The packaging resin market is forecasted to expand from USD 292.98 billion in 2026 to USD 545.46 billion by 2035, growing at a CAGR of 7.15% from 2026 to 2035. This report covers full market segmentation by type (PP, LDPE, HDPE, PET, PVC, PS, EPS) and by application (F&B, consumer goods, healthcare, industrial) along with a comprehensive regional analysis across North America, Europe, Asia-Pacific, Latin America, and MEA.

The study highlights key trends such as sustainability, bioplastics adoption, circular economy growth, and rising demand from the food & beverage sector. Competitive insights include leading companies like BASF, SABIC, Sinopec, Dow, LyondellBasell, and others. It also provides value chain mapping, pricing factors, raw material supply trends, and global trade statistics, including Vietnam’s 75,354 PP-import shipments, China’s 141K tons of epoxide resin imports, and major exporters such as Vietnam, South Korea, and China.

The key players operating in the market are focused on adopting inorganic growth strategies like acquisition and merger to develop advance technology for manufacturing packaging resin which is estimated to drive the global packaging resin market over the forecast period.

The synthetic polymers utilized to develop packaging materials that are designed to protect, contain, and preserve products throughout their lifecycle is known as packaging resin. These resins are molded, extruded, or formed into various shapes and types of packaging, such as bags, films, bottles, trays, and containers, depending on the specific resin type and its intended utilization. The role of packaging resin in modern manufacturing and consumer goods is critical, as it allows safe storage, easy handling, transport, and enhanced shelf life of a wide variety of products.

There are several different types of packaging resins which have been mentioned here as follows: polyethylene, polypropylene, polyethylene terephthalate, polyvinyl chloride, polystyrene, polycarbonate and polyamide. Polylactic acid and polyhydroxyalkanoates are the biodegradable resins. Each of these resins has specific advantages that make them ideal for certain applications, such as protecting food from contamination, offering durability during transportation, or providing easy recyclability for sustainability.

AI is improving efficiency and yield in packaging resin production by enabling real-time monitoring and optimization of manufacturing processes. By automatically adjusting parameters like temperature, pressure, and feed rates, sophisticated algorithms reduce material waste and energy consumption by analyzing data from sensors, machinery, and production lines. AI-powered predictive analytics reduces downtime and enhances operational continuity by spotting possible equipment failures before they happen. Manufacturers benefit from increased output consistency, better resin quality, and increased production yields as a result.

For example, ExxonMobil has implemented AI-driven process optimization in its polyethylene and polypropylene production plants, which has enhanced operational efficiency, improved product consistency, and reduced energy consumption. As a result, manufacturers achieve higher output consistency, improved resin quality, and better overall production yields.

| Metric | Details |

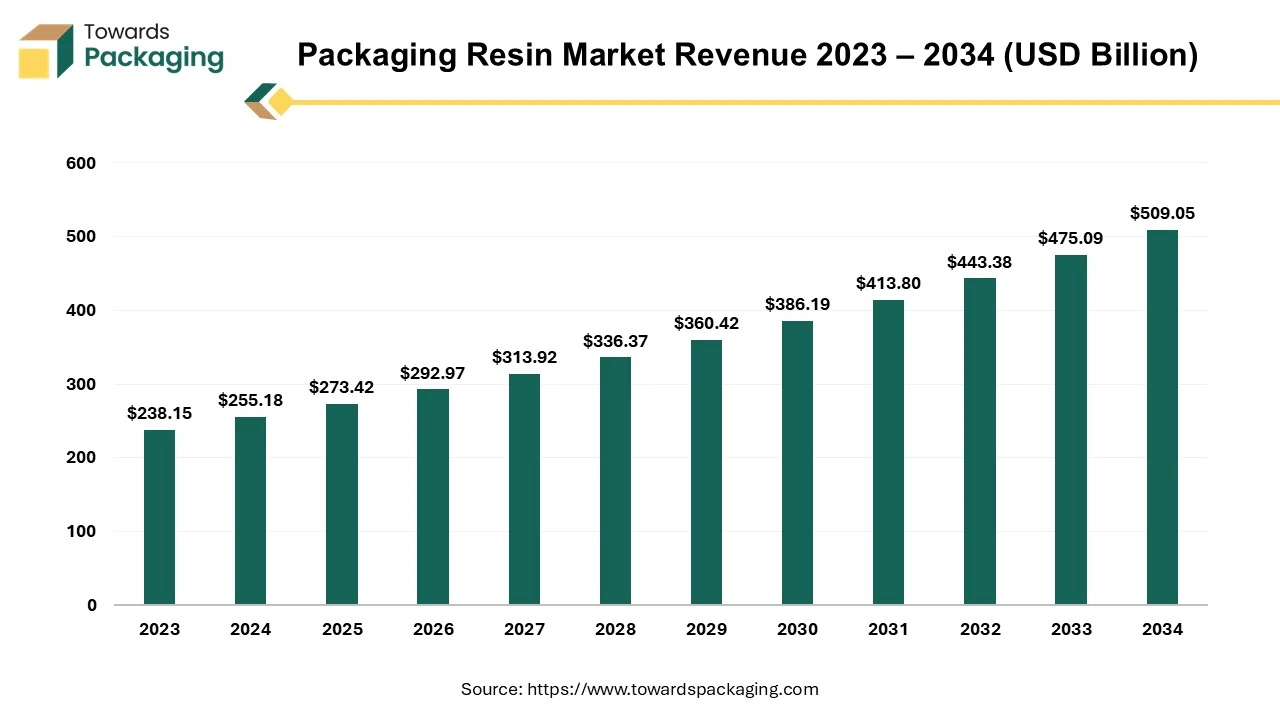

| Market Size in 2025 | US$ 273.43 billion |

| Projected Market Size in 2035 | US$ 545.46 Billion |

| CAGR (2026 - 2035) | 7.15% |

| Leading Region | Asia Pacific |

| Market Segmentation | By Type, By Application and By Region |

| Top Key Players | BASF SA, SABIC, China Petroleum & Chemical Corporation, LyondellBasell, Dow Chemical Company |

Due to busy lifestyle there is rise in demand of the packaged and ready-to-eat food. Packaging resins are integral to the food and beverage sector, where they ensure product safety, freshness, and extended shelf life. The growth of packaged food, convenience foods, and beverages (especially bottled drinks) is a significant driver. Increasing launch of the packaged and ready-to-eat food has risen the demand for the packaging resin, which is estimated to drive the growth of the packaging resin market in the near future.

Shift towards Biodegradable and Recyclable Materials: The demand for eco-friendly packaging solutions has been a dominant trend, driven by both regulatory pressures and consumer preference for sustainable products. Companies are increasingly using recyclable plastics, bioplastics, and compostable materials to reduce environmental impact. Increased Focus on Circular Economy: Packaging companies are investing in systems that allow for the recycling of materials like polyethylene terephthalate (PET) and polyethylene (PE). This includes developing packaging that can be easily sorted, reused, or recycled.

The development of high-performance resins, such as polyamide (PA), polycarbonate (PC), and ethylene vinyl alcohol (EVOH), is growing, especially for premium applications that require higher barrier properties (e.g., for food, pharmaceuticals, and electronics packaging). The demand for packaging resins in the pharmaceutical industry is growing due to the need for sterile, tamper-evident, and safe packaging for medicines and medical devices. The key players operating in the market are focused on carrying out research for developing packaging resin which will be suitable for packaging biologic and pharmaceutical products, which is estimated to create lucrative opportunity for the growth of the packaging resin market in the near future.

| Technological Shifts | Impact on Packaging Resin Market |

| AI & Machine Learning | Enhances production efficiency, reduces waste, and ensures consistent resin quality |

| Advanced Recycling Technologies | Promotes circular economy by enabling high-quality resin reuse |

| Bio-based Resin Innovation | Supports sustainable packaging and reduces reliance on fossil fuels |

| Process Automation & IoT | Minimizes downtime, lowers operational costs, and improves production precision |

| Lightweighting Technologies | Reduces material usage and transportation costs while maintaining performance |

| Barrier Enhancement Technologies | Extends product shelf life, especially for food and pharmaceuticals |

The key players operating in the market are facing issue in fulling the consumer demand due to high cost of raw material and regulatory rules, which is observed to hamper the growth of the packaging resin market in the near future. The cost of key raw materials, such as crude oil and natural gas, which are used to produce resins like polyethylene (PE) and polypropylene (PP), can be volatile. This makes price stability a challenge for manufacturers and can lead to unpredictable costs. The global resin market is often affected by supply chain issues, such as the availability of feedstock materials or disruptions from natural disasters or geopolitical tensions. These factors can impact production timelines, lead to shortages, and raise costs. With the rise of alternative materials like paper, glass, and aluminum, especially in food and beverage packaging, there is growing competition for market share. While resins remain a popular choice, alternatives that promise lower environmental impacts are increasingly attractive to both consumers and brands.

| Rank | Company | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Dow | Midland, Michigan | USA | Global leader in packaging resins with extensive PE, specialty polymers, and recycle-ready packaging innovations | Packaging-grade PE, sealant resins, specialty packaging materials |

| 2 | LyondellBasell | Houston, Texas | USA | One of the world's largest polyolefin producers supplying packaging-grade PE and PP resins | HDPE, LDPE, LLDPE, PP packaging resins |

| 3 | SABIC | Riyadh | Saudi Arabia | Major global supplier of packaging polymers with strong sustainability portfolio | PE, PP, PET, recycled polymers |

| 4 | INEOS | London, England | United Kingdom | Leading producer of polyolefins and packaging resins with global manufacturing footprint | Polyethylene and polypropylene packaging resins |

| 5 | Borealis | Vienna | Austria | Recognized leader in advanced polyolefins and circular packaging materials | PE, PP, recyclable packaging resins |

| Rank | Company | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | ExxonMobil | Spring, Texas | USA | Major supplier of polyethylene resins for flexible and rigid packaging | PE packaging resins |

| 2 | Chevron Phillips Chemical | The Woodlands, Texas | USA | Significant producer of HDPE and LLDPE resins for packaging applications | HDPE, LLDPE packaging resins |

| 3 | Braskem | São Paulo | Brazil | Global supplier of polyolefins and bio-based polyethylene | Bio-based PE, PP resins |

| 4 | Eastman | Kingsport, Tennessee | USA | Producer of specialty copolyesters and circular packaging materials | Copolyesters, recycled-content resins |

| 5 | Mitsubishi Chemical Group | Tokyo | Japan | Manufactures engineering and barrier resins used in packaging | Specialty packaging polymers, EVOH-related materials |

| Rank | Company | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | PureCycle Technologies | Orlando, Florida | USA | Commercial producer of ultra-pure recycled polypropylene for packaging | Recycled PP resins |

| 2 | Avient | Avon Lake, Ohio | USA | Develops specialty compounds and color solutions for packaging resins | Polymer compounds and additives |

| 3 | Kuraray | Tokyo | Japan | Leading supplier of EVOH barrier resins for food packaging | EVOH barrier resins |

| 4 | SK Chemicals | Seongnam | South Korea | Producer of recycled PET and specialty copolyesters for packaging | Recycled PET, copolyester resins |

| 5 | NatureWorks | Plymouth, Minnesota | USA | Leading producer of PLA biopolymers for sustainable packaging | PLA packaging resins |

Asia Pacific region dominated the global packaging resin market in 2023. After the Covid-19 breakout in China the innovation and introduction of vaccines increased in Asia Pacific region which has observed to rise the growth of the packaging resin. APAC is becoming a key hub for biopharmaceutical manufacturing. As the biopharmaceutical sector grows, it creates a demand for advanced packaging solutions, such as multilayered films and specialized containers to protect biologic drugs. These packaging needs often rely on high-performance packaging resins to meet specific storage and transportation requirements, supporting packaging resin market growth.

Asia Pacific region is an increasingly important market for global pharmaceutical companies, with increasing exports and the distribution of medicines across multiple countries. To meet these consumer needs, pharmaceutical products require packaging that can withstand long transit times and varying environmental conditions. Resins that provide better barrier properties, moisture resistance, and temperature stability are in high demand, driving growth in the packaging resin market over the course of period.

Hence, rapid industrialization and well established pharma sector of Asia Pacific region has driven the growth of the packaging resin market

North America region is anticipated to grow at the fastest rate in the packaging resin market during the forecast period. North America, particularly the United States and Canada, has a large and diverse consumer base. With high disposable income, a growing middle class, and a large population, there is a consistent demand for a wide variety of food and beverage products. This provides a strong market for companies to establish and expand their businesses. The food and beverage industry in North America is known for its continuous innovation, from the development of new flavors and product categories to the incorporation of new technologies (e.g., plant-based foods, clean-label products, and functional foods).

The region’s cultural diversity has fostered a wide range of tastes and dietary preferences, encouraging food and beverage companies to offer an extensive variety of products to cater to different consumer needs. From fast food and packaged snacks to organic and health-conscious food, the demand for varied products allows businesses to establish themselves across many niches. Hence, the well-established food and beverages industry in the North America region drives the growth of the packaging resin market in the near future.

Polypropylene (PP) segment held a dominant presence in the packaging resin market in 2025. Polypropylene (PP) has good tensile strength and is resistant to impact, making it an ideal choice for packaging that needs to protect the contents during handling and transportation. It can withstand stress without cracking or breaking easily. Polypropylene is resistant to many chemicals, oils, and solvents, which helps preserve the quality of food and other consumer goods. This property makes it suitable for packaging a wide range of products, from food and beverages to household cleaners. Polypropylene (PP) can be easily recycled, has heat resistance properties, chemical resistance properties, has transparency and clarity.

Food & Beverage segment registered its dominance over the global packaging resin market in 2025. As consumers seek convenience, there is a more demand for on-the-go, ready-to-eat, and easy-to-prepare food and beverage packets. Packaging resins like polyethylene (PE), PET, and polypropylene (PP) are essential for creating packaging solutions that ensure products remain fresh, portable, and easy to use. Packaging resins, especially those with barrier properties (such as PET and multi-layer films), help extend the shelf life of food and beverages by protecting against moisture, oxygen, light, and contaminants.

This extends the freshness of products, reduces food waste, and meets consumer expectations for product quality and safety. Growing consumer and regulatory pressure for sustainability is driving demand for packaging materials that are either recyclable or made from renewable sources. Resins like PET and those used in biodegradable or compostable packaging are gaining popularity due to their reduced environmental impact. This trend aligns with the industry's shift toward eco-friendlier packaging options.

High-density polyethylene (HDPE) is the fastest-growing segment in the packaging resin market, driven by its chemical resistance, high strength-to-density ratio, and recyclable nature. Bottles, containers, and caps are just a few examples of the rigid packaging applications that frequently use it. The use of HDPE in food, beverage, and household product packaging is accelerated by the growing demand for lightweight long lasting and environmentally friendly packaging options.

Consumers goods segment is the fastest-growing end-use category in the packaging resin market, backed by rising consumer demand for lifestyle home care and packaged personal care products. The demand for appealing, safe, and practical packaging is driven by the rapid urbanization and expansion of e-commerce and the shifting lifestyles of consumers. Advanced and recyclable resins are being used by manufacturers more frequently to meet sustainability standards and improve shelf appeal

Packaging resins rely on petrochemical feedstocks, bio-based polymers, and recycled materials. Ensuring a stable supply and quality of raw materials is critical for consistent production and cost management.

Efficient logistics and distribution are essential for the timely delivery of resins to manufacturers and converters. Supply chain optimization, temperature-controlled transport, and strategic warehousing help maintain quality and reduce costs.

Recycling and waste management involve the collection, sorting, and reprocessing of post-consumer and post-industrial resins. Adoption of chemical and mechanical recycling is increasing to meet sustainability goals and regulatory compliance.

By Type

By Application

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPackaging Resin Market