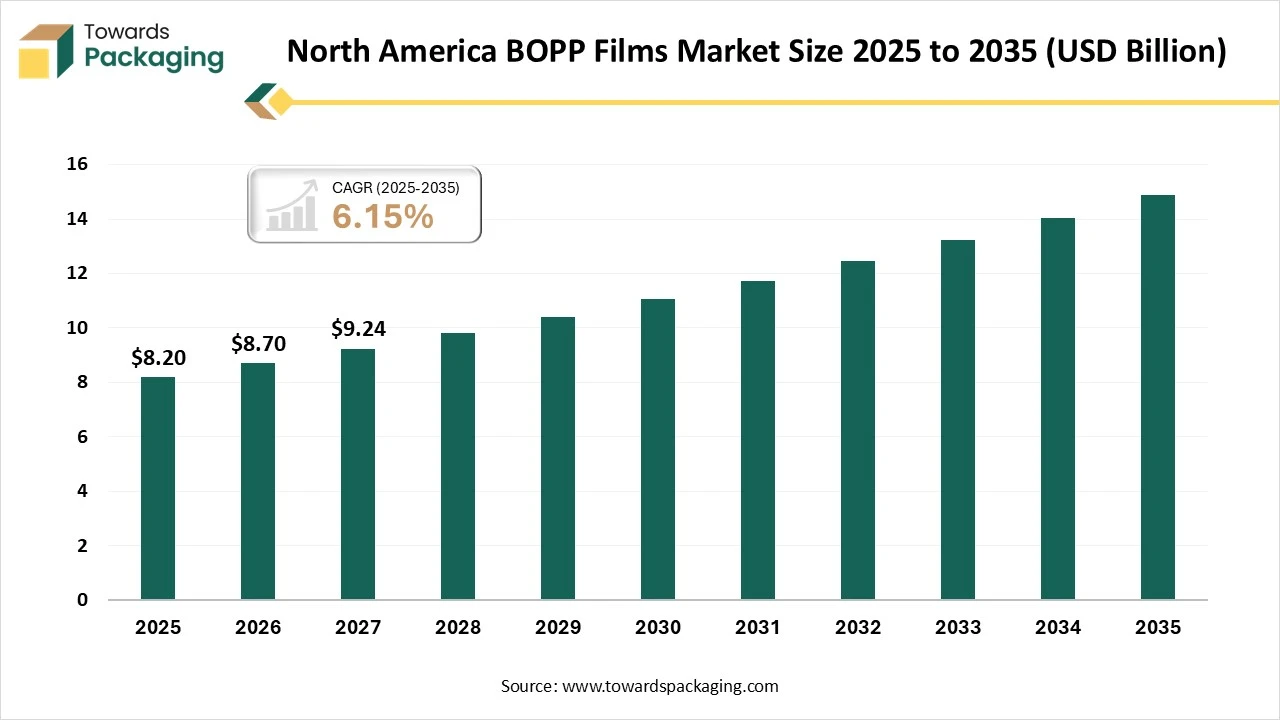

The North America BOPP films market was valued at USD 8.20 billion in 2025 and is projected to grow from USD 8.70 billion in 2026 to USD 14.89 billion by 2035, expanding at a CAGR of 6.15% during the forecast period. This report provides a complete analysis of market size, segment data by film type, thickness, production process, application, and end-user vertical. It also includes detailed company profiles, competitive landscape, value chain analysis, trade data, and insights on manufacturers and suppliers across the region.

North America BOPP films excellent-clarity, durable, and moisture-barrier plastic packaging films formed by widening polypropylene in both transverse and machine directions. Primarily used for flexible packaging, laminating, and labelling these packaging films are important in the food and beverage sectors, personal care, with bags & pouches top demand.

Technological transformation in the North America BOPP films market plays a significant role by producing enhanced barrier functional coatings. Major shift in the direction of mono-resource packaging patterns that allow for enhanced incorporation into present recycling streams. Enhanced acceptance of metallic surfaces in food & beverage that is offering both extended shelf life and high-end aesthetics. Incorporation of machine learning and artificial intelligence to handle production process, reduce thickness variations, and decrease waste.

Food and Beverages Packaging: It is widely utilized for bakery products, snacks, confectionery, dried foods, biscuits, and fresh produce because of its aroma and moisture barrier potential.

The major raw materials utilized in this market are polypropylene (PP) resins, isotactic polypropylene resin (pellets), slip agents, ethylene-propylene, and ethylene-butane-propylene copolymers. These are highly recyclable that can be easily processed back into polymer pellets and decreasing ecological footprint.

Key Players: Vacmet India Limited, Cosmo Films

The component manufacturing in this market comprises extruder, cooling system, transverse direction orientation, and machine direction orientation. It offers enhanced clarity, huge moisture barrier, sealability, and toughness performance.

Key Players: Innovia Films, Dunmore Corporation

This segment ensures huge expansion of these films by meeting the rising demand of the consumers. It ensures easy availability of the films which raise its adoption in a wide range of industries.

Key Players: Cosmo First Limited, Polyplex Corporation Limited

The transparent segment dominated the market with highest share in 2025 due to increasing consumer preference for visibility through packaging. Brand owners utilize transparent films to display freshness and quality of the products, and it directly influences consumer purchasing choices and improves shelf appeal. Inventions in descriptive agents have permitted producers to get glass-like transparency. High recyclability of these films helps in achieving regulatory standards of the brands.

The coated and speciality segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to rising sustainability and recyclability trend. It offers excellent moisture and oxygen barrier nature is important for expanding the shelf life of snack and food products. It is compelling the acceptance of high-presentation coated films that fulfil the strict ecological guidelines. These films provide excellent printability and matte textures for improved visual attractive and functionality.

The 15-30 microns segment dominated the market with highest share in 2025 due to its high tensile strength. These are considered as cost-effective and highly protective coating which support in maintain the quality of the products. It allows resource reduction which is important for fulfilling the sustainability goals while keeping manufacturing costs low. These packaging films are also the suitable for enhanced-speed automated packaging while strengthening their dominance during production.

The above 45 microns segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to enhanced durability in specialized usages. Enhanced puncture resistance, durability, and stiffness have pushed the demand for this segment. The amplified thickness confirms that packages comprising heavy products to not tear while shipping. These films with above 45 microns thickness are frequently used in premium product lamination and textile overwraps.

The tenter process segment dominated the market with highest share in 2025 due to its ability to create enhanced quality films. It produces packaging films with superior dimensional firmness, unchanging thickness, and high visual transparency. It offers suggestively advanced output than the substitute tubular procedure that is making them highly suitable option. It can effortlessly include several coatings and additives at the time of production.

The tubular (double bubble) process segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to its unique capabilities. It is precisely suited for manufacturing dedicated films and upholding balanced properties. This process includes concurrent stretch of a warmed bubble that is ensuing in films that have similar alignment in both transverse and machine directions. It is frequently used for the production of advanced-quality bags, shrink films, and progressive barrier films.

The bags and pouches segment dominated the market with highest share in 2025 due to its sustainability, lightweight, and durability. It has the capability to improve shelf life, offer excellent moisture shield, and its capability to reseal. It offers superior printability that help in branding, enhanced barrier properties, and excellent strength as well as durability while compared with other formats. The growth in e-commerce sector necessitated strong and flexible packaging option for logistics.

The tapes and labels segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to rapid expansion of e-commerce sector and superior label functionality. The huge growth in e-commerce sector influenced high demand for durable and clear BOPP tape. These films provide essential characteristics such as moisture resistance, high tensile strength, and transparency which is confirming product safety at the time of shipping.

The food segment dominated the market with highest share in 2025 due to its enhanced barrier properties. These are highly chosen for food due to their essential moisture barrier and high-transparent sealability. It supports in extending product freshness through fresh-produce, bakery, and snack channels. It is designed precisely to improve the freshness and shelf life of packaged food products.

The pharmaceuticals segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to increasing demand for advanced protection as well as performance. Presence of strict packaging guidelines has pushed the market to grow significantly. Huge demand for advanced packaging for the safety of the sensitive drugs has fuelled the demand for this segment. Rapid technological advancement has appealed a huge number of consumers.

The U.S. held the largest share in the North America BOPP films market share in 2025, due to rising e-commerce sector. It needs enhanced-performance packaging to maintain the extension shelf life and freshness of food. It is boosting for recyclable packaging that is influencing the acceptance of sustainable BOPP options. Producers are investing in progressive technologies which has attracted huge consumers towards this market.

Mexico North America BOPP Films Market Trends

Rapid production capacity has raised the demand for North America BOPP films market in Mexico. It has highly expanded food and beverages sector and e-commerce industry that fuels the demand for this segment. High raw material presence has pushed the industries to meet the demand of the consumers with advancement in the production process. Huge investment for the advancement of such films has enhanced the adoption of this industry.

By Film Type

By Thickness

By Production Process

By Application

By End-User Vertical

By Country

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarNorth America BOPP Films Market