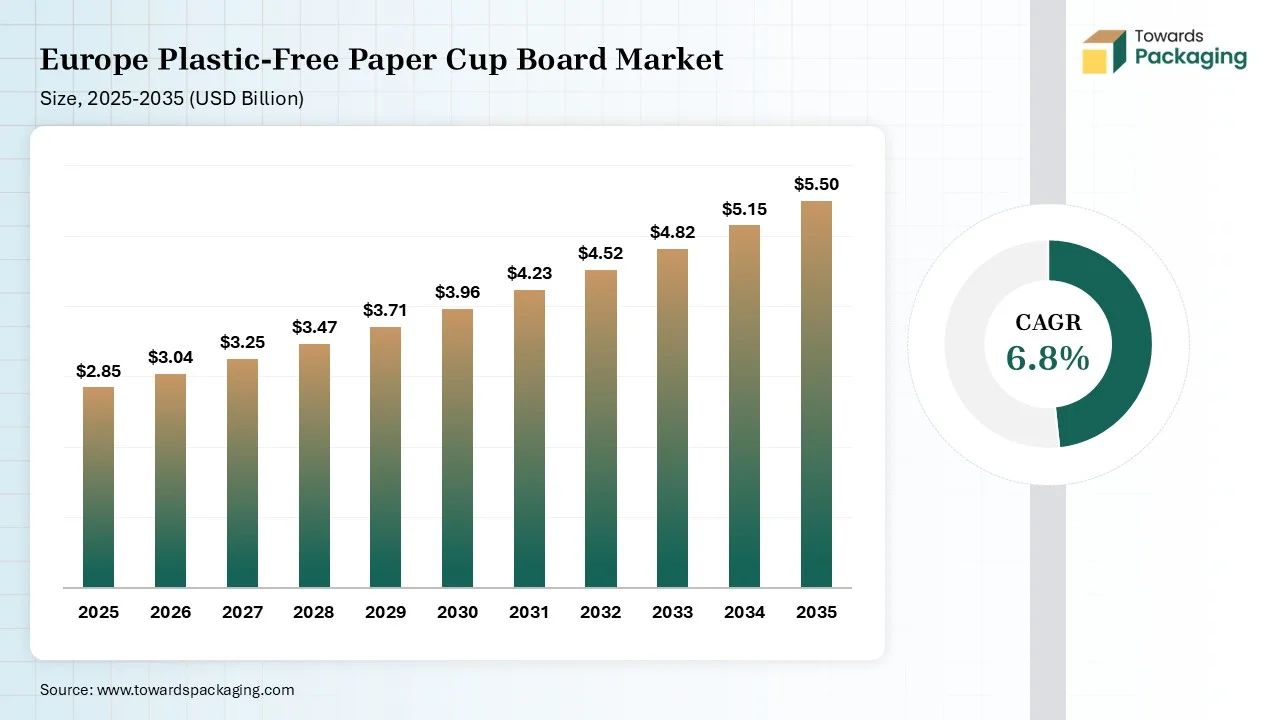

The Europe plastic-free paper cup board market is projected to grow from USD 3.04 billion in 2026 to USD 5.5 billion by 2035, registering a CAGR of 6.8% during the forecast period. The report covers detailed market size analysis, revenue forecasts, segment-wise performance, regional demand trends, company market shares, competitive benchmarking, value chain assessment, trade and import-export analysis, pricing trends, production capacity, and comprehensive profiles of leading manufacturers, suppliers, distributors, and industry participants across Europe.

Market Size (2025): USD 2.85 Billion

CAGR (2025–2035): 6.8%

Market Volume (2025): 2.95 Million Tons

Volume CAGR (2025–2035): 5.9%

Plastic-free paper cup board is an environmentally-friendly feedstock that produces single-use food containers and cups. They possess characteristics like zero plastic, excellent biodegradability, superior printability, and standard recyclability. They have excellent heat resistance and are produced using sustainable materials. Plastic-free paper cup board offers benefits like high compostability, excellent consumer appeal, and easier recyclability. They are used in applications like food containers, portion-controlled cups, beverage cups, catering trays, food sampling containers, and others.

Technological developments like machine vision, digital prototyping, computer vision, predictive maintenance, precision extrusion, and NIR spectroscopy are experiencing Europe plastic-free paper cup board market. Technological developments are driven by the demand for manufacturing precision, sustainable coatings, and recyclability. The AI is a major advancement that helps in material selection and process automation.

AI rapidly develops biodegradable alternatives and selects feedstocks in an appropriate ratio. AI automates pulp mixing process and analyzes defective lined board. AI identifies accurate bio-coating combinations and detects micro-tears in plastic-free paper cup boards. AI analyzes seasonal trends and reduces scrap usage. Overall, AI helps in carbon footprint tracking and the development of advanced materials.

The stage acquires raw materials like bamboo fibers, water-based coatings, virgin wood pulp, sugarcane fibers, and polylactic acid.

Material processing involves steps like raw pulping, coating application, and drying. Conversion includes steps like printing, die-cutting, moisture conditioning, sidewall formation, bottom sealing, and rim curling.

Package design focuses on barrier coatings, material selection, and ergonomics. The prototyping focuses on CAD modeling, rapid prototyping, and seam folding.

The Europe plastic-free paper cup board market is fragmented into eco-friendly packaging developers and well-developed paperboard manufacturers. The Stora Enso company launched a new specialized paperboard product range named Cupforma Natura Solo, which is free from traditional plastic coating. The United Kingdom-based company Notpla & Horizon Europe gained investment of €4 million for increasing the production of home-compostable coffee cups. The new startup Picup company focuses on manufacturing fully plantable paper cups.

Mondi company offers a functional barrier paper range, which includes Ultimate Protection and Cupstock Boards for the production of sustainable packaging. The Huhtamaki company introduced a new recyclable paper cup product, ProDiary, for dairy products. The UK-based company, ButterflyCup, manufactures takeaway paper cups to reduce plastic waste. Benders Paper Cups company uses virgin fiber paperboard for the production of sustainable boards.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Stora Enso | Helsinki | Finland | Leading supplier of plastic-free and dispersion-coated cup board solutions in Europe | Cupforma paper cup boards |

| 2 | Metsä Board | Espoo | Finland | Major producer of recyclable barrier-coated paperboard for foodservice cups | Barrier paperboards |

| 3 | Billerud | Solna | Sweden | Strong presence in sustainable foodservice paperboard solutions | Fiber-based cup board |

| 4 | Huhtamaki | Espoo | Finland | Global leader in paper cup manufacturing and plastic-free cup innovation | Paper cups and foodservice packaging |

| 5 | Graphic Packaging International | Atlanta, Georgia | USA | Commercial supplier of paper-based cup solutions for European foodservice markets | Paper cups and cup stock technologies |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Duni Group | Malmö | Sweden | Major European foodservice packaging supplier transitioning to plastic-free formats | Sustainable beverage cups |

| 2 | Sappi | Johannesburg | South Africa | Supplies specialty papers and barrier technologies for packaging applications | Functional paperboards |

| 3 | UPM Specialty Papers | Helsinki | Finland | Developer of recyclable barrier papers for food packaging | Barrier papers |

| 4 | Walki Group | Espoo | Finland | Produces fiber-based barrier materials and foodservice packaging substrates | Barrier-coated paper solutions |

| 5 | Kotkamills | Kotka | Finland | Pioneer in plastic-free and recyclable cup stock materials | Plastic-free cup boards |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Michelman | Cincinnati, Ohio | USA | Key supplier of water-based barrier coatings enabling plastic-free cups | Functional coating technologies |

| 2 | Paramelt | Heerhugowaard | Netherlands | Supplies specialty coatings for sustainable paper packaging | Barrier coating solutions |

| 3 | Ahlstrom | Helsinki | Finland | Develops specialty fiber materials for sustainable food packaging | Fiber-based packaging substrates |

| 4 | Papkot | Istanbul | Türkiye | Emerging provider of plastic-free barrier coating technologies | Advanced barrier coatings |

| 5 | W-Cycle | Tel Aviv | Israel | Developer of compostable and fiber-based barrier technologies | Food-contact barrier solutions |

The virgin fiber paperboard segment dominated the market with 32% share in 2025 due to the high demand from premium cup producers. The thriving food safety standards and the focus on contamination-free recyclability increase the adoption of virgin fiber paperboard. The need to prevent liquid leakage and the availability of leak-proof sealing increase the use of virgin fiber paperboard. The exceptional printability, high rigidity, and excellent barrier compatibility of virgin fiber paperboard drive the segment growth.

The recycled fiber paperboard segment held the 28% market share in 2025 due to the growing restrictions on plastic-lined cups. The shift away from fossil-based plastics and the ongoing innovations in dispersion barrier coatings increase the adoption of recycled fiber paperboard. The improved visual quality, low carbon footprint, superior recyclability, and cost stability of recycled fiber paperboard support the segment growth.

The bagasse-based paperboard segment held the 15% market share in 2025 due to the growing interest in agricultural waste-based materials. The shift of food packaging towards compostable materials and the focus on zero-deforestation increases the use of bagasse-based paperboard. The transition away from hazardous coatings increases production of bagasse-based paperboard. The superior environmental metrics and robust performance of bagasse-based paperboard boost the segment growth.

The PE-free aqueous coating segment dominated the market with 35% share in 2025 due to the stringent EU regulations. The well-established industrial-composting facilities and the focus on effectively sealing liquids increase the adoption of PE-free aqueous coating. The café chains are actively demanding plastic-free packaging that increases the production of PE-free aqueous coating. The awareness about microplastic migration risks and the need for robust barriers increases the adoption of PE-free aqueous coatings. The true recyclability and uncompromised performance of PE-free aqueous coating drive the segment growth.

The bio-based dispersion coating segment held the 25% market share in 2025 due to the 70% consumer interest in sustainable packaging. The growing enforcement of reuse standards and the company's focus on enhancing environmental image increase the adoption of bio-based dispersion coatings. The increased replacement of plastic liners and the expansion of modern coffee consumers increase the adoption of bio-based dispersion coating. The seamless recyclability and superior profile of bio-based dispersion coating support the segment growth.

The PLA coating segment held the 22% market share in 2025 due to the rising production of eco-friendly cups. The awareness about reducing fossil fuel dependence and the focus on minimizing GHG emissions increase the adoption of PLA coating. The strong foodservice operators' base and green certifications increase the adoption of PLA coating. The superior functional performance, biodegradability, and fewer emissions in PLA coating boost the segment growth.

The hot beverage cups segment dominated the market with 45% share in 2025 due to the huge tea consumption. The thriving takeaway beverages and the move away from PE linings increase demand for hot beverage cups. The growing daily coffee consumption and the focus on keeping the drink warm increase the adoption of hot beverage cups. The excellent thermal insulation and ease of recycling of hot beverage cups drive the segment growth.

The cold beverage cups segment held the 25% market share in 2025 due to the increased takeaway of chilled dairy products. The expanding quick-commerce delivery and the growth in specialty cold beverages increase the adoption of cold beverage cups. The strong presence of iced beverage culture and the robustly growing hospitality chains increases demand for cold beverage cups. The interest in disposable cold cups supports the segment growth.

The food & dessert cups segment held the 20% market share in 2025 due to the well-developed food delivery platforms. The need for a healthier consumer experience and the strong presence of food delivery aggregators increase the adoption of food & dessert cups. The high rate of dessert consumption and the growing use of recyclable materials in the food industry increase the production of food & dessert cups. The rise in guilt-free treats supports the segment growth.

The quick service restaurants (QSRs) segment dominated the market with 30% share in 2025 due to the increasing use of plastic-free paper boards in the QSRs. The increased processing of daily cold beverages and the high hygiene standards increase the adoption of plastic-free paper cup boards. The high volume of takeaway orders and the growing mobile advertising in QSRs increase the adoption of plastic-free paper cup boards. The operational convenience and high customizability of plastic-free paper cup boards in QSRs drive the segment growth.

The cafes & coffee chains segment held the 28% market share in 2025 due to the burgeoning number of daily coffee drinkers. The increased ice cream consumption and the expansion of cold deserts increase the adoption of plastic-free cup boards. The Gen Z consumer preference for cafes and the strong snack culture increases the adoption of plastic-free cup boards. The popularity of premium coffee supports the segment growth.

The institutional segment held the 18% market share in 2025 due to the adoption of certified recyclable packaging in institutions. The strong focus on meeting waste-reduction metrics and the rise in environmentally conscious students increase the adoption of plastic-free cup boards. The increased plastic ban in corporate offices and the focus on hygiene in workplaces increase the adoption of plastic-free cup boards, boosting the segment growth.

The direct B2B sales segment dominated the market with 55% share in 2025 due to the high-volume procurement. The rise in custom printing negotiations and the ESG commitments increases the adoption of direct B2B sales. The high volume of QSR contracts and the rise in custom branding increase the adoption of direct B2B sales. The company's focus on raw material sourcing transparency and the management of high-volume clients increases the adoption of direct B2B sales, driving the segment growth.

The distributors & wholesalers segment held the 30% market share in 2025 due to the requirement for consistent certification documentation. The strong presence of small-sized beverage operators and the focus on just-in-time delivery increase the adoption of distributors & wholesalers. The explosion of cloud kitchens and the rise in the procurement of food-grade cups increases demand for distributors & wholesalers. The presence of custom branding and the convenience of distributors & wholesalers support the segment growth.

The online procurement platforms segment held the 15% market share in 2025 due to the availability of lead-time comparison. The presence of integrated carbon calculators and the availability of specialized plastic-free board suppliers help with expansion. The smaller cafes and the buyers' focus on checking the eco-certifications increase the buying of plastic-free paper cup boards from online procurement platforms.

The United Kingdom is the major shareholder in the market due to the growing foodservice industry. The popularity of takeaway coffee and the excellent recycling infrastructure increases demand for plastic-free paper cup board. The rise in takeaway tea and the growing consumer consciousness about plastic pollution increase the adoption of plastic-free paper cup boards. The innovations, such as aqueous dispersion coatings, support the overall market growth.

Germany is rapidly growing in the market due to the growing aqueous coating advancements. The shift to fully biodegradable alternatives and the presence of a strong paper recycling ecosystem increase the production of plastic-free paper cup board. The well-established coffee chains and the rise in on-the-go beverage culture increase the adoption of plastic-free paper cup boards. The interest in guilt-free packaging drives the market growth.

France is robustly expanding in the market. The stringent legislation for lowering plastic waste and the sustainability commitments increase the use of plastic-free paper cup board. The rise in biodegradable takeout and the awareness of zero-waste packaging increases the use of plastic-free cup boards. The strong fast-food chains boost the market growth.

Italy is substantially growing in the market. The well-developed local recycling infrastructure and the shift away from plastic coatings increase demand for plastic-free paper cup board. The strong presence of coffee shops and the rising development of bio-based coatings increase the production of plastic-free paper cup boards. The well-developed composting infrastructure and the move towards lid-free technology drive the market growth.

By Material Type

By Coating Type

By Application (Cup Type)

By End-Use Industry

By Distribution Channel

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarEurope Plastic-Free Paper Cup Board Market