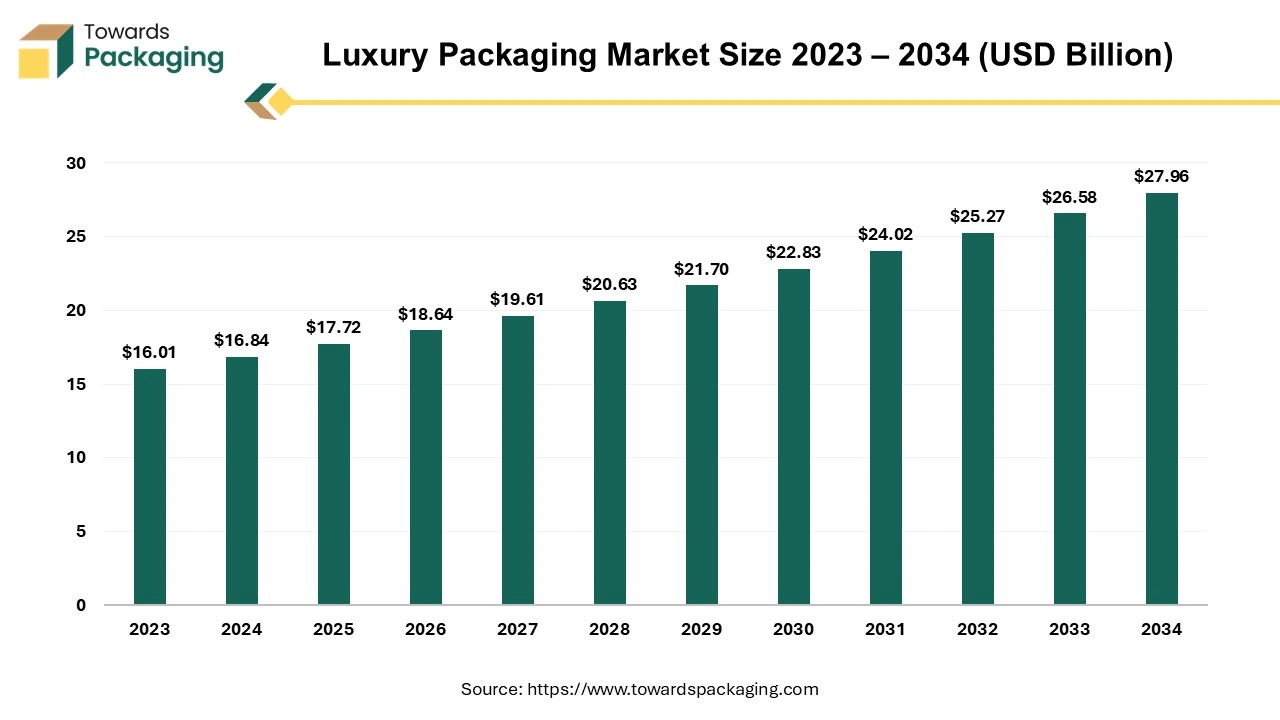

The luxury packaging market is forecasted to expand from USD 18.64 billion in 2026 to USD 29.41 billion by 2035, growing at a CAGR of 5.2% from 2026 to 2035. The market is deeply segmented by material (paperboard, plastic, glass, and metal), product type (bags, bottles, pouches, boxes), and end-use (cosmetics & fragrance, food & beverage, consumer goods). The analysis covers the regional market shares across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Key players in the market include Delta Global, WestRock Company, and DS Smith, among others.

The luxury packaging is a section of the packaging business focusing on luxury goods. This market is focused on developing packaging solutions that match and improve the premium nature of high-end products such as cosmetics, perfumes, jewellery, watches, and designer clothing. The luxury goods sector is changing significantly, with sustainability and digitalization emerging as crucial change drivers. What was once the domain of a small group of environmentally concerned innovators is becoming more common, with luxury brands embracing changes in customer tastes and regulatory needs.

Luxury brands are shifting their approach, including sustainability principles into long-term goals and leveraging digital technologies to improve consumer engagement and create immersive luxury shopping experiences. Luxury goods sales have skyrocketed, exceeding pre-pandemic levels and setting new records. In fiscal year 2022, the Top 100 luxury goods businesses reached composite sales of US$347 billion, a significant rise from the previous record of US$305 billion. Luxury goods sales of more than $5 billion accounted for roughly 70% of overall sales within this exclusive category.

The overall revenue for James Copper in the global luxury packaging business is expected to be £129.7 million by 2023. This amount comprises a capital expenditure of £5.8 million, which represents the company's investment in operations and expansion projects. Furthermore, James Copper has a 34% share of the luxury packaging market, indicating its enormous presence and influence in the business.

Prominent packaging providers can enhance the overall customer experience because they have access to various superior materials and distinctive designs. As a result, there is an increase in demand for luxury packaging solutions as firms focus more on design, production techniques, and overall product development. The market for luxury packaging is hugely competitive and highly fragmented, and we are seeing a rise in the number of new businesses entering quickly expanding sectors.

Packaging for products under luxury brands is considered luxury packaging. Packaging that is biodegradable and sustainable is a recent trend that is propelling the industry. By 2025, the luxury packaging market in Asia Pacific is expected to reach a valuation of over seven billion US dollars.

Leading suppliers are invading the global luxury packaging market, fuelled by the middle class's increasing income levels and the expansion of regional infrastructure. Due to this migration, there is more competition among regional and multinational businesses as they compete for market share. Because of this, there is intense competition across firms in the sector, forcing them to innovate and set themselves apart to win over customers' interest and loyalty.

For Instance,

The competitive landscape of the luxury packaging market is characterized by established industry leaders such as Delta Global, WestRock Company, DS Smith plc, Design Packaging Inc., Lucas Luxury Packaging, Prestige Packaging Industries, Luxpac Ltd., Keenpac, GPA Global, Ardagh Group, McLaren Packaging and Fleet Luxury Packaging. These giants face competition from emerging direct-to-consumer brands, leveraging digital platforms for market entry. Key factors influencing competition include innovation in product offerings, sustainable practices, and the ability to adapt to changing consumer preferences.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Verescence | Paris | France | Global luxury glass packaging leader | Fragrance and cosmetics bottles |

| 2 | Pochet Group | Paris | France | Premium beauty packaging specialist | Luxury glass and closures |

| 3 | AptarGroup | Crystal Lake, Illinois | USA | Premium dispensing and closure systems | Beauty and fragrance packaging |

| 4 | Albéa Group | Gennevilliers | France | Luxury cosmetic packaging provider | Tubes, jars, airless systems |

| 5 | Quadpack | Barcelona | Spain | Sustainable premium beauty packaging specialist | Luxury cosmetic packaging |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | James Cropper | Cumbria | United Kingdom | Premium paper packaging specialist | Luxury cartons and gift boxes |

| 2 | Fedrigoni | Verona | Italy | Luxury paper and label materials leader | Premium papers and labels |

| 3 | HH Deluxe Packaging | Hong Kong | Hong Kong | High-end luxury packaging supplier | Rigid boxes and retail packaging |

| 4 | Texen | Izernore | France | Luxury beauty packaging specialist | Premium closures and accessories |

| 5 | Bormioli Luigi | Parma | Italy | Premium glass packaging producer | Luxury bottles and containers |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | PakFactory | Ontario | Canada | Custom premium packaging solutions | Luxury rigid boxes |

| 2 | Bennett Packaging | Manchester | United Kingdom | Boutique luxury packaging provider | Custom luxury packaging |

| 3 | Robinson Packaging | Chesterfield | United Kingdom | Premium retail packaging solutions | Luxury cartons |

| 4 | McLaren Packaging | Glasgow | United Kingdom | Luxury folding carton specialist | Premium packaging solutions |

| 5 | Prestige Packaging Industries | New York | USA | Specialty luxury packaging supplier | Premium gift packaging |

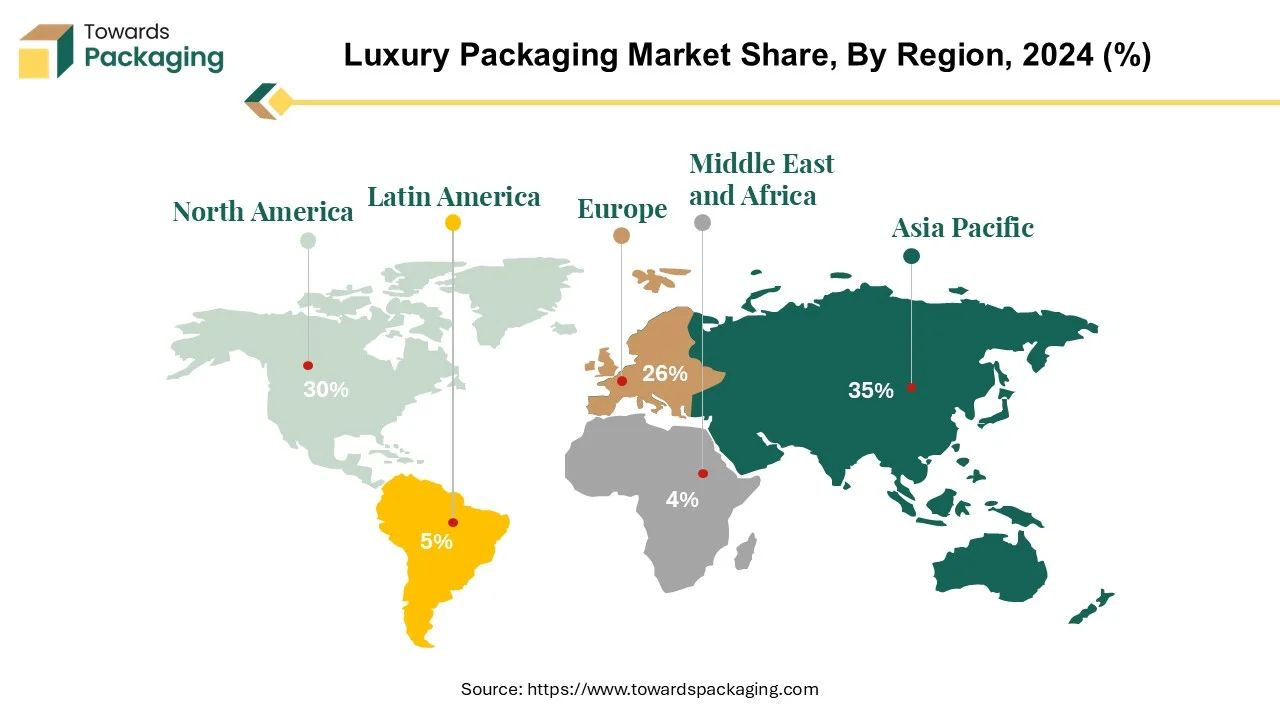

Asia Pacific dominated the luxury packaging market in 2024. The market growth in the region is attributed to the increasing demand for sustainable packaging solution, increasing demand for premium products, increasing disposable incomes and increasing demand for premium products. China and India are dominating countries driving the market growth. The government has implemented various policies to inspire luxury packaging in India.

The Asia-Pacific region emerges as the global leader in luxury packaging, driven by rising disposable income and increased consumer expenditure on luxury goods. The high population expansion and widespread urbanization throughout the region justify this trend. These demographic transitions have promoted an urban lifestyle, resulting in changes in consumer preferences and increased demand for luxury products. Growth prospects for the region remain positive, albeit with more significant pressure and disruptive changes.

Even if the luxury packaging industry's growth in China and other Asian markets may be slowing down, these markets are still expected to remain the main drivers of the expansion. The fashion and cosmetics industries have witnessed a significant increase in product releases, driving market expansion. Environmental concerns have also made sustainable packaging solutions more popular. Notably, major worldwide brands are focusing increasingly on emerging economies, including China, realizing that the country is becoming the world's largest purchaser of luxury goods.

Asia-Pacific area is a dominant force in the luxury packaging market, emphasizing how important it is to meet discriminating customers' changing needs and tastes. Luxury brands in the region need to modify their approaches to effectively seize market prospects as the economy and urbanization continue to rise. Using the growing demand for luxury goods in emerging nations, in addition to adopting sustainable packaging techniques, is necessary to achieve this. By conforming to these patterns, businesses may set themselves up for long-term success and take advantage of the luxury packaging market's explosive growth in the Asia-Pacific region.

For Instance,

North America is expected to grow fastest during the forecast period. The market growth in the region is driven by the increasing use of sustainable packaging practices and materials, growing personal care and cosmetics industries and increasing demand for customized and premium packaging solutions. The U.S. is the fastest growing country contributed to propel the market growth.

North America is the second top region in the luxury packaging market, with around 54% of American customers aware of environmental programs such as the Sustainable Forestry Initiative. This expanding consumer awareness highlights the growing importance of sustainability in the luxury packaging industry. Top luxury companies in North America, including market titans like LVMH and Hermès, have released striking financial results for the year's first half. Revenue for LVMH increased by an astounding 15% to $46.5 billion, and revenue for Hermès increased by a significant 25% to $7.4 billion.

Similarly, Richemont saw a 19% increase in revenue during its first fiscal quarter, reaching $5.9 billion after accounting for constant exchange rates. These remarkable topline increases indicate the region's robust consumer demand and market need for premium goods.

For Instance,

The luxury packaging sector is transitioning significantly towards sustainability, consistent with broader consumer preferences and corporate social responsibility endeavors. Luxury firms prioritize sustainable packaging solutions to suit changing consumer needs as they become more aware of environmental issues. This emphasis on sustainability not only meets consumer expectations but also offers significant opportunities for expansion for the packaging industry overall. Leading luxury brands in the region have strong financial performances, highlighting North America's role as a significant participant in the luxury packaging market. Consumer awareness of sustainability is also vital. Sustainability is expected to stay at the forefront of industry evolution, spurring growth and innovation in the luxury packaging market.

For Instance,

Paper and board have become popular in luxury packaging, providing a diverse canvas for elaborate graphics and intriguing ornamentation. These materials have unique qualities ideal for luxury products' premium nature. Laminations, one-of-a-kind coatings, and sophisticated embossing and debossing processes increase the visual appeal of luxury packaging, attracting discerning customers. Furthermore, paper and board packaging have incredible strength and a luxury tactile sensation, which improves the whole product experience. Paper and board are still the favored choices for luxury firms looking for packaging strategies prioritizing sustainability and innovation because of their adaptability, visual attractiveness, and green credentials.

Paper and board stand out for their capacity to give buyers the impression that the product is of higher quality, even though cardboard is one of the materials used in packaging more frequently than metal, glass, plastic, and wood. The European Paper Recycling Council (EPRC) reports that 2019 the percentage of paper recycled in Europe remained high at 72%. This accomplishment is attributable to the European paper industry's consistent use of paper for recycling (PfR).

For Instance,

Paper has long been a common packaging material in the premium wine and spirits industry. Craft beer businesses also use paper labels to convey the exceptional quality or craftsmanship of their products. Brands may satisfy the changing needs of environmentally concerned consumers and raise the perceived worth of their products by using these materials in the packaging of luxury goods. The combination of strength, visual attractiveness, and environmental sustainability that paper and board provide is essential to luxury packaging. Premium companies may use these materials to develop packaging solutions that improve the product experience and meet customer expectations and sustainability targets as consumer preferences change.

For Instance,

Bags have recently gained popularity, with both men and women spotted carrying them practically everywhere, including schools, malls, businesses, and grocery stores. The fashion industry can be credited for some of this spike in popularity. Paper bags are a popular accessory since prominent clothing companies frequently design them with their emblem or brand name. Individuals who carry these bags gain recognition since they symbolize ownership of high-quality goods and add a touch of sophistication to their look. Printing a company's name or emblem on paper bags is a practical marketing approach that promotes brand awareness wherever the bag is handled. Furthermore, many individuals favour paper bags for their ease, cleanliness, and ability to hold many things.

Paper bags' positive effects on the environment are another reason for their rising popularity. Paper bags are 100% recyclable, biodegradable, and reusable, making them a more environmentally responsible option than plastic bags. Customers concerned about sustainability and lessening environmental impact are drawn to this environmentally-minded feature. Paper bags are also less harmful to animals than plastic bags, which makes them even more appealing to people who care about the environment.

Bags link with designer labels, convenience, and environmental benefits have contributed to their soaring popularity. Paper bags will continue to be a popular alternative for carrying goods and helping the environment as long as people prioritize sustainability and eco-friendly options.

For Instance,

The cosmetics and fragrance sectors of the luxury packaging market have seen a significant transition, with a fundamental move towards premiumization. This trend, known as the "new lipstick effect," is powerful in the premium fragrance market. Premiumization highlights the growing demand for items that convey sophistication, luxury, and intricacy, as evidenced by the intricate and opulent packaging designs throughout the sector. The "new lipstick effect" trend has considerably impacted the global luxury business, with packaging impacting customer views and brand image. Brands are investing extensively in developing packaging that protects and maintains the product while serving as a tangible reflection of luxury and elegance. This emphasis on premium packaging reflects consumers' desire to have a wealthy and aspirational experience when purchasing luxury cosmetics and fragrances.

Luxury packaging in the cosmetics and fragrance industries has grown to include novel materials, complex details, and distinctive design aspects to engage consumers and differentiate businesses in a competitive market. Packaging has evolved from expensive glass bottles covered with ornate embellishments to sleek, minimalist designs expressing subtle luxury, serving as a significant differentiator and essential component of brand storytelling.

Richemont, Chow Tai Fook, and PVH, the three businesses whose fiscal years finish in Q1, experienced the largest increases in revenues in FY2022 (by 50%, 41%, and 33%, respectively), as the pandemic's effects subsided. Between 9% and 29% more sales were made by other Top 10 companies.

For Instance,

Between January 1 2022, and September 1 2023, the top luxury goods companies displayed heightened strategic activity compared to usual. This included significant acquisitions, product launches, and divestitures in sectors such as luxury beauty, watches, and retail, as well as the internalization of licensee operations. The table below summarizes the major deals during this period. Additionally, Tapestry is included as it has the potential to enter the Top 10 list in the fiscal year 2023/2024, pending approval of a relevant deal.

| Company | Activity | Deal Value | Date Announced |

| Kering |

Launched Kering Beauté Acquired Maui Jim eyewear Acquired Creed luxury fragrance Acquired Valentino (30% with 100% option) |

Est €1.5 billion Est €3.5 billion €1.7 billion |

Feb-23 Mar-22 Jun-23 Jul-23 |

| Richemont |

Sale of controlling interest in online luxury retailer YOOX NET-A-PORTER (Y). Acquired Gianvito Rossi. |

Est €3.4 billion n/a |

Aug-22 Jul-23 |

| Estee Launder |

Wound down Designer Fragrance Licensing Division. Acquired TOM FORD brand. |

n/a US$2.8 billion |

Jul-22 Nov-22 |

| L'Oreal | Acquired AÄ“sop brand from Natura & Co. | US$2.525 billion | Apr-23 |

| PVH | Will bring Calvin Klein and Tommy Hilfiger women’s North America wholesale business back in house by 2025-2027. | n/a | Nov-22 |

LVMH expanded its lead among the world's luxury goods corporations in FY2022, with personal luxury goods sales of approximately US$60 billion, up 22.6% yearly. Kering's net luxury goods sales surpassed €20 billion for the first time in fiscal year 2022, up 15.3%. Revenue. Richemont, situated in Switzerland, had the highest increase among the Top 10 firms in FY2022, with luxury goods brand sales increasing by 50.1%. The Estée Lauder Companies (ELC), a US-based cosmetics behemoth, increased its luxury goods sales by 9% in FY2022, with double-digit growth in the Americas and EMEA. Chanel Limited reported net sales growth of 10.1% in FY2022 (17.0% at constant currency exchange rates), with increasing sales volumes accounting for about half.

The shift towards premiumization in the cosmetics and fragrance sectors underscores the importance of packaging as a strategic tool for luxury brands to convey exclusivity, sophistication, and desirability to discerning consumers. As the demand for luxury experiences grows, packaging will remain critical in shaping brand identity and driving consumer engagement in these dynamic and evolving market segments.

For Instance,

Sustainable and biodegradable packaging has emerged as a key market driver in response to rising consumer awareness of environmental issues and a demand for more eco-friendly lifestyles. As a result, many organizations are increasingly prioritizing sustainability in their operations.

For instance,

Consumers choose paper and cardboard packaging because of their ecological features, especially home compostability. Furthermore, these materials are viewed as the most recyclable, with 41% of consumers believing that the recycling rate in the United States is greater than 50%. Recycling rates for paper packaging are 73%, while cardboard packaging is 88%. This strategic commitment to sustainability is consistent with Estée Lauder's goals for sustainable packaging. By 2025, the company hopes to have 50% of its packaging made of post-consumer recycled (PCR) materials. Furthermore, Estée Lauder's collaboration with Origins highlights efforts to ensure that at least 80% of the brand's packaging, by weight, is recyclable, refillable, reused, recycled, or recoverable by 2023.

The transition to sustainable packaging is a more significant movement towards environmental awareness and responsibility in the consumer products industry. Companies understand the need to implement sustainable practices to meet consumer expectations while contributing positively to environmental conservation efforts.

For instance,

The market for luxury goods has expanded worldwide, with top brands increasing their presence in many countries. Most luxury goods come from major European brands, which make up about 70% of global sales. This shows their long history and strong influence.

Sales of luxury goods have grown in non-Western regions due to more wealthy urban consumers and a younger, Western-oriented population. Much of the global luxury goods market's growth is driven by China. Recent analysis suggests that without Chinese consumers, global luxury sales would have dropped by about 2% on average between 2012 and 2015.

Shopping for luxury items while traveling is becoming more popular, especially among the emerging middle class in China and other countries. Airport malls are a key location for this type of shopping. In 2016, shoppers at airport malls made up 6% of total worldwide luxury goods spending, up from 4% in 2015.

By Material

By Product Type

By End Use

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarLuxury Packaging Market