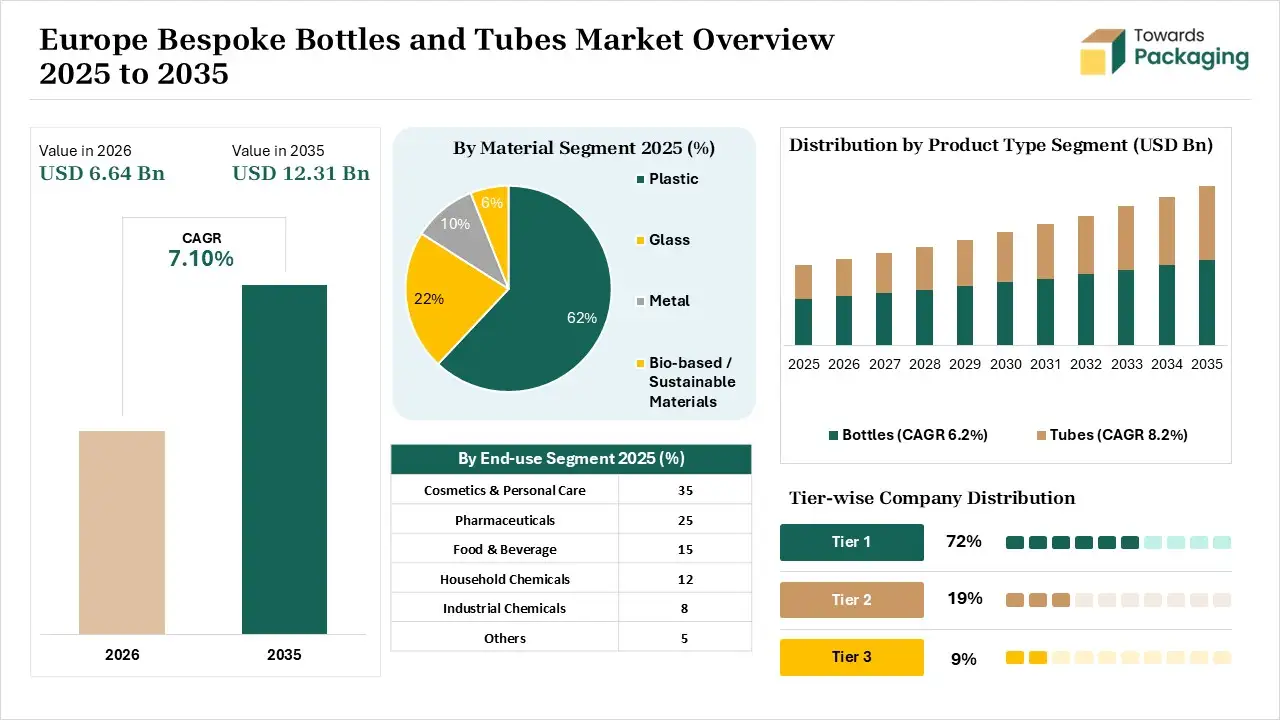

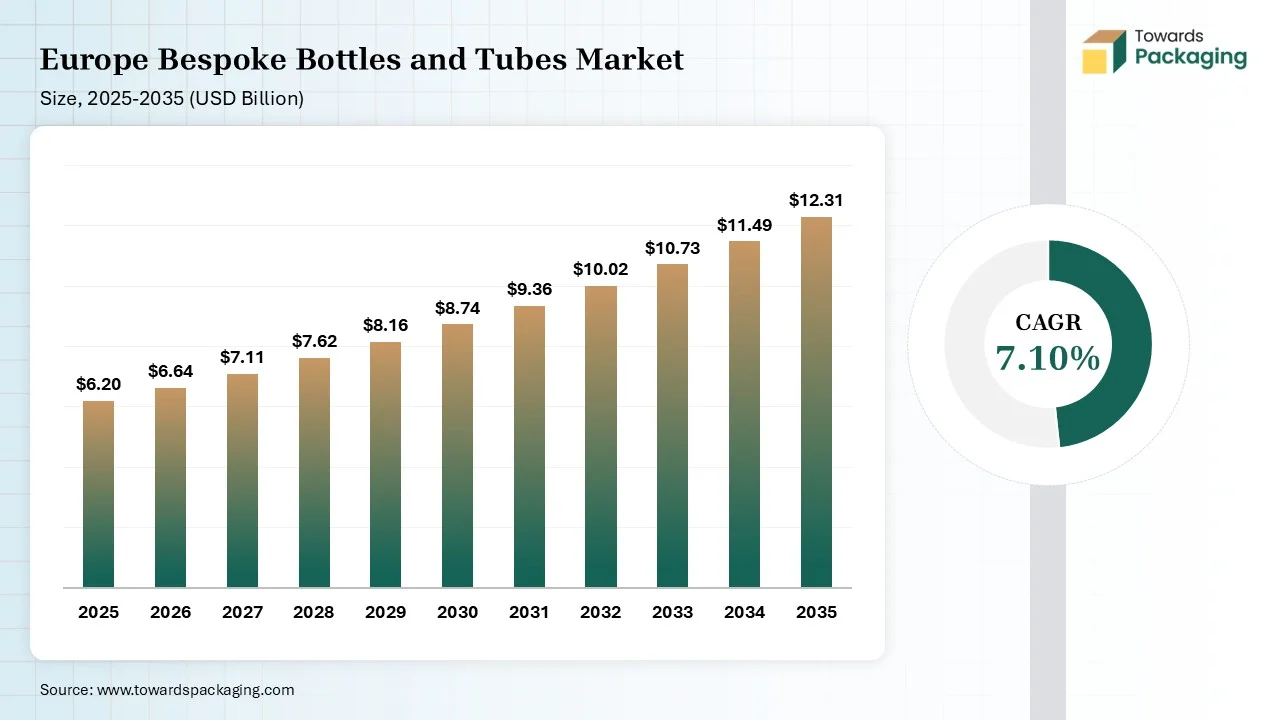

The Europe bespoke bottles and tubes market is projected to grow from USD 6.64 billion in 2026 to USD 12.31 billion by 2035, registering a CAGR of 7.10% during the forecast period. The report provides detailed market size analysis, growth forecasts, segment-level revenue data by material, product type, capacity, end-use industry, and closure type. It also covers regional performance across major European countries, competitive benchmarking of leading companies, manufacturer and supplier profiles, value chain assessment, production and consumption trends, import-export statistics, pricing analysis, and strategic developments shaping the industry.

Market Size (2025): USD 6.20 Billion

CAGR (2025–2035): 7.10%

Market Volume (2025): 35.0 Billion Units

Volume CAGR (2025–2035): 5.80%

Bespoke bottles and tubes are a tailored packaging option that elevates brand. Their characteristics are product protection, strong shelf presence, space optimization, chemical compatibility, viscosity handling, and high durability. They offer benefits like optimized product integrity, travel convenience, exclusivity, unique shelf presence, and lower shipping costs. Bespoke bottles and tubes are widely used in skincare products, medications, confectionery, corporate gifting, specialty labs, gourmet items, and makeup.

Europe bespoke bottles and tubes are undergoing technological developments like 3D printing, airless technology, digital printing, IoT integration, 3D visualization, nanotechnology, smart indicators, UV printing, and QR code integration. The technological developments help in rapid prototyping, functional product protection, and advanced preservation. AI is a key evolution that helps in optimizing complex production.

AI accelerates the creation speed of custom tubes and bottles. AI analyzes regional trends and develops premium textures of bottles and tubes. AI innovates new eco-friendly material for the production of bespoke bottles and tubes. AI supports intelligent production and accelerates the speed of detecting defects. AI monitors production schedules and performs automated copy checks. Overall, AI ensures smooth procurement and offers manufacturing feasibility.

The stage acquires raw materials like LDPE, PP, PET, PCR plastics, soda-lime glass, aluminum, HDPE, borosilicate glass, aluminum plastic laminates, and sustainable paperboard.

The material processing of bespoke glass bottles involves steps like batch preparation, melting, gob formation, molding, and annealing. Bespoke plastic bottles involve steps like polymer processing, preform injection, and stretch blow molding. The material conversion includes steps like blow molding, glass forming, and tube drawing.

Package design focuses on structural design, surface design, and graphics. Prototyping focuses on digital prototyping, machined models, and production-quality comps.

| Rank | Company Name | Headquarters | Country | Why Relevant | Key Products/Services | |

| 1 | Albéa Group | Gennevilliers | France | Global leader in cosmetic tubes and bespoke beauty packaging | Cosmetic tubes, airless systems, bottles | |

| 2 | AptarGroup | Crystal Lake, Illinois | USA | Premium dispensing and customized packaging solutions widely used in Europe | Closures, pumps, custom bottles | |

| 3 | Gerresheimer | Düsseldorf | Germany | Major supplier of custom pharmaceutical and cosmetic containers | Glass and plastic bottles, tubes | |

| 4 | Berlin Packaging | Chicago, Illinois | USA | Extensive bespoke packaging design and manufacturing network in Europe | Premium bottles, jars, packaging design | |

| 5 | Verescence | Puteaux | France | Leading luxury glass bottle producer for prestige brands | Custom glass bottles | |

| Rank | Company Name | Headquarters | Country | Why Relevant | Key Products/Services |

| 1 | Quadpack | Barcelona | Spain | Strong European presence in customized beauty packaging | Tubes, jars, bottles |

| 2 | Lumson | Capergnanica | Italy | Specialized luxury cosmetic packaging producer | Airless bottles, tubes |

| 3 | Eurovetrocap | Trezzano sul Naviglio | Italy | Strong customization capabilities for cosmetics | Glass bottles and accessories |

| 4 | Vidraria Anchieta | Maia | Portugal | Premium custom packaging for personal care products | Bottles and containers |

| 5 | Baralan | Milan | Italy | Customized primary packaging for cosmetics and beauty brands | Glass and plastic bottles |

| Rank | Company Name | Headquarters | Country | Why Relevant | Key Products/Services |

| 1 | HCP Packaging | London | United Kingdom | Growing premium cosmetics packaging supplier | Tubes, bottles, compacts |

| 2 | Premi Beauty Industries | Milan | Italy | Innovative luxury packaging solutions | Airless bottles, custom packaging |

| 3 | Aptar Beauty EMEA | Le Neubourg | France | Specialized regional innovation center for beauty packaging | Premium dispensing systems |

| 4 | Raepak | Norwich | United Kingdom | Bespoke packaging for personal care brands | Bottles, closures, tubes |

| 5 | Frapak Packaging | Zevenaar | Netherlands | Customized plastic packaging producer | PET and HDPE bottles |

The bottles segment dominated the market with 58% share in 2025 due to the growing use in the consumer goods industry. The growing consumer demand for multi-sensory unboxing and the strong presence of high-end brands increase the adoption of bottles. The explosion of beverage consumption and the preference for portable options increases demand for bottles. The powerful visual avatar, unique neck finishes, and tactile labels of bottles drive the segment growth.

The tubes segment held the 42% market share in 2025 due to user convenience and a strong focus on formulation protection. The expansion of the spread and the rise in travel-friendly cosmetics increases demand for tubes. The online retail growth and expansion of condiment products increases the use of tubes. The limitless brand differentiation, premium customization, hygiene, mess-free dispensing, and outstanding aesthetics of tubes support the segment growth.

The plastic segment dominated the market with 62% share in 2025 due to the competitive food industry. The surge in e-commerce shipping and the development of eye-catching aesthetics increase the use of plastic. The superior formability, controlled dispensing, advanced barrier protection, and lightweight logistics of plastic material help with expansion. The need for shape customizability in pharmaceuticals and the focus on limitless design flexibility increase the adoption of plastic, driving the segment growth.

The glass segment held the 22% market share in 2025 due to the circular economy goals in the European region. The rise in artisanal spirits and the focus on maintaining the purity of skincare increase demand for glass. The strong luxury cosmetics industry and the explosion of the premium skincare market increase the use of glass. The infinite recyclability and premium look of glass support the segment growth.

The metal segment held the 10% market share in 2025 due to the stricter eco-mandates. The growing high-end skincare industry and focus on protecting pharmaceutical-sensitive ingredients increase the adoption of metal. The sterile gel packaging and expansion of specialized canned craft beverages increase the adoption of metal. The exceptional recyclability, deposit-return systems, and airless dispensing of metal boost the segment growth.

The cosmetics & personal care segment dominated the market with 35% share in 2025 due to the well-established color cosmetics industry. The high consumer base for personal care and the preservation of sunscreens increases demand for bespoke bottles and tubes. The increased use of diverse skincare formulations and the popularity of liquid foundations increase the adoption of bespoke bottles and tubes. The rising online sales of beauty products drive the segment growth.

The pharmaceuticals segment held the 25% market share in 2025 due to the high production of sensitive biologics. The rise in medication self-administration and the focus on preventing accidental ingestion of medications increase the use of bespoke bottles and tubes. The degradation prevention of complex drugs and the growing topical medications increase the adoption of bespoke bottles and tubes. The burgeoning retail pharmacies support the segment growth.

The food & beverage segment held the 15% market share in 2025. The growth of the segment is attributed due to the growth in premium beverage sector. The growth in on-the-go sports nutrition and the food industry's shift towards lightweight packaging solutions increases the adoption of bespoke bottles and tubes. The improvement in the visual appeal of dairy products and the interest in energy gels increase the use of bespoke bottles and tubes.

The small (<50ml) segment dominated the market with 45% share in 2025 due to the growing use in the fragrance sample industry. The rise in personalised perfume collection and the surge in mini luxury increases use of small sizes. The huge demand for airline carry-on products and the rise in trial-sized purchases increase the adoption of small sizes. The portion control awareness and the focus on perceiving exclusivity increase the adoption of small sizes, driving the overall segment growth.

The medium (50-250ml) segment held the 38% market share in 2025 due to the airline liquid restrictions. The increased purchasing of concentrated active serums and clean beauty favor increases demand for medium sizes. The growing indie beauty labels in Europe and the rise in athleisure participation increase the adoption of medium sizes. The focus on lowering product waste and the popularity of beauty advent calendars support the segment growth.

The large (>250ml) segment held the 17% market share in 2025 due to the rise in bulk purchasing. The expansion of multi-functional skincare and the rise in refill culture increase the adoption of large sizes. The growing value-conscious shopping and the interest in multi-purpose products increase the use of large sizes. The optimized shipping, economic value, and sustainability of large sizes boost the segment growth.

The printed segment dominated the market with 40% share in 2025 due to the focus on intricate visual storytelling. The need for product tracking and the focus on eco-friendly messaging increase demand for the printed format. The innovation in digital printing and the creation of a premium feel of the product help with expansion. The growing corporate demand drives the segment growth.

The coated/frosted segment held the 25% market share in 2025 due to the need for an elegant matte texture. The light sensitivity of the skincare product and the need to improve the tactile experience increase the use of coated/frosted formats. The expansion of the refillable industry and e-commerce durability increases the use of coated/frosted formats. The silent salesperson aesthetics, concealing fingerprints, and customization versatility of coated/frosted format boost the segment growth.

The embossed/debossed segment held the 15% market share in 2025 due to its label-free aesthetics. The brand's focus on protecting its own identity and the creation of visual premiumness increases the adoption of embossed bespoke bottles and tubes. The expansion of quiet luxury and the rise in structural brands increases the adoption of embossed bespoke bottles and tubes. The instant tactile engagement, superior durability, and premium perception of embossed/debossed decoration boost the segment growth.

The B2B direct sales segment dominated the market with 55% share in 2025 due to the growing recurring order volume. The focus on technical precision and the need for total transparency increase the adoption of B2B direct sales. The focus on supply chain control and the rise in complex customization increase the use of B2B direct sales. The volume pricing and direct negotiations in B2B direct sales drive the segment growth.

The distributors & wholesalers segment held the 30% market share in 2025. The growth of the segment is increasing due to the rise in private-label brands. The higher demand for flexible quantities and pre-vetted catalogues increases the adoption of distributors & wholesalers. The prevention of overseas shipping delays and the need for specialized prototyping services increase demand for distributors & wholesalers.

The e-commerce/online procurement segment held the 15% market share in 2025 due to the price transparency and expansion of D2C. The growing startups and the focus on visualizing custom closures increase the adoption of online procurement. The expansion of omnichannel and the faster time-to-market help with growth. The high digital sourcing scalability and the well-established B2B platforms boost the segment growth.

")

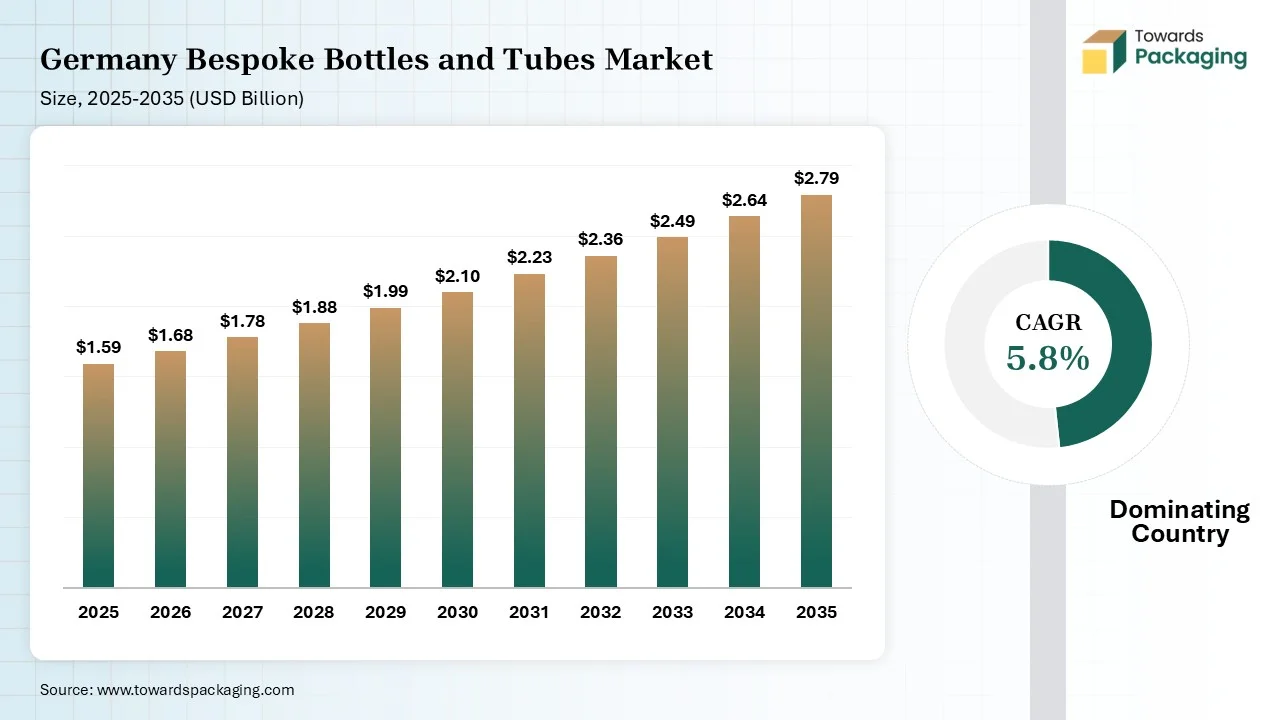

Germany is leading the market due to a well-established base for mechanical engineering. The EU packaging regulations and the expansion of the natural cosmetic industry increase demand for bespoke bottles and tubes. The rise in high-quality pharmaceutical packaging and the intricate surface decoration increases the adoption of bespoke bottles and tubes. The custom-manufactured tubes and the popularity of reusable engineered glass drive the market growth.

")

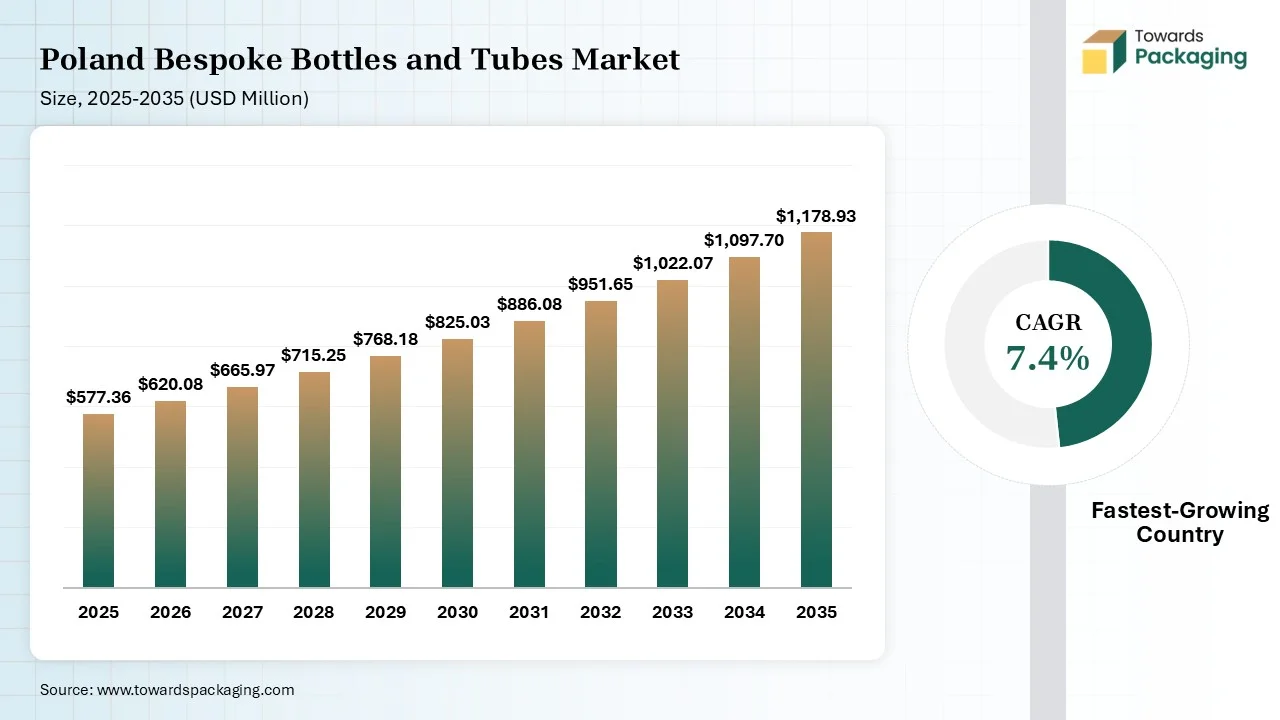

Poland is robustly growing in the market due to the expansion of the local pharmaceutical industry. The modernization of the industrial sector and the growing export of cosmetics increase demand for bespoke bottles and tubes. The expansion of beauty products and the popularity of flexible packaging increase the production of bespoke bottles and tubes. The advanced digital customization and strong logistic hub support the market growth.

By Product Type

By Material

By End-Use Industry

By Capacity

By Decoration & Customization

By Distribution Channel

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarEurope Bespoke Bottles and Tubes Market