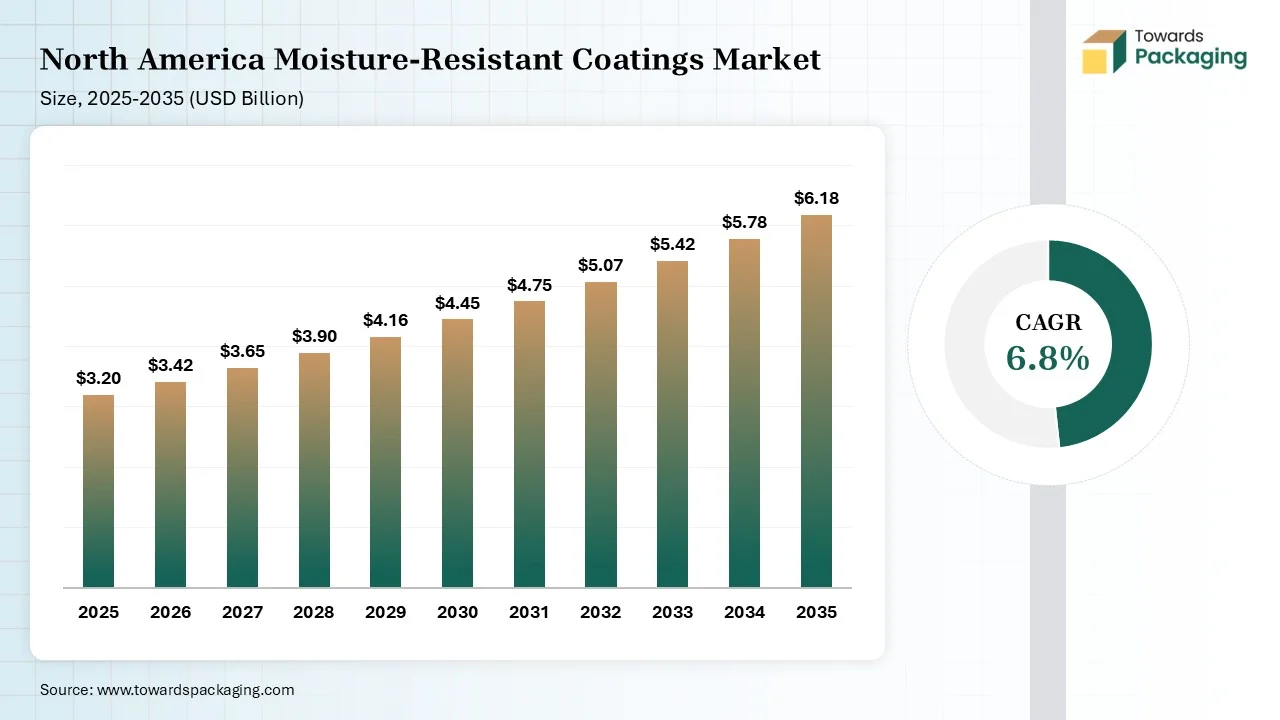

The North America moisture-resistant coatings market is projected to grow from USD 3.42 billion in 2026 to USD 6.18 billion by 2035, registering a CAGR of 6.8% during the forecast period. The market study covers detailed market size analysis, revenue forecasts, segment-wise insights by resin type, coating technology, application, and end-use industry. It also provides regional data across the U.S., Canada, and Mexico, along with competitive analysis, company profiling, value chain assessment, trade flow statistics, and extensive manufacturers and suppliers data. The report further evaluates growth opportunities driven by smart city initiatives, green building standards, and rising demand for durable moisture-protection solutions.

Market Size (2025): USD 3.20 Billion

CAGR (2025–2035): 6.8%

Market Volume (2025): 1.10 Million Tons

Volume CAGR (2025–2035): 5.9%

Moisture-resistant coatings are coatings designed to repel humidity and water in structures. The various types of moisture-resistant coatings are polyurethane coatings, moisture-resistant paints, acrylic coatings, bituminous coatings, and elastomeric coatings. They provide benefits like mildew control, easy maintenance, preventing structural damage, corrosion resistance, and stopping peeling. They possess characteristics like strong adhesion, microbial resistance, vapor permeability, and hydrophobicity. Applications of moisture-resistant coatings are roofing, exterior walls, electronics, and bathrooms.

The North America moisture-resistant coatings market is undergoing technological developments driven by demand for smart functionalities and high performance. Technological developments like nanocomposite formulations, self-healing coatings, and advanced polymer integration help in redefining moisture resistance and offer passive protection. Advancements like hygiene coatings and digital monitoring help in maintaining hygiene and performance monitoring, respectively.

AI integration is a major technological development in the market. AI helps in the rapid discovery of material and the creation of customized formulations according to applications. AI predicts the failure of coatings and easily manages coating applications. AI predicts the shortages of material and designs new formulations quickly. Overall, AI offers optimized production and real-time control of coating quality.

The raw materials like binders, pigments, polymeric-film formers, water-repelling additives, solvents, resins, and extenders are required for developing moisture-resistant coatings.

Material processing involves cleaning, etching, and rinsing. Conversion includes chemical conversion, electrochemical conversion, and hot-dip galvanizing.

Recycling includes methods like mechanical recovery, upcycling waste, repulping, and chemical depolymerization. Waste management focuses on source reduction, wastewater management, powder recovery, safe disposal, waste plastics repurposing, and energy recovery.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Market | Key Packaging Products/Services |

| 1 | Michelman | Cincinnati, Ohio | USA | One of the leading suppliers of moisture-barrier and paper packaging coatings | Water-based moisture-resistant coatings |

| 2 | Actega | Wesel, North Rhine-Westphalia | Germany | Major supplier of barrier coatings for fiber-based packaging | Moisture and functional barrier coatings |

| 3 | Solenis | Wilmington, Delaware | USA | Strong portfolio of packaging barrier and performance coatings | Water-based barrier technologies |

| 4 | Kemira | Helsinki | Finland | Significant packaging chemistry and barrier coating capabilities | Fiber packaging moisture barriers |

| 5 | Dow | Midland, Michigan | USA | Major supplier of moisture-resistant coating materials and polymers | Barrier polymers and coating technologies |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Market | Key Packaging Products/Services |

| 1 | BASF | Ludwigshafen, Rhineland-Palatinate | Germany | Large supplier of coating resins and additives | Moisture-resistant coating raw materials |

| 2 | Arkema | Colombes | France | Advanced specialty polymers for barrier coatings | Sustainable coating materials |

| 3 | Henkel | Düsseldorf, North Rhine-Westphalia | Germany | Functional coating technologies for packaging applications | Protective and barrier coatings |

| 4 | Sun Chemical | Parsippany, New Jersey | USA | Packaging coatings and functional surface technologies | Barrier coatings and specialty coatings |

| 5 | Siegwerk | Siegburg, North Rhine-Westphalia | Germany | Sustainable coating solutions for packaging substrates | Water-based barrier coatings |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Market | Key Packaging Products/Services |

| 1 | Paramelt | Heerhugowaard | Netherlands | Moisture-resistant coating technologies and wax alternatives | Protective barrier coatings |

| 2 | Mactac | Stow, Ohio | USA | Specialty coated packaging materials | Moisture-resistant coated substrates |

| 3 | Cortec Corporation | Saint Paul, Minnesota | USA | Moisture and corrosion protection coatings | Protective packaging coatings |

| 4 | Chemcoaters | Cheshire | United Kingdom | Specialty barrier coating formulations | Moisture-resistant coatings |

| 5 | Coim Group | Offanengo, Lombardy | Italy | Polyurethane and barrier coating chemistries | Packaging coating systems |

The polymer-based coatings segment dominated the market with 38% share in 2025, due to its superior barrier properties. The creation of waterproof barriers in construction projects and the protection of vehicles increases demand for polymer-based coatings. The focus on enhancing the service life of materials and the need to lower replacement costs increases the adoption of polymer-based coatings. The customizable formulations and high elasticity drive the segment growth.

The water-based coatings segment held the 22% market share in 2025 because of stricter environmental regulations. The worker safety focus and the need to lower fire hazard increase demand for water-based coatings. The shift away from traditional plastic layers and the rise in architectural waterproofing increase demand for water-based coatings. The lower odor, ease of application, and improved safety of water-based coatings support the segment growth.

The solvent-based coatings segment held the 16% market share in 2025. The growing need for heavy-duty protection and lowering downtime increases demand for solvent-based coatings. The explosion of infrastructure projects and the growing temperature fluctuations in industrial applications increase demand for solvent-based coatings. The high adhesion, industrial reliability, faster curing times, and excellent moisture tolerance of solvent-based coatings boost the segment growth.

The paper & paperboard segment dominated the market with 42% share in 2025, due to the growing restrictions on the plastics usage. The increasing demand for FMCG and the focus on beverage preservation expands the demand for paper & paperboard. The excellent printability, cost-effectiveness, and sustainability accelerate the segment growth.

The plastic segment held the 25% market share in 2025 because of automotive expansion. The growing electronic device complexity and the need for moisture vapor barriers in industries like packaging increase demand for plastic. The focus on resisting water seepage in construction and the rise in electric mobility increases the use of plastics. The need to prevent metal corrosion and the growth of eco-friendly chemistries increases the adoption of plastics, supporting the segment growth.

The metal segment held the 12% market share in 2025. The surge in automotive manufacturing and the focus on corrosion resistance increase demand for metal. The expanding EV production and the rise in infrastructure rehabilitation increase the adoption of metal. The robustly growing direct-to-metal coatings and the strong focus on low-VOC formulations boost the market growth.

The packaging segment dominated the market with 46% share in 2025, due to the explosion of the RTE food sector. The strong focus on protecting the product during shipping and the need to maintain medical integrity increase demand for packaging with moisture-resistant coatings. The growing use of recyclable paper and the rise in sustainable paper packaging increase demand for moisture-resistant coatings. The development of diverse flexible packaging formats drives the segment growth.

The construction segment held the 18% market share in 2025 because of the development of public transit. The continous flooding events and the focus on preventing structural degradation increase demand for moisture-resistant coatings. The need for long-term asset protection and focus on protecting buildings from heavy rainfall increases the adoption of moisture-resistant coatings. The repairing of housing stock supports the overall segment growth.

The automotive segment held the 14% market share in 2025 due to the need for enhancing automotive paint longevity. The huge EV battery production and protection of under-the-hood parts increase demand for moisture-resistant coatings. The growing vehicle manufacturing and focus on protecting EV components like PCBs & others increases the use of moisture-resistant coatings. The development of innovative exterior finishes requires moisture-resistant coatings, driving the segment growth.

The acrylic-based segment dominated the market with 34% share in 2025, due to its ease of use. The focus on fewer emissions of VOC and the need to prevent moisture buildup in exterior walls increases the use of acrylic-based technology. The need for barrier coating in cardboard and the creation of an interior moisture barrier increase demand for acrylic-based technology. The superior weathering and application ease of acrylic-based technology drive the segment growth.

The polyurethane-based segment held the 28% market share in 2025 due to the transition towards sustainability. The development of long-lasting waterproofing and the creation of aesthetic finishes in aerospace increases demand for polyurethane-based technology. The infrastructure maintenance needs and the development of industrial floors increase the use of polyurethane-based technology. The excellent mechanical properties and superior protection of polyurethane-based technologies support segment growth.

The epoxy-based segment held the 16% market share in 2025. The growing construction initiatives and the burgeoning commercial industry increase demand for epoxy-based technology. The exceptional adhesion of epoxy-based coatings across various surfaces helps with expansion. The excellent water impermeability and unmatched barrier properties of epoxy-based technologies boost the overall segment growth.

The United States dominated the market due to the rise in civil engineering projects. The stricter VOC emission regulations and the strong presence of automotive OEMs increase demand for moisture-resistant coatings. The growing investment in nanotechnology and the ongoing robust infrastructure projects increase the adoption of moisture-resistant coatings. The huge industrial bases and the presence of industry-leading companies drive the market growth.

Canada is experiencing the fastest growth in the market due to its long winters. The development of public infrastructure projects and green building strategies increases demand for moisture-resistant coatings. The data center expansion and the stricter energy efficiency rules increase demand for moisture-resistant coatings. The growing commercial renovations and the growing oil production increase demand for moisture-resistant coatings, supporting the overall market growth.

By Coating Type

By Substrate

By End-Use Industry

By Technology

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarNorth America Moisture-Resistant Coatings Market