Dip Cups Packaging Market Overview 2025 to 2035")

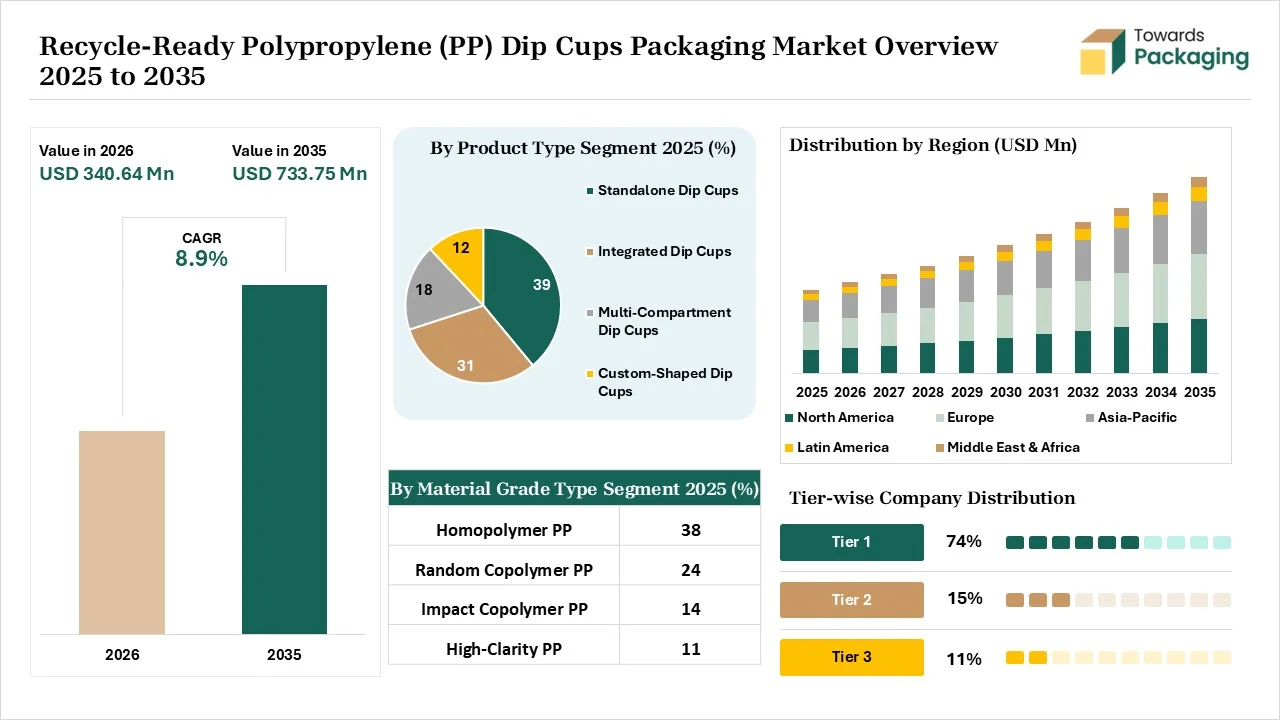

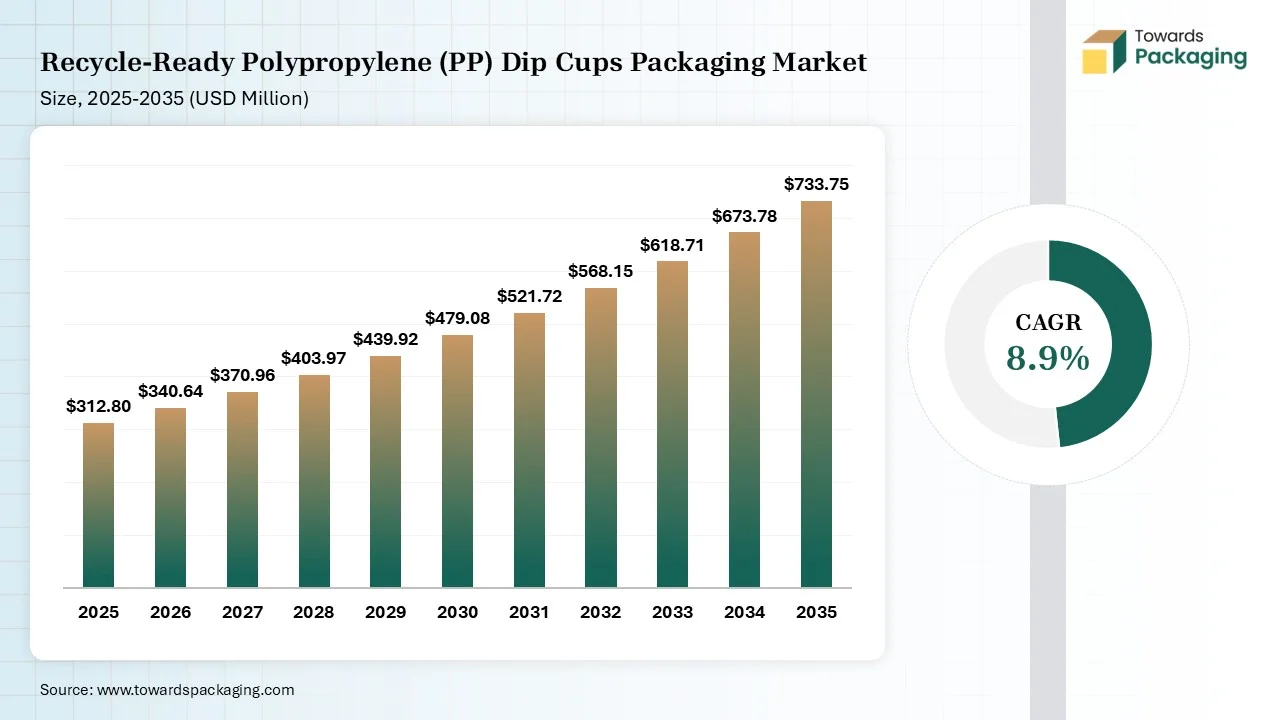

The recycle-ready polypropylene (PP) dip cups packaging market is projected to grow from USD 340.64 million in 2026 to USD 733.75 million by 2035, registering a CAGR of 8.9% during the forecast period. The market report provides comprehensive coverage of market size, revenue forecasts, segment analysis by capacity, closure type, end-use industry, and distribution channel, along with detailed regional demand assessments. The study also includes competitive analysis, company market shares, value chain evaluation, trade statistics, pricing trends, production and consumption analysis, and extensive profiles of manufacturers, converters, suppliers, and packaging solution providers operating across the global market.

Dip Cups Packaging Market Size 2025 to 2035")

Recycle-ready polypropylene dip cups are eco-friendly food containers made from mono-material. They offer features like high performance, consumer convenience, food safety, eco-friendliness, operational efficiency, and customizability. They provide benefits like exceptional food protection, operational efficiency, eco-friendly sustainability, and durability. They offer mono-substrate compatibility, single-stream recyclability, and strong visual branding. They are used in applications like condiments, dips, sauces, spreads, and salad dressings.

The recycle-ready polypropylene dip cups packaging market growth is driven by the enforcement of regulations on plastic waste, growth in packaging leaders, focus on sustainability values in the food industry, presence of major dairy brands, interest in polypropylene cups, growing takeout dining, and the ongoing advancements in chemical recycling infrastructure.

Technological developments like computer vision, advanced intelligent packaging, robotic sourcing, and machine learning are happening in the recycle-ready polypropylene dip cups market. Technological developments driven by demand for replacing traditional polystyrene and improving barrier technology. The major development is the artificial intelligence technology. AI helps in automatic recovery and optimizing packaging design.

AI easily separates food-grade plastics and eliminates the requirement for manual sorting. AI detects hazardous contaminants and identifies different material blends. AI verifies the sustainability of packaging and easily achieves sorting purities. AI understands design variations and identifies specific product types. Overall, AI supports end-of-line education and high-precision sorting.

The stage acquires raw materials like monosubstrate lidding, virgin polypropylene, and recycled polypropylene.

Material processing involves polymerization, additive blending, and pelletizing. The conversion includes thermoforming, mono-material design, and lidding integration.

Package Design focuses on base resin, barrier layers, and lidding. Prototyping focuses on manufacturing compatibility, structural testing, and seal integrity.

The medium capacity segment dominated the market with 46% share in 2025 due to its suitability in standard single-serve condiments. The expansion of delivery-first brands and the protection of moisture-barrier integrity increase the use of medium capacity. The growing on-the-go food applications and the stringent design guidelines increase the adoption of medium capacity. The seamless scalability and optimal portion control of medium capacity drives the segment growth.

The small capacity segment held the 34% market share in 2025 due to the high use in food delivery services. The high demand for dressings and the need to minimize spillage increase the use of small capacity. The focus on limiting condiment usage and the higher national recycling initiatives increases the adoption of small capacity. The smaller carbon footprints, cost efficiency, and operational compatibility of small capacity support the segment growth.

The standalone dip cups segment dominated the market with 39% share in 2025 due to its high recyclability ratings. The high compatibility with dairy filling equipment helps with expansion. The growth in the portion-control market and the thriving food industry increases the use of standalone dip cups. The protection of sauces and the growing convenience sector increase the adoption of standalone dip cups. The growing technology integration with standalone dip cups drives the segment growth.

The integrated dip cups segment held the 31% market share in 2025 due to the higher EPR penalties. The expansion of size-sorting recycling and the restrictions on multi-layered plastics increase the adoption of integrated dip cups. The expansion of takeaway orders and the rise in sauce packaging increase the use of integrated dip cups. The focus on avoiding messy spills and the development of hot condiments increases the use of integrated dip cups, supporting the overall segment growth.

The homopolymer PP segment dominated the market with 38% share in 2025 due to the growing use in heated foodservice. The consumption of heavy sauces and the creation of circular packaging increase the use of homopolymer PP. The interest in food-grade plastics and the rise in microwave sterilization increase the use of homopolymer PP. The superior rigidity, low density, seamless recyclability, and high heat resistance of homopolymer PP drive the segment growth.

The random copolymer PP segment held the 24% market share in 2025 due to the polystyrene replacement. The focus on easy plastic sorting and the rise in refrigerating dips increases the use of random copolymer PP. The expansion of packaging converters and the demand for sustainable cups increases the use of random copolymer PP. The enhanced material performance, high gloss, and seamless operations of random copolymer PP support the segment growth.

The standard recycle-ready PP segment dominated the market with 42% share in 2025 due to the evolving EPR rules. The growing use of recycle-ready PP in food manufacturing and the growing dressing activities increase the use of standard recycle-ready PP. The high consumer acceptance, excellent functional performance, minimal chemical leaching, regulatory alignment, and hot-fill compatibility of standard recycle-ready PP drives the segment growth.

The high moisture barrier PP segment held the 18% market share in 2025 due to the used in oil-based sauces. The expansion of packaging manufacturers and the preservation of sauce flavor increases the adoption of high moisture barrier PP. The growing single-substrate construction in packaging companies increases the use of high moisture barrier PP. The preservation of moisture-sensitive foods supports the segment growth.

The snap-fit lid segment dominated the market with 41% share in 2025 due to the prevention of messy spills. The growing microwaveable reheating of foods and the rise in food transportation increase demand for snap-fit lids. The focus on enhancing sorting potential and the need to eliminate the use of auxiliary locking components increase the adoption of the snap-fit lid. The cost-effective design and excellent leak-tolerance of the snap-fit lid drive the segment growth.

The peelable seal segment held the 18% market share in 2025 due to its compatibility with industrial recycling facilities. The consumer focus on hygiene and need for contamination protection increases the use of peelable seals. The expanded automated filling lines increase the production of peelable seals. The smooth opening, excellent product quality, and delivery-safe integrity of peelable seal support the segment growth.

The injection molding segment dominated the market with 57% share in 2025 due to its ability to provide uniform wall thickness. The development of mono-material cups and the focus on crack prevention during transportation increase the use of injection molding. The creation of a precise rim dimension and the focus on lowering secondary adhesive use increase the adoption of injection molding. The integration of IML technology with injection-molded products drives the segment growth.

The thermoforming segment held the 28% market share in 2025, due to its seamless integration with production equipment. The rise in production of PP labels and the changing global legislation increase the use of thermoforming. The massive foodservice supplies and the higher demand for heat-resistant solutions increase the adoption of thermoforming. The high performance, design versatility, and exceptional sustainability of thermoforming support the segment growth.

The foodservice segment dominated the market with 49% share in 2025 due to the expansion of drive-thru services. The leak prevention of saucy foods and the strong foodservice operators increase the adoption of recycle-ready PP dip cup packaging. The transition to eco-friendly foodservice and the thriving on-the-go dining increases the use of recycle-ready PP dip cup packaging. The presence of high-speed restaurants drives the segment growth.

The food processing segment held the 28% market share in 2025 due to the growing packaged food manufacturing. The rise in high-performance food processing and the focus on food freshness increases the use of recycle-ready PP dip cup packaging. The development of shelf-ready products and the rise in PFAS-free packaging in food processing support the segment growth.

The sauces segment dominated the market with 22% share in 2025 due to the rise in oily sauces. The development of sauces in the food industry and the precise sizes of sauces increases the use of recycle-ready dip cup packaging. The growing takeaway of sauce cups and the high consumption ratings of sauces increase the use of recycle-ready dip cup packaging. The standardized packaging of sauces supports the segment growth.

The ketchup & tomato-based condiments segment held the 18% market share in 2025 due to the high availability in QSRs. The growing delivery platforms and the continued growth in fast food consumption increase the adoption of recycle-ready dip cup packaging. The rise in portion-controlled servings of ketchups & tomato-based condiments helps with expansion. The burgeoning fast-food location supports the segment growth.

The direct sales segment dominated the market with 44% share in 2025 due to its reduced compliance fees. The focus on avoiding third-party markups and the demand for custom-printed lids increase the use of direct sales. The availability of safety certifications and the focus on training staff increase the use of direct sales. The direct vendor-to-client relationships and B2B bulk requirements drive the segment growth.

The packaging distributors segment held the 27% market share in 2025 due to its ability to ensure compliance guarantees. The massive demand for recycle-ready PP dip cup packaging and localized inventory increases buying from packaging distributors. The high accessibility for packaging solutions and the demand for highly circular solutions increase the adoption of packaging distributors, supporting the market growth.

Europe dominated the market with a 33% share in 2025 due to the European Circular Economy Action Plan. The presence of automated recycling facilities and the rise in food-safety innovations increase the adoption of recycle-ready PP dip cup packaging. The strong collection infrastructure and the food processors' focus on meeting recycled-content mandates increase the use of recycled-ready PP dip cup packaging. The mature waste ecosystem drives the market growth.

North America held the 28% market share in 2025 due to the massive sustainability goals. The corporate innovation and the rise in eco-friendly brands increase the use of recycle-ready PP dip cup packaging. The domestic bans on packaging waste and the rise in single-serve condiments increase the adoption of recycle-ready PP dip cup packaging. The improved recycling base supports the segment's overall growth.

Asia Pacific held the 27% market share in 2025 and is expected to grow at the fastest CAGR of 10.6% during the forecast period due to the anti-plastic waste laws. The presence of multinational fast food brands and hygiene regulations increases the use of recycle-ready PP dip cup packaging. The AI sorting integration and the growth in condiment consumption help with expansion. The government bans overpacking, & abundant PP recycling facilities drives the segment growth.

Latin America held the 7% market share in 2025 due to the expansion of on-the-go snacking options. The high consumption of cold dips and the major resin producers increase the adoption of recycle-ready PP dip cups packaging. The expansion of grab-and-go meals and the polystyrene phase-out increases the adoption of recycle-ready PP dip cup packaging. The stabilized supply chains for PP support the segment growth.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products and Services |

| 1. | Amcor | Zurich, Switzerland | Switzerland | The company supports achieving recyclability claims and offers manufacturing equipment. | PP Revolution Platform and EZ Peel Lidding |

| 2. | Berry Global Group | Evansville, Indiana, United States | United States | The company integrates PCR content in food-service containers and focuses on material lightweighting | Standard Dip Cups, Deli Containers, and Portion Cups |

| 3. | Sealed Air Corporation | Charlotte, North Carolina, United States | United States | The company manufactures PP films to serve sectors like foodservice and food. | CRYOVAC VPP MonoPro and CRYOVAC Brand Polypropylene Pots & Trays |

| 4. | Mondi Group | Weybridge, England | England | The company offers advanced sorting facilities and integrates recycling content in packaging. | Re/loop FlowWrap, re/cycle EnvelopeForm, and Mono-Material Thermoforming Films |

| 5. | Dart Container Corporation | Mason, Michigan | Michigan | The company offers portion cups and dip cups to serve various sectors. | Conex Complements Polypropylene Portion Containers Portfolio |

Dip Cups Packaging Market Companies")

By Capacity

By Product Type

By Material Grade

By Barrier & Functional Property

By Closure Type

By Manufacturing Process

By End Use Industry

By Application

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarRecycle-Ready Polypropylene (PP) Dip Cups Packaging Market