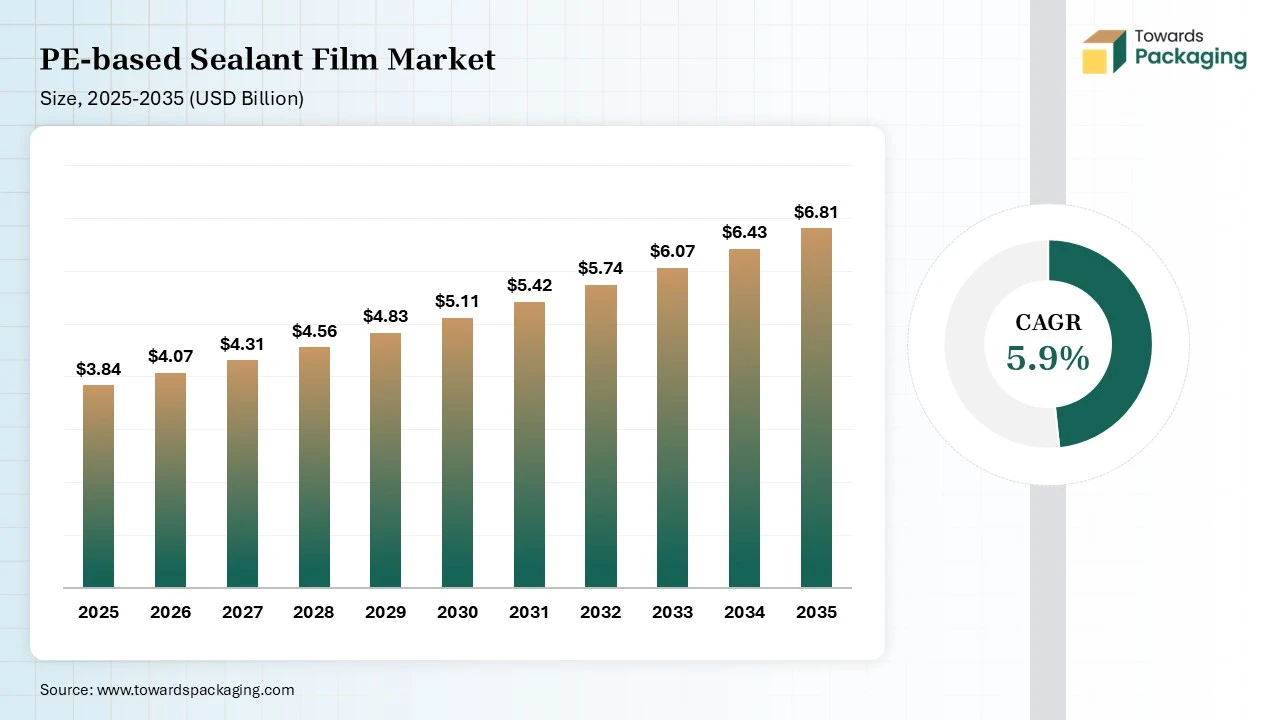

The PE-based Sealant Film market is forcasted to grow from USD 4.07 billion in 2026 to USD 6.81 billion by 2035, registering a CAGR of 5.9% during 2026-2035. The report covers market size, share, growth trends, segmentation by product type, application, end-use industry, and region, along with detailed regional analysis, competitive landscape, company profiles, manufacturers and suppliers, value chain analysis, trade statistics, pricing trends, demand-supply analysis, and emerging market opportunities shaping the industry.

PE-based sealant film is the heat-activable PE layer present in the flexible packaging. The characteristics include product safety, low melting point, low sealing temperature, high chemical resistance, excellent adhesion, and superior toughness. Their types are LLDPE, HDPE, LDPE, and mLLDPE. PE-based sealant film offers benefits like excellent sealability, high flexibility, excellent clarity, superior peelability, superior moisture barrier, and cost-effectiveness. They used across lidding films, tamper-evident seals, seal sachets, heavy-duty bags, and pouches.

The PE-based sealant film market growth is driven by the logistic expansion, convenience food growth, light-weighting trends, skyrocketing demand for packaged goods, silage wrapping expansion, growing mono-PE structures, development of mPE, exploding sterile packaging formats, and the interest in easy-open films.

The PE-based sealant market is going through technological developments due to the demand for sustainability, improved recyclability, and excellent barrier protection. The molecular design, co-extrusion automation, digital markers, recyclability software, predictive modelling, and smart packaging are ongoing technological developments in the market. The key development in the market is the incorporation of AI, which helps in optimizing formulation.

AI predicts the performance of diverse PE grades under different conditions. AI monitors the process of blown film extrusion and spots inconsistencies in the packaging film. AI predicts the potential failures and monitors the seal-window limits. AI schedules the machine repair and easily adjusts environmental variables. AI optimizes the sourcing strategies of the raw materials. Overall, AI supports material discovery and process optimization.

For instance, Colines integrates Mastermind, a virtual AI assistant, in its PE film extrusion production lines for setting-up times and optimizing production.

The stage acquires raw materials like ethylene-vinyl acetate, anti-blocking agents, metallocene-catalyzed polyethylene, plastomers, antioxidants, LLDPE, mLLDPE, and LDPE.

Key Players:- ExxonMobil Chemical, SABIC, Braskem, Chevron Phillips Chemical, Formosa Plastics, Dow Inc., LyondellBasell, Nova Chemicals, Borealis AG

Material processing involves blown film extrusion, cast film extrusion, and co-extrusion. Conversion includes lamination, surface treatment, and slitting.

Key Players:- Berry Global, Constantia Flexibles, UFlex Limited, Mitsubishi Chemical Group, Plastopil Flexible Packaging, Amcor, Sealed Air Corporation, ProAmpac

Design focuses on the seal initial temperature, peelability, and mono-material structures. Prototyping includes extrusion of film, lamination, pilot line trials, and application testing.

Key Players:- The Dow Chemical Company, ExxonMobil, ProAmpac, Bemis Manufacturing Company, Polifilm, Amcor Flexibles, Berry Global, Borealis AG

The LLDPE segment dominated the PE-based sealant film market with 34% share in 2025. The rigorous consumer packaging use and the expansion of the hot-seal range increase the use of LLDPE. The popularity of lightweight packaging and the need to improve the recyclability of packaging increase the adoption of LLDPE. The growing downgauging capability and demand for reliable seals increase the use of LLDPE. The high clarity, stable pricing, excellent sealability, and mono-material compatibility of LLDPE drive the segment growth.

The mPE segment held the 18% market share in 2025 and is expected to grow at the fastest CAGR of 7.40% during the forecast period. The focus on preventing the burst of packaging and the need for feedstock savings increases the adoption of mPE. The interest in all-PE designs and focus on enhancing retail appeal increases the use of mPE. The growing demand for exceptional downgauging and the expansion of mono-material solutions increase the use of mPE. The enhanced cost efficiency, high transparency, exceptional impact strength, and excellent hot tack of mPE support the segment growth.

The multilayer film segment dominated the PE-based sealant film market with 62% share in 2025 and is expected to grow at the fastest CAGR of 6.8% during the forecast period. The high demand for tamper-evident seals and the focus on a superior balance of mechanical properties increase the adoption of multilayer film. The preservation of material heat-sealing ability and the development of easy-tear seals increase the adoption of multilayer film. The increased utilization of 3-layer films in the diagnostic kits and food industry helps with expansion. The convenience features and superior moisture barrier of multilayer film drive the segment growth.

The monolayer film segment held the 38% market share in 2025. The focus on achieving remarkable stiffness and the medical shelf life extension increases the adoption of monolayer film. The focus on packaging line compatibility and the shift away from expensive adhesive layers increases the adoption of monolayer film. The burgeoning resin innovations and the retailers' focus on maintaining their scorecards increase the use of monolayer film. The high processing efficiency and the robust moisture barriers of monolayer film support the segment growth.

The 31-60 microns segment dominated the PE-based sealant film market with 41% share in 2025. The higher puncture resistance demand during the transportation of products and the need for a consistent weld track increase the use of 31-60 microns. The rise in multi-layer flexible packaging and the diverse sealing temperature in food packaging increases the use of 31-60 microns. The huge development of stand-up pouches increases the use of 31-60 microns. The superior tear resistance, wide applicability, and reliable hermetic sealing of 31-60 microns drive the segment growth.

The above 100 microns segment held the 12% market share in 2025 and is expected to grow at the fastest CAGR of 6.50% during the forecast period. The increased use of stretch hood films and the need for heavy-duty lidding increase the adoption of films with thicknesses above 100 microns. The rise in bulk protective wraps and demand for a thick sealant layer to maintain healthcare integrity increases the use of films with thicknesses above 100 microns. The development of heavy-duty garbage bags and heavy-duty courier bags requires films with thicknesses above 100 microns, supporting the overall segment growth.

The heat seal segment dominated the PE-based sealant film market with 52% share in 2025. The prevention of distortion of film and the need to maintain an airtight barrier increase the use of heat seal technology. The massive flexible packaging manufacturing and the development of low-friction wrapping increase the adoption of heat seal technology. The shelf-stable food demand and the expansion of anti-static bags increase the use of heat seal technology. The compatibility of heat seal technology with diverse PE grades drives the segment growth.

The resealable seal segment held the 13% market share in 2025 and is expected to grow at the fastest CAGR of 7.60% during the forecast period. The explosion of mono-material bags and the demand for convenience in closing & opening packaging increases the use of resealable seals. The interest in easy-peel capabilities and the priority for the safety of the packaged product increase the use of resealable seals. The user-friendly access, cold resistance, and no contamination in the resealable seal help with the expansion. The use of resealable seals in fresh produce supports the segment growth.

The blown film segment dominated the PE-based sealant film market with 44% share in 2025. The customization of packaging thickness and the focus on avoiding the failure of packaging increase the use of blow film technology. The development of heavy-duty industrial liners and the need for forgiving sealing windows increases the adoption of blown film technology. The higher moisture barrier demand and the need for flexibility in downgauging increase the use of blown film. The lower operational cost and superior toughness of blown film drive the segment growth.

The co-extruded film segment held the 21% market share in 2025 and is expected to grow at the fastest CAGR of 7% during the forecast period. The rise in the merging of various physical properties in film to provide customized performance increases the adoption of co-extruded films. The focus on preventing under-sealing issues and the higher adoption of co-extruded PE structures increase the use of co-extruded film. The higher utilization of high-performance resins and the integration of a dedicated sealant layer increase the use of co-extruded film. The targeted performance and low inventory cost of co-extruded film support the segment growth.

The food packaging segment dominated the PE-based sealant film market with 47% share in 2025. The focus on less energy consumption in food processing and the focus on fresh produce moisture retention increase the adoption of PE-based sealant films. The safety requirements for food safety and the expanding packaged consumables increase the adoption of PE-based sealant films. The circular adaptability in the major food brands and the avoidance of external contaminants in food increase the use of PE-based sealant film, driving the overall segment growth.

The pharmaceutical packaging segment held the 13% market share in 2025 and is expected to grow at the fastest CAGR of 6.9% during the forecast period. The sterility maintenance in the packaging of pharma products and the pharmaceutical stability requirements increase the use of PE-based sealant films. The need to improve medical-grade performance and the explosion of sterilization methods increase the use of PE-based sealant films. The focus on maintaining drug purity and focus on avoiding degradation of hygroscopic medications increases the use of PE-based sealant films, supporting the overall segment growth.

The food & beverage industry segment dominated the PE-based sealant film market with 49% share in 2025. The unmatched barrier demand in seafood products and the need for leak prevention in beverages increase the adoption of PE-based sealant film. The rising use of cling wrap in the food industry and the key brands' focus on minimizing handling cost increase the use of PE-based sealant film. The prevention of freezer burn in frozen items and the growth in frozen vegetables increase the use of PE-based sealant films, driving the segment growth.

The pharmaceutical industry segment held the 14% market share in 2025 and is expected to grow at the fastest CAGR of 6.9% during the forecast period. The oxygen protection demand in tablets and the increased use of clean-room processing for pharmaceuticals increase the adoption of PE-based sealant film. The focus on lowering pharmaceutical carbon emissions and the health authorities' regulations for packaging increases the adoption of PE-based sealant film. The burgeoning unit-dose pharmaceutical systems and the focus on stable drug deliveries increase the use of PE-based sealant films, supporting the segment growth.

Asia Pacific dominated the PE-based sealant film market with a 38% share in 2025 and is expected to grow at the fastest CAGR of 7.10% during the forecast period. The thriving demand for frozen meals and the high growth in pharmaceutical production increase the adoption of PE-based sealant film. The localized film converters and the development of high-tech PE films help with the expansion. The expansion of packaged grocery items and the drug manufacturing hubs in the ASEAN countries increases the use of PE-based sealant film. The demand for an appealing shelf display packaging drives the market growth.

China

India

North America held the 24% market share in 2025. The state-level environmental regulations and the expansion of recycled resin capacity increase the production of PE-based sealant film. The higher demand for medical lidding films and the rising ready-meal categories increase the use of PE-based sealant film. The explosion of e-commerce packaging and the stricter packaging laws increases the use of PE-based sealant film. The cost-effective feedstock supports the market growth.

United States

Canada

Europe held the 22% market share in 2025. The transition away from multi-polymer laminates and the presence of automated packaging equipment increase the development of PE-based sealant film. The increased use of sterile sealant films in the food industry and the innovations in the co-extrusion technology increase the production of PE-based sealant films. The increasing need for protective pharmaceutical blister packs supports the market growth.

Latin America held the 9% market share in 2025. The convenience stores' expansion and the circular economy shift increase the adoption of PE-based sealant films. The growth in agricultural output and the growing functional film innovation increase the use of PE-based sealant films. The safety regulations in the medical pouches and the growth in RTE meals increase the use of PE-based sealant films. The increased improvement in feedstocks supports the market growth.

The Middle East & Africa held the 7% market share in 2025. The abundance of cost-efficient feedstocks and the availability of packaged meat increase the adoption of PE-based sealant films. The high investment in medical tourism bases and the demand for protective heat-seal films increase the adoption of PE-based sealant films. The transition to western-style convenience and the increased development of urbanization projects increase the use of PE-based sealant films, boosting the market growth.

The high plastic availability and the focus on enhancing product freshness increase the use of PE-based sealant films.

The focus on minimizing import dependency and the massive construction of residential projects increases the adoption of PE-based sealant films.

| Rank | Company Name | Headquarters | Country | Major Contribution to PE-based Sealant Film Market | Key Packaging Products and Services |

| 1. | Amcor | Zurich, Switzerland | Switzerland | The company manufactures specialty functional sealants and offers BioVantage Sealant Film. |

|

| 2. | Sealed Air Corporation | Charlotte, North Carolina, United States | United States | The company focuses on recyclable film innovations and provides Darfresh technology for the manufacturing of food packaging. |

|

| 3. | Mitsui Chemicals Tohcello | Chiyoda-ku, Tokyo, Japan | Japan | The company collaborated with Siam Tohcello and SCG chemicals to develop highly functional PE films. The company mainly offers T.U.X. high-performance L-LDPE. |

|

| 4. | Coveris | Vienna, Austria | Austria | The company offers a high-barrier liquid packaging solution and also incorporates PCR content in the PE films. |

|

| 5. | Berry Global | 101 Oakley Street, Evansville, Indiana, 47710, United States | United States | The company uses VOID technology for developing micro-scale air pockets in the polyethylene films. The company uses PCR in the flexible film range. |

|

By Material Type

By Film Structure

By Thickness

By Sealing Technology

By Processing Technology

By Application

By End User

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPE-based Sealant Film Market