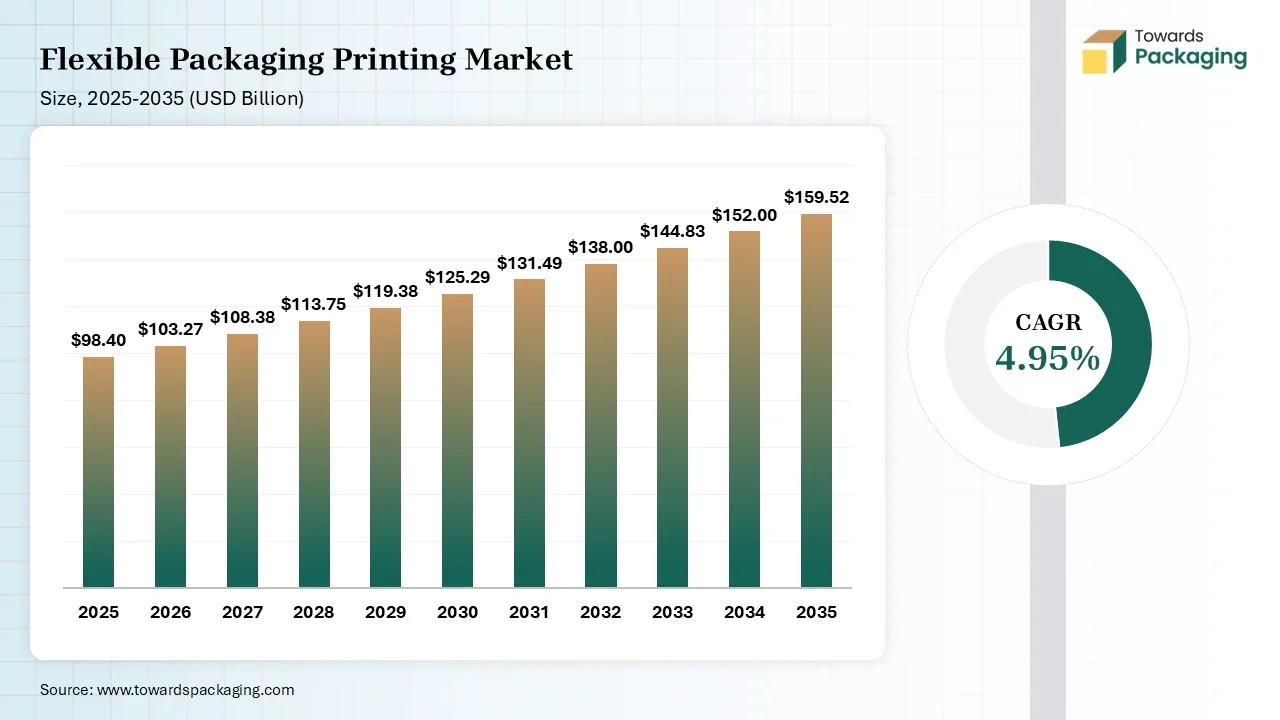

The Easy Open Packaging Market is projected to grow from USD 103.27 billion in 2026 to USD 159.52 billion by 2035, expanding at a CAGR of 4.95% during the forecast period. The report provides detailed market size forecasts, segment-wise analysis by material, packaging type, end-use industry, and opening mechanism, along with regional insights, company profiles, competitive analysis, value chain assessment, trade statistics, import-export analysis, manufacturer and supplier landscape, technological developments, and emerging growth opportunities.

Flexible packaging printing is the application of information, designs, graphics, and other details on diverse flexible packaging materials. These include materials like aluminum foils, PE films, PET films, and paper. Flexible packaging printing offers features like 360-degree branding, barrier protection, low material waste, and consumer convenience. It provides benefits like cost-efficient short-run production, product freshness, sustainability, and high shelf impact. The major printing technologies are digital printing, flexographic printing, and rotogravure printing. Digital printing is a new printing method that prints digital images on diverse media bases. Flexographic printing develops high-quality printed materials by using flexible photopolymer. Rotogravure printing is an industrial printing process that includes engraving, inking, scraping, and transfer methods. Flexible packaging printing is used in applications like stand-up pouches, sterile printing, squeeze tubes, single-serve treat packs, flexible wraps, and many more.

The flexible packaging printing market growth is driven by the expansion of high-speed flexo presses, AI integration in color inspection, booms in online shopping, expanding brand premiumization, sustainable ink advancements, adoption of packaging waste regulations, serialization mandates, exploding hybrid printing systems market, interest in resealable packaging formats, and the transition to eco-friendly substrates.

Surging Digitalization:- The focus on avoiding excess inventory use and the growing launch of targeted regional campaigns increases demand for digitalization, which increases the use of flexible packaging printing. The growing traceability demand across industries and workflow automation requirements increase the use of flexible packaging printing.

Surging Eco-Friendly Inks:- The increased penalties on petroleum-based inks and the need to avoid contamination in the recycling stream increase the use of eco-friendly inks. The air pollution reduction and circular recycling systems increase demand for eco-friendly inks.

Hybrid Printing Expansion:- The demand for visually striking packaging and the rise in on-demand customization increase the adoption of hybrid printing. The low setup time, highly targeted marketing, lower energy use, and superior quality of hybrid printing help with the expansion.

Flexible Packaging Industrial Adoption:- The high cost of rigid containers and the focus on warehouse footprint increases the adoption of flexible packaging. The rising use of formats like retort pouches, sterile sachets, squeezable tubes, stretch films, and others across industries helps with the expansion.

Several technological advancements, like cloud-based orchestration, ML-based quality control, automated metallization, IoT integration, TIJ coding, and electrophotography, are happening in the flexible packaging printing market. The demand for sustainability, printing-on-demand, minimized waste, and inventory obsolescence reduction drives the technological developments in the market. The AI integration is gaining major traction in the market.

AI helps in prototyping the concept of packaging and detecting color discrepancies. AI understands precise ink requirements and lowers the wastage of substrates. AI spots misregistration and supports dynamic personalization. AI optimizes the printing layout and detects ink faults instantly. AI optimizes the nest designs and provides anticounterfeiting tracking. AI supports demand-based production of flexible packaging. Overall, AI helps in artwork management, ink optimization, and sustainable operations.

Raw materials like PET, paper, varnishes, solvent-based inks, UV-curable inks, BOPP, printable nylon, water-based inks, and additives are required.

The stage includes surface treatment, printing, lamination, slitting of film, rewinding, and pouch or bag making.

Design includes steps like die line setup, color space, preparation of artwork, pre-press & production, prototyping, and approval of the client. Prototyping includes stating specifications, creation of a dieline, selection of material, digital printing, lamination, cutting, and physical testing.

The flexographic printing segment dominated the flexible packaging printing market with 39% share in 2025. The manufacturing of modern flexible packaging and the high-speed volume of packaging increase the use of flexographic printing. The availability of non-porous printing materials and the availability of UV inks increases the adoption of flexographic printing. The broad substrate compatibility and exceptional production speed of flexographic printing help with the expansion. The fast expansion of the food industry and the higher print quality demand drive the segment growth.

The rotogravure printing segment held the 30% market share in 2025. The long print runs production, and the focus on fine details increases the use of rotogravure printing. The demand for smooth tonal gradations and the focus on registration accuracy increase the use of rotogravure printing. The development of modern retail sachets and the continuous printing of high-resolution graphics increases the use of rotogravure printing. The huge manufacturing of stand-up pouches supports the segment growth.

The digital printing segment held the 17% market share in 2025 and is expected to grow at the fastest CAGR of 10.80% during the forecast period. The focus on preventing large inventory commitments and the creation of data-driven packaging increases the use of digital printing. The need to avoid toxic photo chemicals and massive growth in D2C brands increases the use of digital printing. The development of box pouches and the focus on utilizing less ink have increased the use of digital printing. The sustainable operations and design flexibility of digital printing boost the segment growth.

The solvent-based inks segment dominated the flexible packaging printing market with 43% share in 2025. The rise in synthetic flexible films and the demand for high graphic durability during shelf storage increases the use of solvent-based inks. The expansion of high-speed rotogravure presses and a focus on lower cost-per-impression increases the use of solvent-based inks. The extreme durability and compatibility with diverse plastic substrates of solvent-based inks help with the expansion. The rapid drying times and exceptional adhesion of solvent-based inks drive the segment growth.

The water-based inks segment held the 24% market share in 2025. The focus on eliminating the use of costly thermal oxidizers and the mandates for indirect food contact increase the adoption of water-based inks. The growing emulsions developments and the focus on avoiding swelling of printing plates increase the use of water-based inks. The brand image protection and the focus on enhancing worker safety increase the use of water-based inks. The increased press efficiency and enhanced indoor air quality of water-based inks support the segment growth.

The electron beam (EB) curable inks segment held the 8% market share in 2025 and is expected to grow at the fastest CAGR of 8.80% during the forecast period. The complete elimination of chemical contamination and the development of food wrappers increases the use of EB curable inks. The demand for sharp print quality and less energy consumption increases the use of EB curable inks. The growing eco-friendly operations and European safety standards increase the use of EB curable inks. The zero-VOC emissions, enhanced speed, and exceptional food safety of EB curable inks boost the segment growth.

The plastic films segment dominated the flexible packaging printing market with 56% share in 2025. The rise in high-speed graphic reproduction and the demand for lighter packaging increases the use of plastic films. The preservation packaging demand in personal care products and the development of shrink sleeves increase the use of plastic films. The demand for product design flexibility and innovations in recyclable solutions increases the use of plastic films. The unbeatable printing compatibility and tailored barrier qualities of plastic films drive the segment growth.

The paper segment held the 18% market share in 2025. The growing localized plastic bans and the move away from plastic films increase the use of paper. The surge in fast delivery and the focus on maintaining brand distinctiveness increase the use of paper. The advancing flexographic printing and the adoption of biodegradable coatings increase the use of paper. The evolution in digital printing and the massive consumer goods packaging increases the use of paper, supporting the segment growth.

The biodegradable & compostable films segment held the 6% market share in 2025 and is expected to grow at the fastest CAGR of 14.60% during the forecast period. The plastic-free regulations and demand for enhanced packaging performance increase the use of biodegradable & compostable films. The heavy taxes on non-biodegradable formats and the FMCG sustainability goals increase the use of biodegradable & compostable films. The innovations in material science and the trending fiber-based barrier coatings increase the use of biodegradable & compostable films, boosting the overall segment growth.

The pouches segment dominated the flexible packaging printing market with 31% share in 2025 and is expected to grow at the fastest CAGR of 7.20% during the forecast period. The crowded shelves of the retail industry and the focus on minimizing packaging transit space increase the adoption of pouches. The demand for value-added user convenience and the focus on keeping light out of food packaging increase the use of pouches. The reduction of manufacturing costs and e-commerce compatibility of the pouch help with the expansion. The expanding development of biodegradable pouch formats drives the segment growth.

The bags & sacks segment held the 20% market share in 2025. The interest in lightweight protective mailer boxes and the availability of resealable zippers increase the use of bags. The development of highly aesthetic graphics and the focus on higher economic benefits increase the use of bags & sacks. The exploding unit-dose packaging and the shift away from heavy-duty printed plastic increase the adoption of bags & sacks. The expansion of flexible paper bags supports the segment growth.

The wraps segment held the 12% market share in 2025. The focus on storage cost reduction and the increased use of advanced aesthetics to attract buyers increases the adoption of wraps. The high-barrier protection demand and the move to biodegradable films increase the development of wraps. The competitive retail environments and the tailored wrap designs help with the expansion. The non-standard shapes of wraps and cost-efficient logistics boost the segment growth.

The reverse printing segment dominated the flexible packaging printing market with 42% share in 2025. The focus on preventing scuffing in the handling of shipments and the need for the product to stand out on competitive shelves increases the use of reverse printing. The minimization of migration risks of chemicals and moisture protection demand in liquid products increases the use of reverse printing. The no ink smudging, longevity, strong abrasion resistance, excellent gloss, and tactile experience of reverse printing drive the segment growth.

The surface printing segment held the 34% market share in 2025. The removal of the lamination step and the shift to single-ply flexible packaging increase the use of surface printing. The quick creation of promotional campaigns and the high-gloss finishes demand increases the use of surface printing. The manufacturing of finished pouches and the development of limited edition SKUs increase the use of surface printing. The enhanced ink technologies and short-run adaptability of surface printing support the segment growth.

The lamination printing segment held the 17% market share in 2025 and is expected to grow at the fastest CAGR of 6.20% during the forecast period. The protection of packaging from external environmental factors and the high logistics resilience increase the use of lamination printing. The popularity of solventless lamination and the innovations in laminating technology help with the expansion. The demand for encapsulation of printed inks and the prevention of tearing in liquid-fill contents increases the use of lamination printing. The faster production and premium branding in lamination printing boost the segment growth.

The food & beverages segment dominated the flexible packaging printing market with 47% share in 2025. The focus on capturing consumer attention across F&B brands and the protection of drink products increases the use of flexible packaging printing. The demand for nutritional value display and promotional labeling in F&B increases the use of flexible packaging printing. The product safety demand in food delivery services and the massive F&B packaging volume increase the use of flexible packaging printing, driving the overall segment growth.

The pharmaceuticals segment held the 14% market share in 2025. The anti-counterfeit measures across the pharmaceutical industry and the growing unit-level tracking increase the adoption of flexible packaging printing. The rise in clinical trials and the focus on pharmaceutical brand security increases the adoption of flexible packaging printing. The regulations for tracking each drug unit and the complex pharmaceutical powders increase the use of flexible packaging printing. The expanding child-resistant blister foils support the segment growth.

The pet food segment held the 5% market share in 2025 and is expected to grow at the fastest CAGR of 6.80% during the forecast period. The presence of boutique pet brands and the massive demand for pet food packaging increase the use of flexible packaging printing. The growing number of modern pet owners and the demand for high-quality pet food ingredients increase the use of flexible packaging printing. The thriving therapeutic pet diets and the burgeoning online purchasing of pet food increase the adoption of flexible packaging printing. The pet owners' demand for portion control boosts the overall segment growth.

The direct sales segment dominated the flexible packaging printing market with 54% share in 2025. The brand owners demand the creation of personalised short-run designs, and the demand for direct communication increases the adoption of direct sales. The interest in specialized B2B consultation and the negotiation of bulk pricing increases the use of direct sales. The acceleration of launching cycles and demand for secure environments increases the adoption of direct sales. The collaborative innovation across direct sales drives the segment growth.

The packaging converters segment held the 28% market share in 2025. The need to improve profit margins and the expansion of D2C models increase the adoption of packaging converters. The increased printing on advanced materials and the frequent artwork changes increase demand for packaging converters. The huge production of resealable pouch formats and the smaller pack sizes increases the use of packaging converters, supporting the overall segment growth.

The online procurement segment held the 5% market share in 2025 and is expected to grow at the fastest CAGR of 6.20% during the forecast period. The huge industrial print runs and the focus on minimizing financial barriers increase the use of online procurement. The rise in email-based purchase orders and agile marketing testing increases the adoption of online procurement. The printing of unique QR codes and the buyers' demand for 24/7 access increase the adoption of online procurement. The testing of newly developed sustainable films and the supply chain digitization boost the overall growth of the segment.

Asia Pacific dominated the flexible packaging printing market in 2025 with a 42% share and is expected to grow at the fastest CAGR of 6.80% during the forecast period. The vast FMCG production bases and the increased pharmaceutical consumption increase demand for flexible packaging printing. The robust growth in the middle-class retail industry and the rise in brand personalization increase the use of flexible packaging printing. The mass demand for household goods and the increased manufacturing of rollstock increase the use of flexible packaging printing. The interest in eye-catching printing drives the market growth.

China held the highest share in the market. The push for on-the-go consumption and the popularity of personalized packaging increase the use of flexible packaging printing. The provincial plastic bans and the increased utilization of compostable materials increase the adoption of flexible packaging printing. The proliferation of SKUs and the massive expansion of digital printing support the overall market growth.

India is rapidly expanding in the market. The rise in 10-minute deliveries and the need to protect groceries increases the use of flexible packaging printing. The popularity of flexible pouches and the high investment in high-quality graphics increase the use of flexible packaging printing. The stringent EPR norms and the food processing boom increase the adoption of flexible packaging printing. The technological upgradation in machinery helps with the growth.

North America held the 26% market share in 2025. The increased use of automation in the retail sector and the rise in away-from-home consumption increase the adoption of flexible packaging printing. The expansion of portable snacks and the transition to mono-material printing technologies increase the use of flexible packaging printing. The well-established converting capabilities and the high demand for lightweight flexible mailers drive the overall growth of the market.

The United States is a robust contributor to the market. The escalating growth in the pharmaceutical industry and the brands' focus on developing highly customized designs increase the use of flexible packaging printing. The transition to bioplastics and the interest in automation-ready printing help with the expansion. The time-crunched lifestyles of consumers and the demand for rapid artwork changes increase the use of digital printing. The flexography innovations support the market growth.

Canada is growing in the market. The continuous F&B expansion and the rise in craft breweries increase the use of flexible packaging printing. The mandates for using eco-friendly inks and the skyrocketing retail ecosystems increase the adoption of flexible packaging printing. The advancements in the hybrid flexographic and the regulatory-based redesign of packaging boost the overall market growth.

Europe held the 23% market share in 2025. The growing investment in lamination techniques and the demand for portion-controlled packaging due to the shrinking household sizes increase the use of flexible packaging printing. The thriving online retail in European countries and the upgradation of printing machinery increase the adoption of flexible packaging printing. The logistics lightweighting demand drives the overall growth of the market.

Germany held the major share of the market. The rising use of durable packaging in the pharmaceutical sector and the innovations in printing technology help with the expansion. The adoption of biodegradable packaging inks and the German Packaging Act increases the use of flexible packaging printing. The burgeoning flexible packaging formats and the interest in cost-effective printing support the overall growth of the market.

The United Kingdom is growing in the market. The transition to smart materials and the rise in short-run campaigns increase the adoption of flexible packaging printing. The burgeoning flexible packaging formats and the PPT mandates increase the adoption of flexible packaging printing. The expansion of the UK baby food industry and the growth in the brand’s seasonal editions support the market growth.

Latin America held the 5% market share in 2025. The rise in the processing of single-serve foods and the explosion of modern retail formats increase the use of flexible packaging printing. The growing domestic adoption of bio-based plastics and the incorporation of technologies in printing help with the expansion. The modern supermarket presence and the focus on improving personalised consumer engagement increase the use of flexible packaging printing, driving the market growth.

Brazil is a key contributor to the market. The booming modern supermarkets and the high utilization of food processing packaging increase the adoption of flexible packaging printing. The burgeoning water-based inks industry and the well-developed flexographic printing help with the expansion. The thriving agribusiness and the production of eye-catching labels increase the use of flexible packaging printing, supporting the overall market growth.

Argentina is robustly expanding in the market. The interest in single-serve meals and the presence of price-conscious consumers increase demand for flexible packaging printing. The exploding digital printing and the presence of low-income groups increase demand for cost-effective packaging, which requires flexible packaging printing. The shift to recyclable films boosts the overall segment growth.

The Middle East & Africa held the 4% market share in 2025. The changing eating habits are driving demand for frozen foods, and the interest in branded consumer goods is increasing the adoption of flexible packaging printing. The growing popularity of sachets and the introduction of recycling mandates in MEA countries increase the adoption of flexible packaging printing. The healthcare manufacturing and the mono-materials demand drive the overall growth of the market.

Saudi Arabia dominated the market in the MEA region. The young demographics' higher demand for packaged food and the vast refining ecosystem increase the use of flexible packaging printing. The initiatives like NIDLP and the growing local pharmaceutical investment increase the adoption of flexible packaging printing. The growing domestic demand for printing graphics services supports the overall market growth.

South Africa is rapidly growing in the market. The transition to paper-based laminates and the increasing sales of trial-size sachets increase the adoption of flexible packaging printing. The higher adoption rate of digital presses and the connected packaging growth help with the expansion. The use of smaller-sized pouches boosts the overall growth of the market.

| Rank | Company | Headquarters | Country | Major Contribution to the Flexible Packaging Printing Market | Key Packaging Products and Services |

| 1 | Amcor plc | Zurich, Switzerland | Switzerland | The company focuses on utilizing water-based inks and mainly invests in digital printing solutions. The company focuses on expanding its printing capacities in Oshkosh, Wisconsin. | Sunshine Technology, Accelerate Prepress Services, Amcor Amplify, Jaholo Prismatic Effects |

| 2 | Sealed Air Corporation | Charlotte, North Carolina, United States | United States | The company has in-line printing technologies and provides digital packaging portfolios. The company also offers plant-based stand-up pouches. | AutoPrint, CRYOVAC Barrier & Non-Barrier Films, Custom Mailers, AUTOBAG Systems, Shrink Wrap Films |

| 3 | Huhtamaki Oyj | Epsoo, Finland | Finland | The company has modern digital presses for creating personalized packaging & others. The company also offers specialized prepress services. | Rotogravure Printing, Digital Printing, Value-Added Finishes, Flexography Printing |

| 4 | Mondi plc | Weybridge, England, United Kingdom | United Kingdom | The company offers sustainable inks and high-performance digital printing. The company also operates traditional printing technologies. | Flexographic Printing, White Ink Digital, Rotogravure Printing, Digital Printing, FlexiBags, Formable Paper Packaging |

| 5 | Constantia Flexibles | Vienna, Austria | Austria | The company offers an aluminum digital printing solution. The company acquired Drukpol Flexo to expand flexographic printing capacity across the European region. | Shadow Printing, Digital Printing |

By Printing Technology

By Ink Type

By Packaging Material

By Packaging Format

By Printing Process

By End-Use Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarFlexible Packaging Printing Market