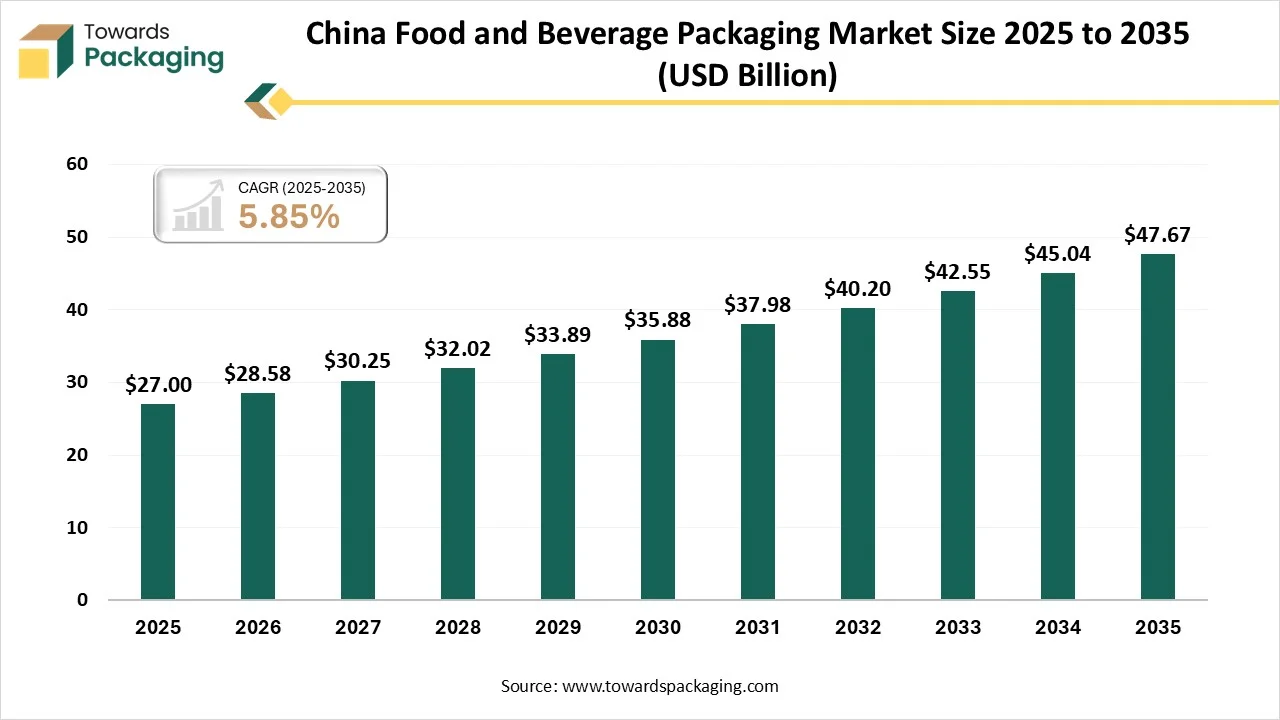

The China food and beverage packaging market is projected to grow from USD 28.58 billion in 2026 to USD 47.67 billion by 2035, registering a CAGR of 5.85% during 2026-2035. The market study provides comprehensive insights covering detailed segment analysis by material type, packaging format, product type, and end-use applications across the food and beverage industry.

It also includes regional demand analysis across major provinces in China, along with trade data, import-export trends, and supply chain evaluation. The report further highlights key manufacturers, suppliers, company market shares, and competitive strategies, while offering an in-depth value chain analysis and industry structure overview. Rising urbanization, changing consumer lifestyles favoring convenience foods, and increasing disposable income continue to drive packaging demand across the country.

Food and beverage packaging is necessary for current food systems. Without accurate packaging, food spoils quickly, contains pollutant risks that would develop, and the worldwide food supply is impossible to track. Every food link material should align with strong safety standards to protect toxic substances from shifting into the required food products.

The food & beverage industry is currently the main driver of invention in packaging. Lines should ensure flexibility, food safety, and constant manufacturing, which accepts fast adaptation to the latest formats and has extremely sustainable materials. Bioplastics, compostable solutions, and high-performance papers are sequentially substituting regular options. This discovery is being driven not only by mechanical technologies, but also significantly by the coordination between connectivity, advanced automation, and talented digital systems. Predictive monitoring software is being assisted by real-time data analysis and sensors, which allows organizations to predict failures, lower waste and energy usage, and update performance.

The plastic packaging segment dominated the market in 2025 as they have become an integral material in the packaging of food and drinks due to its lower cost, durability, and lightweight nature. The most routine types of plastic utilized in food packaging are high-density (HDPE), polyethylene terephthalate (PET), polypropylene (PP), and polyvinyl chloride (PVC). PET is prevalently used to package regular drinks such as soda and water because of its high tensile strength and clarity. Additionally, the manufacturing of such plastics generally involves the polymerization of petrochemical monomers, which can have a major effect on the environment.

The paper and paperboard segment is expected to witness the fastest CAGR during the forecast period. Paper food packaging is a kind of material created from paper or paperboard that is secured for direct or indirect contact with food. Kraft paper is a reliable and rigid paper that is created from the kraft pulping procedure, which involves chemically transforming wood into a pulp with the help of sodium sulfide and sodium hydroxide. Such a strategy protects the long cellulose fibers, resulting in a material that has perfect tensile power and tear resistance as compared to regular paper.

The flexible packaging segment dominated the market in 2025, as it has mainly developed in the food and beverage sector. Because of its several advantages, it is frequently the packaging of choice for different food products on a domestic and worldwide level. By utilizing non-rigid materials in order to pack food, producers can tailor the container to match the brand and product. Flexible packaging is available in a variety of sizes, shapes, and materials that can be made in either formed or unformed patterns.

The semi-rigid packaging segment is expected to witness the fastest CAGR during the forecast period. Semi-rigid packaging points to containers and materials that integrate elements of both flexible and rigid packaging designs. Such containers carry their shape under normal conditions, which can be leveraged smoothly under certain pressure without breaking. Such different characteristics are created specifically for perfectly suited food products, which demand step-by-step assistance during display and transport while staying economical and lightweight to manufacture. The most prevalent semi-rigid packaging materials in the food sector include lined crayons, folding cartons, thermoformed containers, and aseptic cartons. Every kind delivers a particular aim that relies on the food product’s needs for shelf life, barricade prevention, and user convenience.

The bottles & jars segment dominated the market in 2025 as various product types urge various glass designs, and the selection frequently comes down to balancing branding, working, and user expectations. For condiments and sauces, packaging demands to be feasible for the purpose of dispensing or pouring while constantly preventing flavor integrity. Spread and jams advantage from wide-mouth jars, which give importance to reusability and freshness.

The carton packaging segment is expected to witness the fastest CAGR during the forecast period. The Design for Recycling Guidelines from the Food and Beverage Carton Alliance (FBCA) are an important link for making sure that liquid packaging cartons are crafted with recyclability. Such updated rules assist recyclers, producers, waste management, policymakers, and the professionals who match perfect practices, which assist a circular economy.

The beverage segment dominated the market in 2025 as aluminum is the go-to packaging material for several carbonated beverages, energy drinks, and beers. Their famous roots come from their excellent recyclability, lightweight nature, and potential to firmly stand with heavy pressure surroundings, which is found in carbonated beverage filling surfaces and hot filling for constant beverages. On the other hand, glass bottles show luxury quality for several soda, beer, and juice brands. They serve ideal barricade characteristics and online clarity, which have a sensitive nature with careful attention.

The ready-to-eat segment is projected to experience the fastest CAGR during the forecast period. Packaging design is important for such products. The bulk quantity of purchase decisions is created in-store at the moment, and currently, such packaging plays a crucial role in the decision-making procedure. One point that convinces users to buy a ready-to-eat meal product is its presentation. Organizations can use exceptional packaging designs to sell textures and push freshness cues to protect the product’s shelf life.

The China food and Beverage Packaging market is expected to develop rapidly as the development of this region is initially being driven by fast urbanization, developing user choice, and increasing disposable incomes for safety and convenience. The growing food processing sector and developing demand for packaged food and beverages have further fueled market development. Furthermore, strict government regulations on food safety and packaging standards push the acceptance of high-quality and cutting-edge packaging solutions.

Technological developments in terms of packaging materials, such as eco-friendly and biodegradable selections, also encourage the market scenario. The growth of the retail industry and e-commerce creates a need for groundbreaking packaging to establish product integrity during transit. In addition to that, growing alertness about sustainability among users and producers is encouraging a move towards eco-friendly packaging materials, which has further proposed market growth.

By Packaging Material

By Packaging Type

By Product Type

By Application

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarChina Food and Beverage Packaging Market