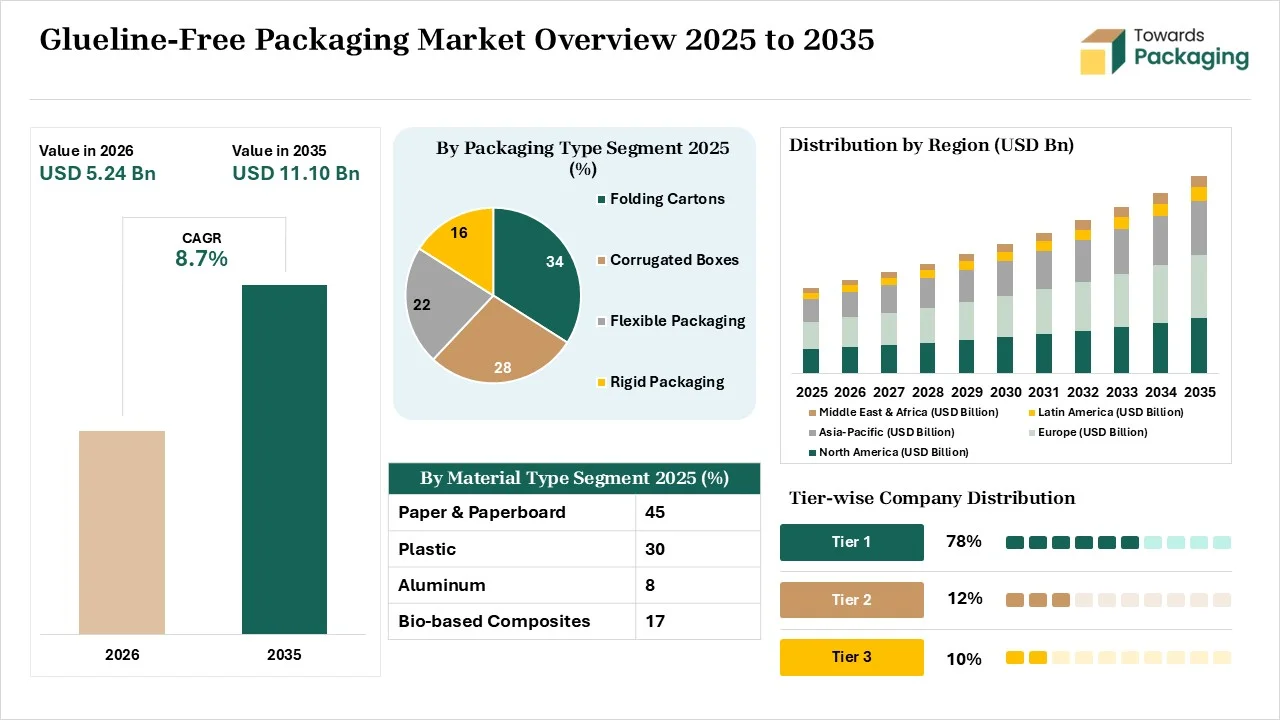

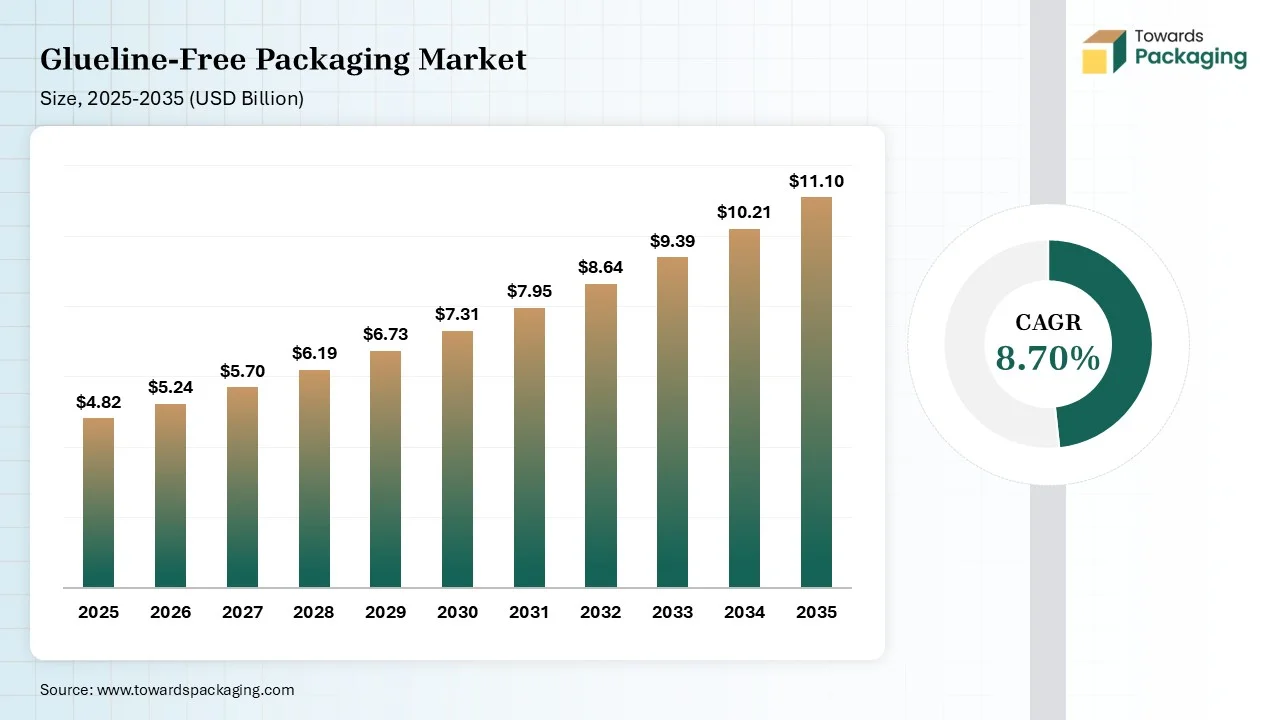

The glueline-free packaging market is projected to grow from USD 5.24 billion in 2026 to USD 11.10 billion by 2035, registering a CAGR of 8.70% during the forecast period. The study provides comprehensive coverage of market size, revenue forecasts, growth trends, segment analysis by material type, packaging format, technology, and end-use industry. It also includes detailed regional assessments, company profiles, competitive benchmarking, market share analysis, value chain evaluation, trade flow analysis, and extensive insights into leading manufacturers, converters, suppliers, and emerging industry participants shaping the global market.

Glueline-free packaging is a packaging solution that does not contain traditional adhesive. It relies on double-wall methods, interlocking tabs, corrugated paperboard, cellulose resins, tear tapes, interlocking slots, recycled folding cartons, water-activated tapes, plant resins, and one-fold locking structures. Glueline-free packaging is used in applications like bakery, e-commerce, pizza boxes, die-cut mailer boxes, confectionery trays, and shipping cartons. It offers benefits like reduced waste, tamper evidence, enhanced recyclability, simplified operations, and reduced cost.

The glueline-free packaging market growth is driven by the e-commerce expansion, popularity of no plastic design frameworks, ban on harmful chemical adhesives, growing home deliveries, growing eco-friendly markets, interest in corrugated cardboards, rise in purchasing eco-friendly products, innovations in packaging engineering, thriving cosmetic sector, and focus on retail efficiency.

The glueline-free packaging market is going through technological developments fueled by demand for sustainability, automation, and the development of fully recyclable packaging. Technological developments like 3D folding mechanics, robotic folding automation, digital watermarks, and intelligent sortation integration help in improving recovery rates and material utilization. AI is the biggest technological development in the market, which helps in accelerating structural design.

AI calculates lock-tab dimensions and easily analyzes cardboard properties. AI predicts packaging part failures and verifies interlocking structural configurations. AI offers precise fold geometries and helps in locking glueless boxes. AI easily creates 3D folding structures and rejects misaligned folds. AI accelerates the launch of a new packaging product. Overall, AI helps in structural simulation and automated supply of glueline-free packaging.

Raw materials like molded pulp, virgin kraft paper, recycled paperboard, and corrugated board are required for glueline-free packaging.

The material processing focuses on mechanical interlocking, thermal bonding, water-activated coatings, and lock-style design. Conversion includes steps like structural design, specialized material selection, precision die-cutting, stripping, and final assembly.

Package design focuses on structural engineering, dieline precision, and sustainability benefits. Prototyping involves steps like dieline engineering, hack prototypes, digital modelling, and testing.

The folding cartons segment dominated the market with 34% share in 2025 due to the growing use in FMCG branding. The focus on a flat printable surface and the need to improve space efficiency increase the use of folding cartons. The huge demand for renewable paperboard formats and the focus on lowering warehousing costs increase the adoption of folding cartons. The demand for eye-catching packaging in the retail sector drives the segment growth.

The corrugated boxes segment held the 28% market share in 2025 due to the move away from chemical solvents. The focus on lowering packing time and the need to maximize warehouse space increases the use of corrugated boxes. The focus on preventing damaged returns and achieving zero chemical residue increases the adoption of corrugated boxes. The interest in glue-free shipping corrugated boxes supports the segment growth.

The flexible packaging segment held the 22% market share in 2025 due to its lower environmental impact. The expansion of food-contact applications and the optimization of freight loads increase the use of flexible packaging. The shift away from heavy materials and the focus on utilizing fewer feedstocks enhance the development of flexible packaging. The burgeoning recyclable pouch format boosts the segment growth.

The paper & paperboard segment dominated the market with 45% share in 2025 due to the growing use in glueline-free display boxes. The rise in high-quality printing and the ESG targets in brands increases the use of glueline-free packaging. The focus on vibrant graphic printing and businesses' focus on cutting carbon emissions increases the use of paper & paperboard. The interest in glueline-free folding cartons drives the segment growth.

The plastic segment held the 30% market share in 2025 due to the growing use in durable packaging. The focus on less energy usage and unparalleled oxygen resistance increases the adoption of plastics. The interest in PVC-free plastics and the burgeoning specialty plastic development helps with expansion. The increased development of custom plastic shapes and the interest in glueline-free plastics boost the segment growth.

The bio-based composites segment held the 17% market share in 2025 due to the elimination of toxic chemicals. The high compliance fees on plastic packaging and the presence of paper recycling waste streams increase the adoption of bio-based composites. The consumer preference for fully compostable materials and the transitioning away from petroleum-based laminates increases the use of bio-based composites, supporting the segment growth.

The heat seal technology segment dominated the market with 36% share in 2025 due to its excellent efficiency in high-speed production. The surging eco-friendly paperization and the active ingredient preservation in industries like pharmaceuticals increase the use of heat seal technology. The advancing modern heating equipment helps with expansion. The massive utilization across food packaging drives the segment growth.

The mechanical locking (glueless folding) segment held the 34% market share in 2025 due to its supply chain stability. The safety regulations in the workplace and the volatility in material prices increase the use of mechanical locking. The focus on preventing packaging theft and securing content in online delivery increases the use of mechanical locking. The tool-free assembly, excellent security, cost stability, and circularity of mechanical locking support the segment growth.

The pressure-sensitive adhesive-free tapes segment held the 18% market share in 2025 due to its easy integration with cardboard. The expansion of the logistics sector and the focus on enhancing air quality increase the adoption of PSA-free tapes. The rise in heavy-duty transit and the focus on accelerating packing times increase the use of PSA-free tapes. The VOC-free manufacturing, excellent recyclability, and operational efficiency of PSA-free tapes boost the segment growth.

The food & beverage segment dominated the market with 32% share in 2025 due to the growth of food delivery apps. The stringent FSSAI regulations and the rising bans on non-compostable beverage containers increase the adoption of glueline-free packaging. The focus on avoiding chemical contamination in packaged food and the growing frozen food industry increases the adoption of glueline-free packaging. The strong F&B companies drive the segment growth.

The e-commerce & retail segment held the 26% market share in 2025 due to the consumer demand for frustration-free opening. The focus on tracking product dimensions and the growing parcel shipping rates increases the adoption of glueline-free packaging. The expansion of the digital marketplace and the need to avoid hefty fines increase the use of glueline-free packaging. The consumer transition to online shopping supports the segment growth.

The pharmaceuticals segment held the 18% market share in 2025 due to the growing healthcare spending. The development of sensitive pharmaceuticals and the focus on reducing medicine exposure increase the adoption of glueline-free packaging. The child-resistant packaging demand and the focus on lowering maintenance costs in pharmaceutical manufacturing increase the use of glueline-free packaging, boosting the segment growth.

Europe dominated the glueline-free packaging market with 32% share in 2025 due to the growing penalties on hard-to-recycle materials. The rising demand for contamination-free recycling and the established FMCG companies increase the adoption of glueline-free packaging. The strong innovation hubs and the advancements in interlocking technologies help with expansion. The shift away from toxic chemical adhesives and the robust paper sector drives the market growth.

North America held a 28% market share in 2025 due to the strong focus on eliminating the use of packaging adhesive. The expansion of shipping boxes and the rising mono-material paper solutions increases the adoption of glueline-free packaging. The focus on e-commerce optimization and the safety priority in the pharmaceutical sector increases the adoption of glueline-free packaging. The interest in mechanical locks supports the market growth.

Asia Pacific held a 27% share in the market in 2025 and is expected to grow at the fastest CAGR of 10.2% during the forecast period due to the stricter rules to eliminate non-biodegradable waste. The expansion of local deliveries and the transition towards non-toxic packaging increase the use of glueline-free packaging. The presence of key conglomerate giants and stricter green regulations helps with expansion. The high investment in high-speed manufacturing boosts the overall market growth.

Latin America held a 7% market share in 2025 due to the growing adoption of glue-free disposables in the food service industry. The abundance of forest-based raw materials and the powerhouse of agriculture export increases the production of glueline-free packaging. The burgeoning wellness trends and the regulations against harmful chemicals increase the use of glueline-free packaging, supporting the market growth.

The Middle East & Africa held a 6% market share in 2025 due to the higher demand for self-lock corrugated packaging. The focus on minimizing total packaging weight and the high expense of industrial glues increases the use of glueline-free packaging. The thriving pharmaceutical cold-chain and the focus on eliminating adhesive residue increase the adoption of glueline-free packaging. The tech-savvy demographics and the availability of mechanical locks in glueline-free packaging boost the overall market growth.

| Rank | Company | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products and Services |

| 1. | Tetra Pak | Pully/Lausanne, Switzerland | Switzerland | The company focuses on developing paper-based carton barriers and invested €60 million in its Lund facility for the production of paper-based barrier materials. | Tetra Brik, Tetra Recart, Tetra Evero Aseptic |

| 2. | Berry Global | Evansville, Indiana | United States | The company manufactures hybrid packaging solutions and focuses on eliminating adhesive from packaging. | HiBloc MCLR Films, Entour Family of Films |

| 3. | Amcor plc | Zurich, Switzerland | Switzerland | The company manufactures adhesive-free solutions and glue-free molded fibre labeling. | AmPrima Recycle-Ready Solutions, AmSky Blister System ,AmFiber Performance Paper ,AmLite HeatFlex Recycle-Ready |

| 4. | Mondi Group | Weybridge, England | England | The company manufactures glue-free products like TwinBox & Lunch Box and focuses on developing PE-free wrappers. | Glue-Free Corrugated Solutions ,dotlock ,TwinBox |

| 5. | Smurfit Westrock | Dublin, Ireland | Ireland | The company uses water-activated adhesive technology for the development of glueline-free packaging. | ActiBlu |

By Packaging Type

By Material

By Technology

By End-Use Industry

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarGlueline-Free Packaging Market