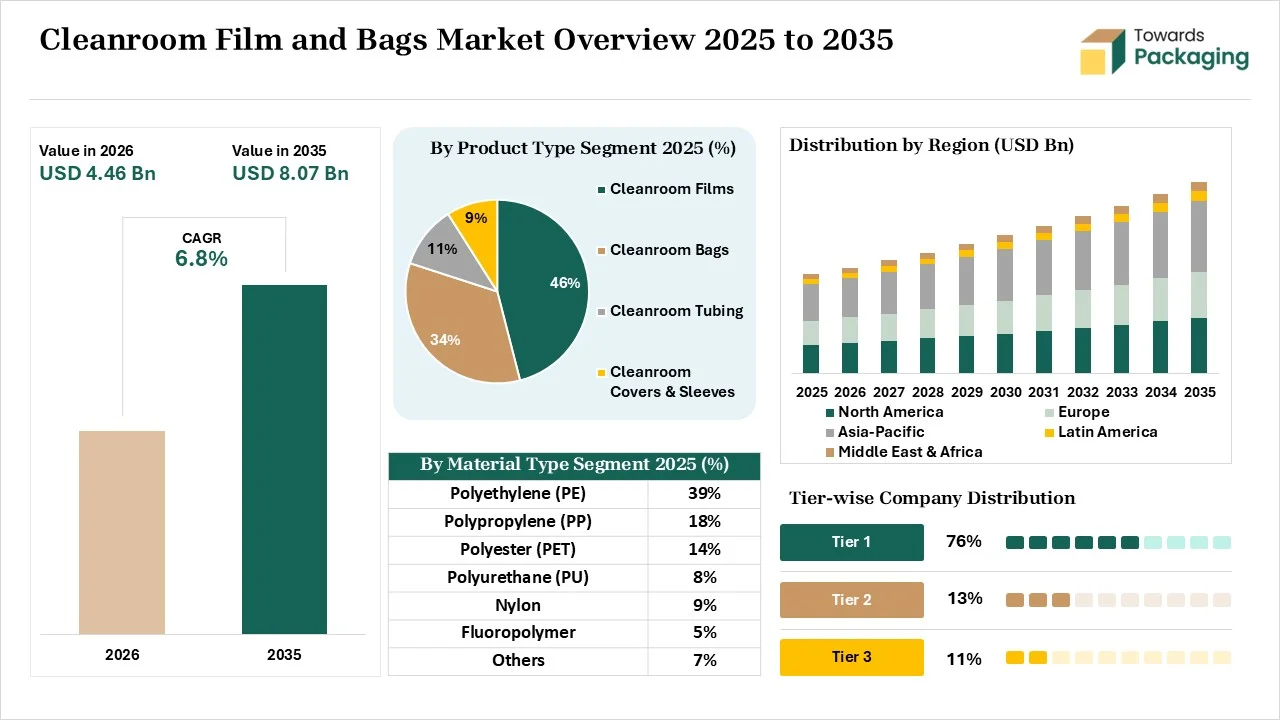

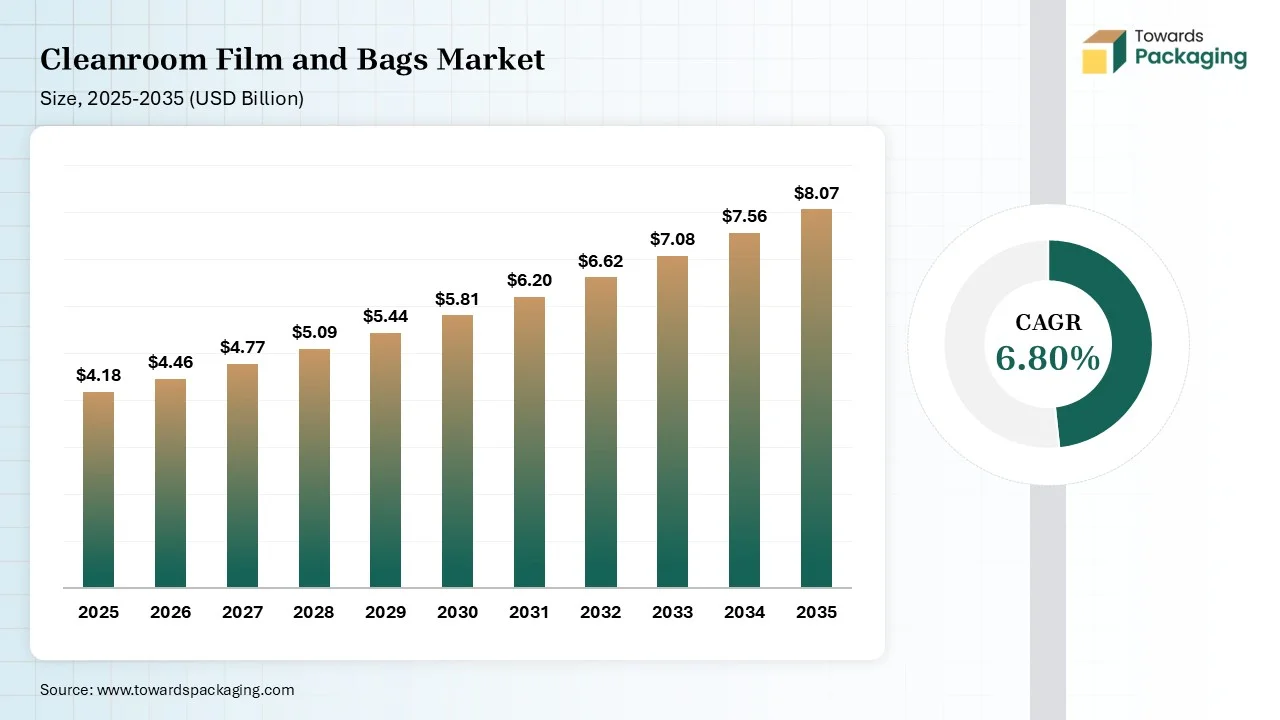

The cleanroom film and bags market is projected to grow from USD 4.46 billion in 2026 to USD 8.07 billion by 2035, registering a CAGR of 6.80% during the forecast period. The study provides comprehensive coverage of market size, share, growth trends, segment-level performance, regional analysis, competitive benchmarking, company profiles, value chain assessment, trade flow analysis, manufacturing trends, supplier landscape, pricing evaluation, and strategic developments. The report also examines the impact of increasing adoption of single-use technologies, stringent contamination-control requirements, and rising demand for particulate-free packaging across pharmaceutical, biotechnology, semiconductor, and advanced manufacturing industries.

Cleanroom film and bags are ISO-certified packaging materials produced in controlled environments that prevent contamination. They feature characteristics like low outgassing, superior barrier protection, excellent sterilization compatibility, ultra-low particulate generation, ESD protection, and high puncture resistance. They offer benefits like superior durability, contamination control, and sterility maintenance. They are used in applications like sterile surgical tools, housing sensitive chips, high-value spacecraft, shipping raw chemicals, clean food processing, and many more. The common examples include lay flat tubing, clean poly bags, header bags, shrink film, and anti-static bags.

The cleanroom film and bags market is growing due to the development of flexible cleanroom bags, enhancements in manufacturing base, burgeoning production of gene therapies, higher demand for gamma-compatible bags, stringent ISO regulations, thriving microchips manufacturing, expansion of ESD solutions, growing cryogenic storage, and the expansion of semiconductor fabrication plants.

The cleanroom film and bags market is going through several technological developments, like IoT, cleanroom computer integration, robotics manufacturing, digital twin technology, and blockchain. The technological developments fueled by customized solutions, contamination control, and sterilization standards. The major technological breakthrough is that artificial intelligence supports automating quality inspection.

AI spots pinholes in the cleanroom film & bags and predicts failures of the sealing machine. AI develops consistent polymer blends and accelerates the manufacturing of specialized films. AI helps in energy management in the cleanrooms and performs tamper-proof audit trails. AI reduces the need for human presence and easily tests various barrier combinations. Overall, AI helps in material research, contamination minimization, and equipment maintenance.

The stage acquires raw materials like polypropylene, Tyvek, polyethylene, anti-slip agents, aluminum foil, nylon, and anti-static agents.

Material Processing involves cast extrusion, blending, and cleanroom execution. Material conversion involves slitting, cutting, biaxial orientation, winding, and sealing.

Package design focuses on material selection, sealing capability, custom configurations, and printability. Prototyping focuses on material testing, leak testing, usability evaluation, and sterilization compatibility.

The cleanroom films segment dominated the market with 46% share in 2025 due to the increasing use in cleanroom pouches. The varying sterilization requirements and the focus on virtually eliminating outgassing increase the adoption of cleanroom films. The expansion of highly regulated industries and the development of critical electronics increase the adoption of cleanroom films. The focus on safeguarding biological materials drives the segment growth.

The cleanroom bags segment held the 34% market share in 2025 due to the stricter regulations in biotech supply chains. The growth in single-use bioprocessing and the focus on protecting aerospace components increase the use of cleanroom bags. The biopharmaceutical production and the circuit board protection increase the use of cleanroom bags. The burgeoning sterile transport requirements support the overall segment growth.

The polyethylene (PE) segment dominated the market with 39% share in 2025 due to its ability to prevent airborne contamination. The growth in delicate electronic components and the development of tamper-evident encapsulation increase the adoption of polyethylene. The medical component transportation and the stricter FDA rules for pharmaceutical packaging increase the use of polyethylene. The sterilization compatibility, excellent sealability, flexibility, and zero outgassing of polyethylene drive segment growth.

The polypropylene (PP) segment held the 18% market share in 2025 due to its ability to resist static buildup. The growing medical-device storage and increasing use of anti-static formulations increase the adoption of polypropylene. The focus on eliminating contamination in unclosed products and the interest in affordable polymers increase the use of polypropylene. The low particle shredding and excellent chemical resistance of polypropylene support segment growth.

The ISO class 4-5 segment dominated the market with 34% share in 2025 due to the growing aseptic pharmaceutical processing. The manufacturing of thin-film displays and patient safety focus increases the use of ISO class 4-5. The preparation of cell therapy and the protection of printed circuit boards increase the use of ISO class 4-5. The high batch integrity in ISO class 4-5 drives the segment growth.

The ISO class 6-7 segment held the 31% market share in 2025 due to the rising production of high-resolution displays. The assembly of medical devices and the creation of general pharmaceuticals increase the use of ISO class 6-7. The surging injectables and focus on ensuring lot traceability increase the use of ISO class 6-7. The prevention of color inconsistency in LED uses ISO class 6-7, supporting the overall segment growth.

The sterile segment dominated the market with 61% share in 2025 due to microbial contamination in the medical industry. The transportation of store buffers and the prevention of adverse effects in patients increase the use of cleanroom film and bags. The transition to disposables in the biotech industry and the interest in gamma irradiation treatments increase the use of cleanroom film and bags, driving the segment growth.

The non-sterile segment held the 39% market share in 2025 due to the demand for particle-free protection in electronic industry. The internal transport of microchips and the shielding of circuitry increase the use of cleanroom film and bags. The burgeoning chip fabrication and the contamination prevention in feedstocks of electronics increase the use of cleanroom films and bags, supporting the segment growth.

The 2-4 mil segment dominated the market with 42% share in 2025 due to the growing use in sterile packages. The semiconductor parts manufacturing and the focus on maintaining integrity in the healthcare industry increase the use of 2-4 mil. The international packaging regulations increase the use of 2-4 mil. The optimal balance, excellent tear resistance, manufacturing resilience, and cost efficiency of 2-4 mil drives the segment growth.

The 4-6 mil segment held the 28% market share in 2025 due to the increasing use in aseptic processing. The focus on preventing puncturing in medical tools and the development of ultra-clean aerospace parts increases the use of 4-6 mil. The interest in high-integrity disposables and the transportation of pre-filled syringes increases the use of 4-6 mil. The lower batch failures in 4-6 mil supports the segment growth.

The cast film extrusion segment dominated the market with 36% share in 2025 due to its clean manufacturing. The huge industrial demands and the focus on zero pinholes increase the adoption of cast film extrusion. The inspection of packaged electronics and the mass production of cleanroom film & bags increases the use of cast film extrusion. The precise gauge control, strict thickness tolerance, superior optics, and high contamination visibility in cast film extrusion drive the segment growth.

The blown film extrusion segment held the 28% market share in 2025 due to increased use in the packaging of sensitive semiconductor components. The production of multi-layer films and customizable barrier films increases the use of blown film extrusion. The flexible manufacturing capabilities increase the use of blown film extrusion. The high mechanical integrity, multi-layer barrier protection, and excellent material purity of blown film extrusion support the segment growth.

The pharmaceuticals segment dominated the market with 31% share in 2025 due to the growing biologicals packaging. The interest in disposable bioprocessing bags and the focus on protecting medication integrity increase the use of cleanroom film and bags. The focus on sterile transport of tissue cultures and the expanding sensitive injectables increases the adoption of cleanroom film and bags. The higher utilization of bioprocess containers drives the segment growth.

The semiconductor & electronics segment held the 20% market share in 2025 due to the thriving microelectronics manufacturing. The safe transportation of chips and the miniaturization of internal components of electronic devices increase the use of cleanroom film and bags. The focus on shielding electronic sensors and the expansion of OSAT facilities increase the use of cleanroom film and bags. The worldwide fabrication expansion supports the segment growth.

The direct sales segment dominated the market with 45% share in 2025 due to increased purchasing in the medical device industry. The product design collaboration and long-term partnerships of B2B increase the adoption of direct sales. The focus on end-to-end traceability and proper documented certifications increases the use of direct sales. The seamless technical communication and the high-volume contracts increase the use of direct sales, driving the overall segment growth.

The distributors & wholesalers segment held the 31% market share in 2025 due to the rising demand across regulated industries. The local inventory management and the simplification of full documentation increase the adoption of distributors & wholesalers. The increased purchasing of diverse clean bags & film formats and demand for application-specific products increases the adoption of distributors & wholesalers.

Asia Pacific dominated the market with a 37% share in 2025 and is expected to grow at the fastest CAGR of 8.10% during the forecast period due to the massive hub for electronics development. The increased production of sensitive electronic components and the rising generic drug production increase the adoption of cleanroom film & bags. The need for sterilized packaging for cleanroom consumables and the demand for highly standardized packaging increase the use of cleanroom film & bags. The increasing investment in the installation of cleanroom technology drives the market growth.

North America held the 29% market share in 2025 due to the burgeoning medical device manufacturing. The thriving microelectronics industry and the surging branded drugs increase the use of cleanroom film and bags. The stringent regulations on drug manufacturing and the focus on safeguarding sterile drugs increase the adoption of cleanroom film and bags. The rise in high-tech electronics fabrication and the focus on protecting wafers increases the adoption of cleanroom film and bags, supporting the market growth.

Europe held the 24% market share in 2025 due to the stricter standards in vaccine transportation. The growing production of advanced therapies and the expanding semiconductor sector increases the use of cleanroom film and bags. The need for contamination-free packaging in ATMPs and booming biotech manufacturing increases the adoption of cleanroom film & bags. The expansion of CDMO supports the market growth.

Latin America held the 5% market share in 2025 due to its strong pharmaceutical manufacturing hub. The advanced healthcare ecosystem and the strong semiconductor assembly sector increase the adoption of cleanroom film and bags. The increased use of ESD pouches and the stricter ISO standardization increases the development of cleanroom film and bags. The increased FDI investment in cleanroom film and bags boosts the market growth.

The Middle East and Africa held the 5% market share in 2025 due to the modernization of healthcare facilities. The production of sterile injectables and the prevention of static discharge in pharmaceutical products increase the adoption of cleanroom film and bags. The expansion of single-use systems and the increasing use of sensitive equipment in the medical industry increase the use of cleanroom film & bags. The interest in anti-static pouches supports the market growth.

| Rank | Company | Headquarters | Country | Major Contribution to Cleanroom Film and Bags Market | Key Packaging Products and Services |

| 1. | Amcor | Zurich, Switzerland | Switzerland | The company focuses on specialized cleanroom manufacturing and the development of sterile barrier pouches. | Optym Forming Films, Optym Pure Films, Optym Header Bag & Medical Bag Films |

| 2. | Sealed Air Corporation | Charlotte, North Carolina, United States | United States | The company focuses on certified cleanroom manufacturing and bioprocessing bag integration. | NEXCEL BIO 1250 |

| 3. | Mondi Group | Weybridge, England, United Kingdom | United Kingdom | The company manufactures specialized protective bags and develops sterile healthcare packaging. | Clean Cast Technology |

| 4. | Fruth Custom Packaging | Placentia, California, United States | United States | The company performs Level 100 cleanroom operations and focuses on leach prevention. | Standard & Class 100 Bags, Cleanroom Films & Rollstock, High-Heat Nylon Oven Bags, FOUP Bags |

| 5. | Pristine Clean Bags | 11511 Cronridge Drive, Owing Mills, Maryland 21117, United States | United States | The company focuses on high-purity manufacturing and the development of custom substrates. | Nylon Cleanroom Bags, Barrier Bags, Polyethylene Bags, ESD Bags |

By Product Type

By Material

By Cleanroom Class Compatibility

By Sterility

By Thickness

By Manufacturing Process

By End User

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarCleanroom Film and Bags Market