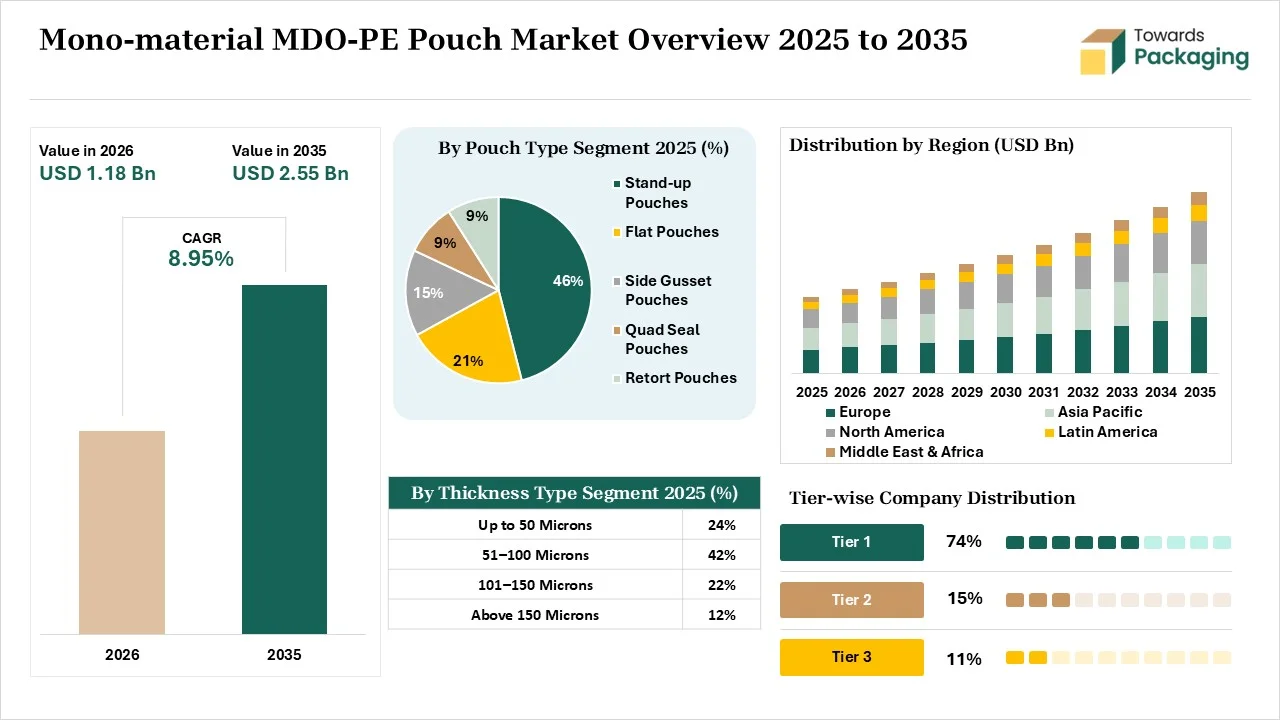

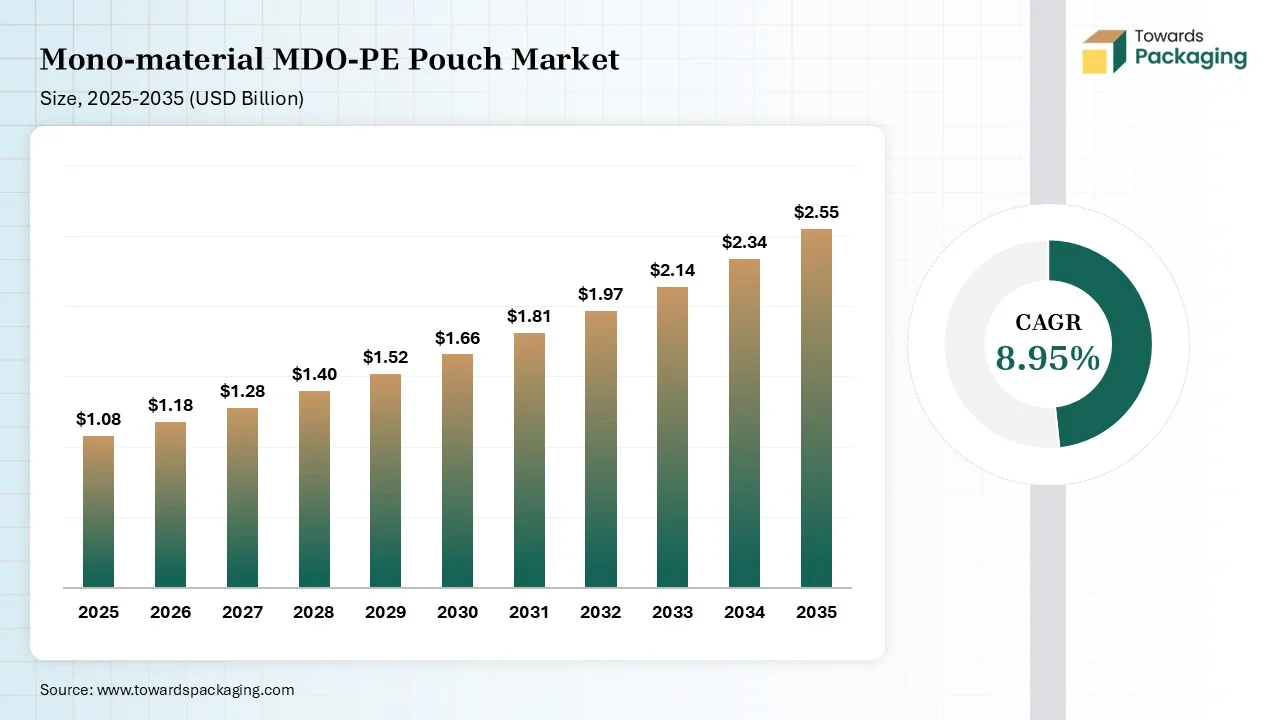

The Mono Material MDO PE Pouch Market is projected to grow from USD 1.18 billion in 2026 to USD 2.55 billion by 2035, registering a CAGR of 8.95% during the forecast period. This report provides comprehensive insights into market size, growth forecasts, segment-wise analysis, regional performance, company profiles, competitive landscape, value chain assessment, trade data, manufacturers and suppliers analysis, pricing trends, demand outlook, and sustainability-driven market developments shaping the industry.

The mono-material MDO-PE pouch is a sustainable packaging bag made from polyethylene. The pouch offers high barrier capabilities and is made up of MDO technology. The pouches are 100% recyclable and have a premium printability. The pouches offer benefits like superior puncture resistance, premium aesthetics, total circular economy, downgauging, and customizable barrier protection. The mono-material MDO-PE pouches are used for dry goods, liquid products, shelf-ready display bags, frozen fruits, liquid soaps, and confectionery items.

The mono-material MDO-PE pouch market growth is driven by the growing number of brands favoring circular designs, rising lightweighting, brands' commitments towards sustainability, superior printability needs, retail display trends, burgeoning mono-material designs, adoption of EVOH dispersion techniques, growth in e-commerce delivery, and the emerging frozen food industry.

The mono-material MDO-PE pouch is experiencing technological developments due to demand for resolving traditional limitations of packaging. Developments like digital twin simulations, digital pouch workflows, automated extrusion controls, and smart diagnostics help in providing BOPP-like stiffness and maximizing output. AI is a robust technological development in the market that resolves material limitation problems.

AI easily simulates the mechanical properties of the mono-materials and inspects print inconsistencies in packaging. AI prevents the deformation of the pouch and automatically adjusts processing parameters in packaging developments. AI recovers the high-purity material and optimizes the process of film extrusion. AI offers predictive designs of packaging and easily tracks packaging specifications. Overall, AI helps from the material formulation to supply chain traceability.

The raw materials, like Base MDO-PE films, high-barrier additives, sealant PE, accessory components, and coatings, are required.

Material processing involves steps like extrusion, MDO, and cooling. The conversion includes steps like printing, lamination, and pouch fabrication.

Design and prototyping include steps like outer substrate selection, sealing layer addition, integration of barrier components, lamination, pouch manufacturing, pouch trials, and recyclability validation.

The stand-up pouches segment dominated the market with 46% share in 2025. The focus on the reduction of scope 3 carbon emissions and demand for stable base packaging increases the adoption of stand-up pouches. The interest in flat-pack designs and the growing vertical display activities increases the use of stand-up pouches. The brand visibility enhancements and the rising use of packaging that stands upright increase the use of stand-up pouches. The cost-saving logistics and exceptional printability of stand-up pouches drive the segment growth.

The retort pouches segment held the 9% market share in 2025 and is expected to grow at the fastest CAGR of 10.2% during the forecast period. The texture preservation of shelf-stable foods and the elimination of glass jars increase the use of retort pouches. The focus on compatibility of high-heat sterilization and the rising retail pressure increases the use of retort pouches. The high barrier protection and excellent mechanical performance of retort pouches help with expansion. The operational benefits, true recyclability, and circular design of retort pouches support the segment growth.

The 51-100 microns segment dominated the market with 42% share in 2025. The focus on puncture protection of retail goods and the need for PET-like stiffness increases the use of 51-100 microns. The development of thinner packaging formats and the focus on optical clarity of packaging increase the adoption of 51-100 microns. The need for high barrier and the development of flat-bottom bags increases the use of 51-100 microns. The versatile weight capacity and ideal sealability of 51-100 microns drive the segment growth.

The above 150 microns segment held the 12% market share in 2025 and is expected to grow at the fastest CAGR of 10.1% during the forecast period. The growing packaging of heavy pet food and focus on avoiding reprocessing contamination increases the adoption of above 150 microns. The rise in online shipping and the growing replacement of bulky pouches increases the use of above 150 microns. The requirement for a rigid pouch wall and the rising high-speed packaging processing increases the adoption of above 150 microns. The improved mechanical durability of above 150 microns supports the segment growth.

The zipper closure segment dominated the market with 44% share in 2025. The prevention of pet care spills and the development of highly recyclable packs increase the adoption of zipper closures. The rising use of low-temperature sealants and the focus on safely resealing products increase the adoption of zipper closures. The on-the-go convenience and the focus on avoiding separate disparate closures increase the adoption of zipper closures. The production line efficiency and perfect material compatibility of the zipper closure drive the segment growth.

The spout closure segment held the 14% market share in 2025 and is expected to grow at the fastest CAGR of 10.5% during the forecast period. The increased packaging of energy drinks and the demand for mess-free dispensing increase the use of spout closures. The demand for anti-choke closures and the focus on product differentiation increase the use of spout closures. The need for resealability for condiments and the focus on preventing cap litter increase the adoption of spout closures. The innovations, like automated spout-insertion, support the segment growth.

The medium barrier segment dominated the market with 38% share in 2025. The well-developed polyethylene recycling streams and the growth in fast-moving consumer goods increase the adoption of medium barrier pouches. The focus on the prevention of deformation and the frozen goods packaging increases the use of medium barrier pouches. The growth in fresh produce and the retailers' demand for shelf-life increases the use of medium barrier pouches. The high machinability and superior cost-effectiveness of medium barrier drives the segment growth.

The ultra-high barrier segment held the 14% market share in 2025 and is expected to grow at the fastest CAGR of 10.8% during the forecast period. The focus on avoiding EPR fees and the need for high-quality printing on packaging increases the adoption of ultra-high barrier pouches. The premiumization of chilled dairy and the demand for barrier protection against moisture vapor transmission increase the adoption of ultra-high barrier pouches. The protection of oxygen-sensitive products and the expanding retort utilization increase the use of ultra-high barrier pouches, supporting the segment growth.

The food packaging segment dominated the market with 51% share in 2025. The demand for flexographic printing in food packaging and the need for protecting food products from UV light increase the use of mono-material MDO-PE pouches. The rise in eco-friendly food packaging and the focus on keeping snack items fresh increase the use of mono-material MDO pouches. The shelf-life requirements in the food industry and the environmental pledges in the food brands increase the adoption of mono-material MDO-PE pouches, driving the segment growth.

The pharmaceutical & healthcare segment held the 6% market share in 2025 and is expected to grow at the fastest CAGR of 10.6% during the forecast period. The rising need for medical device protection and the focus on healthcare supply chains' durability increases the adoption of mono-material MDO-PE pouch. The focus on maintaining sterile integrity of surgical instruments and the recyclability mandates in pharmaceutical infrastructure increases the adoption of mono-material MDO-PE pouches. The prevention of diagnostic degradation and the shifting away from rigid medical packaging increases the adoption of mono-material MDO-PE pouches, supporting the segment growth.

The food & beverage manufacturers segment dominated the market with 56% share in 2025. The food manufacturers' focus on waste reduction and the need to avoid expensive equipment redesigns increases the adoption of mono-material MDO-PE pouches. The optimal food protection demand and the avoidance of rigid containers increase the adoption of mono-material MDO-PE pouches. The focus on lowering inventory complexity and the growing dried food industry increases the adoption of mono-material MDO-PE pouches, driving the overall segment growth.

The pharmaceutical companies segment held the 7% market share in 2025 and is expected to grow at the fastest CAGR of 10.8% during the forecast period. The need for low OTR rates in pharmaceuticals and the increasing use of drug pouches increase the adoption of mono-material MDO-PE pouches. The flawless machinability demand in drug packaging and the protection of moisture-sensitive APIs increase the use of mono-material MDO-PE pouches. The excellent safety needs in pharmaceuticals and the requirements for a high barrier in pharmaceuticals support the segment growth.

The direct sales segment dominated the market with 48% share in 2025. The selection of proper resin and the complex technical specifications of pouches increase the adoption of direct sales. The consistent quality demand and the customized sealant layers need increased adoption of direct sales. The adjustments of machinery and the preservation of premium margins increase the use of direct sales. The focus on strengthening supplier relationships drives the overall segment growth.

The online procurement platforms segment held the 8% market share in 2025 and is expected to grow at the fastest CAGR of 11.3% during the forecast period. The increased streamlining of specific polymers and the rise in technical sourcing increase the use of online procurement platforms. The focus on viewing transparent specifications and the expanding rapid-delivery models increases the use of online procurement platforms. The sourcing of compatible components and the digitalization of tailored packaging increase the adoption of online procurement platforms, supporting the overall segment growth.

Europe dominated the market with a 31% share in 2025. The legislative mandates and the presence of leading packaging converters increase the adoption of mono-material MDO-PE pouches. The huge plastic packaging taxes and strong material recovery facilities increase the use of mono-material MDO-PE pouches. The brand's focus on minimizing compliance fees and the corporate eco-targets increases the use of mono-material MDO-PE pouch. The need for high-barrier packaging in medical products drives the market growth.

Asia Pacific held the 29% share of the market in 2025 and is expected to grow at the fastest CAGR of 10.1% during the forecast period. The transition away from multilayer packaging and the focus on protecting hygiene products increases the use of mono-material MDO-PE pouches. The rising personal care refills and the standardization of sustainable packaging increase the use of mono-material MDO-PE pouches. The stringent waste legislation and the transitioning away from multi-layer foams increase the use of mono-material MDO-PE pouches. The high investment in high-barrier MDO-PE supports the market growth.

North America held the 26% market share in 2025. The state-level mandates on retail and the recyclability issues in the multi-layer composites increase the adoption of mono-material MDO-PE pouches. The focus on enhancing post-consumer sorting and the growing consumer pressure on brands increases the use of mono-material MDO-PE pouches. The innovations, like advanced sealants and the rise in packaging reengineering in industries, support the overall growth of the market.

The growing sorting challenges in multi-material and the redesigning of packaging in food retail increase the adoption of mono-material MDO-PE pouches.

The demand for premium shelf life and the focus on minimizing transport emissions increase the use of mono-material MDO-PE pouches.

Latin America held the 8% market share in 2025. The mandates on recycled content in Latin American countries and the focus on using minimal raw material increase the adoption of mono-material MDO-PE pouches. The focus on shelf life protection of pharmaceutical products and the popularity of premium personal care in the middle class increase the adoption of mono-material MDO-PE pouch. The thriving specialized pet food sector boosts the market growth.

The Middle East & Africa held the 6% market share in 2025. The introduction of EPR rules in African countries and the shift to lightweight pouches in online food delivery increase the adoption of mono-material MDO-PE pouches. The high utilization of moisture-resistant barriers and the presence of affordable unit-dosing increase the adoption of mono-material MDO-PE pouches. The expansion of on-the-go pouches supports the market growth.

The industrial sustainability programs and the high production of polymer resins increase the adoption of mono-material MDO-PE pouch.

The burgeoning date export industries and the development of customizable pouches support the expansion.

| Rank | Company | Headquarters | Country | Major Contribution to Mono-material MDO-PE Pouch Market | Key Packaging Products and Services |

| 1 | Amcor Plc | Zurich, Switzerland | Switzerland | The company collaborated with Cheer Pack Na and Stonyfield Organic to introduce all-PE spouted pouches. The company manufactures pouches to lower the brand’s footprint. | AmPrima PE Plus Liquid Pouches, AmPrima PE Plus Personal Care Pouches, AmPrima PE Plus Dry & Pet Care Pouches |

| 2 | Berry Global Inc. | Evansville, Indiana, United States | United States | The company offers Entour Sealant & Print films to manufacture pouches. The company also provides voiding agent technologies. | Preserve PE PCR Pouches, Entour Films, Entour Sealant Web, Entour Bold |

| 3 | SABIC | Riyadh, Saudi Arabia | Saudi Arabia | The company manufactures stand-up pouches for non-food items and food items. The company also offers heat-resistant mono-PE solutions. | SABIC HDPE F05060MD, SUPEER mLLDPE, SABIC BOPE BX202, COHERE Polyolefin Plastomers |

| 4 | Constantia Flexibles | Vienna, Austria | Austria | The company invested in Hosokawa Alpine MDO technology and provides high-barrier capabilities for consumer goods applications. | EcoLamHighPlus, EcoLam, EcoLamPlus |

| 5 | Sealed Air Corporation | North Carolina 28208, United States | United States | The company developed pouches for liquid and pumpable foods. The company manufactures pouches with high barrier properties and lowered polyamide content. | FlexPrep Dispensing Pouches, AUTOBAG SidePouch Bags, CRYOVAC VPP MonoPro, CRYOVAC Spout Pouches, CRYOVAC Recyclable Coffee Pouch |

By Pouch Type

By Thickness

By Closure Type

By Barrier Level

By Application

By End User

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarMono-material MDO-PE Pouch Market