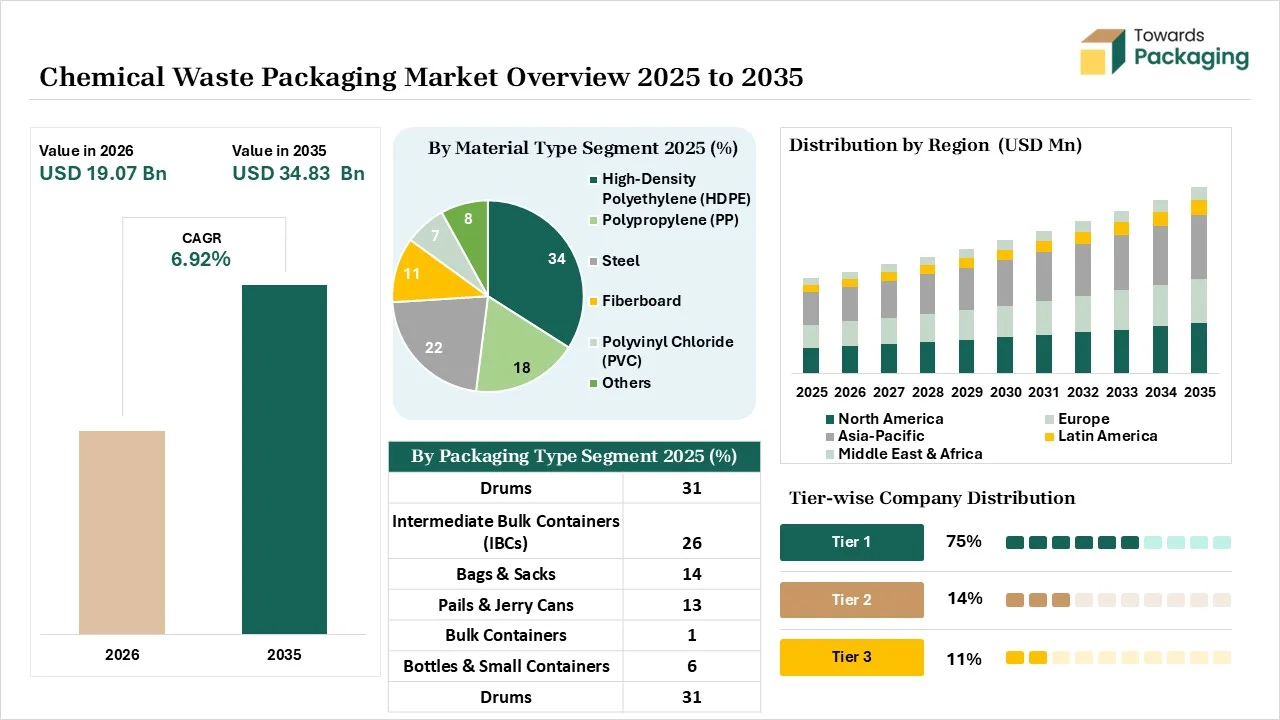

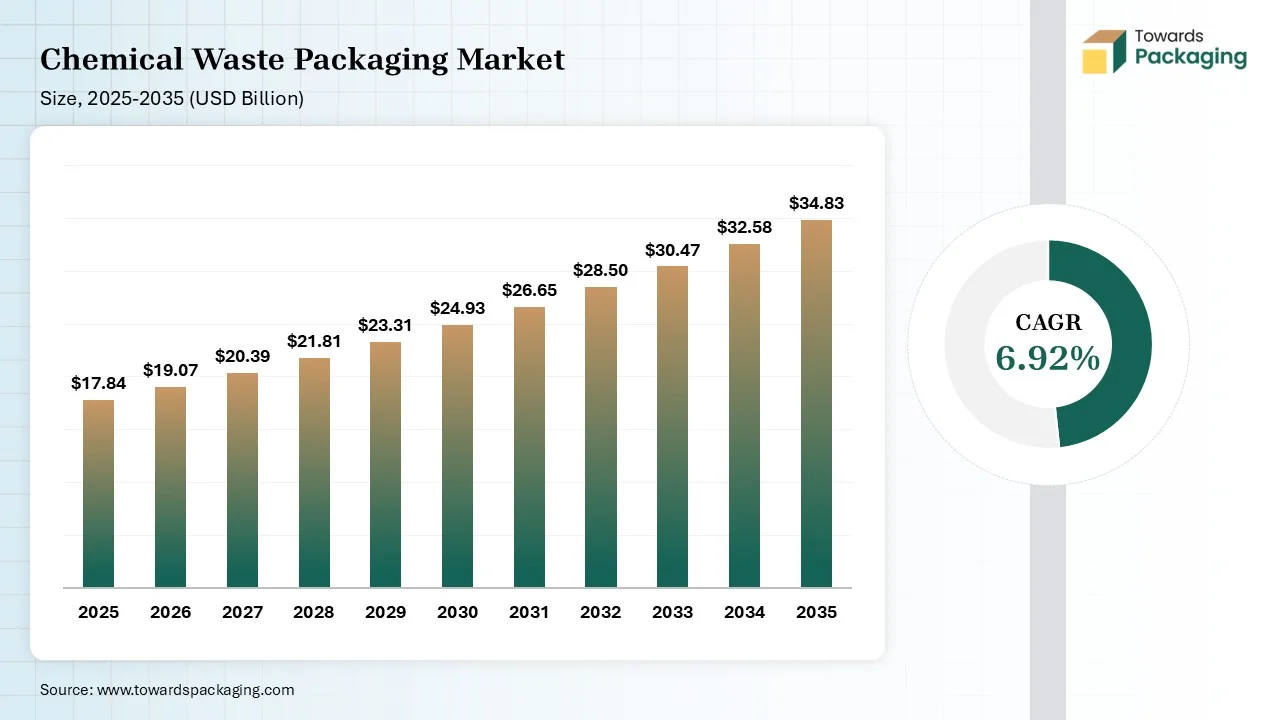

The Chemical Waste Packaging Market is projected to grow from USD 19.07 billion in 2026 to USD 34.83 billion by 2035, registering a CAGR of 6.92% during the forecast period. The report covers market size, share, growth trends, segment analysis, regional insights, competitive analysis, company profiles, manufacturer and supplier assessment, value chain analysis, trade statistics, pricing trends, regulatory developments, and future growth opportunities across key global markets.

Market Size (2025):- USD 17.84 Billion

Revenue CAGR (2025–2035):- 6.92%

Market Volume (2025):- 9.63 Million Tons

Volume CAGR (2025–2035):- 5.88%

Chemical waste packaging is the process of safe labeling, containing, and segregating toxic chemical byproducts for short-term disposal and storage. The key functionalities are tamper-evidence, reactivity prevention, and chemical compatibility. It offers benefits like environmental protection, streamlined waste disposal, workplace safety, and resource recovery. The key components include vapor expansion space, tight closures, HDPE, segregation product, and labelling. The various types of chemical waste are solid chemical waste, bulk chemical waste, liquid chemical waste, and contaminated waste. Chemical waste packaging includes rigid IBCs, heavy-duty polyethylene bags, IBCs, open head drums, woven sacks, hopper containers, polyethylene drums, and many more.

The chemical waste packaging market growth is driven by the interest in corrosion-resistant packaging, the manufacturing of agrochemicals, rising investment in reusable raw materials, high volume of hazardous waste, rising interest in smart packaging, growing international mandates for hazardous chemicals, high chemical consumption, and innovation in packaging technology.

The chemical waste packaging industry is seeing major tech-driven development in response to growing demand for digital traceability, smart tracking, sustainable materials, and regulatory compliance. Technological developments like IoT sensors integration, embedded sensors, blockchain, and smart tracking systems help in real-time monitoring and preventing accidental spills. The most prominent advancement in the market is the adoption of artificial intelligence.

AI identifies eco-friendly packaging solutions and maintains the chemical waste integrity. AI automates the documentation process and identifies cost-effective raw materials. AI prevents accidental leaks and provides fuel-efficient routes for the transportation of hazardous material. AI predicts the hazardous chemical reactions during transportation and provides accurate material combinations for the development of chemical waste packaging. Overall, AI helps in route optimization, automated sorting, and material optimization.

Raw materials like polypropylene, glass, fluoropolymers, steel, HDPE, galvanized iron, stainless steel, and specialized epoxy phenolic linings are required.

The material processing involves steps like assessment, segregation, packaging, labeling, and transportation. Conversion includes methods like thermochemical conversion, depolymerization, upcycling, direct chemical treatment, and solvolysis.

Package design involves steps like hazard analysis, selection of UN-approved packaging, absorption, secure closure, and clear labelling. Prototyping includes requirement analysis, material selection, structural design, safety testing, labelling, iteration, and production validation.

The major industrial players contribute to the growth of the chemical waste packaging market. Amcor plc company majorly invested in chemical recycling technology and integrates chemically recycled content in its packaging options. Berry Global Group uses PCR plastics in the packaging and heavily invests in advanced resins for toxic chemical applications. Sealed Air Corporation uses digital tracking for monitoring temperature and other factors during transportation.

Mauser Packaging Solutions & Greif, Inc. manufactures heavy-duty sacks, UN-certified drums, and IBCs, as well as company focuses on expanding reconditioning services. Clean Harbors company provides initiatives like the CustomPack Self-Pack Program, which offers a cost-effective packaging alternative to customers for waste chemicals. The initiative manages final transportation and supplies UN-approved packaging materials.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Mauser Packaging Solutions | Oak Brook, Illinois | USA | Global leader in industrial and hazardous materials packaging with extensive UN-certified product portfolio | Drums, IBCs, hazardous waste containers, reconditioning services |

| 2 | Greif | Delaware, Ohio | USA | One of the world's largest industrial packaging suppliers serving chemical and waste sectors | Steel drums, plastic drums, IBCs, bulk packaging |

| 3 | SCHÜTZ | Selters | Germany | Global leader in IBC solutions for hazardous chemicals and waste transportation | ECOBULK IBCs, industrial packaging systems |

| 4 | Time Technoplast | Mumbai, Maharashtra | India | Major producer of industrial packaging and composite IBCs for chemicals | Polymer drums, IBCs, hazardous goods packaging |

| 5 | Berry Global | Evansville, Indiana | USA | Significant supplier of industrial containers and specialty chemical packaging solutions | Chemical containers, hazardous material packaging |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Balmer Lawrie | Kolkata, West Bengal | India | Major steel drum and industrial packaging supplier serving chemical industries | Steel drums and industrial containers |

| 2 | Sicagen India | Chennai, Tamil Nadu | India | Producer of UN-certified industrial packaging solutions | Drums and hazardous material containers |

| 3 | Müller Group | Rheinfelden | Germany | Specialist in hazardous materials packaging and pharmaceutical containers | Stainless steel drums and containers |

| 4 | CurTec | Rijen | Netherlands | Supplier of high-performance packaging for chemicals and hazardous goods | Plastic drums and specialty containers |

| 5 | AST Plastic Containers | Houston, Texas | USA | Industrial packaging provider focused on chemical handling | Chemical drums and containers |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Snyder Industries | Lincoln, Nebraska | USA | Manufacturer of industrial chemical storage and transport containers | Chemical tanks and containers |

| 2 | Denios | Bad Oeynhausen | Germany | Specialist in hazardous substance storage and containment solutions | Hazardous waste containers |

| 3 | Thielmann | Granada | Spain | Producer of industrial containers for chemical transport and storage | Stainless steel containers |

| 4 | Pensteel | Singapore | Singapore | Supplier of industrial steel drums for chemical waste handling | Steel drums and industrial packaging |

| 5 | EnviroTain | Phoenix, Arizona | USA | Specialized hazardous waste packaging provider | Waste containment systems |

The high-density polyethylene (HDPE) segment dominated the market with 34% share in 2025 due to the growing demand from chemical processors. The focus on lowering handling costs and the need to enhance transportation safety during the transportation of hazardous waste increases demand for HDPE. The excellent chemical inertness, high impact resistance, design flexibility, and safety compliance of HDPE help with expansion. The thriving production of fluorinated HDPE drives the segment growth.

The steel segment held the 22% market share in 2025 due to the focus on preventing aggressive chemicals' dangerous leaks. The high variety of hazardous waste and the stringent plastic pollution regulations increase steel demand. The focus on automated waste sorting and the need to lower procurement costs increases the adoption of steel. The extreme durability, excellent chemical compatibility, infinite recyclability, and longevity of steel support the segment growth.

The drums segment dominated the market with 31% share in 2025 due to the high preference from chemical plants. The government's safety mandates and focus on preventing fumes during transition increase the use of drums. The rise in petroleum-based waste and the expansion of closed-loop logistics increase the use of drums. The bulk handling capabilities, excellent durability, exceptional reusability, and excellent strength of drums drive the segment growth.

The intermediate bulk containers (IBCs) segment held the 26% market share in 2025 due to the rise in bulk chemical logistics. The rigorous safety protocols in the transportation of industrial intermediates and the focus on simplifying waste cleanup increase the use of IBCs. The focus on lowering the total cost of transportation and the growth in the pharmaceutical sector increase the use of IBCs. The shift to recycling rigid IBCs and the interest in flexible IBCs support the segment growth.

The hazardous chemical waste segment dominated the market with 52% share in 2025 due to the increased generation of toxic chemical waste. The stringent transport rules and the high reactivity of hazardous waste increase demand for chemical waste packaging. The high amount of waste generation in metal processing and the huge amount of chemical byproducts increase the adoption of chemical waste packaging. The focus on preventing dangerous reactions drives the segment growth.

The non-hazardous chemical waste segment held the 28% market share in 2025 due to the enhanced efficiency of waste handling. The manufacturing industry strong focus on minimizing landfill waste, and the well-established multinational pharmaceutical companies increase the adoption of chemical waste packaging. The growing downstream industries and the stringent regulations for waste segregation increase the use of chemical waste packaging, supporting the overall segment growth.

The 100-250 liters segment dominated the market with 34% share in 2025 due to the growing use in industrial chemical facilities. The strong focus on standard shipping pallets and the growing industrial distribution increases demand for 100-250 liters. The strong industrial production lines and the focus on maximizing cargo space increase the use of 100-250 liters. The versatile waste accumulation, logistics efficiency, and optimal transport of 100-250 liters drive the segment growth.

The 20-100 liters segment held the 26% market share in 2025 due to the growing demand for medium-capacity containers. The growing chemical handling applications and the robust growth in laboratory environments increase the adoption of 20-100 liters. The focus on batch separation in industrial sectors and the focus on maximizing payload space increase the use of 20-100 liters. The optimal manual portability, high traceability, and improved safety features of 20-100 liters support the segment growth.

The chemical manufacturing segment dominated the market with 33% share in 2025 due to the expanded chemical production. The growing internal consumption of various chemicals and the focus on avoiding contamination in the chemical industry increase demand for chemical waste packaging. The rising commodity chemical manufacturing and the strong presence of specialty chemical manufacturers increase the use of chemical waste packaging, driving the segment growth.

The oil & gas segment held the 16% market share in 2025 due to the growing generation of complex waste in the oil & gas industry. The growing upstream activities and the expansion of the waste oil industry increase the use of chemical waste packaging. The growing resource recovery and increased downstream activities increase the adoption of chemical waste packaging. The initiatives for industrial spill prevention support the segment growth.

The storage segment dominated the market with 36% share in 2025 due to the growing long-term storage in industrial facilities. The focus on preventing ecological damage and catastrophic leaks increases demand for storage. The high bulk volumes of petrochemicals and the storage of high-performance materials increase demand for storage. The chemical stockpiling activities drive the overall growth of the segment.

The transportation segment held the 31% market share in 2025 due to the expansion of agrochemical production. The cross-border chemical transportation and the booming manufacturing activities increase demand for transportation. The shift to the circular model and the growing IoT integration in logistics help with market expansion. The expanding industrial outsourcing supports the overall segment growth.

The UN certified packaging segment dominated the market with 41% share in 2025 due to rigorous performance testing. The growth in export-oriented industries and the global guidelines for transportation increases the use of UN certified packaging. The focus on insurance protection and legal compliance increases the adoption of UN certified packaging. The international hazardous waste transport regulations drive the segment growth.

The DOT compliant packaging segment held the 19% market share in 2025 due to the stringent regulatory enforcement. The rise in closed-loop initiatives and the focus on corporate risk management increase demand for DOT compliant packaging. The higher demand for specialized containment solutions increases the use of DOT compliant packaging. The rise of third-party logistics and booming global chemical manufacturing support the segment growth.

The direct sales segment dominated the market with 48% share in 2025 due to the surging demand for customized packaging solutions. The industry's focus on guaranteed compliance and the rising demand for co-engineered solutions increase the adoption of direct sales. The focus on a clean chain of custody and the growing demand for on-site consulting increase the adoption of direct sales. The liability management, bulk purchasing, and high accountability in direct sales drive the segment growth.

The industrial distributors segment held the 27% market share in 2025 due to the high preference for just-in-time delivery. The growing demand for chemical-resistant containers and the company's focus on navigating complex requirements increase buying from industrial distributors. The end-user's strong focus on lowering logistical bottlenecks and the management of complex logistics increases the use of industrial distributors. The immediate availability of the product on industrial distributors supports the segment growth.

The reusable packaging segment dominated the market with 58% share in 2025 due to the focus on lowering corporate carbon emissions. The waste reduction initiatives and the need to lower TCO increase the use of reusable packaging. The ESG targets and the occupational safety mandates increase demand for reusable packaging. The rising development of industrial reusable packaging drives the segment growth.

The single-use packaging segment held the 42% market share in 2025 due to contamination prevention. The focus on hazardous risk mitigation and the need to lower return freight costs increases the use of single-use plastic packaging. The focus on environmental safety during the disposal process and the need to avoid expensive logistics increase the use of single-use packaging. The expansion of contamination-sensitive applications supports the overall segment growth.

Asia Pacific dominated the market in 2025 with a 34% share and is expected to grow at the fastest CAGR of 8.24% in the market during the forecast period. The strong petrochemical manufacturing hub and the stringent mandates for hazardous waste management increase demand for chemical waste packaging. The high agricultural production and the prevention of water contamination increase the adoption of chemical waste packaging. The thriving commercial development and expanded chemical recycling ecosystem create a higher demand for chemical waste packaging. The continuously growing end-use sectors drive the market growth.

China

India

North America held the 27% market share in 2025. The strong focus on handling hazardous materials and the presence of leading agrochemical companies increase the adoption of chemical waste packaging. The interest in closed-loop initiatives and the federal guidelines for hazardous material storage increases the adoption of chemical waste packaging. The mature domestic biotechnology manufacturing infrastructure and the rise in the digitization of supply chains support the market growth.

United States

Canada

Europe held the 24% market share in 2025. Transitioning away from single-use virgin plastics and the Hazmat safety standards increases the demand for chemical waste packaging. The rise in advanced paint manufacturing and European green deal initiatives increases the adoption of chemical waste packaging. The ongoing innovation in chemical recycling and the major focus on corporate circularity boost the market growth.

Germany

France

Latin America held the 8% market share in 2025. The government focuses on managing industrial pollution, and the surging mining activities increase demand for chemical waste packaging. The focus on storing biomedical waste and the shift away from hard-to-recycle plastics increase demand for chemical waste packaging. The expansion of nearshoring trends and the higher demand for compliant chemical packaging support the market growth.

Brazil

Argentina

The Middle East & Africa held the 7% share in 2025. The strong oil & gas production hub and the rising utilization of agriculture chemical increases demand for chemical waste packaging. The huge polymer production and the increased biomedical chemical waste increase the adoption of chemical waste packaging. The well-established petrochemical companies and industrial expansion boost the market growth.

Saudi Arabia

United Arab Emirates

By Material Type

By Packaging Type

By Waste Type

By Capacity

By End Use Industry

By Packaging Function

By Compliance Standard

By Distribution Channel

By Reusability

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarChemical Waste Packaging Market