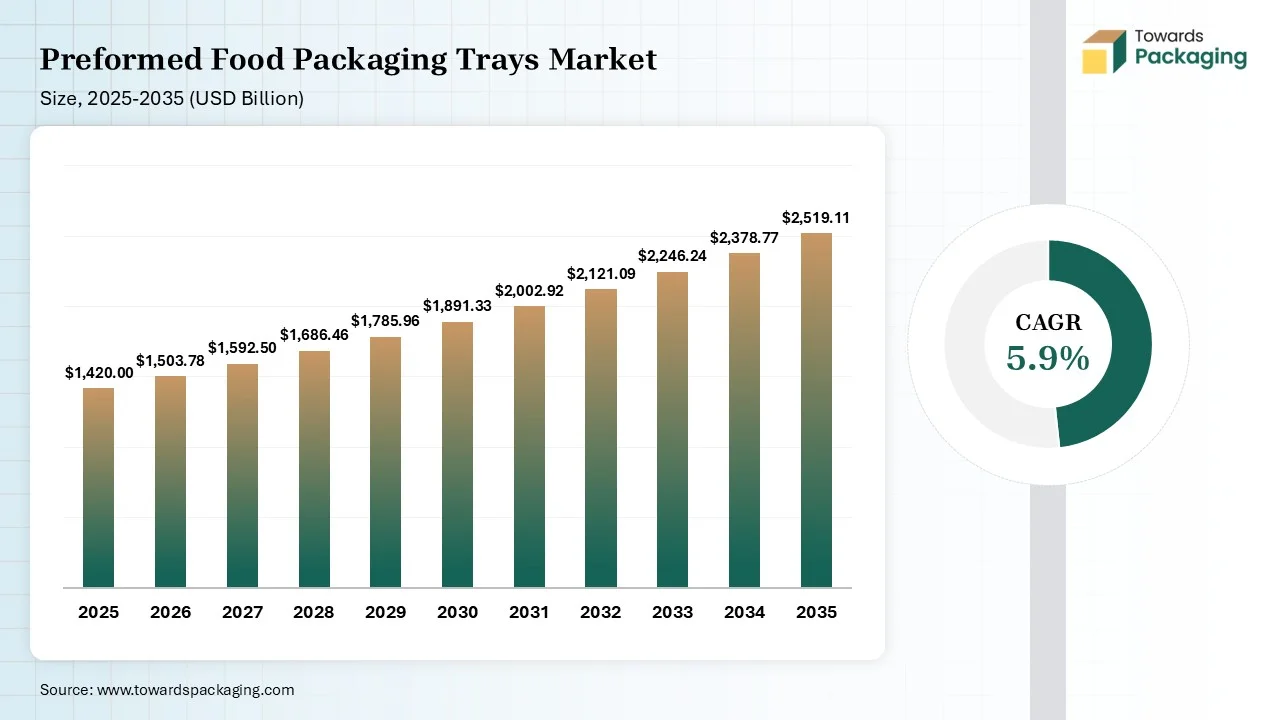

The preformed food packaging trays market is projected to grow from USD 1503.78 million in 2026 to USD 173.76 million by 2035, registering a CAGR of 6.8% during the forecast period. The report provides a complete view of the market, covering detailed segment-level data by material type, product type, and end-use applications. It also includes regional insights across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Additionally, the study analyzes key companies, competitive landscape, value chain structure, trade data, and comprehensive information on manufacturers and suppliers, helping stakeholders understand market dynamics and future opportunities.

Preformed food packaging trays are pre-shaped rigid containers used for protecting, packaging, and displaying food products. These trays are manufactured from various types of materials, including polypropylene (PP) or CPET, through a thermoforming process. It is used in modified atmosphere packaging or vacuum skin packaging for extending shelf life, delivering a leak-proof barrier, and offering consumer convenience, to carry a wide range of food items. Also, it is designed to handle freezing temperatures and transportation stress.

AI has played a transformative role in shaping the preformed food packaging trays industry. Firstly, AI scanners help in detecting micro-level defects such as dents, cracks, deformed trays, and correcting tray dimensions. Secondly, AI tools enhance the capabilities to design and develop lightweight, eco-friendly trays for maintaining structural integrity. Thirdly, AI enables the analysis of market trends, sales history, and seasonal patterns to predict demand for specific types of preformed trays, and helps in reducing overproduction.

The raw materials used in the production of preformed food packaging trays comprise PET, CPET, pulp, plastics, and PLA.

Recycling of preformed food packaging trays involves a specialized process of sorting, collection, cleaning, and reprocessing to reform old trays into new ones. At sorting plants, near-infrared (NIR) technology is important to distinguish between mono-layer and multi-layer PET trays.

The distribution channel for preformed food packaging trays primarily involves direct sales from manufacturers to food processors, and indirect channels through packaging suppliers, distributors, and retailers.

The plastic segment dominated the market with 58% share in 2025. This is due to the increasing adoption of plastic-based packaging trays from the food industry for transporting bulk amount of seafood, meat, and bakery items across the world. The plastic packaging trays also offer enhanced protection, superior durability, and cost-effectiveness in the end-user industries.

The paper & paperboard segment held the second largest share of 22% in 2025 and expects the fastest CAGR of 8.5% during the forecast period, owing to the surging use of paperboard trays from the ready-to-eat products industry. These trays provide several benefits, including enhanced durability, superior shock absorption capability, and vibration prevention.

The aluminum segment held the third largest share of 12% in 2025, because aluminum-based trays are widely used in the food manufacturing sector for storing food items. These trays offer numerous advantages, such as superior thermal properties, recyclability, enhanced protection, and cost-effectiveness.

The rigid trays segment dominated the market with 64% share in 2025, owing to the growing use of these trays for transporting meat and dairy items. Also, these trays provide several benefits, such as enhanced durability, structural integrity, and extended shelf life for food products.

The semi-rigid trays segment held the second largest share of 23% in 2025. This is due to the surging application of these trays in the food industry for storing and transporting snacks and bakery items. These trays are supported by microwaves and freezers, making them suitable for the processed food industry.

The flexible trays segment held the third largest share of 13% in 2025 and expects the fastest CAGR of 8.9% during the forecast period, owing to the increasing demand for lightweight trays from the catering service providers globally. These trays are manufactured using PET, PP, and CPET, which makes them cost-effective as compared to other types of trays.

The standard packing segment dominated the market with 41% share in 2025, owing to the rapid adoption of this packaging technology by the food industry to ensure safety, enhance quality, and provide integrity during the storage, transport, and handling of food items.

The modified atmosphere packaging (MAP) segment held the second largest share of 27% in 2025. This is owing to the increasing use of this packaging technology by the processed food industry to extend the shelf life of perishable products by slowing down the respiration process and reducing microbial growth. This technology helps in maintaining freshness, preserving color and texture, reducing food waste, and lowering the need for food preservatives.

The vacuum skin packaging (VSP) segment held the third largest share of 18% in 2025. This is due to the increasing adoption of this packing technology by the bakery sector for transporting their products across the world. This packing technology helps in extending the shelf life of food items by removing aerobic bacteria and maintaining the texture of food products.

The active packaging segment held the fourth largest share of 14% in 2025 and expects the fastest CAGR of 9.3% during the forecast period, owing to the surging use of this packaging technology by catering service providers to deliver cooked foods to customers. Active packaging technology helps in environment protection and enhancing supply chain optimization.

The meat, poultry & seafood segment dominated the market with 36% share in 2025, owing to the growing adoption of rigid trays by the supermarkets for displaying seafood items. Also, the poultry and meat companies are collaborating with packaging brands to use high-quality preformed trays for transporting their products in different regions.

The ready-to-eat meals segment held the second largest share of 18% in 2025. This is due to the growing demand for processed food items from office goers in several nations, including the U.S. and China. Preformed trays are used for packaging ready-to-eat meals to extend their shelf life.

The bakery & confectionery segment held the third largest share of 14% in 2025. This is due to the rapid investment by the bakery companies in opening new stores globally to enhance their brand value. Semi-rigid trays are generally used in the confectionery sector for storing various items such as breads, cakes, and pastries.

The fruits & vegetables segment held the fourth largest share of 12% in 2025 and expects the fastest CAGR of 8.2% during the forecast period. This is owing to the growing use of plastic and paper trays for storing and transporting fruits and vegetables in different parts of the world. Preformed trays are widely adopted by fruit and vegetable providers to enhance shelf life and improving sustainability.

The food processing companies segment dominated the market with 46% share in 2025, owing to the increasing use of preformed hydroloq padless tray to store meat-based products. Additionally, the food processing companies are collaborating with packaging solution providers to adopt eco-friendly trays for maintaining sustainability.

The retail & supermarkets segment held the second largest share of 28% in 2025. This is owing to the growing adoption of plastic-based trays for displaying food products in supermarkets. Also, the rapid investment by the processed food companies in opening new retail outlets in different areas has contributed to the industrial development.

The foodservice industry segment held the third largest share of 16% in 2025. This is due to the surging use of molded pulp & bagasse trays from the foodservice sector for maintaining sustainability. Additionally, the growing focus of the catering service providers to expand their businesses across the world has increased the demand for preformed packaging trays.

The e-commerce food delivery segment held the fourth largest share of 10% in 2025 and expects the fastest CAGR of 9.8% during the forecast period. Preformed trays are widely used in the e-commerce food delivery sector to prevent leakages during transport, ensure food safety, and improve delivery convenience. The e-commerce companies have started partnering with tray manufacturers to use high-quality trays for delivering food items globally.

Asia Pacific dominated the preformed food packaging trays market with 34% share in 2025. This is due to the increasing demand for plastic food trays from the railway sector, along with the rise in the number of bakeries in India and Japan. The integration of advanced technologies such as AI and IoT in the packaging industry, coupled with the growing consumer awareness about sustainability. This region is home to several prominent companies, including Huhtamaki India Pvt Ltd, Uno Plast, and Vinpac Innovations, which are adopting several strategies, including product launches, business expansions, and collaborations, that contribute to the overall industrial development.

China Preformed Food Packaging Trays Market Trends

China is a leading contributor to the preformed food packing trays market in the Asia Pacific region. The rising investment by tray manufacturers in opening new production centers, along with partnerships among restaurant chains and packaging companies, has boosted the industrial development. Moreover, the growing demand for processed foods, as well as technological advancements in the plastic recycling sector, is playing a prominent role in shaping the industry in a positive direction.

Latin America is expected to rise with the fastest CAGR of 8.3% during the forecast period. This is owing to the increasing demand for frozen foods in several countries, including Argentina, Brazil, Peru, and Colombia. Also, the growing adoption of eco-friendly packaging solutions by restaurants, coupled with the opening of production centers, has contributed to the market expansion. In addition, numerous government initiatives aimed at strengthening the food and beverage sector, as well as the surging proliferation of e-commerce platforms, are expected to drive the growth of the preformed food packaging trays market in this region.

Brazil Preformed Food Packaging Trays Market Trends

Brazil is a prominent contributor to the preformed food packaging trays industry in the Latin America region. This is due to the increasing preference of the corporate offices to order food items from caterers, as well as the rise in the number of packaging startups in this country. Additionally, the growing demand for convenience foods, coupled with numerous collaborations among plastic manufacturers and retail companies, has accelerated the market growth.

By Material Type

By Product Type

By Packaging Technology

By Application

By End-user

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPreformed Food Packaging Trays Market