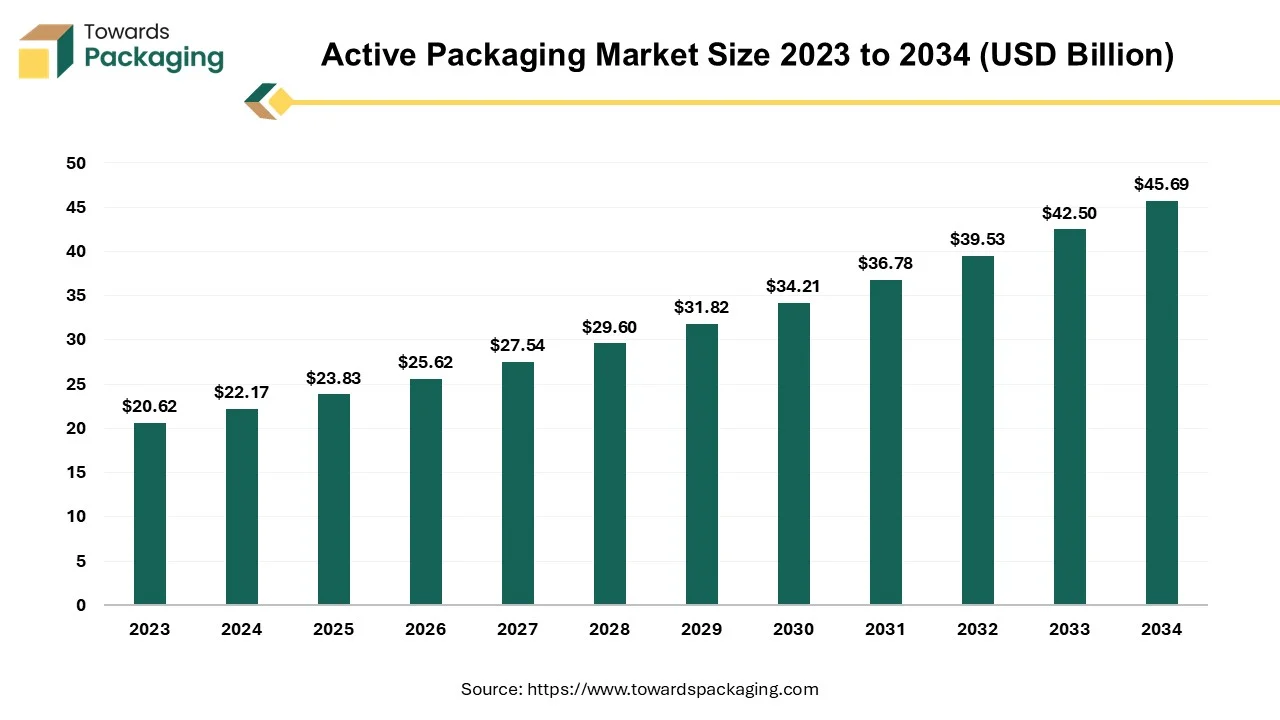

The active packaging market is forecasted to expand from USD 25.62 billion in 2026 to USD 49.12 billion by 2035, growing at a CAGR of 7.5% from 2026 to 2035. The report provides in-depth segmentation by type (oxygen scavenger, moisture absorber, shelf-life sensing, and others), application (food & beverage, healthcare, pharmaceuticals, personal care, etc.), and region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa). North America led the market in 2024, while Asia Pacific is forecasted to grow fastest through 2035.

The study covers a full value chain analysis, detailed trade statistics, and profiles of major manufacturers including Amcor, Bemis, W.R. Grace, Ampacet, and Ball Corporation, offering competitive benchmarking and supplier mapping.

The key players operating in the market are focused on adopting inorganic growth strategies like acquisition and merger to develop advance technology for manufacturing active packaging which is estimated to drive the global active packaging market over the forecast period.

The advanced type of packaging engineered to interact with the product which contains to extend shelf-life, maintain quality, and enhance safety is known as active packaging. The active packaging only serves as a passive barrier, active packaging actively responds to environmental changes and improves the condition of the packaged product. The key functions of active packaging are extending shelf life, maintaining freshness, enhancing safety, and improves product quality.

| Metric | Details |

| Market Size in 2025 | USD 23.83 Billion |

| Projected Market Size in 2035 | USD 49.12 Billion |

| CAGR (2026 - 2035) | 7.5% |

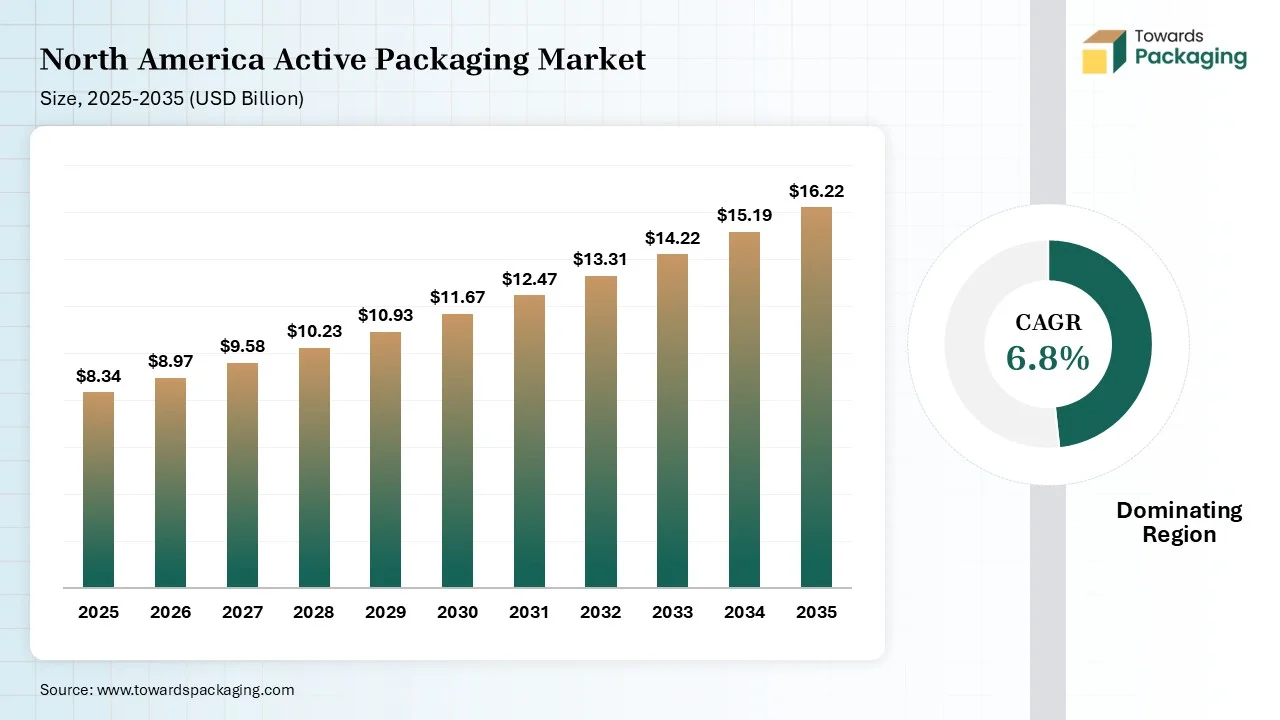

| Leading Region | North America |

| Market Segmentation | By Type, By Application and By Region |

| Top Key Players | W. R. Grace and Company, Ampacet Corporation, Ball Corporation, Graham Packaging Company Inc., Rexam plc. |

The innovation of modified atmosphere packaging (MAP) has adjusted composition of gases inside packaging to extend shelf life, accounts for over 50% of total demand in the active packaging sector. Food deteriorates in quality and spoils naturally as result of oxidation, which happens when it is exposed to air. This especially problematic for goods that contain a lot of oils and fats because they are more prone to oxidation.

Increasing environmental awareness is prompting companies to innovate eco-friendly and biodegradable active packaging materials, aligning with global sustainability goals and reducing reliance on plastics. For instance, in September 2024, according to power adhesives company, its biodegradable hot melt adhesive is a “world first” and is intended for use by contract packers, point of sale (POS) converters, cartons, and corrugated packaging.

According to certification, the adhesive is guaranteed to decompose entirely in the presence of oxygen, producing only harmless byproducts and no microplastics. According to Power Adhesives, Tecbond 2014B is made up of 44% bio-based components and is approved by AST D6400 and EN13432, two European Union standards that outline the specifications for products that are biodegradable and compostable.

The artificial integration can significantly improve the active packaging market by optimizing production, enhancing quality control, and enabling smart packaging solutions. The artificial intelligence integration driven sensors can monitor temperature, humidity gas levels, and products freshness in real-time. Machine learning algorithms analyze this data to provide insights on product safety and shelf life.

For instance, AI –powered labels that change color when food spoils or temperature-sensitive packaging that alerts consumers to improper storage. The artificial intelligence powered computer vision can inspect packaging for defects, ensuring consistent quality and reducing product recalls.

When combined with AI models, smart packaging can allow patients and caregivers greater visibility and control over the appropriate dosage and impact of medications given to patients. Pharmacies can better manage their supply chain by tracking packages from manufacturing to final consumption, and consumers can now confirm product authenticity due to connected packaging, which also helps avoid the consumption of counterfeit medications.

As the online food and pharmaceutical sales rise, packaging that maintains product quality during shipping is in higher demand. Online retail involves longer supply chains and increased handling, requiring packaging that ensures product freshness, stability, and protection from external conditions like temperature fluctuations, moisture, and oxygen exposure. The rise of grocery and meal kit delivery services demands packaging that maintains food quality, prevents spoilage, extends shelf-life, especially for perishable goods. Active packaging solutions like antimicrobial films and oxygen scavengers help to maintain freshness during transit. Hence, the expansion of the e-commerce platform has estimated to drive the growth of the active packaging market in the near future.

For instance, according to the data published by the National Ecommerce Association, in 2025, online commerce will account for 21% retail sales, the largest percentage to date. By 2027, it is anticipated that 22.6% of all retail transactions will take place online. Since 2021, the percentage of retail purchases made online has increased by an average of 0.32% per year.

The key players operating in the market are facing issue due to regulatory challenges, limited consumer awareness, and compliance issues, which has estimated to restrict the growth of the active packaging market. Strict food safety and environmental regulations vary across regions, making compliance complex and costly. Approval processes for new packaging materials can be time-consuming. Many consumers and businesses are unaware of the benefits of active packaging or hesitate to pay a premium for it. Advanced materials, smart sensors, and specialized coatings increase production costs, making active packaging more expensive than traditional options.

Integration of technologies like QR codes, RFID, and time-temperature indicators can help track product conditions and enhance supply chain transparency. Smart packaging solutions that offer real-time freshness indicators appeal to both consumers and businesses. Governments and regulatory agencies are pushing for safer, more sustainable packaging solutions, creating opportunities for eco-friendly active packaging innovations.

Countries in Asia-Pacific, Latin America, and Africa are experiencing growing urbanization and packaged food consumption, creating a lucrative market for active packaging. Hence, adoption of active packaging in emerging markets has estimated to create lucrative opportunity for the growth of the active packaging market in the near future.

The oxygen scavenger segment held a dominant presence in the active packaging market in 2025. Oxygen exposure accelerates food spoilage, oxidation, and microbial growth. Oxygen scavengers helps extend shelf life, making them essential for packaged food, beverages, and pharmaceuticals. Oxygen scavengers are utilized in packaged meat, baked goods, dairy, snacks, and ready-to-eat meals to maintain freshness and prevent discoloration.

They are also used in beer, wine, and other beverages to prevent oxidation and flavor degradation. Many drugs and biologics degrade in the presence of oxygen. Oxygen scavengers ensure the stability of oxygen-sensitive medications, increasing their shelf life. New developments such as self-activating and biodegradable oxygen scavengers, are making them more efficient and sustainable.

The food and beverage segment registered its dominance over the global market in 2025. Active packaging solutions like oxygen scavengers, moisture absorbers, and ethylene absorbers helps to reduce spoilage, keeping food fresh for longer. Anti-microbial packaging prevents bacterial and fungal growth preserving taste, texture, and nutritional value. Shields food from moisture, oxygen, UV light, and temperature fluctuations, which can degrade quality. Smart packaging solutions, such as freshness sensors and time-temperature indicators, provide real-rime information on food quality.

Numerous companies have specialized in active packaging solutions for the food and beverage industry, offering technologies that enhances product freshness, extend shelf-life, and ensure safety. Amcor Group GmbH offers innovative active and intelligent packaging technologies for various industries, including beverages and food. Bemis company has specialized in flexible packaging solutions, offering active packaging options. Clariant international company is a specialised in chemicals company that provides additives and functional materials for active packaging applications in the food industry.

Sustainability is reshaping the active packaging market as manufacturers lessen their impact on the environment. Manufacturers are using more recyclable, biodegradable, and bio-based materials. Waste reduction techniques and environmentally friendly packaging design are being promoted by regulations and circular economy projects run by agencies like the European Commission. To reduce food waste and promote global sustainability goals, businesses are also creating active packaging solutions that increase shelf life. This change enhances long-term market expansion and brand reputation in addition to aiding environmental protection.

Government regulations focused on food safety, environmental protection, and waste reduction are playing a major role in expanding the active packaging market. Extended Producer Responsibility regulations encourage businesses to use recyclable and environmentally friendly materials, and the Food Safety and Standards Authority of India establishes packaging standards to guarantee product safety. The European Commission is spearheading programs in Europe that support circular economy principles and sustainable packaging designs. Manufacturers are being encouraged by these combined efforts to create cutting-edge active packaging solutions that increase shelf life and decrease food waste.

The active packaging market is strengthening its resilience through sustainable materials, advanced preservation technologies, and stricter safety regulations. Support from the authorities, like the European Commission and the U.S. Food and Drug Administration, encourages innovation in safe and eco-friendly packaging. Increasing demand for longer shelf life and reducing food waste further support steady market growth.

Additionally, producers are broadening their sources for raw materials in order to lower supply chain risks and guarantee production continuity. Constant investment in recyclable materials and smart packaging technologies helps businesses stay flexible and competitive in ever-evolving markets.

| Key Area | Impact on ROI |

| Shelf-Life Enhancement | Active packaging technologies help extend product freshness, allowing companies to maximize sales opportunities and reduce expired inventory. |

| Waste Reduction | Lower spoilage rates decrease financial losses and improve overall operational efficiency. |

| Brand Value Growth | Improved product safety and quality strengthen consumer trust and long-term brand loyalty. |

| Regulatory Alignment | Compliance with guidelines from the U.S. Food and Drug Administration and sustainability initiatives supported by the European Commission enhances market credibility. |

| Supply Chain Optimization | Better product stability supports smoother transportation and storage, reducing unexpected disruptions. |

| Innovation Advantage | Adoption of smart and sustainable packaging solutions creates differentiation and supports premium pricing strategies. |

North America region held a significant share of the active packaging market in 2025. North America region has highest consumption of ready-to-eat meals, frozen foods, and snacks, driving the need for packaging that extends shelf life and maintains freshness. Companies in North America are developing intelligent packaging solutions with QR codes. Freshness sensors, and nanotechnology-based materials. Key Players in North America region, such as Amcor, Avery Dennison, Sealed Air, and Berry Global company, are investing in active packaging solutions.

U.S. market players play major role in active packaging industry. The more than half population of the U.S. earns more than average and due to this there is rising demand for fresh, minimally processed foods. As the U.S. market is mature and is home for various pharmaceutical industries the demand for the active packaging is high.

")

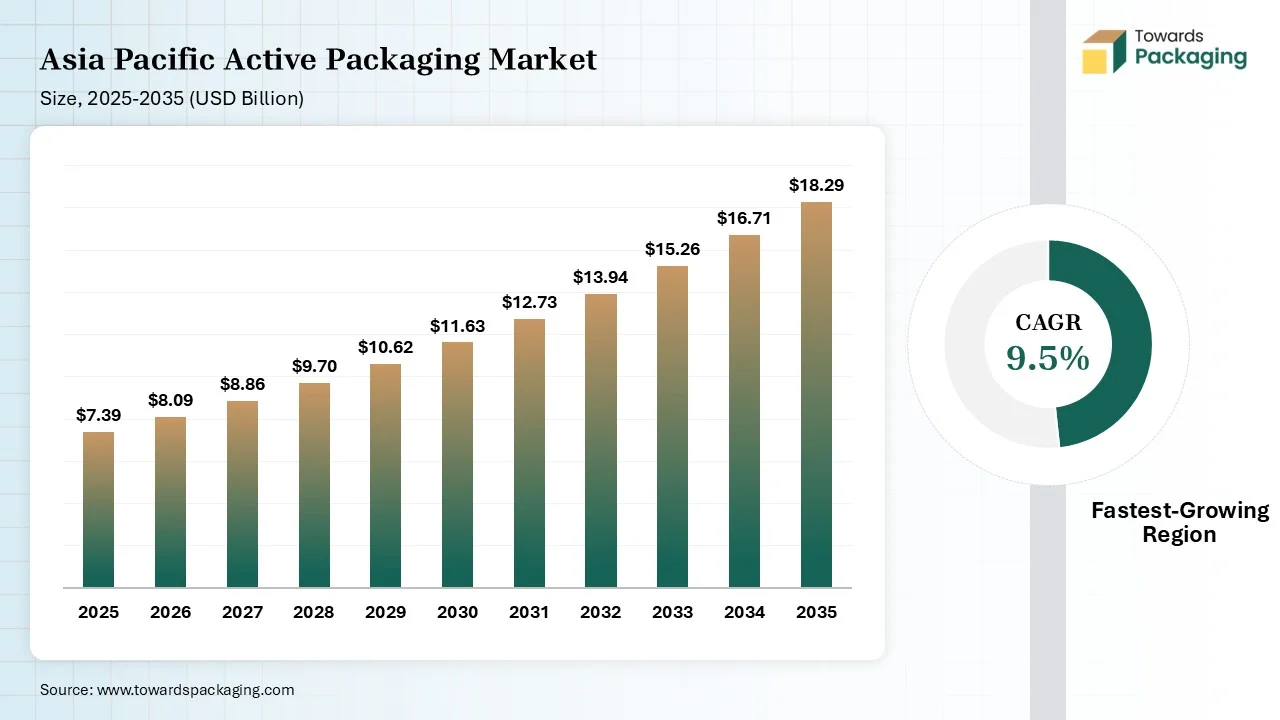

Asia Pacific region is anticipated to grow at the fastest rate in the active packaging market during the forecast period. Increasing urban populations and busy lifestyles drive demand for convenience foods, ready-to-eat meals, and packaged snacks, boosting the demand for advanced packaging solutions in Asia Pacific region. Rising income levels in countries like China, Southeast Asia and India are leading to higher consumption of premium, packaged and fresh food products, which require active packaging for quality preservation.

Asia Pacific is major hub for processed food, dairy, seafood, and meat industries, all of which require active packaging to extend shelf life and maintain freshness. India’s online food delivery platform Zomato, Swiggy, Swish has raised the demand for the active packaging in India. Asia-Pacific is a fast growing pharmaceutical market, increasing the demand for moisture-resistant, oxygen-absorbing, and temperature-sensitive packaging. Countries like China, Japan, India and South Korea have implemented strict food safety laws, pushing companies to adopt high-quality, functional packaging solutions.

China’s pharmaceutical sector is rapidly expanding, with increasing demand for moisture-resistant and oxygen-barrier packaging to protect drugs and medical supplies. The Chinese government promotes packaging innovation as part of its “Made in China 2025” strategy, boosting investment in smart and active packaging technologies. Chinese consumers are more health-conscious, demanding organic, fresh, and chemical-free foods, which require advanced active packaging solutions. Growth in premium and imported food products in China region has increased the demand for high-quality protective packaging.

The developing number of urban residents with developed disposable income has led to a bigger demand for packaged, ready-to-eat, and frozen foods, all of which benefit from the extended shelf life served by active packaging. Rising consumer awareness about food safety, hygiene, and quality is encouraging producers to accept high-level packaging technologies. Events like the COVID-19 Pandemic have further heightened consumer issues about contactless delivery and safety, too. The growing number of urban residents with growing disposable incomes has led to a bigger urge for sustainable and bio-based packaging solutions. Producers are innovating with environmentally active elements and materials to align with this demand.

Europe region is observed to grow at a considerable growth rate in the upcoming period. The European Food Safety Authority (EFSA) and EU regulations enforce strict guidelines on food quality, fostering the adoption of advanced active packaging solutions. Compliance with Regulation (EC) NO 1935/2004 ensures that packaging materials do not compromise food safety, increasing demand for oxygen scavengers, antimicrobial films, and moisture absorbers. The EU’s Circular Economy Action Plan and bans on single-use plastics push companies towards biodegradable and recyclable active packaging.

Europe leads in nanotechnology, intelligent sensors, and RFID-based active packaging for real-time food quality monitoring. Countries like Germany, the U.K. and France invest heavily in fresh indicators, smart labels, and temperature-sensitive packaging. The expansion of Amazon Fresh, Ocado, Carrefour, and local grocery delivery services increased the demand for protective, freshness-preserving packaging for online food distribution.

One of the initial machines is RFID (Radio Frequency Identification ), which allows automated data capture and management without demanding direct line-of-sight, just like regular barcodes. With RFID, every product can carry a different identifier, which enables it to be managed from manufacturing through delivery, providing real-time data that develops accuracy and efficiency.

Just like regular barcodes that need manual scanning and are restricted in the information that they can store, RFID tags carry and transfer detailed data automatically. This type of automation lowered labour costs and minimizes errors linked with manual entry. Furthermore, RFID technology assists faster, multiple-item sacking, which saves valuable time in warehouses and distribution centres.

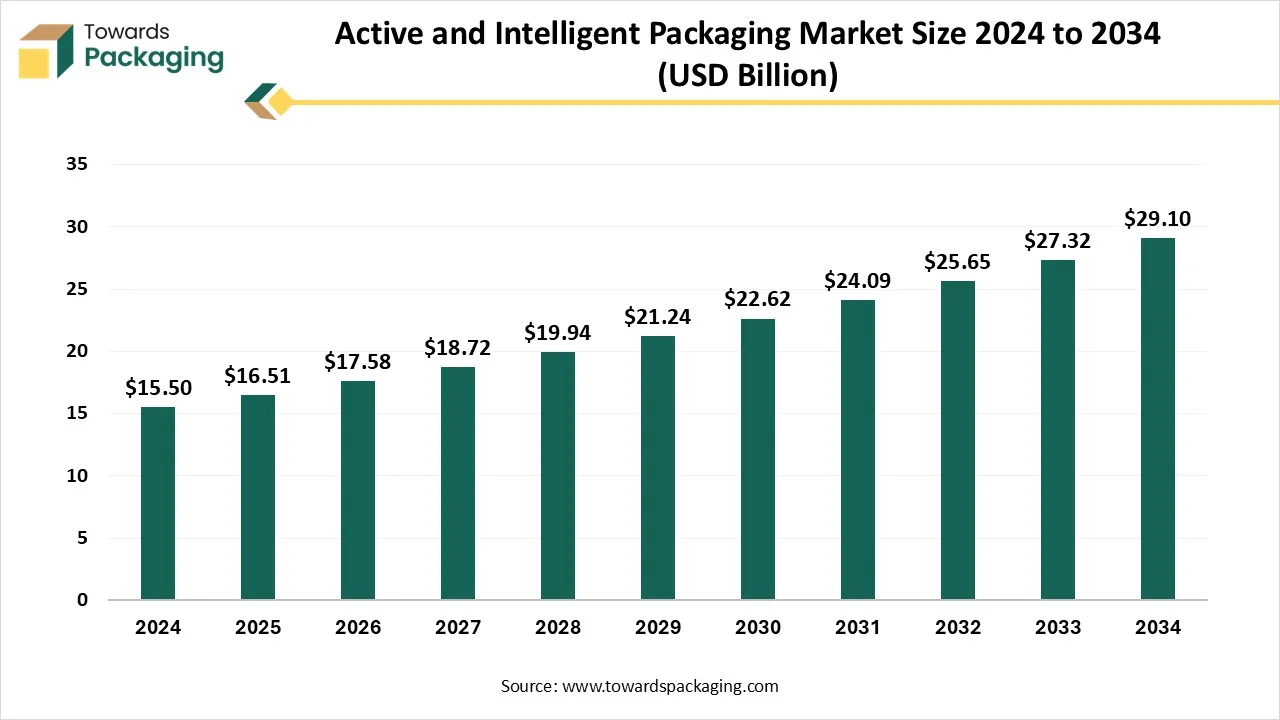

The global active and intelligent packaging market is forecasted to expand from USD 16.51 billion in 2025 to USD 29.1 billion by 2034, growing at a CAGR of 6.5% from 2026 to 2035. The market is driven by demand for supply chain transparency, food safety, extended shelf life, and consumer engagement technologies. Emerging innovations include oxygen scavengers, antimicrobial films, time-temperature indicators, and smart labels with QR/NFC. With North America emerging as the fastest-growing area and Asia Pacific holding the greatest share in 2024, the global active and intelligent packaging market is expanding quickly. The most popular technology type was active packaging, but intelligent packaging is predicted to rise significantly.

The global active & intelligent packaging market involves advanced packaging systems that go beyond traditional containment and protection by enhancing shelf life, monitoring product conditions, and improving consumer interaction. These solutions are widely applied across industries like food & beverage, healthcare, pharmaceuticals, logistics, cosmetics, and electronics. Smart packaging pertains to packaging that utilises technology to develop the user experience. It consists of the main elements: active packaging and intelligent packaging. Active packaging communicates with the product. It can incorporate oxygen or release preservatives. This assists in expanding shelf life and tracking quality. Intelligent packaging serves to convey information about the product's condition. It may contain sensors that examine freshness or temperature.

The active vacuum packaging technology market is booming, poised for a revenue surge into the hundreds of millions from 2026 to 2035, driving a revolution in sustainable transportation. The rising demand for enhancing the shelf-life of the food product and increasing concern towards hygiene and safety of the food products has driven the growth of the market.

The active vacuum packaging technology market refers to the segment within the packaging industry that involves vacuum-based systems integrated with active packaging technologies to enhance food preservation. These systems remove air from packaging to reduce oxidation and microbial growth, while also incorporating active components like oxygen scavengers, moisture regulators, antimicrobial agents, and ethylene absorbers. This packaging solution is primarily used in food, pharmaceuticals, and industrial goods to extend shelf life, maintain product quality, and meet sustainability goals.

The active packaging for healthcare market is accelerating, with forecasts predicting hundreds of millions in revenue growth between 2026 and 2035, powering sustainable infrastructure globally. The demand for active packaging in healthcare is increasing due to the rising requirement for extended shelf life of various pharmaceutical and diagnostic products.

The active packaging for healthcare market refers to the segment of packaging technologies designed not only to contain and protect healthcare products but also to interact with the product or environment to extend shelf life, enhance safety, improve product performance, and ensure regulatory compliance. These packaging systems incorporate components such as moisture absorbers, oxygen scavengers, antimicrobial agents, and temperature indicators that actively respond to external conditions. Active packaging is critical in pharmaceuticals, diagnostics, and medical devices, particularly where drug stability, sterility, and traceability are essential.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Amcor | Zurich | Switzerland | Global leader in active food packaging innovation and shelf-life extension technologies | Active flexible packaging, high-barrier packaging |

| 2 | Sealed Air | Charlotte, North Carolina | USA | Major provider of active food preservation systems | Cryovac active packaging solutions |

| 3 | AptarGroup | Crystal Lake, Illinois | USA | Industry leader in active material science and pharmaceutical packaging technologies | Moisture control and active packaging systems |

| 4 | Berry Global | Evansville, Indiana | USA | Large-scale packaging producer integrating active technologies into packaging formats | Active food and healthcare packaging |

| 5 | Mondi | Weybridge, England | United Kingdom | Significant investment in sustainable active packaging innovation | Functional flexible and paper-based packaging |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Mitsubishi Gas Chemical | Tokyo | Japan | Pioneer and global leader in oxygen scavenger technologies | Ageless oxygen absorbers |

| 2 | Multisorb Technologies | Buffalo, New York | USA | Major supplier of active packaging components | Oxygen absorbers, desiccants |

| 3 | Coveris | Vienna | Austria | Active participant in shelf-life extension packaging solutions | Active flexible packaging |

| 4 | Constantia Flexibles | Vienna | Austria | Supplier of high-barrier and active packaging structures | Functional laminates and films |

| 5 | Huhtamaki | Espoo | Finland | Developer of food packaging technologies that support freshness preservation | Foodservice and food packaging |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Microban International | Huntersville, North Carolina | USA | Specialist in antimicrobial active packaging technologies | Antimicrobial packaging solutions |

| 2 | Insignia Technologies | Dundee, Scotland | United Kingdom | Developer of freshness indicators and active packaging technologies | Freshness indicators |

| 3 | Tosaf | Kibbutz Ein Hamifratz | Israel | Supplier of active packaging additive technologies | Active masterbatches |

| 4 | Desiccare | Reno, Nevada | USA | Specialized supplier of moisture-control packaging solutions | Desiccants and active packaging |

| 5 | Clariant | Muttenz, Basel-Landschaft | Switzerland | Provides functional additives for active packaging applications | Active packaging additives |

By Type

By Application

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarActive Packaging Market