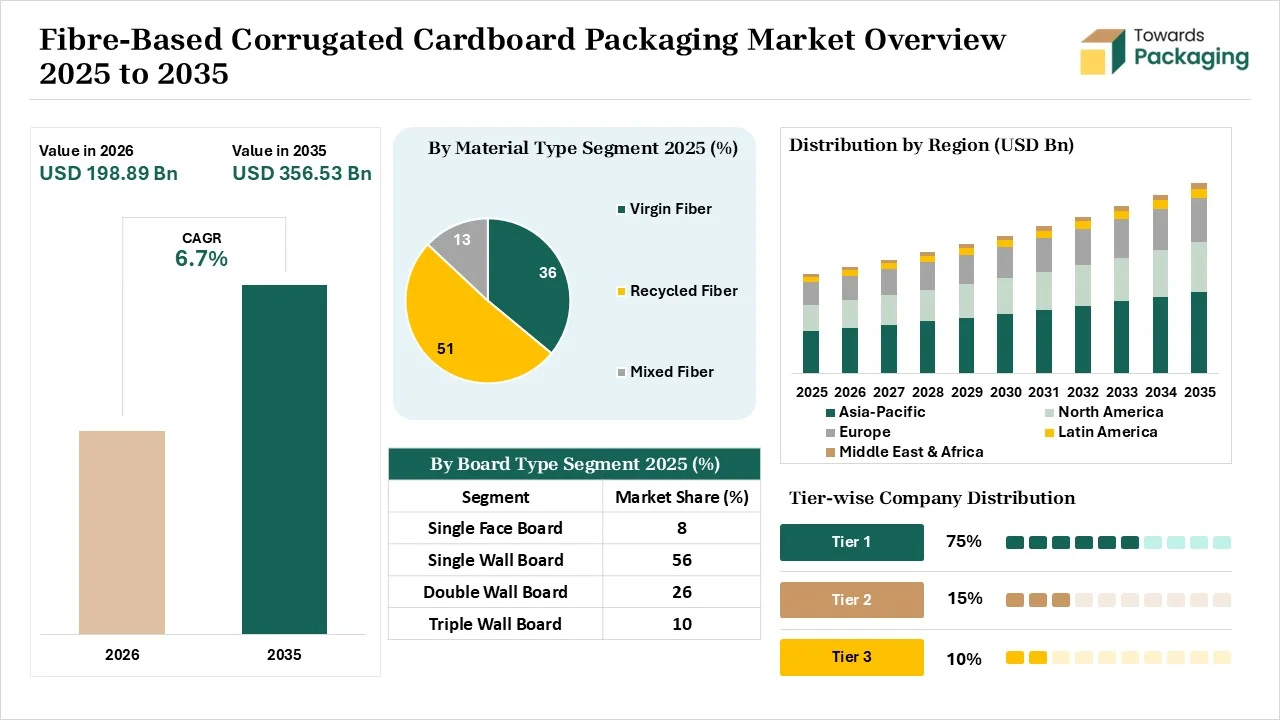

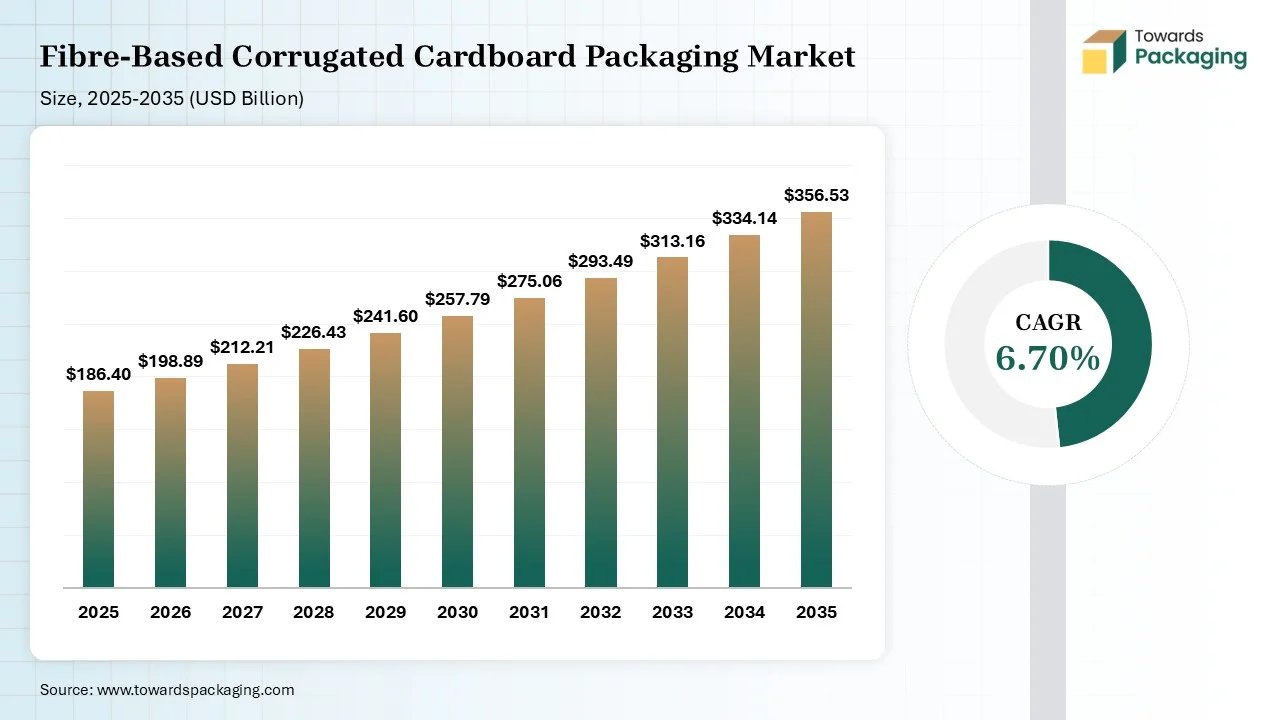

The Fibre Based Corrugated Cardboard Packaging Market is projected to grow from USD 198.89 billion in 2026 to USD 356.53 billion by 2035, registering a CAGR of 6.70% during the forecast period. This report covers market size, growth forecasts, detailed segment analysis, regional insights, country-level trends, competitive landscape, company profiles, market share analysis, value chain assessment, raw material and supply chain evaluation, import-export trade data, pricing trends, manufacturers, suppliers, distributors, technology developments, sustainability initiatives, and emerging opportunities shaping the global industry.

Fiber-based corrugated cardboard packaging is a packaging solution made up of paper-based materials. The core components of packaging are linerboard, adhesive, and fluted medium. The diverse levels of fiber-based corrugated cardboard packaging are single-wall, double-wall, and triple-wall. It offers benefits like cost-effectiveness, brand-friendliness, superior cushioning, and sustainability. It possesses characteristics like shock absorption, lightweight, and high vertical compression resistance. The common box includes Roll End Tuck Top, Telescope Boxes, FOL, RSC, Half Slotted Container, and auto-bottom. Fiber-based corrugated cardboard packaging core roles are lightweight transport efficiency, excellent branding, cushioning, and circularity.

The fiber-based corrugated cardboard packaging market growth is driven by the plastic replacement mandates, growing food industry demand, preference for automation-compatible design, smart packaging incorporation, interest in eco-friendly pulping, e-commerce expansion, advancements in lightweighting technologies, rise in short-run mass customization, green packaging demand, and the thriving packaged food sales.

Growing Omnichannel Shipping Drives Growth

The focus on elevating the convenience of the consumer and hyper-personalization increases the demand for omnichannel shipping. The frictionless digital payment systems and the growing number of omnichannel shoppers increase the rate of omnichannel shipping. The growing number of online orders and the focus on last-mile durability increase the use of fiber-based corrugated cardboard packaging.

The need for seamless reverse logistics and the need to bridge the gap between physical & online branding increases the use of fiber-based corrugated cardboard packaging. The demand for custom solutions and the need to improve brand engagement increase the use of fiber-based corrugated cardboard packaging. The sustainable replacement and enhanced traceability of omnichannel shipping help with expansion. The growing omnichannel shipping is a key driver for the growth of the market.

FMCG Demand for Plastic Substitution Unlocks Market Opportunity

The increased replacement of polystyrene inserts and EPR mandates in FMCG increases the adoption of fiber-based corrugated cardboard packaging. The modern consumer's interest in eco-friendly alternatives and the need to lower municipal waste increase the adoption of fiber-based corrugated cardboard packaging. The rising use of secondary packaging in FMCG and the complex omnichannel distribution increases the use of fiber-based corrugated cardboard packaging.

The replacement of rigid polymers and the development of attractive retail displays increase the use of fiber-based corrugated cardboard packaging. The stringent hygiene standards and the FMCG brands' transformation to fiber-based formats increase the adoption of fiber-based corrugated cardboard packaging. The FMCG demand for plastic substitution creates a great opportunity for the growth of the market.

High Energy Consumption Restricts Market Expansion

The need for high energy in the overall manufacturing of packaging increases the cost. Processes like drying heavy sheets, sourcing raw materials, and others require a high amount of electricity. The dependence on fossil-based grid energy increases the amount of energy required. The development of paper from recycled fiber and deforestation regulations increases the energy consumption, which leads to heavy compliance costs.

The growing use of massive steam boilers and the secure packaging production increases the energy consumption. The mechanical processes of fiber-based corrugated packaging production and recycling of fibers require high amounts of energy. Factors like high-pressure stream, converting machines, pulping, and low production speed increase the energy consumption. The high energy consumption is a major restraint on the growth of the market.

The fiber-based corrugated cardboard packaging market is experiencing several technological developments like machine learning, IoT integration, cloud-based ERP, automation, nanotechnology, and robotics. The developments driven by the demand for lowering material waste, eco-friendliness, and smart tracking. AI plays an important role in the market, driven by real-time quality control and automated structural design.

AI optimizes the structural integrity and predicts equipment failure. AI easily inspects flute crush and optimizes the liner weights. AI helps in sorting recyclable fibers and simulates 3D mockups. AI optimizes the cutting patterns and analyzes the printing misalignments. AI generates print-ready dielines and spots structural deficiencies. AI develops lighter packages and cuts delivery costs. Overall, AI supports design automation and sustainable manufacturing.

For instance, Smurfit Westrock uses AI for predictive supply-chain modeling and achieving right-sized packaging

Raw materials like linerboard, virgin fibers, adhesive, inks, recycled fibers, and coatings are required for manufacturing fiber-based corrugated cardboard packaging.

The material processing involves fluting, application of adhesives, bonding, heat drying, and cutting into sheets. Conversion includes printing, scoring, die-cutting, and gluing.

Design focuses on material selection, structural engineering, and digital drafting. Prototyping focuses on sample creation, physical evaluation, laboratory testing, and iterative refinement.

The logistics focuses on transport optimization, structural integrity, weight reduction, one-way supply chains, and sustainability. Distribution steps are sourcing of fiber, corrugation, conversion, palletizing, warehousing, and last-mile delivery.

In March 2026, DS Smith invested €13.4 million for the upgradation of its Denmark corrugated packaging facility. The facility is located in Grenaa, and the investment focuses on enhancing the fiber-based packaging solutions capacity. The investment aims to improve printing and converting capacities. The new plant installs a rotary die-cutting line, and the new line offers greater precision.

The Recycled Fiber Segment Dominated the Market With 51% Market Share in 2025

The recycled fiber segment dominated the fiber-based corrugated cardboard packaging market with 51% share in 2025 and is expected to grow at the fastest CAGR of 8.10% during the forecast period. The regulators' pressure on avoiding single-use plastics and the focus on eliminating the primary wood pulping cost increase the adoption of recycled fiber. The modernization in papermaking technologies and the development of closed-loop packaging increase the use of recycled fibers. The need to avoid pulping new trees and manufacturing advancements increases the use of recycled fiber, driving the segment growth.

The virgin fiber segment held the 36% market share in 2025. The long transition routes and the demand for high-end branding increase the adoption of virgin fiber. The demand for long-haul shipping protection and the need for contamination control increase the use of virgin fiber. The rise in luxury packaging and the hygiene focus in the pharmaceutical industry increases the use of virgin fiber. The high burst strength, consistent quality, and superior structural strength of virgin fibers support the segment growth.

The mixed fiber segment held the 13% market share in 2025. The growing rigorous global shipping and the focus on meeting EPR targets increase the use of mixed fiber. The prevention of packaging structural integrity and the focus on bypassing forestry reliance increase the use of mixed fiber. The eco-friendly substitute demand and the creation of thinner packaging increase the use of mixed fiber. The popularity of mixed-fiber corrugated fanfold boosts the segment growth.

The Single Wall Board Segment Dominated the Market With 56% Market Share in 2025

The single wall board segment dominated the fiber-based corrugated cardboard packaging market with 56% share in 2025. The focus on protecting products from vibrations and increased everyday shipping of electronics increases the adoption of single wall board. The reduction of transit expenses and the need to balance print quality increase the use of single wall board. The regional recycling mandates and the booming delivery industry increase the adoption of single wall board. The lower shipping cost and high cost-effectiveness of single wall board drive the segment growth.

The double wall board segment held the 26% market share in 2025. The growth in parcel-drop standards and the long-distance distribution increases the use of double wall board. The circular-economy alternatives demand and the increased moving of industrial equipment increase the demand for double wall board. The growing long-distance automotive shipping and the rough handling in e-commerce increase the use of double wall board, boosting the segment growth.

The triple wall board segment held the 10% market share in 2025 and is expected to grow at the fastest CAGR of 8.40% during the forecast period. The growing wood substitution and the demand for holding extreme weights increase the use of triple wall board. The rising heavy-industrial exports and the longer transit distances increase the use of triple wall board. The high-value goods protection demand and the transportation of heavy automotive components increase the use of triple wall board. The excellent weight-bearing capacity and the high structural integrity of triple wall board support the segment growth.

The C Flute Segment Dominated the Market With 31% Market Share in 2025

The C flute segment dominated the fiber-based corrugated cardboard packaging market with 31% share in 2025. The need for stacking boxes in trucks and the irregularities in the product shape increase the use of C flute. The focus on lowering washboarding and the need to increase the use of recycled fiber increase the adoption of C flute. The printing of product information on packaging and the rise in general shipping cases increase the use of c flute. The balanced printability, excellent all-round cushioning, and optimal compression of C flute drives the segment growth.

The B flute segment held the 18% market share in 2025. The focus on less shipping space and demand for a consistent outer surface increases the adoption of B flute. The increased packaging of compact electronics and the structural stability focus increase the adoption of B flute. The demand for material-efficient alternatives and the production of compact mailer boxes increases the use of B flute. The transportation of canned goods boosts the segment growth.

The F flute segment held the 5% market share in 2025 and is expected to grow at the fastest CAGR of 8.9% during the forecast period. The demand for flat printing surfaces across diverse industries like cosmetics and the interest in fiber-based solutions increase the use of F flute. The increased penalizing of bulky boxes and the rising replacement of solid boards increases the adoption of F flute. The rise in spot-UV printing and the focus on protecting fragile items increases the use of F flute. The focus on the reduction of pallet heights supports the overall segment growth.

The Corrugated Boxes Segment Dominated the Market With 58% Market Share in 2025

The corrugated boxes segment dominated the fiber-based corrugated cardboard packaging market with 58% share in 2025. The heavy items transportation and the growing demand for packaging solutions that support frequent handling increase the use of corrugated boxes. The digital printing availability and the presence of renewable wood fibers increase the production of corrugated boxes. The multi-stop delivery of parcels and the focus on fuel cost reduction increase the use of corrugated boxes. The easy customization and superior structural strength of corrugated boxes drive the segment growth.

The corrugated sheets segment held the 10% market share in 2025. The use of secondary packaging in quick commerce deliveries and legal sustainability targets in brands increases the use of corrugated sheets. The elimination of excess filler materials in packaging and the higher utilization of stackable packaging increase the adoption of corrugated sheets. The innovations, such as lighter corrugated sheets, boost the segment growth.

The die-cut packaging segment held the 9% market share in 2025 and is expected to grow at the fastest CAGR of 8.60% during the forecast period. The increased purchasing of precisely-sized boxes and the supermarkets' demand for die-cut display trays increases the use of die-cut packaging. The shift away from shrink-wrapped trays made with plastics and inline printing innovations increases the use of die-cut packaging. The rise in DTC marketing and the strong need for dimensional weight optimization increase the use of die-cut packaging. The advancing digital die-cutting supports the segment growth.

The Flexographic Printing Segment Dominated the Market With 63% Market Share in 2025

The flexographic printing segment dominated the fiber-based corrugated cardboard packaging market with 63% share in 2025. The increased manufacturing of finished RSC in a single pass and the long FMCG manufacturing runs increase the use of flexographic printing. The integration of fast-drying inks and the low marginal cost of flexographic printing help with the expansion. The incorporation of UV-curable inks and the focus on inline processing efficiency increase the use of flexographic printing. The unmatched production speed, eco-friendly compliance, and substrate compatibility of flexographic printing drive the segment growth.

The offset lithography segment held the 16% market share in 2025. The focus on e-commerce appeal and the need to increase consumer conversion rates increases the adoption of offset lithography. The increased use of offset-laminated boxes and the demand for exceptional graphic quality increase the use of offset lithography. The increased printing of complex gradients and demand for consistent color accuracy increase the adoption of offset lithography, boosting the segment growth.

The digital printing segment held the 15% market share in 2025 and is expected to grow at the fastest CAGR of 10.80% during the forecast period. The rise in limited-edition campaigns and the increased printing of marketing graphics on both sides of the cardboard increase the adoption of digital printing. The integration of QR codes in brands' packaging and the focus on minimizing physical waste increase the use of digital printing. The creation of an excellent unboxing experience and seasonal promotions increases the use of digital printing. The fast setup, supply chain agility, and lower lead times in digital printing support the segment growth.

The Food & Beverages Segment Dominated the Market With 29% Market Share in 2025

The food & beverages segment dominated the fiber-based corrugated cardboard packaging market with 29% share in 2025. The need to protect glass bottles and the huge demand for frozen foods increase the adoption of fiber-based corrugated cardboard packaging. The high environmental sustainability pressure on fast-food chains and the need to maintain the longevity of beverages increase the use of fiber-based corrugated cardboard packaging. The popularity of shelf-ready packaging in organized retail and the spoilage prevention demand during transit increases the use of fiber-based corrugated cardboard packaging. The increased storage of refrigerated liquids drives the segment growth.

The e-commerce & logistics segment held the 24% market share in 2025 and is expected to grow at the fastest CAGR of 9.20% during the forecast period. The rise in handling of e-commerce packaging multiple times and the expensive return rates of parcels increases the use of fiber-based corrugated cardboard packaging. The lightweight packaging needs and the expansion of box-on-demand technology increase the adoption of fiber-based corrugated cardboard packaging. The focus on reinforcing brand identity and the complex touchpoints in e-commerce distribution increases the use of fiber-based corrugated cardboard packaging, supporting the segment growth.

The consumer electronics segment held the 10% market share in 2025. The growing online sales of electronics items and the superior protection demand for items like laptops increase the use of fiber-based corrugated cardboard packaging. The focus on safeguarding delicate screens and the focus on avoiding physical damage to electronic products increases the adoption of fiber-based corrugated cardboard packaging. The increased buying of gaming consoles through D2C supports the segment growth.

The Direct Sales Segment Dominated the Market With 61% Market Share in 2025

The direct sales segment dominated the fiber-based corrugated cardboard packaging market with 61% share in 2025. The demand for direct partnerships with packaging manufacturers increases the use of direct sales. The focus on integrated logistics and the high volume of orders increases the use of direct sales. The need for close monitoring of environmental impact and focus on ensuring material traceability increases the use of direct sales. The creation of personalised board grades and supply chain continuity demand increases the use of direct sales, driving the segment growth.

The packaging distributors segment held the 29% market share in 2025. The preference for standardized shipping boxes and the demand for just-in-time delivery increase the adoption of packaging distributors. The focus on efficient sourcing of materials and the changing design needs increases buying from packaging distributors. The highly optimized cardboard demand and the smaller quantities production increase the adoption of packaging distributors, boosting the overall market growth.

The online sales segment held the 10% market share in 2025 and is expected to grow at the fastest CAGR of 9.40% during the forecast period. The growing number of SMEs and the creation of dynamic 3D designs increase the adoption of online sales. The growing ordering of promotional packaging and the focus on prototype packaging immediately increases the use of online sales. The standardized quality focus and automating reorder points help with expansion. The automated specification workflows and on-demand customization in online sales support the segment growth.

Asia Pacific dominated the fiber-based corrugated cardboard packaging market in 2025 with a 43% share and is expected to grow at the fastest CAGR of 8.10% during the forecast period. The massive machinery manufacturing base and the explosion of D2C consumer delivery increase the demand for fiber-based corrugated cardboard packaging. The implementation of stricter legislation across ASEAN countries and the strong F&B industry increases the use of fiber-based corrugated cardboard packaging. The large export of electronics and the rapid digitization have increased the use of fiber-based corrugated cardboard packaging. The last-mile delivery expansion drives the market growth.

China held the largest share in the market in 2025. The high manufacturing quantities of industrial goods and the presence of an integrated pulp-to-packaging ecosystem increase the production of fiber-based corrugated cardboard packaging. The expanding JD.com platforms and the strong recycled fiber ecosystem increase the use of fiber-based corrugated cardboard. The high adoption rate of recyclable corrugated alternatives supports the market growth.

India is experiencing rapid growth in the market. The shift to paper packaging and the skyrocketing of online shopping have increased the use of fiber-based corrugated cardboard packaging. The unprecedented growth in processed beverages and the expansion of micro-fulfillment centers increase the use of fiber-based corrugated cardboard packaging. The growing pharmaceutical deliveries boost the overall market growth.

North America held the 26% market share in 2025. The increased use of right-sized packaging in e-commerce and the plastic substitution policies increases the adoption of fiber-based corrugated cardboard packaging. The compostable packaging targets and the rise in transportation of health supplements increase the use of fiber-based corrugated cardboard packaging. The rise in micro-flute technologies and the burgeoning industrial manufacturing drives the market growth.

The United States is a major contributor to the market. The higher demand for cost-effective shipping containers and the focus on fulfilling the demand of eco-conscious shoppers increase the use of fiber-based corrugated cardboard packaging. The multi-stop distribution of the products and EPR statutes increases the use of fiber-based corrugated cardboard packaging. The adoption of high-speed inkjet supports the market growth.

Mexico is experiencing the fastest growth in the market. The availability of foreign direct investment and the presence of e-commerce giants increase the adoption of fiber-based corrugated cardboard packaging. The shift away from rigid plastics and the presence of domestic automated corrugator plants increase the production of fiber-based corrugated cardboard packaging. The AI-enabled designs boost the overall market growth.

Europe held the 23% market share in 2025. The massive recycling rates across the region and the online retail boom increase demand for fiber-based corrugated cardboard packaging. The grease-resistant coatings innovations and the development of fully recyclable packaging increase the adoption of fiber-based corrugated cardboard packaging. The development of a moisture-resistant board and the innovations in shelf-ready designs support the market growth.

Germany holds the major market share in 2025. The aggressive packaging regulations in food brands and the need to optimize transit space during transportation increase the use of fiber-based corrugated cardboard packaging. The strong commercial paper recycling infrastructure and the increased use of smart tools in corrugating facilities increase the production of fiber-based corrugated cardboard packaging. The high-tech engineering infrastructure boosts the overall market growth.

France is growing in the market. The regulations, like AGEC, and the consumer's move to online shopping, increase the demand for fiber-based corrugated cardboard packaging. The presence of advanced design labs and the luxury brands' commitment to sustainability increases the use of fiber-based corrugated cardboard packaging. The soaring number of e-commerce shipments supports the overall market growth.

Latin America held the 5% market share in 2025. The growing online retail hubs in Latin American countries and the burgeoning agro-industrial exports increase the adoption of fiber-based corrugated cardboard packaging. The government's efforts to lower plastic waste and the focus on enhancing domestic manufacturing capacities increase the production of fiber-based corrugated cardboard packaging. The thriving global trade supports the overall market growth.

Brazil dominated the market in 2025. The higher demand for micro-flute corrugated boxes helps market expansion. The federal sustainability initiatives and the thriving perishable food industry increase the adoption of fiber-based corrugated cardboard packaging. The presence of paper leaders and the high-graphics corrugation increases the production of fiber-based corrugated cardboard packaging. The expansion of agribusiness boosts the market growth.

Argentina is rapidly expanding in the market. The rise in last-mile logistics and the shift away from aluminum pouches increase the adoption of fiber-based corrugated cardboard packaging. The strong dairy transportation infrastructure and the upgradation of industrial automation increase the use of fiber-based corrugated cardboard packaging. The environmental responsibility of brands and technological modernization drives the market growth.

The Middle East & Africa held the 3% market share in 2025. The interest in modular corrugated containers and the safe international delivery demand increases the adoption of fiber-based corrugated cardboard packaging. The corporate efforts for accelerating eco-friendly packaging use help with the expansion. The growing equipment shipping and the rise in regional trade integration drive the market growth.

Saudi Arabia is a key contributor to the market. The focus on avoiding last-mile delivery challenges and the national food security focus increases the adoption of fiber-based corrugated cardboard packaging. The rising biodegradable fiber packaging helps with expansion. The growing non-oil exports and the interest in export-ready packaging boost the market growth.

The United Arab Emirates is experiencing robust growth in the market. The expansion of Amazon UAE and the large distribution centers increases the adoption of fiber-based corrugated cardboard packaging. The investment in micro-flutes and the advancements in printing technology help with the expansion. The major parcel volumes support the market growth.

| Rank | Company | Headquarters | Country | Major Contribution to Fibre-Based Corrugated Cardboard Packaging Market | Key Packaging Products and Services |

| 1 | Smurfit WestRock plc | Dublin, Ireland | Ireland | The company operates dozens of recycling plants & paper mills. The company also acquired Ecuador-based corrugated packaging company Cartomanabi. | Retail Ready Packaging & Trays, Molded Fiber Packaging, Corrugated Pallets & Slip Sheets, Standard & Heavy-Duty Corrugated Boxes, CanCollar, FiberSeal |

| 2 | Oji Holdings Corporation | Tokyo, Japan | Japan | The company introduced a new corrugated packaging plant in India at Sri City to enhance packaging production. The company focuses on liquid packaging recycling. | HiPLE-ACE, Paper Pallets, Flexo-Printed Corrugated Containers, Die-Cut Displays, Weather-Resistant Produce Boxes, Heavy-Duty Corrugated Containers |

| 3 | Packaging Corporation of America (PCA) | Lake Forest, Illinois, United States | United States | The company operates many containerboard mills and focuses on the development of fit-to-purpose containers. | Containerboard, Heavy-duty Corrugated Boxes, Record Storage Boxes, High-Impact Retail Displays |

| 4 | Graphic Packaging Holding Company | Atlanta, Georgia, United States | United States | The company manufactures heavy-weight cartons and invested multi-million dollars for the production of Coated Recycled Board. | Strength Packaging, SIOC Packaging, Barrier Papers, LithoFlute, Folding Cartons |

| 5 | International Paper Company | Memphis, Tennessee, United States | United States | The company’s annual production capacity of Old Corrugated Containers is approximately 7 million. The company invested $225 million to expand the Mississippi facility. | MaxNest, SpaceKraft, Corrugated Sheets, eCommerce Solutions |

By Material Type

By Board Type

By Flute Type

By Product Type

By Printing Technology

By End-Use Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarFibre-Based Corrugated Cardboard Packaging Market