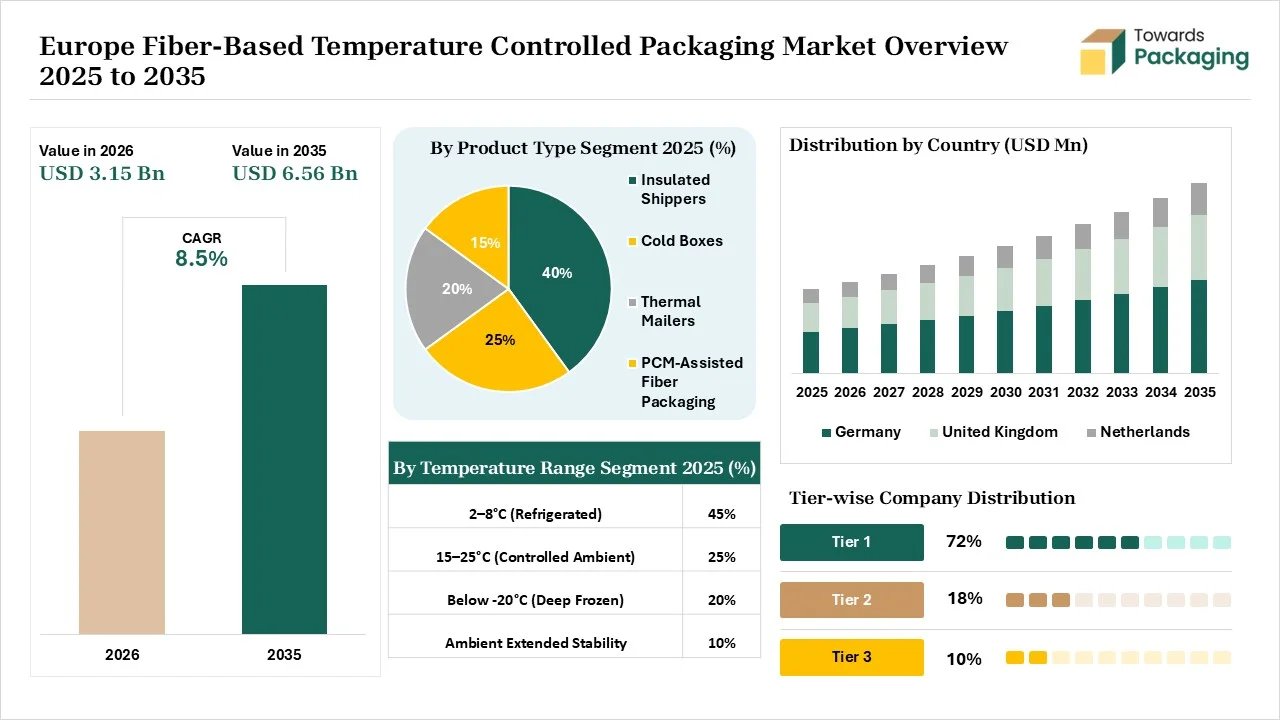

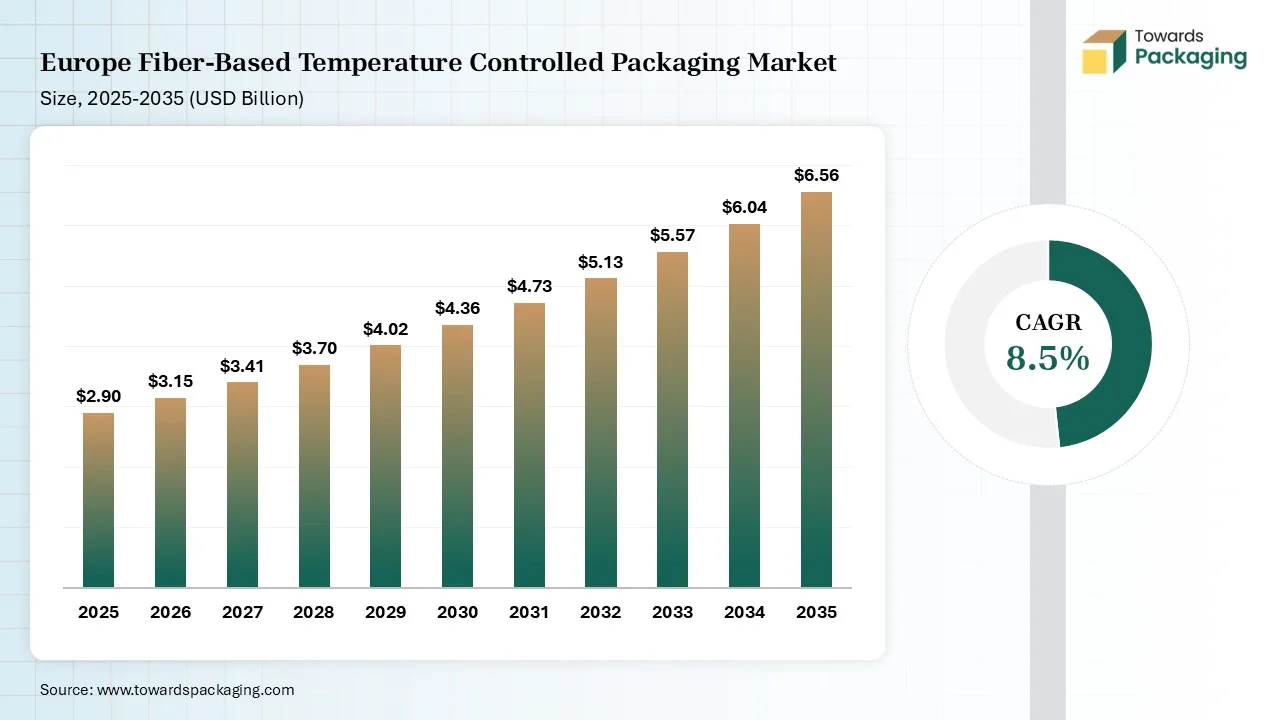

The Europe fiber-based temperature controlled packaging market is projected to grow from USD 3.15 billion in 2026 to USD 6.56 billion by 2035, registering a CAGR of 8.5% during the forecast period. The study provides an in-depth assessment of market size, revenue forecasts, segment-wise performance, regional demand patterns, company market shares, competitive benchmarking, value chain analysis, trade and import-export trends, pricing outlook, production capacity, and detailed profiles of leading manufacturers, suppliers, and industry participants. The market growth is supported by the increasing demand for premium meal kit deliveries and stringent Good Distribution Practice (GDP) regulations across Europe.

Market Size (2025): USD 2.90 Billion

CAGR (2025–2035): 8.5%

Market Volume (2025): 1.65 Billion Units

Volume CAGR (2025–2035): 9.0%

Fiber-based temperature controlled packaging is a packaging made up of sustainable thermal liners and shipping containers. They offer characteristics like high-performance insulation, customization, sustainability, and space-saving logistics. They offer benefits like superior thermal insulation, cost efficiency, excellent versatility, circular lifecycle, and cube optimization. Fiber-based temperature controlled packaging is widely used in applications like perishable food delivery, temperature-sensitive chemicals protection, floral product transportation, and the biotech cold chain.

The Europe fiber-based temperature controlled packaging market growth is driven by the push towards the circular economy, the rise in regional production of biopharmaceuticals, the shift to online grocery shopping, innovations in molded fiber, the surge in eco-friendly brands, the expansion, and the rise in convenience trends.

Europe Fiber-based temperature controlled packaging market is going through several technological developments, like parametric predictive modeling, RFID integration, blockchain traceability, embedded sensors, automated fiber modelling, and IoT integration, which help in developing advanced insulation materials, tracking temperature, and monitoring transit metrics. The market’s major revolution is the AI integration that helps in automating quality assurance.

AI easily updates the expiry dates of the products and helps in anomaly detection. AI optimizes the packaging thickness and tracks production lines. AI detects the structural deformities and minimizes manufacturing waste. AI prevents production line stoppages and detects seal failures. AI increases the accuracy of inventory and evaluates shelf-life estimation. Overall, AI helps in developing the structural design of fiber-based temperature controlled packaging.

The raw materials include recycled paper, specialty fibers, moisture barriers, natural binders, insulated box liners, virgin wood pulp, agricultural fibers, grease barriers, and phase change materials.

The material processing includes fiber preparation, insulation formation, and integration of phase change materials. The material conversion includes corrugated manufacturing, thermoforming, and coating.

The design includes steps like predictive thermal modeling, form mapping, and material evaluation. Prototyping focuses on dimensional assessment, functionality testing, and thermal validation.

The Europe fiber-based temperature-controlled packaging market includes several major players like DS Smith, Tetra Pak, va-Q-tec AG, and many more creates new products and initiatives. The UK-based company DS Smith introduced a new solution, TailorTemp, for pharmaceutical transport. The Austria-based Mondi Group collaborated with other European-based pharmaceutical & food players to develop a paper-based solution.

Papacks company uses molded plant cellulose fibers for the development of a tailored container. Va-Q-Tec company expanded its network of environmentally-friendly temperature-controlled logistics. Ranpack collaborated with RAJA to manufacture fiber-based cushioning solutions. The major company focuses on fulfilling demands for pharmaceutical cold chains.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Amcor | Zurich | Switzerland | Global leader in rigid PET packaging with extensive lightweighting programs and North American manufacturing footprint | Lightweight PET jars and containers |

| 2 | Berry Global | Evansville, Indiana | USA | Major rigid packaging supplier with strong PET container portfolio | Lightweight PET packaging solutions |

| 3 | Plastipak Packaging | Plymouth, Michigan | USA | One of North America's leading PET packaging manufacturers | PET jars, preforms, and containers |

| 4 | Silgan Plastics | Chesterfield, Missouri | USA | Major supplier of custom PET packaging for food and personal care markets | Lightweight PET jars |

| 5 | Pretium Packaging | Chesterfield, Missouri | USA | Large North American producer of PET jars and containers | PET jars for food and consumer products |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Graham Packaging | Lancaster, Pennsylvania | USA | Significant producer of rigid PET packaging across North America | PET jars and bottles |

| 2 | Alpha Packaging | St. Louis, Missouri | USA | Strong presence in food, nutraceutical, and healthcare PET packaging | Lightweight PET containers |

| 3 | Altium Packaging | Atlanta, Georgia | USA | Major rigid plastic packaging supplier with PET expertise | PET packaging solutions |

| 4 | Container and Packaging | Eagle, Idaho | USA | Supplier of PET jars for food and consumer products | Stock PET jars |

| 5 | Comar | Voorhees, New Jersey | USA | Specialized packaging provider serving healthcare and consumer markets | PET pharmaceutical jars |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | TricorBraun | St. Louis, Missouri | USA | Major packaging supplier offering lightweight PET jar solutions | PET packaging portfolio |

| 2 | Berlin Packaging | Chicago, Illinois | USA | Extensive PET container offerings and packaging innovation services | Lightweight PET jars |

| 3 | MJS Packaging | Livonia, Michigan | USA | Specialized rigid packaging supplier | PET jar solutions |

| 4 | O.Berk Company | Union, New Jersey | USA | Supplier of PET packaging for multiple industries | PET jars and containers |

| 5 | Drug Plastics Group | Boyertown, Pennsylvania | USA | Specialist in pharmaceutical and nutraceutical packaging | PET healthcare jars |

The insulated shippers segment dominated the market with 40% share in 2025 due to the rise in healthcare logistics. The surge in premium organic foods and the expansion of GLP-1 therapies increase demand for insulated shippers. The surging small payload distribution and the strong biotechnology ecosystem increase the use of insulated shippers. The last-mile boom and the rise in clinical trial shipments increase the use of insulated shippers, driving the overall segment growth.

The cold boxes segment held the 25% market share in 2025 due to the surge in biologics. The rise in at-home healthcare and the stringent pharma regulations increase the use of cold boxes. The brand's focus on green logistics and the expansion of DTC grocery deliveries increase the adoption of cold boxes. The rise in direct-to-patient deliveries and the burgeoning meal-kit deliveries support the overall segment growth.

The thermal mailers segment held the 20% market share in 2025 due to the strong focus on last-mile efficiency. The focus on minimizing warehouse storage space and the expansion of home-delivery healthcare increase the adoption of thermal mailers. The cost-effective performance, last-mile efficiency, and superior sustainability of thermal mailers help with expansion. The rise in pharma distribution and minimal preparation time boosts the overall segment growth.

The 2-80C (refrigerated) segment dominated the market with 45% share in 2025 due to high-value shipments. The stringent temperature sensitivity and the aggressive sustainability goals increase the adoption of 2-80C temperature range. The transportation of high-quality perishables and the exponential surge in mRNA vaccines increase the adoption of 2-80C temperature range. The explosion of clinical trials and the stringent biopharma requirements drive the segment growth.

The 15-250C (controlled ambient) segment held the 25% market share in 2025 due to the expansion of specialized therapeutics. The rise in oral medications and the increased development of food supplements increase the adoption of 15-250C temperature range. The burgeoning shipments of clinical trials and the surging telemedicine help with expansion. The temperature extrusion protection and passive performance enhancement support the segment growth.

The below -200C (deep frozen) segment held the 20% market share in 2025 due to a surge in cryogenic drugs. The fiber engineering advancements and the growing grocery delivery increase the adoption of below -200C temperature range. The expansion of mRNA therapeutics and bio-based insulation helps with expansion. The rise in specialty meat deliveries and the surge in fiber integration boost the segment growth.

The pharmaceuticals segment dominated the market with 38% share in 2025 due to the increased production of complex personalized medicines. The increased number of clinical trials in European countries and the growth of large-molecule drugs enhance the use of fiber-based temperature-controlled packaging. The insulin integrity focus and the protection of clinical shipments increase adoption of fiber-based temperature-controlled packaging. The burgeoning biologics manufacturing industry drives the segment growth.

The food & beverage segment held the 30% market share in 2025 due to the focus on food waste reduction. The rise in RTE deliveries and the focus on lowering the spoilage of food increase the adoption of fiber-based temperature-controlled packaging. The foodborne illness prevention and the growing online grocery delivery increase the adoption of fiber-based temperature-controlled packaging, supporting the overall segment growth.

The e-commerce & retail segment held the 20% market share in 2025 due to the high consumer preference for home delivery. The popularity of frozen foods and the expansion of natural cosmetics increase the adoption of fiber-based temperature-controlled packaging. The thriving fresh food deliveries and the shift to eco-friendly shipping increase the adoption of fiber-based temperature-controlled packaging. The explosion of e-healthcare boosts the segment growth.

The corrugated fiberboard segment dominated the market with 35% share in 2025 due to the rising utilization in biologic pharmaceuticals. The thriving biotechnology market and the transportation of temperature-sensitive items increase the adoption of corrugated fiberboard. The natural thermal insulation, high customizability, lightweight efficiency, and excellent cushioning of corrugated fiberboard drive the segment growth.

The molded fiber segment held the 30% market share in 2025 due to the move away from petroleum-based packaging. The strong next-generation thermoforming and the plastic-free targets increase the adoption of molded fiber. The focus on saving valuable warehousing and interest in eco-conscious materials increases the adoption of molded fiber. The excellent thermal insulation, superior leak resistance, and space savings in molded fiber support the segment growth.

The paperboard with insulation coatings segment held the 20% market share in 2025 due to the sustainable brand commitments. The rise in premium e-commerce and focus on keeping pharmaceuticals safe increases the adoption of paperboard with insulation coatings. The rise in the acquisition of aqueous coating and the explosion of the pharma cold chain increase the use of paperboard with insulation coatings. The premium printing efficiency, superior circularity, and excellent sustainability of paperboard with insulation coatings boost the segment growth.

The single-use shippers segment dominated the market with 50% share in 2025 due to its superior space efficiency. The need for open-ended distribution and lower upfront acquisition increases the adoption of single-use shippers. The focus on healthcare sustainability and the need to lower air freight costs increases the use of single-use shippers. The no-return logistics, cost efficiency, and operational flexibility of single-use shippers drive the segment growth.

The reusable packaging systems segment held the 20% market share in 2025 due to the pharmaceutical expansion. The growing cold-chain logistics and the structural integrity protection increase the adaptation of reusable packaging systems. The explosion of green initiatives and brand image development increases the adoption of reusable packaging systems. The strong economic viability supports the segment growth.

The foldable/flat-pack systems segment held the 15% market share in 2025. The optimization of warehouse space and the focus on lowering volumetric weight increase the adoption of foldable/flat-pack systems. The reliable insulation, driver convenience, efficient transit, and pharmaceutical efficacy of foldable/flat-pack systems help with expansion. The growing vaccine distribution boosts the segment growth.

The modular multi-compartment systems held the 15% market share in 2025. The growing high-quality biologic transport and the management of various temperature increases the use of modular multi-compartment systems. The focus on preventing cross-contamination and the need to minimize empty space increases the adoption of modular multi-compartment systems. The rise of innovation in thermal modelling supports the overall segment growth.

Germany leads the market due to the well-established life sciences hubs. The well-developed parcel delivery network and the growing transportation of temperature-sensitive vaccines increase demand for fiber-based temperature-controlled packaging. The expansion of premium meal kit subscriptions and the strong healthcare supply chains increases demand for fiber-based temperature-controlled packaging. The presence of major pharmaceutical hubs and the burgeoning online grocery shopping drive the market growth.

The United Kingdom is experiencing the fastest growth in the market. The strong focus on safeguarding sensitive payloads and the well-developed life science clusters increases demand for fiber-based temperature-controlled packaging. The surge in at-home delivery and the innovative molding technologies increases the production of fiber-based temperature-controlled packaging. The transportation of temperature-sensitive gene therapies and the penetration of online retail support the market growth.

France is substantially growing in the market. The well-established biopharmaceutical industry and the rise in export of agricultural products increase demand for fiber-based temperature-controlled packaging. The robustly expanding food delivery and the strong pharmaceutical manufacturing hub increase demand for fiber-based temperature-controlled packaging. The growing use of passive systems in the TCP industry boosts the market growth.

Italy is significantly expanding in the market. The major production hub for specialty medications and the high export rate of beverages increase demand for fiber-based temperature-controlled packaging. The surging domestic e-commerce and the rise in sustainable consumerism increase demand for fiber-based temperature-controlled packaging. The advanced manufacturing infrastructure and the rise in biologics export support the market growth.

By Product Type

By Temperature Range

By End Use Industry

By Material Type

By Packaging Format

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarEurope Fiber-Based Temperature Controlled Packaging Market