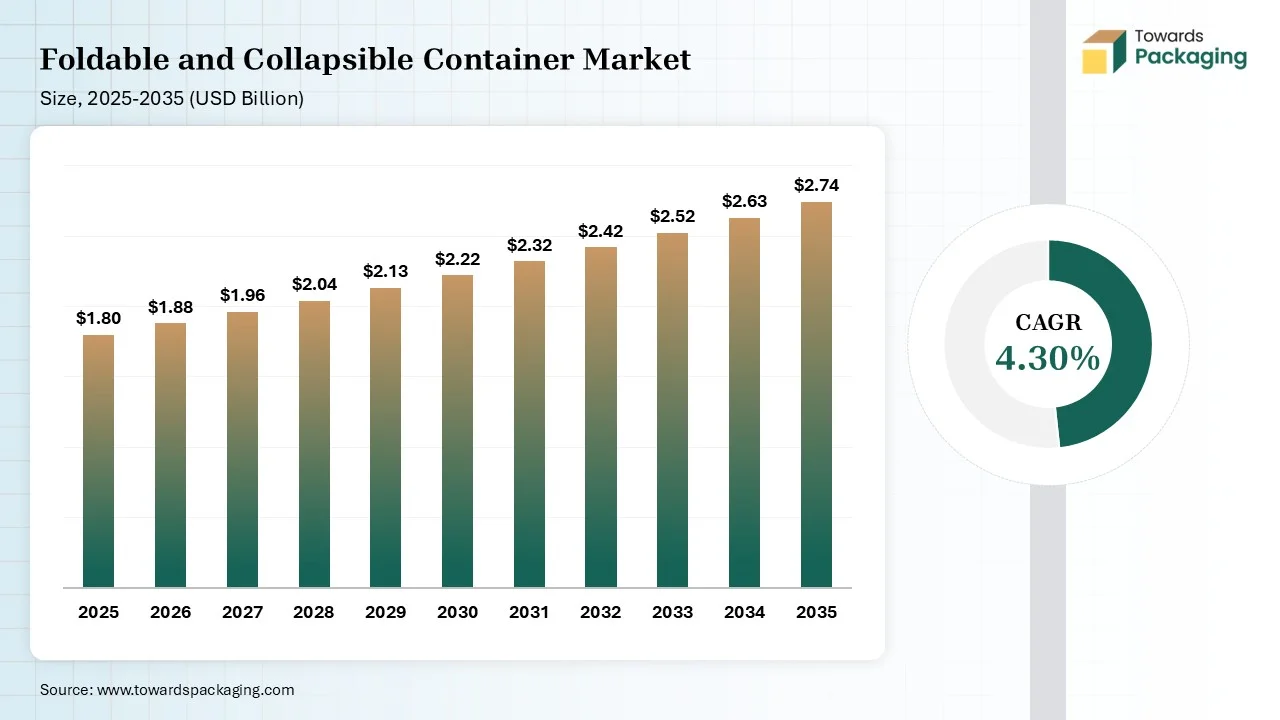

The foldable and collapsible container market is expected to increase from USD 1.88 billion in 2026 to USD 2.74 billion by 2035, growing at a 4.30% CAGR from 2026 to 2035. The study provides comprehensive market sizing, revenue forecasts, segment analysis by product, material, capacity, application, and end use, along with regional trends, competitive landscape, company benchmarking, manufacturers and suppliers data, value chain analysis, import-export statistics, and strategic market insights.

The foldable and collapsible containers are reusable transport containers that decrease storage space and eliminate redundant fees. These collapsible containers can be folded back up when empty to free up space in businesses' warehouses and maximize transportation efficiency. New market demand on the supply chain for advanced packaging and material handling solutions is accompanied by the expansion of international trade.

The increasing demand for space-efficient and environmentally-friendly packaging solutions is fueling the growth of the foldable and collapsible container market. The expansion of international trade is complementing the new demand of the supply chain for advanced packaging and advanced material handling solutions. Additionally, sustainability regulations and corporate circular-economy initiatives are accelerating the adoption of reusable containers over single-use packaging formats.

The foldable and collapsible container market is undergoing a shift toward technology and AI. The adoption of AI-driven analytics in company systems is on the rise, helping organizations track container movements and fine-tune distribution logistics for containers. Machine learning algorithms help logistics companies minimize empty container movements and cut operational costs.

Advanced RFID tags, Internet of Things (IoT) sensors, and real-time tracking platforms offer a way to maintain visibility of the container throughout the entire supply chain. That helps check the container location and condition, and monitor the amount of use. Digital twins and simulation software are also used by manufacturers to create lighter, sturdier container structures that resist repeated handling and also result in a reduction in material usage. Furthermore, predictive maintenance tools also assist operators in minimizing replacement costs and maximizing the lifespan of their products by predicting damage and wear before it happens.

Sourcing materials, including plastics, metals, composites, and recycled materials, forms the basis of the production of foldable and collapsible containers. Suppliers offer non-toxic ingredients that contribute to sustainable packaging and can easily convert to multi-use and lightweight designs.

Raw materials are turned into components for containers such as panels, frames, hinges, locking devices, and structures. Molding, extrusion, fabrication, and reinforcement technologies used by manufacturers provide strength and flexibility.

Foldable and collapsible containers are engineered by manufacturers to have an optimised structure to enhance both storage efficiency and durability, as well as transport options. This is only possible due to the advanced engineering, which allows us to design it to be space-saving, ergonomic, and easy to handle by automated logistics systems.

Integrated with tracking technologies, including RFID, Internet of Things sensors, and digital monitoring solutions for supply chain visibility. Quality testing assures load-bearing ability, safety performance, durability in the life cycle, and compliance with industry standards.

Filled containers are delivered to the automotive, retail, food logistics, manufacturing, and warehousing industries. Distributing networks have the potential to implement the adoption of reusable packaging in global supply chains and reverse logistics systems.

Containers are circulated back through the supply chain, cleaned, inspected, and reused for subsequent trips. Meanwhile, efficient reuse programmes help to maximise the use of assets, minimise packaging waste, and help promote circular economy models.

The plastic segment dominated the market with a share of 54% in 2025, as it provided highly competitive lightweight performance, durability, and operational flexibility. The material facilitates high-throughput deliveries in automotive, retail, food, and industrial supply chains. Plastic containers provide high moisture, corrosion, and handling resistance, making them well-suited for modern-day warehouses. Adoption of plastic-based solutions is likely to continue robustly in order to focus on reusables and efficient storage solutions for industries.

The metal segment held a 24% market share in 2025, owing to its strength, stability, and longevity. Steel and aluminum containers are used for the transportation of automotive parts, machinery components, and industrial materials. Metal-based solutions continue to increase in certain niche applications with demanding protection and durability needs.

The composite & others segment held an 11% market share in 2025, as these specialized solutions of containers are increasingly being embraced for automotive and aerospace applications and high-value industrial applications. These materials provide improved structural performance while reducing overall container weight, helping companies optimize transportation efficiency. Demand is robust in niche logistics segments, helped by higher investments in advanced material technologies and customized reusable packaging systems.

The bulk bins segment dominated the market with a share of 26% in 2025, due to their prevalent use in medium- and heavy-material handling industries. The containers offer increased storage capacity and structure over smaller reusable formats. Sufficient bulk bins are used for the bulk transport of heavy and high-volume materials in industries like automotive, chemicals, agriculture, and food processing. Furthermore, manufacturers are now developing recycled content as well to help achieve sustainability goals and reduce packaging waste.

The pallets segment held a 22% market share in 2025, as they continue to be an important element in the global transportation and warehousing system. Pallets are essential for companies from manufacturing to logistics and distribution, ensuring consistency in storage and optimizing loading processes. Stability and handling efficiency continue to be crucial for supply chain operations, making pallets essential.

The crates segment held a 21% market share in 2025, owing to its increasing demand from retail and e-commerce distribution centres and urban distribution networks. They are designed to be compact so that they are easy to carry, can be stacked, and fitted for regular transport throughout supply lines. Collapsible crates are now a popular option for retailers and logistics companies to arrange products for safe storage and transport.

The 501–1000 liters segment dominated the market with a share of 33% in 2025, due to its suitability for industrial-scale transportation and storage operations. These containers prove to be ideal in terms of carrying capacity, handling efficiency, and space utilization along the supply chain. This capacity range is being increasingly used by manufacturing, automotive, food processing, and logistics businesses for the transport of medium- to large-volume materials. Advanced design with better frames, folding mechanisms, and load stability is being developed by manufacturers. The emphasis on optimization of the supply chain drives further growth in this segment.

The 251–500 liters segment held a 29% market share in 2025, aided by businesses expanding their regional fulfillment network and automated fulfillment centers. These boxes facilitate quicker movement of products and minimize operational problems with manual handling requirements. The expansion of the shipment of medium-capacity containers is fueled by increasing demand for versatile and reusable packaging containers.

The up to 250 liter segment held a 21% market share in 2025, due to rising demand for lightweight storage and transportation applications. Such containers offer businesses a convenient handling feature for frequently moving smaller amounts of products. They have lower door-to-door volume and promote space-saving operations in urban distributions. Companies are becoming interested in the segment because of its flexible solution for last-mile logistics and for the movement of material inside an organization's premises.

The medium duty segment dominated the market with a share of 38% in 2025, as it allows for a balance between durability, flexibility, and cost efficiency. Medium-duty solutions clear the goods intermediate between those transported on lightweight products and industrial-duty structures that provide them with greater protection. They are versatile in nature and fit easily into all types of warehouses, logistics, and inventory systems.

The heavy duty segment held a 34% market share in 2025, due to increasing demand for high-strength solutions across industrial and commercial supply chains. Increased forklift rigour, stacking pressure, and regular handling demands are easily taken by these containers. Heavy-duty designs are currently being enhanced by reinforced structures, while improved polymeric materials and corrosion resistance are enhancing the use of these stainless steels.

The light duty segment held a 28% market share in 2025, driven by increased applications' need for easy handling and mobility, and frequent product handling. They are designed to do smaller loads for ease of retail, distribution, and in-house warehouse functions. The segment benefits from an increase in e-commerce activity and an increase in localized delivery networks.

The industrial & automotive segment dominated the market with a share of 32% in 2025, due to strong demand for durable transport packaging across manufacturing and component supply chains. These containers are utilized in the automotive industry for the transportation of components, assemblies, and raw materials between production sites and suppliers. Reusable containers are preferred by Industrial companies due to the possibility of using them for multiple handling cycles, and they are useful for warehouse organization. These solutions are strong and stackable, which helps to minimize damage to the materials in transit.

The food & beverage segment held a 24% market share in 2025, owing to the increasing requirements for safe, hygienic, and reusable transport solutions. The manufacturers are releasing containers that are constructed of new materials, new ventilation, and/or new designs, suitable for food-grade applications. Additionally, companies are integrating tracking technologies to gain better visibility of their inventory and to monitor the movement of their products.

The retail & e-commerce segment held an 18% market share in 2025, driven by increasing demand for flexible packaging solutions across distribution and fulfillment operations. Efficient storage, sorting, and delivery systems have grown as online shopping has increased. Collapsible containers are used to control the movement of stock from the warehouses, stores, and customers in retail companies. Their folds allow these containers to be stored at a lower capacity and make the return logistics easier.

Asia Pacific dominated the market with a 37% share in 2025 and is expected to grow at the fastest CAGR of 5.2% during the forecast period, driven by rapid industrial development, manufacturing growth, and ongoing logistics infrastructure development. An efficient, reusable transport packaging system is emphasized by countries such as Japan, India, the Republic of Korea, and China for their production networks.

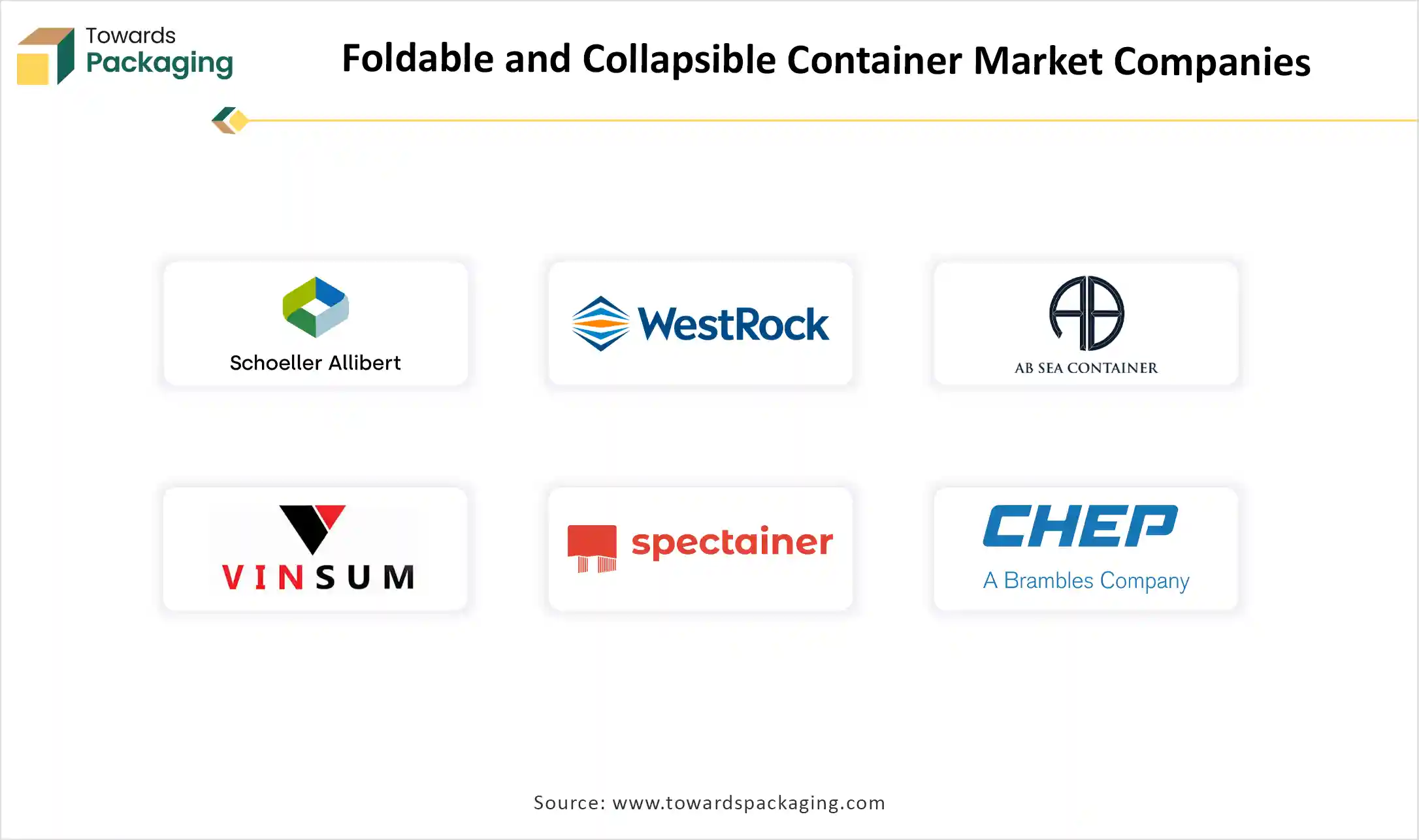

The automation trends are driving a growth in the demand for standardized collapsible containers, which can work efficiently with robotic handling systems. Companies like Schoeller Allibert, CABKA Group, and SSI SCHAEFER are working on container solutions that are suitable for automated supply chains.

North America held 28% market share in 2025, due to the well-developed logistics network, a high level of automation, and a solid network for reusable packaging. The automotive sector, retail and food distribution, and industrial sectors have well-settled supply chains in the United States and Canada. The increasing recognition of sustainability needs is also driving businesses to consider reusable transportation methods, including foldable and collapsible containers.

The Europe held a 25% market share in 2025, as a result of an effective environmental policy, supporting circular economy projects, and an increasing demand for sustainable packaging systems. Foldable and collapsible containers are becoming popular in Europe for industries that want to make their transport more efficient and reduce packaging waste.

Latin America held the 6% market share in 2025, due to the rapid expansion of agricultural exports, food processing operations, and regional manufacturing activities. Brazil is building logistics infrastructure to increase the efficiency of supply chains and their increasing trade volumes at home and abroad. Reusable containers are widely used in the region to transport fresh produce, processed foods, and export goods to facilitate efficient handling operations and cut packaging waste among the companies.

The Middle East & Africa held the 4% market share in 2025, as governments and private enterprises highly investing in logistics infrastructure, industrial diversification, & supply chain modernization initiatives. Increasing volumes of shipment cargo flowing through the major ports and logistics corridors are stimulating companies to invest in collapsible container systems that enable maximum space utilization when they are being returned. Moreover, these developments position the Middle East & Africa as an increasingly important market for advanced reusable transport packaging solutions.

| Rank | Company | Headquarters | Country | Major Contribution to the Foldable and Collapsible Container Market | Key Packaging Products and Services |

| 1 | Schoeller Allibert | Hoofddorp, Netherlands | Netherlands | The company specializes in reusable transport packaging solutions and develops foldable containers focused on supply chain efficiency, automation compatibility, and circular logistics. | Foldable Large Containers (FLCs), Euro Containers, Automotive Containers, Reusable Plastic Pallets, Attached Lid Containers |

| 2 | WestRock Company | Atlanta, Georgia, United States | United States | The company focuses on sustainable packaging solutions and develops advanced container systems using recyclable materials for industrial and consumer supply chains. | Reusable Packaging Solutions, Corrugated Packaging Systems, Folding Cartons, Protective Packaging Solutions |

| 3 | A B Sea Container Private Limited | Mumbai, India | India | The company provides collapsible container solutions for logistics and industrial applications, focusing on space optimization and efficient transportation systems. | Collapsible Storage Containers, Foldable Cargo Containers, Industrial Storage Solutions, Material Handling Containers |

| 4 | Vinsum Axpress | Mumbai, India | India | The company supports logistics operations through reusable packaging and transportation solutions designed for efficient warehousing and distribution management. | Returnable Packaging Solutions, Logistics Containers, Supply Chain Management Services, Storage & Handling Solutions |

| 5 | Spectainer | Melbourne, Australia | Australia | The company develops collapsible container technologies that improve empty container transportation efficiency and reduce logistics space requirements. | Collapsible Shipping Containers, Foldable Cargo Units, Container Modification Solutions, Space-Saving Transport Systems |

By Material

By Product Type

By Capacity

By Load Capacity

By End Use

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarFoldable and Collapsible Container Market