Form-Fill-and-Seal Solution (FFS) Market Overview 2025 to 2035")

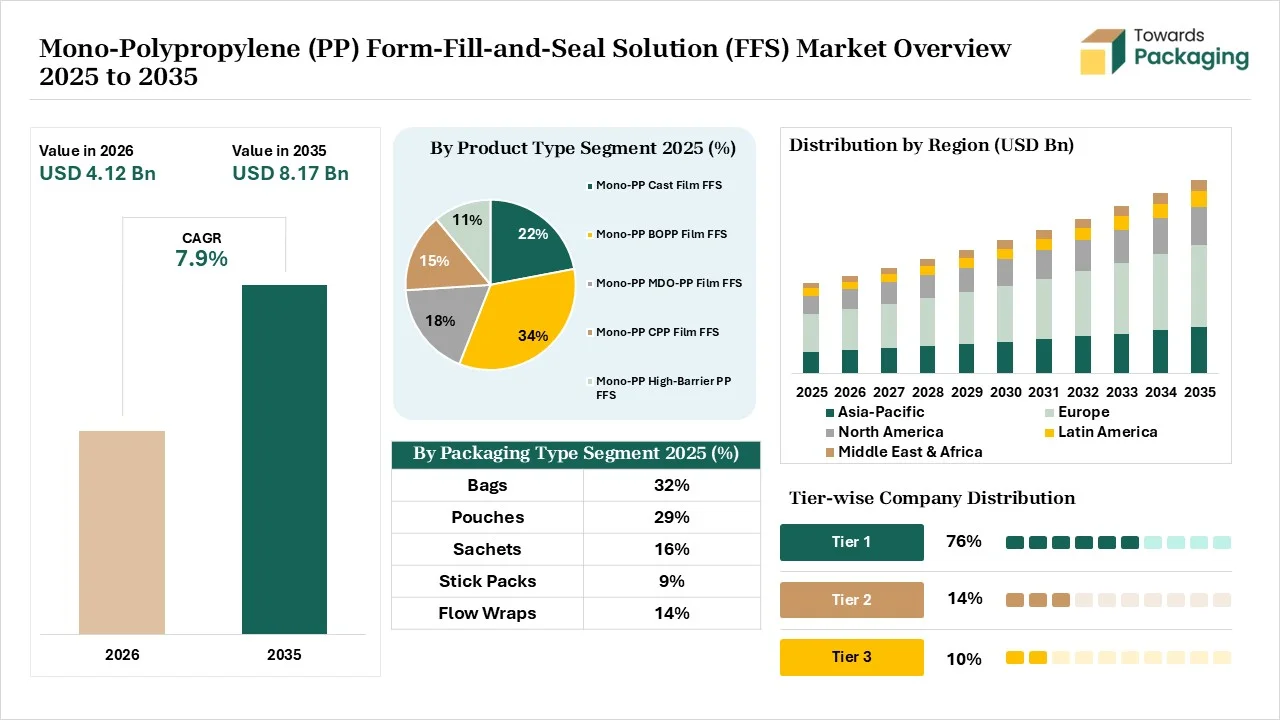

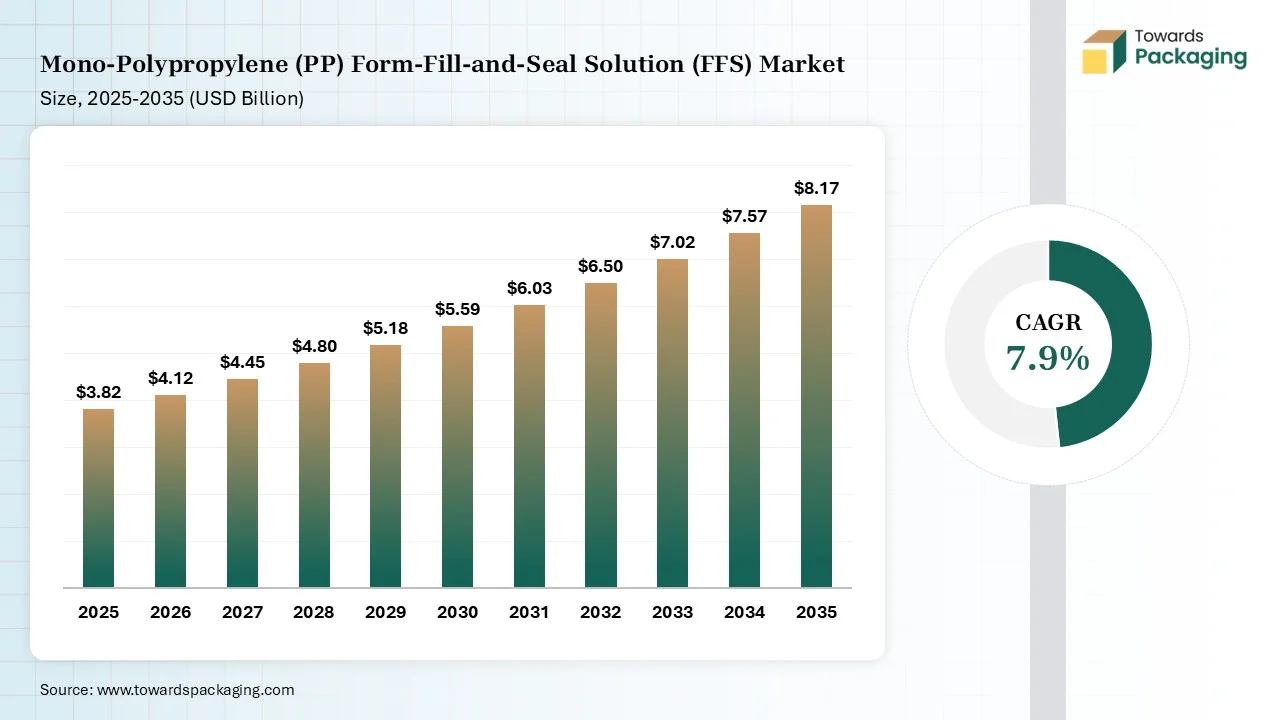

The mono-polypropylene (PP) form-fill-and-seal solution (FFS) market is projected to grow from USD 4.12 billion in 2026 to USD 8.17 billion by 2035, registering a CAGR of 7.9% during the forecast period. The report provides comprehensive coverage of market size, market share, growth trends, segment analysis, regional performance, competitive benchmarking, company profiles, value chain assessment, trade statistics, manufacturing analysis, supplier landscape, pricing trends, technological advancements, and future opportunities. Rising demand for recyclable packaging, regulatory pressure to reduce plastic waste, and increasing adoption of single-serve snack packaging are supporting market expansion across multiple industries.

Form-Fill-and-Seal Solution (FFS) Market Size 2025 to 2035")

Mono-polypropylene (PP) form-fill-and-seal (FFS) solution is a packaging system that uses a single material to seal and develop containers. The features of the mono-PP FFS solution are excellent barrier protection, sealing optimization, high recyclability, excellent mechanics, and down-gauging capabilities. It offers benefits like lightweight efficiency, high-speed machinability, and reduced carbon footprints. The simplified supply chain and product integrity are the main reasons to use the mono-PP FFS solution. Its applications are stationery, dry goods, wet wipes, pet food, hygiene products, and confectionery.

The mono-polypropylene (PP) form-fill-and-seal (FFS) solution market growth is driven by demand for excellent material performance, interest in seamless integration, booming RTE meals industry, rise in single-polymer packaging, popularity of hot-filled products, innovations in FFS technology, expansion of automated FFS, and rising polymer modifications.

The technological developments like predictive maintenance, integrated web tensioning, IoT, machine vision, and machine learning are driving the growth of mono-polypropylene form-fill-and-seal solution market. The brand sustainability goals and real-time defect detection are the main factors for the adoption of technological developments. AI is the major technological development that drives market growth.

AI adjusts sealing machine speeds and checks the integrity of the seal. AI detects misalignment and reduces unplanned stoppages. AI identifies incorrect barcodes and understands the purity standards of mono-PP FFS solution. AI easily inspects filling volumes and automates format changeovers. Overall, AI supports tackling material constraints, advanced recycling, and streamlining manufacturing planning.

The raw materials, such as barrier PP, oriented polypropylene, homopolymer PP, EVOH, cast polypropylene, and anti-block agents, are required.

Material processing includes steps like forming, filling, and sealing. The conversion involves co-extrusion, orientation, metallization, and inclusion of recycled content.

Package design focuses on barrier optimization, regulatory compliance, material synergy, and openability features. Prototyping focuses on forming, temperature management, and advanced sealing jaws.

The mono-PP BOPP film FFS segment dominated the market with 34% share in 2025 due to its compatibility with high-speed FFS. The focus on enhancing aroma retention of dry goods and protecting moisture-sensitive products increases the use of mono-PP BOPP film FFS. The focus on handling reverse printing and the need to preserve the crispness of diverse foods increases the use of mono-PP BOPP film FFS. The lightweighting, functional coatings integration, and unmatched recyclability of mono-PP BOPP film FFS drives the segment growth.

The mono-PP cast film FFS segment held the 22% market share in 2025 due to its consumer-friendly aesthetics. The advancements in polymer modifications and the growing demand for sterilized medical products increase the adoption of mono-PP cast film FFS. The rise of hot-fill processes and innovations in co-extrusion technology helps with expansion. The excellent heat resistance, high-speed sealability, and excellent gloss of mono-PP cast film FFS support the segment growth.

The bags segment dominated the market with 32% share in 2025 due to the increased storage of dry food products. The focus on preventing contamination in the dairy sector and the need to lower production downtime increase the use of mono-PP FFS bags. The shift away from cardboard boxes and the preservation of pet food increases the use of mono-PP FFS bags. The versatile design, excellent moisture barrier, and freight cost savings of mono-PP FFS bags drive the segment growth.

The pouches segment held the 29% market share in 2025 due to the rise in personal care refills. The focus on lowering polymer consumption and demand for single-material alternatives increases the use of mono-PP FFS pouches. The Gen-Z focus on portion-controlled and the convenience-food trends increases the use of mono-PP FFS pouches. The compatibility of pouches with FFS machinery and logistics optimization supports the segment growth.

The vertical form fill seal (VFFS) segment dominated the market with 68% share in 2025 due to its gravity-fed efficiency. The focus on precise tension management and the rising consumption of pourable foods increases the adoption of VFFS. The fewer mechanical failures, advanced sealing jaws, compact footprint, and lower initial outlay of VFFS help with expansion. The interest in dry snack foods and the massive food packaging operations drive the segment growth.

The horizontal form fill seal (HFFS) segment held the 32% market share in 2025 due to its use in snack applications. The prevention of deformation and flexible plastic streams increases the adoption of HFFS. The development of premium pouches and the need to maintain seal integrity increase the use of HFFS. The huge demand for flow wraps and the rise in doy-packs increase the adoption of HFFS, supporting the segment market.

The standard barrier segment dominated the market with 39% share in 2025 due to the expansion of dry food packaging. The focus on lowering the manufacturing cost of snack products and the advancements in monomaterials help with expansion. The solid waste reduction and the packaging circularity increase the use of mono-PP FFS solution. The use of standard barriers in short shelf-life products drives the segment growth.

The medium barrier segment held the 28% market share in 2025 due to the rise in microwavable packaging. The polymer innovations and the rigorous mechanical demand increase the use of medium barrier. The burgeoning retail requirements and the utilization of heat-resistant packaging increase the adoption of medium barrier. The surge in processed food and the retort capability of medium barrier supports the segment growth.

The 30-50 microns segment dominated the market with 41% share in 2025 due to its optimal machinability. The high-speed HFFS production lines and the focus on keeping out moisture increase the adoption of 30-50 microns. The growing pouch forming and the focus on keeping cookies fresh increase the use of 30-50 microns. The high machine compatibility, superior mechanical properties, perfect stiffness, and balanced performance of 30-50 microns drive the segment growth.

The 51-80 microns segment held the 28% market share in 2025 due to the growing use in packaging heavy goods. The elimination of complex recycling layers and industrial packaging increases the use of 51-80 microns. The integration of 51-80 microns with MDO film technology helps with expansion. The shipping efficiency, optimal stiffness, high-speed machinability, and better puncture resistance of 51-80 microns support the segment growth.

The food & beverage segment dominated the market with 46% share in 2025 due to the popularity of microwaveable meals. The F&B brands' transformation to mono-materials and the increased packaging of granular foods increase demand for mono-PP FFS solutions. The expansion of freezer-stored foods and the consumer interest in convenience foods increase the use of mono-PP FFS solutions. The protection of organoleptic properties of beverages drives the segment growth.

The pet food segment held the 12% market share in 2025 due to the growing demand for dry-kibble bags. The higher production volume of pet food and the focus on retaining the crunch of pet food increase the use of mono-PP FFS solutions. The need for retort sterilization in wet pet food and the expansion of premium pet segments increase the adoption of mono-PP FFS solution. The pet nutrition focus supports the segment growth.

The direct sales segment dominated the market with 44% share in 2025 due to the high preference for custom equipment. The need for expert engineers and the strict compliance regulations increases the use of direct sales. The complex retrofitting activities and the need for volume discounts increase the adoption of direct sales. The availability of continuous software updates and custom material tuning in direct sales drives the segment growth.

The packaging converters segment held the 31% market share in 2025 due to the simplified recycling streams. The focus on lowering eco-modulated taxes and the use of specialized coating increases the adoption of packaging converters. The development of advanced PP films and costly material separation processes increases the use of packaging converters. The high operational efficiency in packaging converters supports the segment growth.

Europe dominated the market with a 42% share in 2025 due to the availability of the EU plastic strategy. The plastic packaging tax and the specialized recycling infrastructure increase the adoption of the mono-PP FFS Solution. The presence of advanced film converters and the growing cleanliness needs in the pharmaceutical industry increase the adoption of mono-PP FFS solutions. The well-established machine manufacturers and the expanding dairy industry drive the market growth.

Germany

The use of sterile packaging in the healthcare industry and the presence of beverage manufacturers increase the adoption of mono-PP FFS solutions.

The regulations, like Verpackungsgesetz and mono-PP compatibility with existing polyolefin recycling streams, help with expansion.

Italy

The machinery expertise and the vast export-based beverage industry increase demand for mono-PP FFS solution.

The well-established presence of flexible packaging machinery and the large microwaveable food sector increases the adoption of mono-PP FFS solution.

Asia Pacific held the 24% share of the market in 2025 due to the strong recycling mandates. The increased spending on online grocery deliveries and the high-speed automation capabilities increase the adoption of the mono-PP FFS solution. The higher need for contamination-free packaging in the healthcare sector and the shift away from complex multi-layer plastics increase demand for mono-PP FFS solution. The explosive consumer goods industry supports the segment growth.

China

India

North America held the 20% share of the market in 2025 due to the growing benefits of using mono-materials. The expansion of meal-kit services and the focus on preventing food deterioration increase the adoption of mono-PP FFS solution. The burgeoning consumption of on-the-go snacks and the need to maintain the integrity of the cold chain increase the use of mono-PP FFS. The surging automated machinery supports the market growth.

United States

Canada

Latin America held the 8% share of the market in 2025 due to the growing agricultural exports. The cost-efficiency of automated processing and the consumption of ambient dairy foods increase demand for mono-PP FFS solutions. The presence of food producers and the focus on preserving goods increase the use of mono-PP FFS solutions. The rising use of flexible packaging across diverse industrial bases boosts the segment growth.

Brazil

Argentina

The Middle East & Africa held the 6% share in the market in 2025 and is expected to grow at the fastest CAGR of 9.8% during the forecast period due to the strong presence of juice processors. The growing working demographics and the shift away from complex multilayer barrier films increase the use of FFS pouches for the packaging of diverse items. The rising shipping of specialty pharmaceuticals and the abundance of resins increase the production of mono-PP FFS solution. The burgeoning demand for packaged snacks supports the overall market growth.

Saudi Arabia

United Arab Emirates

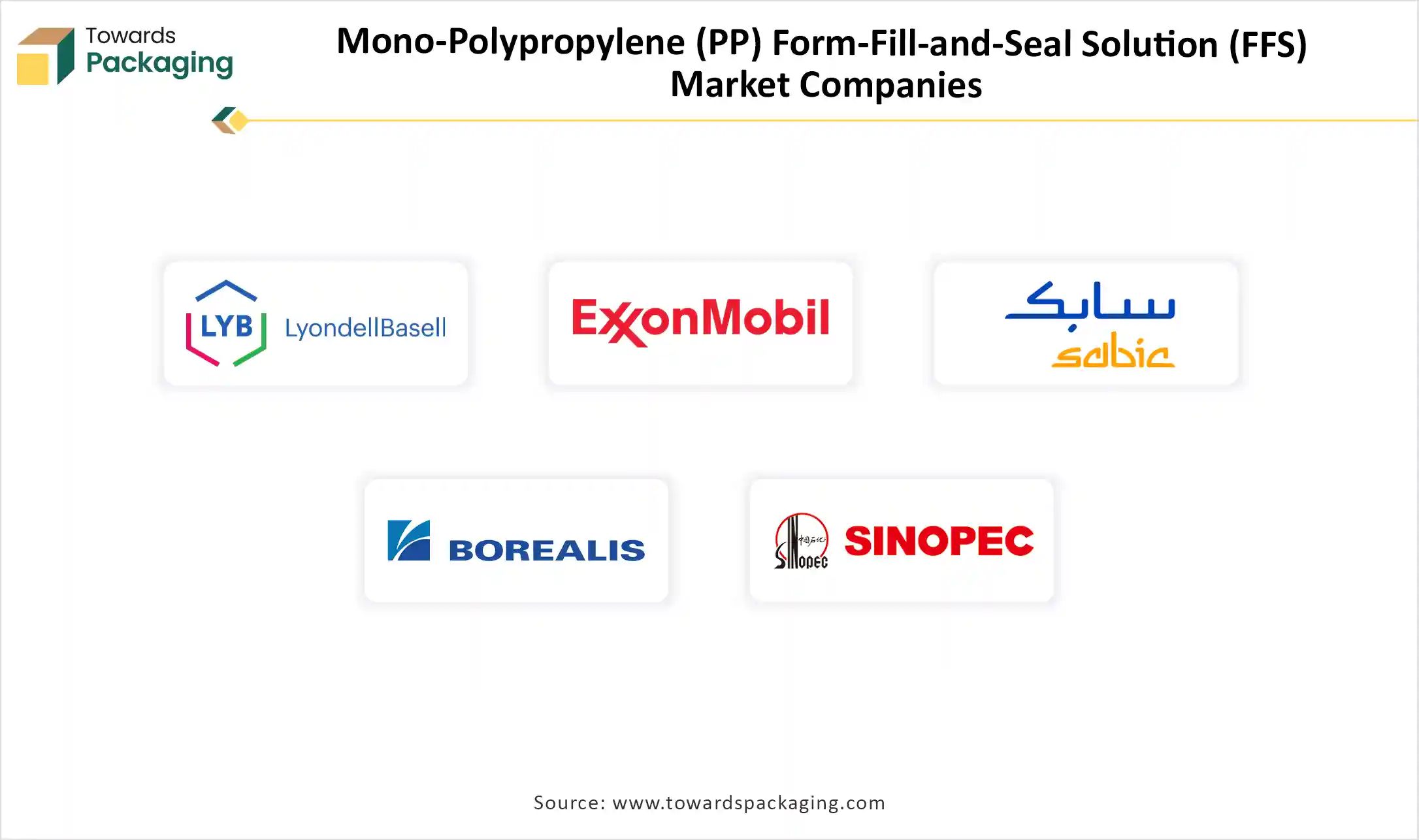

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products and Services |

| 1. | LyondellBasell | Netherlands | Netherlands | The company focuses on the development of specialty resins and supports sustainability integration. | Adflex, Clyrell, Adsyl, Moplen, Adstif |

| 2. | ExxonMobil Corporation | Spring, Texas, USA | United States | The company focuses on value-chain collaborations and high-speed machinability. | Exceed High Performance PP, Vistamaxx Performance Polymers, Oppera Modifiers, ExxonMobil PP |

| 3. | SABIC | Riyadh, Saudi Arabia | Saudi Arabia | The company focuses on material reduction and supports high-speed FFS processability. | SABIC PP 622L Resin, SABIC PP-UMS, SABIC BOPP Polymers, SABIC QRYSTAL PP |

| 4. | Borealis AG | Vienna, Austria | Austria | The company uses Borstar Nextension technology to develop premium PP grades. | Borpact SH950MO, Borealis HC101BF & HC110BF, BorPure RE539MF, Borealis TD310BF |

| 5. | Sinopec | Beijing, China | China | The company offers heat-sealing capabilities and supplies specialty resins. | Homopolymer Polypropylene, Impact Copolymer Polypropylene, and Random Copolymer Polypropylene |

Form-Fill-and-Seal Solution (FFS) Market Companies")

By Product Type

By Packaging Format

By Machine Type

By Barrier Level

By Thickness

By End-Use Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarMono-Polypropylene (PP) Form-Fill-and-Seal Solution (FFS) Market