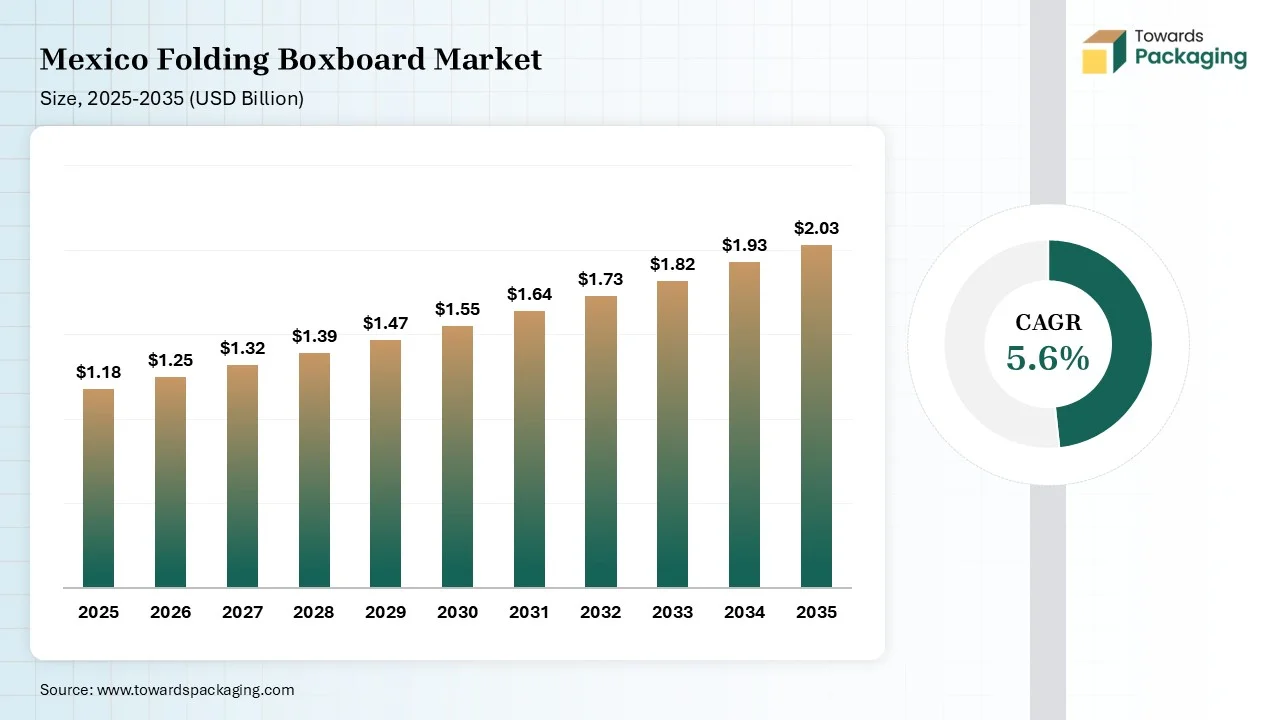

The Mexico folding boxboard market is projected to grow from USD 1.25 billion in 2026 to USD 2.03 billion by 2035, registering a CAGR of 5.6% during the forecast period. The report provides detailed insights into market size, growth trends, segment data by grade type, application, and end-use industries, along with regional data and demand analysis. It also covers leading companies, manufacturers, suppliers, competitive analysis, value chain analysis, pricing trends, production capacity, import-export trade data, and future market opportunities driving industry expansion.

Market Size (2025): USD 1.18 Billion

CAGR (2025–2035): 5.6%

Market Volume (2025): 1.42 Million Tons

Volume CAGR (2025–2035): 4.9%

Pricing Data (2025):

Mexico’s folding boxboard refers to the paperboard resources utilized in Mexico to create foldable packaging and cartons, generally used for consumer goods, food, cosmetics, and pharmaceuticals. These resources are identified for their enhanced strength-to-weight ratio, sustainability, and printability, often presenting several layers of pulp.

Technological transformation in the Mexico folding boxboard industry plays a significant role in the development of advanced coating technologies. The rising digital printing technology has fuelled the integration of progressive technology in manufacturing. The integration of AI in this sector supports the production of smart packaging that improves brand protection. These technologies are widely used for the development of lightweight packaging that is suitable for transportation purposes.

The major raw materials utilized are virgin wood pulp, chemical pulp, recycled fibre, and thermomechanical pulp. These are the materials used to enhance the flexibility of the boxboard.

Component manufacturing comprises virgin fiber, mechanical pulp, chemical pulp, and duplex board. These components enhance the packaging performance of the boxes.

This segment ensures safe handling from production to supply chain handling process. It enhances container density and optimizes transportation.

The FBB segment dominated the Mexico folding boxboard market with 41% share in 2025, due to the rising demand for superior printability and high versatility of the packaging. FBB is a lightweight structure that reduces material cost while maintaining strength. This grade of the food industry expands usage due to sustainability. These export-oriented packaging drives volume growth.

The SBS segment held 34% of the market share in 2025, due to its durability, premium, and high-quality printed packaging. These are premium packaging demand increases in cosmetics and pharmaceuticals. The major manufacturers prioritize high-quality printing surfaces. Major brands invest in visual appeal and durability.

The WLC segment held the 25% market share in 2025, due to enhanced demand for sustainability advantages, cost-effective packaging, and high-quality finish. The recycled content aligns with sustainability regulations. These are cost-effective solutions for mass-market goods. The rising retail packaging demand boosts adoption.

The food packaging segment dominated the Mexico folding boxboard market with 46% share in 2025, due to the rising demand for sustainable packaging options for the packaging of processed food and consumer goods. Processed food consumption rises across urban areas. Major brands demand eco-friendly packaging formats. The regulatory push favors paper-based materials.

The beverage packaging segment held the 18% market share in 2025, due to the increasing demand for durable, lightweight, and eco-friendly packaging. It raises production because premium beverage brands adopt rigid cartons for branding. The growth in craft beverages increases packaging variety. The rising export packaging demand strengthens the segment.

The personal care & cosmetics segment held the 14% market share in 2025, due to the increasing demand for sustainable, premium, and aesthetic packaging of the products. The rising premiumization trends drive aesthetic packaging demand. Major brands focus on shelf differentiation. The increasing exports boost packaging volumes.

The food & beverage segment dominated the Mexico folding boxboard market with 52% share in 2025, due to the increasing demand for durable, lightweight, and sustainable packaging. The rising packaged food demand fuels consumption. The expansion of supermarkets increases product variety and raises the demand for these packages. The sustainable packaging initiatives accelerate adoption.

The personal care segment held the 15% market share in 2025, due to the rising demand for protective packaging for high-end beauty products. The cosmetic exports increase demand for premium cartons. The rising branding and design drive packaging upgrades, which enhance the adoption of such packaging. The consumer preference shifts toward eco-friendly materials.

The healthcare segment held the 13% market share in 2025, due to the increasing concern for sterile, compliant, and safe packaging of the products. Pharmaceutical manufacturing grows domestically, that enhance the production demand for such packaging. The increasing export requirements demand high-quality packaging. The regulatory standards increase material utilization.

The 200–350 GSM segment dominated the Mexico folding boxboard market with 49% share in 2025, due to the expansion in the demand of pharmaceutical, food, and personal care products sectors. It is an ideal balance between strength and cost that drives adoption. These are widely used in food and cosmetics. The major manufacturers standardize production in this range.

The up to 200 GSM segment held the 28% market share in 2025, due to the huge-volume consumer goods packaging demand. The rising adoption of lightweight packaging reduces transportation costs. These are suitable for small consumer goods. The major brands focus on cost efficiency.

The above 350 GSM segment held the 28% market share in 2025, due to the increasing demand for premium and high-rigidity packaging in several sectors. The rapid growth in premium packaging demand increases its usage. The major luxury brands prefer rigid structures. The increasing requirements for protection drive the growth of this segment.

The coated segment dominated the Mexico folding boxboard market with 68% share in 2025, due to its suitability for premium packaging and high stiffness. The high-quality printing enhances brand visibility. The rising food safety compliance requires coated surfaces. The increasing premium packaging demand supports growth.

The uncoated segment held the 32% market share in 2025, due to the rising adoption of luxury and sustainable packaging. The increasing sustainability trends favor natural finishes. The rising cost-sensitivity of applications increases their adoption. The huge demand for recycling compatibility improves market demand.

The offset printing segment dominated the Mexico folding boxboard market with 54% share in 2025, due to its cost-effectiveness and large-scale production. The development of high-quality graphics supports branding requirements. These are widely used for large-scale production. The cost efficiency of this segment improves the adoption.

The flexographic printing segment held the 28% market share in 2025, due to high-speed capabilities for large production and its cost-effectiveness. The faster production speeds benefit high-volume packaging. This segment is suitable for corrugated integration. The increasing cost-effectiveness of bulk orders has raised the demand for this segment.

The digital printing segment held the 18% market share in 2025. Due to the increasing demand for luxury packaging and high-volume production. The increasing customization trends drive demand for short runs. The rising e-commerce packaging boosts variable printing. The rapid technology advancements improve the quality of the packaging.

The direct sales segment dominated the Mexico folding boxboard market with 47% share in 2025, due to the increasing demand for customized packaging. Huge manufacturers prefer direct procurement. Bulk purchasing reduces the cost of production of the packages. The long-term contracts stabilize supply chains.

The distributors segment held the 38% market share in 2025, due to the increasing requirement for supply chains and localized support. Small and medium enterprises mainly rely on distributors. The increasing inventory flexibility supports the increasing demand. The regional reach enhances accessibility to this packaging industry.

The online sales segment held the 15% market share in 2025, due to the rapid extension of the e-commerce sector. Digital procurement platforms gain popularity with this segment. SMEs adopt online sourcing, which has raised the demand for such packaging. Convenience and pricing transparency drove the growth of this sector.

The major growth factors include the rapid innovation and digitalization in the packaging sector. The rising food and beverages industry, pharmaceutical sector, and personal care sector have fuelled the demand for this sector. The rapid expansion of the e-commerce sector has raised the demand for high-quality printing, which has fuelled the demand for this sector.

By Grade Type

By Application

By End-Use Industry

By Thickness

By Coating Type

By Printing Technology

By Distribution Channel

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarMexico Folding Boxboard Market