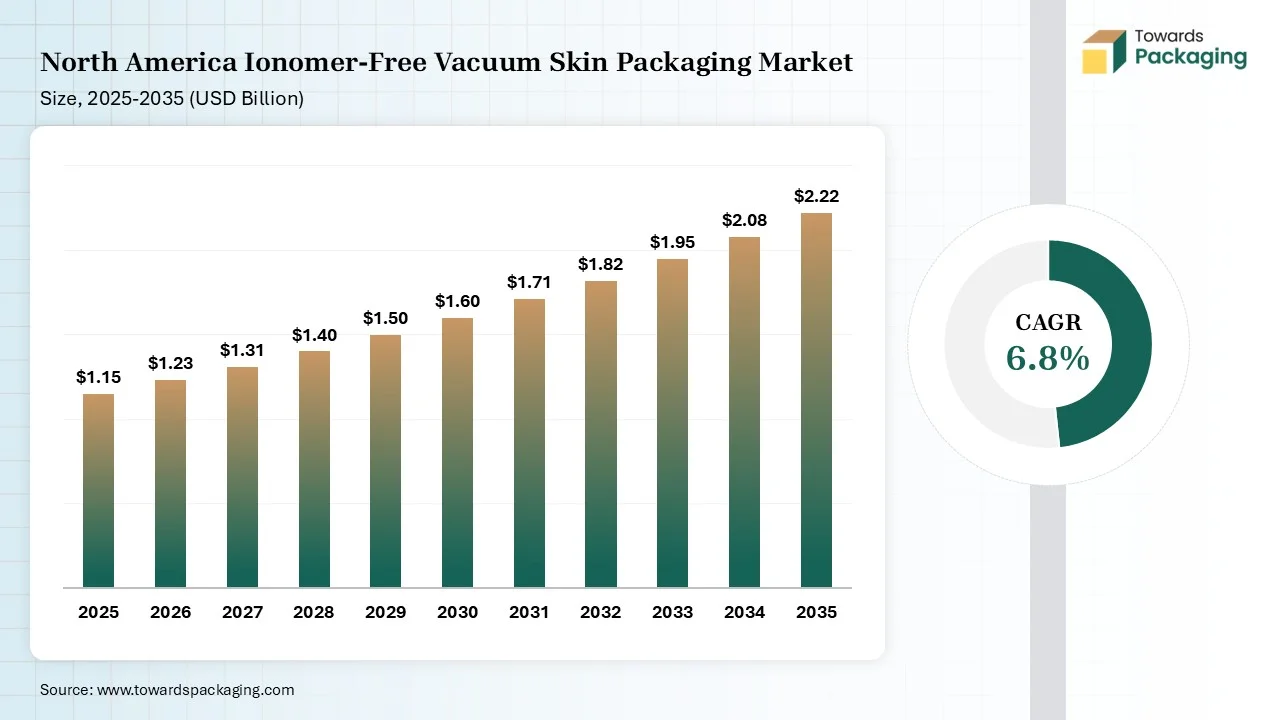

The North America ionomer-free vacuum skin packaging market is projected to grow from USD 1.23 billion in 2026 to USD 2.22 billion by 2035, registering a CAGR of 6.8% during the forecast period. The study provides detailed market size forecasts, segment-level revenue analysis by material type, application, end-use industry, and packaging format, along with regional demand assessments across North America. It further evaluates competitive positioning, company market shares, manufacturer and supplier landscapes, value chain dynamics, pricing trends, production capacity, trade statistics, import-export analysis, distribution networks, and strategic developments shaping the industry.

Ionomer-free vacuum skin packaging (VSP) is a cost-effective packaging that does not contain traditional ionomers. The packaging is a combination of barrier materials and polyolefin-based resins. The production process includes steps like film extrusion, product placement, heating, evacuation, and sealing. Its key features are exceptional optics, superior seal integrity, supply resilience, and mechanical durability. It offers benefits like excellent processing, enhanced display, cost-effectiveness, and extended shelf life. The applications of ionomer-free VSP are processed meat, cheeses, RTE meals, fish, dairy, and fresh meat.

The North America ionomer-free vacuum skin packaging market is growing due to the rise in material shortages, high consumption of fresh proteins, focus on regional sustainability goals, increased mono-material use, thriving seafood industry, focus on household food waste reduction, rise in DTE meal kits, and the development of high-value industrial components.

The North America ionomer-free vacuum skin packaging market is experiencing technological developments due to growing material costs and the rising supply chain issues. Developments like computational modeling, IoT integration, digital automation, and smart packaging integration are driven by demand for premium performance and improved scalability. AI is the major redefining shift in the market.

AI predicts the barrier efficacy of latest formulations & easily spots uneven film stretching. AI supports layout optimization and easily evaluates equipment performance. AI predicts the seal integrity of packaging and detects a weak seal. AI predicts temperature fluctuations and component failures. AI combats counterfeiting issues and reduces film consumption. Overall, AI helps in material optimization, defect detection, and intelligent tracking.

Raw materials like EVA polymers, MAH-grafted LLDPE, mLLDPE, EVOH, and metallocene polyethylene are required.

Material processing involves resin selection, cast film extrusion, and down-gauging. Conversion includes heating, evacuation, and sealing.

Package design focuses on preparation, film selection, evacuation, hermetic sealing, and aeration. Prototyping focuses on blow film extrusion, machine trials, and shelf-life testing.

The PE-based multilayer films segment dominated the market with 38% share in 2025 due to its excellent cost-to-performance ratio. The focus on lowering product loss and the need for faster sealing cycles increases the adoption of PE-based multilayer films. The growing meat packaging and the expansion of mass-scale packaging increase the adoption of PE-based multilayer films. The high optical clarity, excellent heat-sealing, and superior product visibility in PE-based multilayer films drive the segment growth.

The EVOH barrier films segment held the 22% market share in 2025 due to its superior visual appeal. The curbside recycling guidelines and the North American pharmaceutical expansion increase demand for EVOH barrier films. The strong focus on maintaining packaging performance and spoilage prevention of ready meals increases the use of EVOH barrier films. The flexibility, easier recyclability, and excellent formability of EVOH barrier films support the segment growth.

The PET-based films segment held the 18% market share in 2025 due to the high utilization in retail-ready packaging. The focus on preventing freezer burn and the need for vertical retail display increase the adoption of PET-based films. The rise of premiumization of food items and the need to slow oxidation increase the use of PET-based films. The high puncture resistance, exceptional product aesthetics, and operational adaptability of PET-based films boost the segment growth.

The food packaging segment dominated the market with 52% share in 2025 due to the flavor preservation of seafood. The strong poultry industry and the rise in self-service retail increase the adoption of ionomer-free VSP. The rise in food transport and food waste reduction in the home environment increases the use of ionomer-free VSP. The focus on replacing chemical preservation in the food sector and the increasing food retail presentation accelerates the segment growth.

The pharmaceuticals & medical packaging segment held the 18% market share in 2025 due to the rise of minimally invasive procedures. The increased use of disposable surgical instruments and the focus on zero product contamination increase the use of ionomer-free VSP. The growth of sensitive medical instruments and the medical company's focus on meeting sustainability targets enhance the use of ionomer-free VSP, drives the overall segment growth.

The e-commerce & retail packaging segment held the 13% market share in 2025 due to the growing long-distance e-commerce shipping. The increased distribution of meal kits and the focus on preventing transit delays increase the adoption of ionomer-free VSP. The rise in home-delivered goods and the retail grocery expansion increases the use of ionomer-free VSP. The focus on improving customer experience boosts the segment growth.

The tray-based vacuum skin packaging segment dominated the market with 41% share in 2025 due to the growing use in modern supermarkets. The brand visibility enhancement and the focus on maintaining food hygiene increase the adoption of tray-based VSP. The focus on preserving seafood's natural color and growing vertical merchandising in the retail sector increases the adoption of tray-based VSP. The leak prevention and automated manufacturing compatibility of tray-based VSP drives the segment growth.

The preformed rigid tray systems segment held the 25% market share in 2025 due to the growing use in the poultry industry. The focus on eliminating drip loss and the expansion of deli segments increases the use of preformed rigid tray systems. The protection of awkwardly shaped items and the need to minimize retail food waste increase the use of preformed rigid tray systems. The structural integrity and operational efficiency of preformed rigid tray systems support the segment growth.

The film-only vacuum skin packs segment held the 24% market share in 2025 due to the supply chain stability. The increased purchasing of perishable items and the focus on package weight reduction increase the use of film-only vacuum skin packs. The growing mid-scale processors and the need to enhance sustainability increase the use of film-only vacuum skin packs. The premium presentation and high transparency of film-only vacuum skin packs support the segment growth.

The direct OEM sales segment dominated the market with 46% share in 2025 due to the availability of machinery-to-film integration. The customized automation demand and the need for prototype testing increase the adoption of direct OEM sales. The reduction of film waste and the focus on providing uninterrupted access increase the use of direct OEM sales. The growing direct purchasing drives the segment growth.

The packaging converters segment held the 28% market share in 2025 due to the cost-saving benefits. The demand for consistent supply and the interest in advanced flexible films increase the adoption of packaging converters. The focus on increasing businesses' profit margins and burgeoning material conversion flexibility increases the adoption of packaging converters.

The distributors & wholesalers segment held the 20% market share in 2025 due to the availability of diverse materials. The high-volume demand in the medical industry and the presence of small enterprises increase the adoption of distributors & wholesalers. The demand for specialty films in local retailers and the minimum order quantities increase the need to buy from distributors & wholesalers. The growing centralized sourcing boosts the segment growth.

The United States is the leading contributor to the market. The strong focus on preventing microbial growth on food and the rise in recyclable packaging initiatives increase demand for ionomer-free VSP. The higher demand for high-quality seafood and the development of high-performance resins increase the adoption of ionomer-free VSP. The organized retail chains and the advanced packaging capabilities drive the market growth.

Canada is rapidly growing in the market. The preference for mono-material structures and the rise in green initiatives increase demand for ionomer-free VSP. The robust protein industry and the tamper-evident standards increase the use of ionomer-free VSP. The surge in subscription meal kits and the growing demand for high-end cheeses increase the use of ionomer-free VSP. The food waste minimization supports the market growth.

Mexico is substantially growing in the market. The availability of metallocene polyethylene resins and the burgeoning food processing operations increase the adoption of ionomer-free VSP. The rising production of case-ready proteins and the flourishing export industry increase demand for ionomer-free VSP. The focus on vertical retail displays supports the overall market growth.

In May 2026, ExxonMobil partnered with G.Mondini, Kuraray, and GAP to launch an ionomer-free vacuum skin packaging solution for the food industry. The new packaging solution is made using EVAL EVOH barrier material, polyethylene resins, and EVA. The packaging includes three resins like ExxonMobil EVA 06519FL polymer, Exceed Flow+ m 0516 metallocene polyethylene, and Exceed Tough+ m 0512 metallocene polyethylene. The gloss level of ionomer-free VPA is 81, and packaging offers premium visual quality.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products and Services |

| 1. | Sealed Air Corporation | Charlotte, North Carolina, United States | United States | The company focuses on the development of sustainable VSP solutions and offers microwavable VSP options. | VSP Bottom Carriers & Trays, CRYOVAC Simple Steps VSP, and CRYOVAC Darfresh Top Web Films |

| 2. | Amcor | Zurich, Switzerland | Switzerland | The company focuses on minimizing plastic usage and extending fresh proteins' retail shelf life. | SkinTite Films, VSP Trays and Rollstock, 10K OTR Films |

| 3. | Winpak | Winnipeg, Manitoba, Canada | Canada | The company focuses on the development of high-barrier films and offers custom packaging consulting. | WINfresh VSP Films, MAPfresh Trays & Bags, and ReForm & ReLam Thermoforming Films |

| 4. | ProAmpac | Cincinnati, Ohio, United States | United States | The company uses mono-material films and supports sustainable fiber innovation. | ProActive Recyclable R-2200D Easy-Peel Open film |

| 5. | ExxonMobil | Spring, Texas | United States | The company offers advanced polyethylene resins for the development of ionomer-free VSP. The company collaborated with Videplast to manufacture ionomer-free VSP film. | Exceed Flow+ (m 0516), Exceed XP 7052ML, Exceed Tough+ (m 0512), and ExxonMobil EVA 06519FL |

By Material Type

By End-Use Industry

By Packaging Format

By Distribution Channel

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarNorth America Ionomer-Free Vacuum Skin Packaging Market