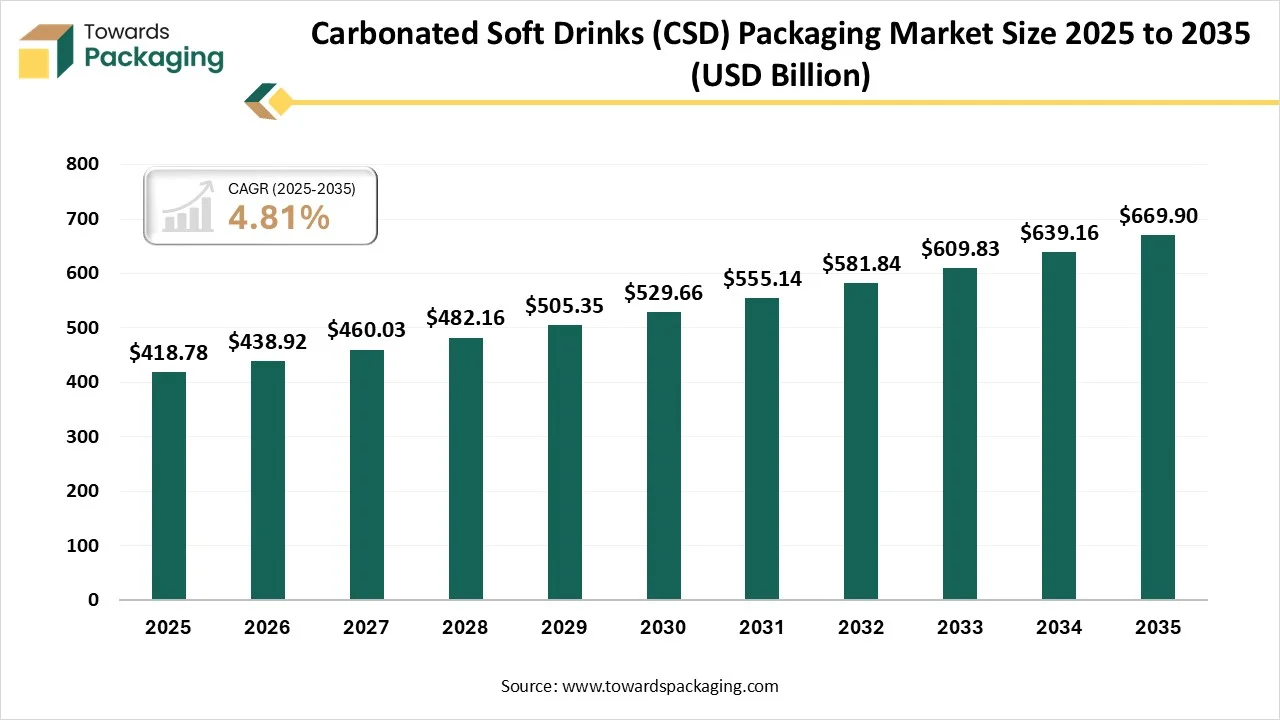

The Carbonated Soft Drinks (CSD) Packaging market is projected to grow from USD 438.92 billion in 2026 to USD 669.90 billion by 2035, registering a CAGR of 4.81% during the forecast period. The report provides complete market coverage including detailed segmentation by materials (metal, plastic, glass, carton) and packaging types (cans, bottles, cartons). It also includes in-depth regional analysis across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, along with company profiles, competitive landscape, value chain analysis, trade data, and comprehensive insights on manufacturers and suppliers.

Packaging market Size 2025 - 2035")

The carbonated soft drinks (CSD) packaging market encompasses all packaging formats such as PET bottles, aluminum cans, glass bottles, cartons, and paper-based packages used specifically to contain, preserve, and deliver carbonated soft drinks. It includes packaging materials, formats, and technologies designed for shelf appeal, product integrity (e.g., carbonation retention), convenience (resealability, portability), and sustainability.

Carbonated soft drinks are non-alcoholic beverages created from carbonated water and flavoring and sweetening with sugar or a non-nutritive sweetener. CSD is a kind of beverage that adds carbon dioxide to give it an effective taste. It is further classified as non-colas, colas, and diet soft drinks, and regular swift drinks too. It also utilises cola nuts from the African trees, cola acuminata and cola nitida, as flavouring agents. Due to phosphoric acid, which can expand the acidity, it is prevalently used as an acidulant in the cola-flavoured carbonated beverages. Phosphoric acid has the same element as cola flavours, which is dry and sometimes balsamic. They account for a sizeable space of the worldwide soft drink sector.

Artificial Intelligence can assist drink brands in forecasting and planning. AI’s potential to process huge amounts of data and check patterns and exceptions is being used to determine market trends for the most searched product series and range, to the most regular locations, along with competitor activity. It can also track data to analyse and forecast user trends, utilising this to identify or even suggest new formulations and ingredient combinations. Data sets could also count consumer choice, nutritional profiles, and flavourful combinations.

Furthermore, AI can also deliver personalised product recommendations to drinkers, both in-person and online. Online, AI can personalize product suggestions depending on the browser's buying habits and purchases created by others like them. This counts as suggesting drinks to pair with specific dishes or cuisine, for instance. This can be personalised by the user themselves too, to include favourite flavour zones, allergy information, and nutritional demands. AI can also be utilised during production. Functions of artificial intelligence like robotics, automation, and machine learning can all be allied by the producer of drinks, performing repetitive tasks accurately and speedily, such as classifying produce or packaging, to lower labour costs and develop efficiencies.

Health-Focused Drinks Are The Preferred Choice

Consumers are urging for more for their daily drinkables, seeking ingredients that develop their mood, hydration, gut health, and more. At the same time, wellness mixers and beverages frequently cost more than famous sugary soda brands, but users find an eagerness to pay for them. For them, hydration is the main goal, but wellness mixtures like protein powders and prebiotics are developing. Despite having economic issues, retail sales data display constant development in the beverage industry, which highlights important user spending. Apart from these, Gen Z is driving the urge for easy, flavourful, and non-alcoholic drinks that can be consumed socially or on the go, so no mix-ins are demanded.

The quickest developing category features a huge flavour range from sweet to savoury -that includes the energy drinks, bottled water, soft drinks, sports drinks, CBD-infused options, and kombucha too.

Carbonated soft drinks have many limitations, like a heavy risk of chronic diseases such as type 2 diabetes, obesity, and heart disease due to their high sugar and calorie content. They are also responsible for dental issues, like enamel erosion and excessive sugar, which can lead to weakened bones by interfering with calcium absorption, and their caffeine content, too, which can cause sleep problems and addiction. Additionally, they contribute to dehydration and can negatively affect behaviour and brain function, especially in children.

The future possibilities in the carbonated soft drink industry are being shaped by growing consumer preferences, health trends, and sustainability goals. With rising health consciousness, companies are concentrating on low-sugar, sugar-free, and functional CSDs that count added vitamins, probiotics, or natural ingredients to attract health-oriented consumers. Flavoured sparkling water and premium craft sodas are gaining popularity as alternatives to traditional colas. Sustainability is another strong driver, with brands increasingly investing in eco-friendly packaging such as recycled PET. Aluminum cans and biodegradable materials.

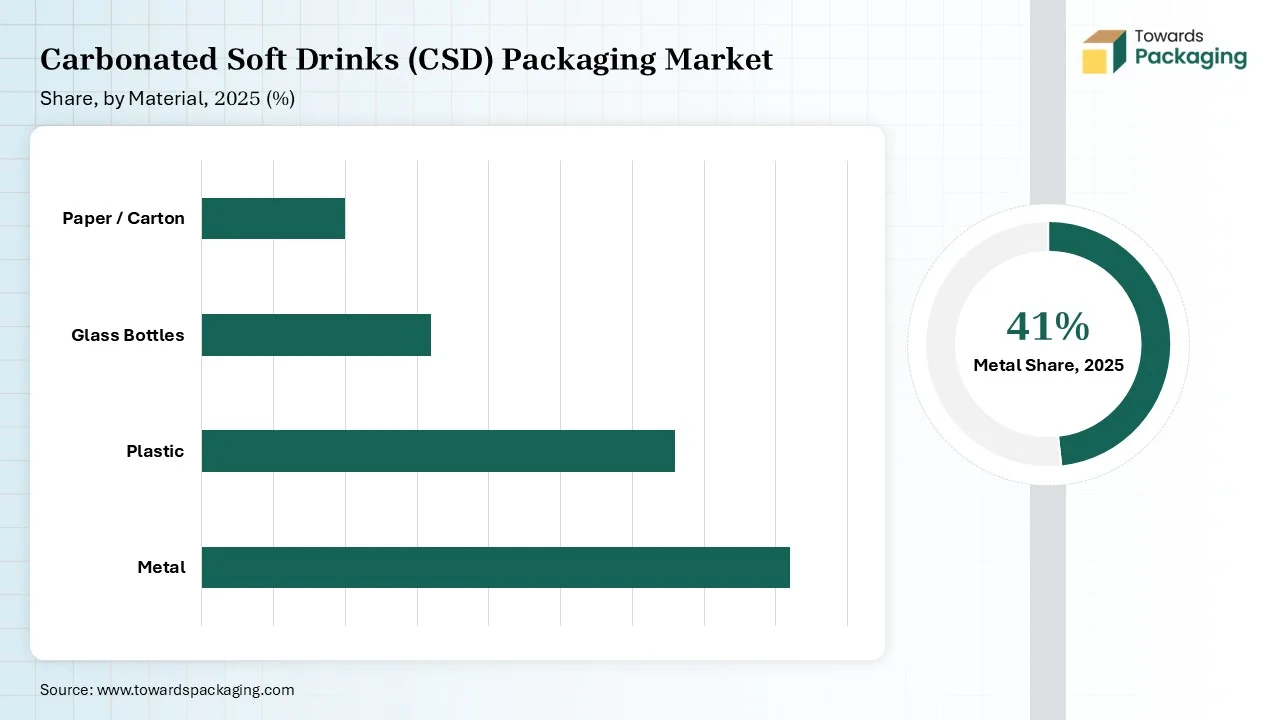

Packaging Market Share, by Material Type 2025 (%)")

How Did The Metal Segment Dominate The Carbonated Soft Drinks (CSD) Packaging Market?

The metal segment dominated the market in 2025 as it is the most widely used packaging solution in the carbonated soft drinks industry due to its lightweight, strong nature, and excellent barrier properties that preserve carbonation and flavour. They are highly preferred for their portability, convenience, and recyclability, making them a sustainable choice in the current eco-conscious market. With increasing focus on the circular economy, the demand for aluminum cans in CSD packaging is rising. They can be recycled infinitely without losing quality. This makes them ideal for convenience, product safety, and sustainability, too, which is very crucial for everything.

Plastic segments are predicted to be the fastest in the market during the forecast period. Plastic bottles like PET (Polyethylene Terephthalate) and recycled PET are extensively used due to their lightweight, shatter-resistant, and cost-effective nature. PET bottles offer excellent clarity and the power to carry carbonation, while rPET is gaining momentum as brands shift toward sustainability and reducing plastic waste. Increasing recycling technologies and regulatory support are driving the use of rPET, helping companies lower their carbon footprint while maintaining product quality and safety.

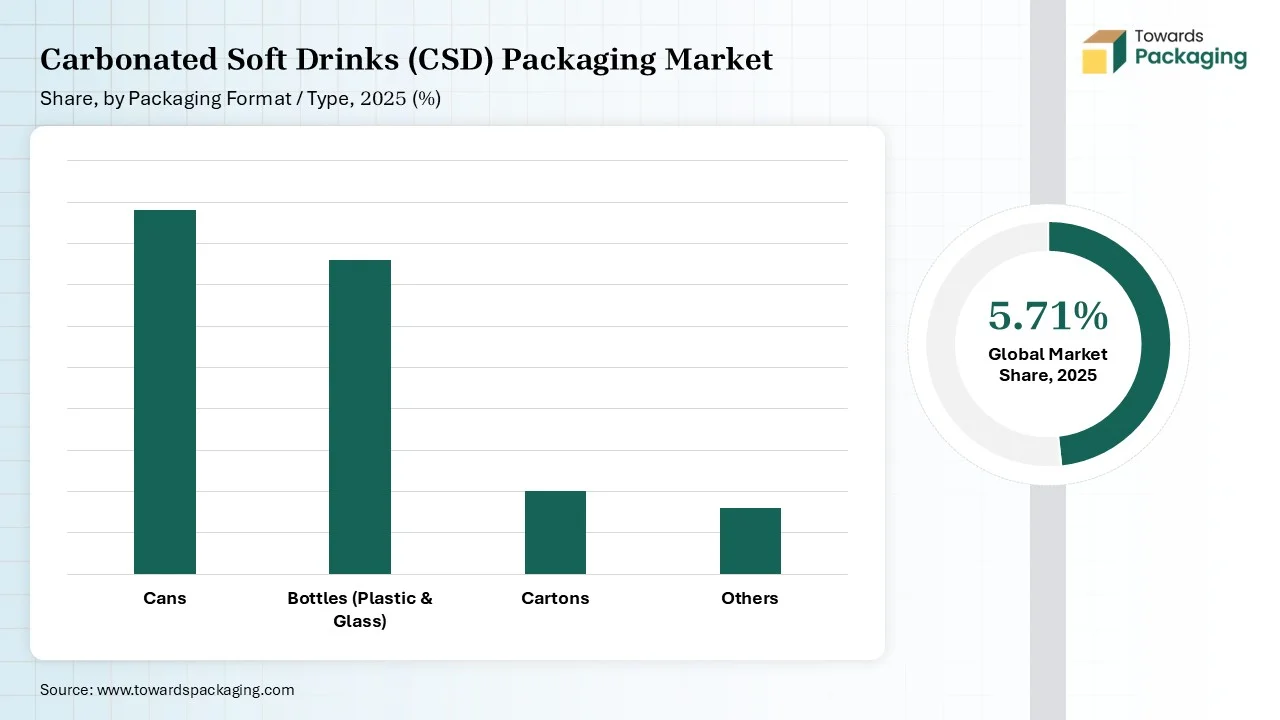

Packaging Market Share, by Packaging Format / Type 2025 (%)")

How Can Segment Dominate The Carbonated Soft Drinks (CSD) Packaging Market?

The can segment dominated the carbonated soft drinks (CSD) packaging market in 2025 due to its ideal ability to preserve carbonation, freshness, and shelf life of the product. They are lightweight in nature, stackable, and highly portable, making them convenient for both consumers and retailers. Cans, in particular, are widely used because they are 100% recyclable, without having a loss of global encouragement toward sustainability. Additionally, cans serve strong barrier properties against light and oxygen, ensuring taste consistency . With increasing consumer selection for eco-friendly packaging, and on-the-consumption, cans remain a main and growing segment in CSD packaging.

Bottles segment are expected to be the fastest in the market during the forecast period. They play a major role in the carbonated soft drinks sector, being the most common due to their cost-effectiveness and lightweight nature. They are easy to transport, resealable, and available in multiple sizes. Catering to both individual and family consumption. Glass bottles. Though less dominant currently, they are still valued for their luxury feel, strong carbonation and retention, and recyclability, often used by niche heritage brands. With growing demand for sustainability, the industry is increasingly accepting rPET bottles to reduce plastic waste and meet environmental goals, making bottles a versatile yet evolving solution in CSD packaging.

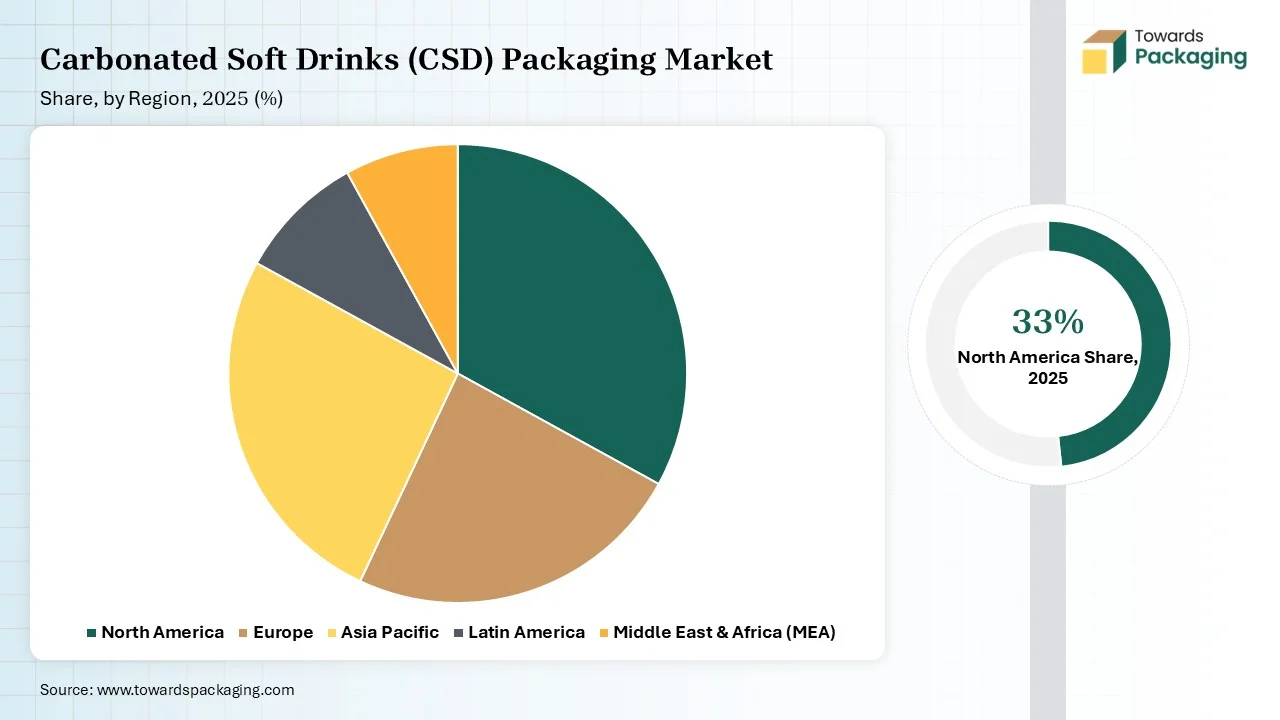

Packaging Market Share, by Region Type 2025 (%)")

North America dominated the carbonated soft drinks (CSD) packaging market in 2025, industry because it is growing steadily, driven by consumer choices, sustainability initiatives, and growth in packaging technologies. PET bottles, aluminium cans and glass bottles remain the primary formats, with PET bottles leading due to their durability, lightweight and convenience properties. However, rising environmental concerns are boosting the acceptance of recycled PET bottles and cans as both meet the circular economy rules and regulations. Additionally, growth in the ready-to-drink market, e-commerce, and on-the-go consumption has further accelerated the need for innovative packaging formats that balance sustainability, ease, and comfort, too, with carbonated soft drink packaging demands.

Asia Pacific is expected to grow in the market during the forecast period. The demand and production of carbonated soft drinks in the Pacific region are witnessing a dynamic shift fueled by innovation, sustainability, and evolving consumer behavior. It has come up as the fastest-growing region globally for CSD packaging, spurred by rapid urbanization, expanding middle-class populations, and shifting taste choices-particularly toward low-sugar, health-oriented, and on-the-go choices. Brands are feeding back by rolling out intelligent and portable designs, with PET bottles that track cost-efficiency and ease.

Material Processing and Conversion: The material processing and conversion of CSD packaging count on transforming raw materials like PET, rPET, and aluminium cans and paperboard into functional beverage containers. PET and rPET experience polymerization, extrusion, and blow molding to generate shatter-resistant bottles. Aluminum is rolled into sheets, printed, and deep-drawn into smooth cans, valued for their recyclability and product protection.

Package Design and Prototyping: Package design and prototyping in this kind of CSD packaging concentrate on creating a functional. Sustainable and visually appealing solutions that balance consumer convenience with brand identity. The design stage counts conceptualising shapes, sizes, and materials that develop shelf presence while maintaining durability and carbonation retention.

Logistics and Distribution: This space plays a crucial role in making sure beverages reach retailers and consumers efficiently while tracking product quality. The procedure counts on optimised warehousing, palletization, and transportation strategies to handle high volumes of bottles, cans, or glass containers. Packaging is crafted for durability, stackability, and space efficiency, reducing the risk of leakage, breakage, or loss of carbonation during transit.

Packaging Market Companies")

By Material

By Packaging Format / Type

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarCarbonated Soft Drinks (CSD) Packaging Market