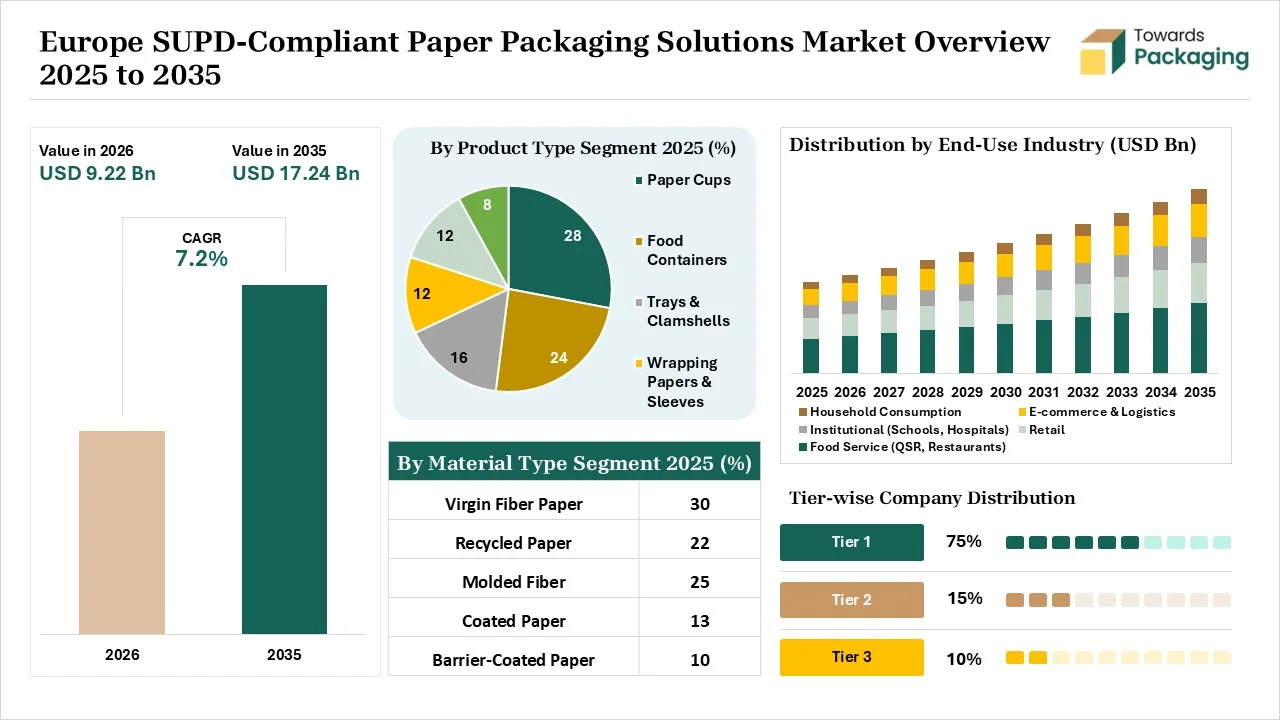

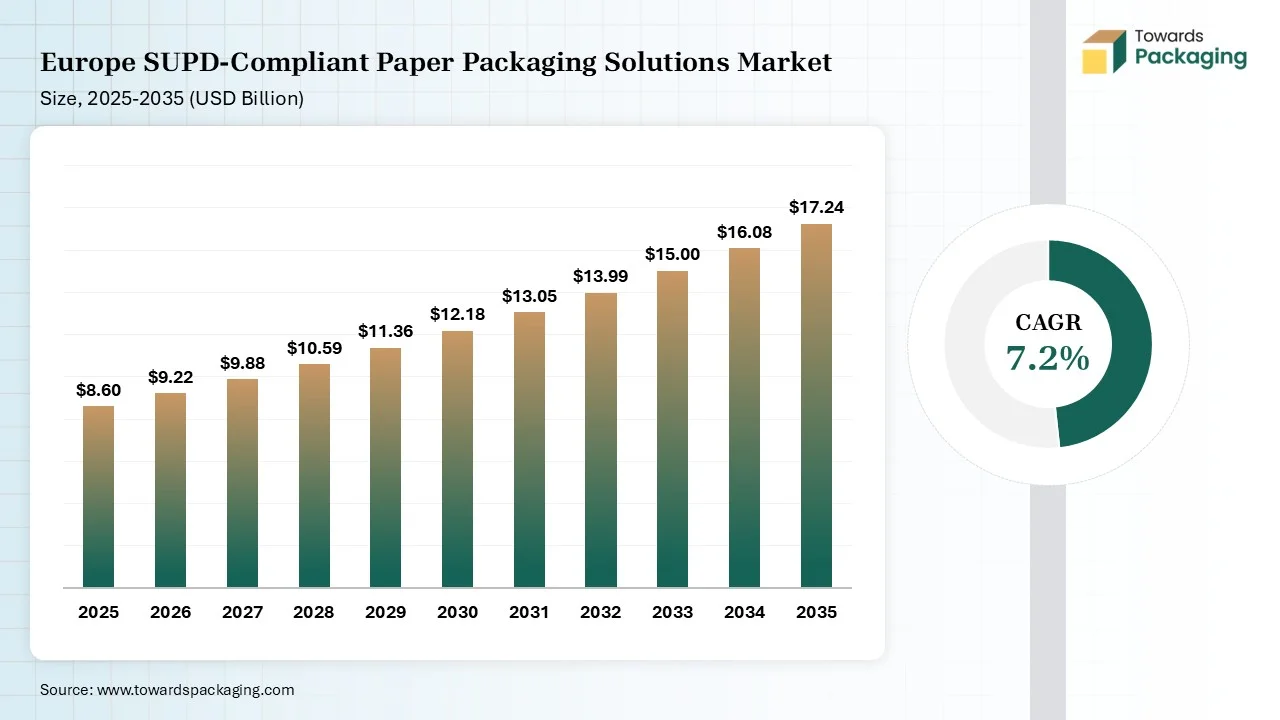

The Europe SUPD-compliant paper packaging solutions market is projected to grow from USD 9.22 billion in 2026 to USD 17.24 billion by 2035, registering a CAGR of 7.2% during the forecast period. The report provides detailed market size forecasts, segment-wise revenue analysis, regional demand assessment, competitive benchmarking, company market share evaluation, manufacturer and supplier profiles, value chain analysis, trade flow statistics, import-export trends, pricing outlook, production capacity analysis, and strategic developments shaping the European packaging industry.

SUPD-compliant paper packaging solutions are packaging products manufactured using paper materials that meet the requirements of the EU’s SUPD. They are free from microplastics and made from bio-based coatings. They offer characteristics like industrial recyclability, biodegradability, seamless scalability, and are free from PFAS. They offer benefits like exceptional barrier protection, true recyclability, immediate regulatory compliance, improved shelf appeal, and lower plastic waste. Their common applications are SUPD-compliant bowls, flow wraps, paper cups, fast food trays, and containers.

The Europe SUPD-compliant paper packaging solutions market growth is driven by the stringent packaging regulations, surging consumer preference for renewable packaging, corrugated substrates innovations, strong circular commitments, surging delivery of RTE convenience foods, well-established paper collection infrastructure, innovation in material technology, and brands' commitment to ESG goals.

The Europe SUPD-compliant paper packaging solutions market is going through several technological developments, like automated quality control, digital twins, sortation trackers, NFC tags, machine learning, smart packaging integration, and digital traceability helps in optimizing material efficiency and ensuring complete repulpability. The robust technological development in the market is the integration of artificial intelligence.

AI rapidly tests diverse variations of paper packaging and evaluates the structural integrity of packaging. AI analyzes packaging material properties and easily sorts the packaging waste. AI tests the durability of packaging and lowers paper usage. AI offers guidance on end-of-line recyclability and identifies structural defects in the packaging process. AI identifies incorrect barcodes present on the packaging. Overall, AI helps in automated compliance and quality assurance.

Raw materials like moulded pulp, bio-polymers, plant-based waxes, water-based adhesives, virgin pulp, aqueous coatings, nanocellulose, compostable inks, and resins are required.

Material processing involves steps like base paper selection, bio-based barrier coating, and sealing varnish application. Conversion includes printing, cutting, and forming.

Package design focuses on heat sealability, grammage optimization, bio-based coatings, and metallization. Prototyping includes 3D conceptualization, material testing, industrial scaling, and validation.

The major European companies manufacture a diverse range of SUPD-compliant paper packaging solutions to serve industries. BOBST, UPM Specialty Materials, and Michelman launched oxygen barrier wraps for single-pack chocolate & cookies, and also introduced packets & wrappers for the packaging of sugar-stick packs & other items. Lecta unveiled SBB for manufacturing paper cups. Lecta’s SBB contains bio-based barrier coatings. Mondi focuses on replacing single-use plastic films by developing specialized kraft papers.

The Stora Enso company developed fiber-based packaging boards for consumer goods and the food service industry. Coveris introduced the MonoFlex Fibre range, which complies with EU regulations. Sonoco Europe offers recycling infrastructure for paper-based packaging solutions. Huhtamaki offers a recyclable packaging solution for the F&B sector.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Huhtamaki | Espoo | Finland | Global leader in fiber-based foodservice packaging and SUPD-compliant paper solutions | Paper cups, lids, food containers |

| 2 | Mondi | Weybridge, England | United Kingdom | Major supplier of recyclable barrier paper packaging replacing plastic formats | Barrier paper and food packaging |

| 3 | Stora Enso | Helsinki | Finland | Leading developer of renewable fiber packaging and plastic-free boards | Fiber packaging and cartonboard |

| 4 | Smurfit Westrock | Dublin | Ireland | Extensive European fiber packaging footprint and sustainable packaging portfolio | Paper-based packaging solutions |

| 5 | DS Smith | London, England | United Kingdom | Major European supplier of recyclable fiber packaging aligned with SUPD requirements | Corrugated and paper packaging |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Billerud | Solna | Sweden | Strong provider of sustainable paper packaging and fiber innovations | Paper packaging and cartonboard |

| 2 | Graphic Packaging International | Atlanta, Georgia | USA | Significant European presence in paper foodservice packaging | Fiber-based food packaging |

| 3 | Metsä Board | Espoo | Finland | Premium lightweight paperboard supplier for plastic replacement packaging | Folding boxboard and food packaging |

| 4 | Coveris | Vienna | Austria | Expanding paper-based packaging portfolio for food applications | Sustainable paper packaging |

| 5 | Walki Group | Espoo | Finland | Specialist in recyclable barrier papers and fiber-based materials | Barrier paper solutions |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | PulPac | Gothenburg | Sweden | Pioneer in Dry Molded Fiber technology for plastic replacement | Molded fiber packaging |

| 2 | Paptic | Espoo | Finland | Developer of fiber-based alternatives to plastic packaging | Flexible fiber packaging |

| 3 | Notpla | London, England | United Kingdom | Developer of plastic-free coatings and fiber packaging technologies | Seaweed-coated paper packaging |

| 4 | BioPak Europe | London, England | United Kingdom | Specialist supplier of compostable and fiber-based foodservice packaging | Paper cups and food containers |

| 5 | Vegware | Edinburgh, Scotland | United Kingdom | Supplier of compostable foodservice packaging aligned with SUPD trends | Fiber foodservice packaging |

The paper cups segment dominated the market with 28% share in 2025 due to the growing hot beverages consumption on the go. The high restriction on the use of plastic cups and the well-established food delivery platforms increase the use of paper cups. The presence of a major coffee franchise and the modern consumer preference for eco-friendly solutions increase the use of paper cups. The superior brand marketing, high scalability, and the existing infrastructure compatibility of paper cups drive the segment growth.

The food containers segment held the 24% market share in 2025 due to the changing dining habits. The bans on plastic food containers and the explosion of QSRs increase the adoption of SUPD-compliant paper food containers. The interest in fiber-first packaging and the food chains' focus on achieving clean-label branding increases the adoption of SUPD-compliant paper food containers. The innovations, like eco-friendly linings and busy lifestyles, support the segment growth.

The trays & clamshells segment held the 16% market share in 2025 due to the food retailers' focus on eliminating plastic use. The huge consumption of RTE meals and the growing adoption of biodegradable alternatives in food chains increase the adoption of SUPD-compliant paper trays & clamshells. The rising use of trays in retail supply chains & grocery deli sections, and enhanced transportation in clamshells boost the segment growth.

The virgin fiber paper segment dominated the market with 30% share in 2025 due to its no contamination risk. The hygiene focus in the pharmaceutical sectors and the focus on high puncture resistance increase the adoption of virgin fiber paper. The expanding premium applications and advanced coating compatibility increase the use of virgin fiber paper. The premium aesthetics, superior tensile strength, premium brand image, purity, and advanced barrier functionalities of virgin fiber paper drive the segment growth.

The molded fiber segment held the 25% market share in 2025 due to the high preference for fiber-based alternatives. The brand's focus on staying compliant with changing laws and the rise in heavy food takeout increases the adoption of molded fiber. The focus on light transport and the focus on finding alternatives to rigid plastic packaging increase the use of molded fiber. The innovative chemistry, excellent protective performance, and circular economy alignment of molded fiber support the segment growth.

The recycled paper segment held the 22% market share in 2025 due to the growing use in FMCG brands. The presence of a strong system for recycling paper increases the production of recycled paper. The focus on lowering non-recyclable waste and the rising development of takeout containers increase the use of recycled paper. The consumer preference for natural-looking packaging and the abundance of raw waste paper increase production of recycled paper, boosting the overall segment growth.

The water-based dispersion coatings segment dominated the market with 34% share in 2025 due to the strict SUPD laws. The EU’s green economy goals and the growing demand for high-barrier protection increase the use of water-based dispersion coatings. The stringent food-contact regulations and the rise in beverage packaging increase the use of water-based dispersion coatings.

The bio-based coatings segment held the 26% market share in 2025 due to its excellent barrier performance. The higher chocolate consumption and the diverse FMCG brands increase the adoption of bio-based coatings. The move towards fossil-free packaging and the growing development of plant-based polymers increase the adoption of bio-based coatings. The manufacturing efficiency, improved compostability, and end-of-life viability of bio-based coatings support the segment growth.

The silicone/dispersion barrier systems segment held the 16% market share in 2025 due to the growing plastic replacement. The focus on packaging waste reduction and the shelf-life preservation of sensitive items increases the use of silicone barrier systems. The ban on fluorochemicals and the growing demand for high-barrier food packaging increase the adoption of dispersion barrier systems. The clean-release properties and superior functionality of silicone/dispersion barrier systems boost the segment growth.

The food service (QSR, restaurants) segment dominated the market with 38% share in 2025 due to growing demand for single-use cutlery. The rising demand for takeaway foods in urban lifestyles and the home delivery boom increases the adoption of SUPD-compliant paper packaging solutions. The busy work-life routines and the presence of corporate cafeterias increase the adoption of SUPD-compliant paper packaging solutions. The shift away from plastic cups and the surge in ghost kitchens drive the segment growth.

The retail segment held the 22% market share in 2025 due to enhanced shipping operational benefits. The expansion of food retailers and the explosion of eco-friendly brands increase the adoption of SUPD-compliant paper packaging solutions. The retailers' focus on increasing branding and the expansion of omnichannel drives the adaptation of SUPD-compliant paper packaging solutions. The supermarket's preference for paper-based packaging supports the segment growth.

The e-commerce & logistics segment held the 18% market share in 2025 due to the huge demand for sustainable mailers. The e-commerce platforms focus on staying compliant with legal regulations and eco-friendly expectations in online purchasing, which increases the adoption of SUPD-compliant paper packaging solutions. The expansion of SUPD-compliant honeycomb wrapping helps with growth. The burgeoning quick commerce boosts the segment growth.

The beverage cups segment dominated the market with 32% share in 2025 due to the entrenched café culture. The rising takeaway of cold beverages and the massive coffee consumption habits enhance demand for SUPD-compliant paper beverage cups. The surging bans on plastic beverage cups increase the use of SUPD-compliant paper beverage cups. The burgeoning of takeaway hot beverages in institutional settings and the high utilization of beverage cups in the foodservice industry drive the segment growth.

The takeaway food containers segment held the 28% market share in 2025 due to the burgeoning food delivery. The food industry's focus on avoiding heavy penalties & the increase in off-premises dining accelerate demand for SUPD-compliant takeaway paper food containers. The major base of cloud kitchens and the shift away from plastic clamshell packaging increase the adoption of SUPD-compliant takeaway paper food containers. The development of takeaway boxes supports the segment growth.

The wrapping & packaging materials segment held the 18% market share in 2025 due to the rising demand across the retail sector. The explosion of fast-food wrapping and the preference for grease-resistant paper increases the adoption of SUPD-compliant wrapping and packaging materials. The focus on increasing the usability of packaged goods and the rise in wrapping of baked goods increase the adaptation of SUPD-compliant wrapping and packaging materials, driving the overall market growth.

Germany is leading the market due to the thriving environmental legislation. The fully developed paper mills and the strong presence of packaging manufacturers increase demand for SUPD-compliant paper packaging solutions. The large e-commerce industry and the established bioplastic recycling infrastructure increase the adoption of SUPD-compliant paper packaging solutions. The massive convenience food industry and the presence of industry-leading packaging companies drive the market growth.

France is growing at the fastest rate in the market due to the industry's shift to biodegradable alternatives. The massive beverage industry and the high volume of e-commerce parcels increase the adoption of SUPD-compliant paper packaging solutions. The shift to easily C and the strong anti-waste laws increase the adoption of SUPD-compliant paper packaging solutions. The French retailers' shift to circular packaging solutions supports the market growth.

The United Kingdom is rapidly expanding in the market due to the massive e-commerce sector. The government's financial penalties on packaging and the high consumer eco-consciousness increase demand for SUPD-compliant paper packaging solutions. The interest in plastic-free alternatives helps with expansion. The advancements in sealed paper packaging and bio-based coatings innovations boost the segment growth.

Italy is significantly growing in the market due to the EU’s PPWR compliance. The increased buying of household products packed in eco-friendly alternatives and the impressive recycling rate increase the adoption of SUPD-compliant paper packaging solutions. The rise in Italian food exports and the transition to the recyclable paper solution increase the adoption of SUPD-compliant paper packaging solutions, fueling the overall market growth.

By Product Type

By Material Type

By Barrier / Coating Type

By End-Use Industry

By SUPD Compliance Application

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarEurope SUPD-Compliant Paper Packaging Solutions Market