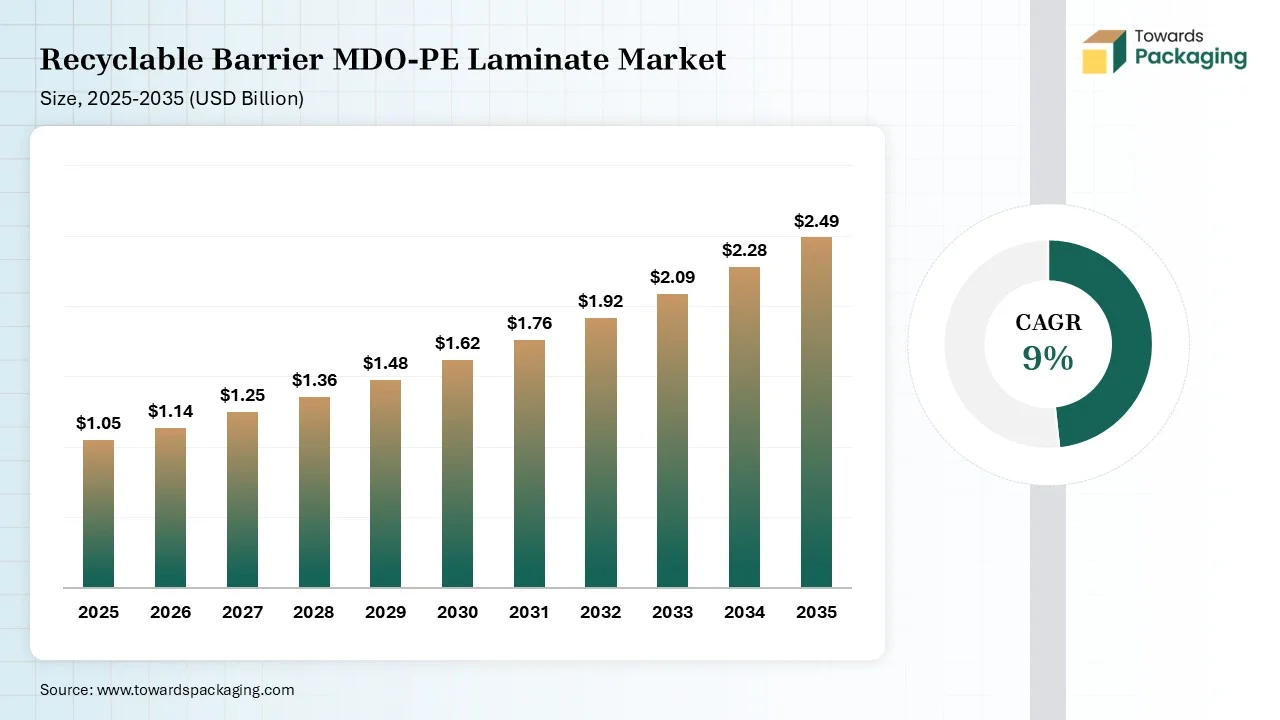

The Recyclable Barrier MDO-PE Laminate Market is projected to grow from USD 1.14 billion in 2026 to USD 2.49 billion by 2035, registering a CAGR of 9% during the forecast period. This report provides comprehensive coverage of market size, market share, segment analysis, regional market performance, company benchmarking, competitive landscape, value chain assessment, trade analysis, production and supply trends, manufacturers and suFppliers data, technological developments, regulatory landscape, and investment opportunities. The study further highlights the impact of sustainable packaging adoption, corporate environmental responsibility, and increasing replacement of conventional plastic packaging

Recyclable barrier MDO-PE laminate is a sustainable, flexible packaging film. These laminates offer PET-like performance and comply with recycling initiatives. The laminate offers prolonged shelf life, exceptional strength, enhanced recyclability, structural integrity, and premium printability. The features of the recyclable barrier MDO-PE laminate are high barrier performance, efficient conversion, true circularity, and high mechanical strength. The recyclable barrier MDO-PE laminate is used in premium matte pouches, flexible bags, heavy-duty sacks, and stand-up pouches.

For instance, in June 2025, RKW Horizon introduced a new film in the RKW Horizon range. The newly developed product is MDO-PE films with an EVOH barrier. The new film offers high transparency, printability, and tear resistance. The new film is used across flow packs, stand-up pouches, lidding films, and side gusset bags.

The recyclable barrier MDO-PE laminate market growth is driven by the worldwide bans on plastics, stricter EPR fees, enhancements in barrier coatings, e-commerce expansion, growth in solvent-free lamination adhesives, rise in mono-material solutions, innovations in the downgauging, growing environmental awareness, and the shift to flexible pouches.

Several technological developments, such as simulation software, machine learning, smart sorting, and digital extrusion, are happening in the recyclable barrier MDO-PE laminate industry. Factors like multi-material complexity, improved sustainability, and premium branding drive the technological developments. AI integration is a major revolution in the market that maintains the compliance of packaging.

AI easily identifies the barrier materials and monitors the thickness of the film. AI easily calculates the eco-fees and sorts MDO-PE laminates from other materials. AI optimizes the inventory and prevents the complex machinery from breaking down. AI offers structural transparency and easily evaluates the portfolios of packaging. Overall, AI supports predictive simulation, defect reduction, and contamination control.

Raw materials like polyethylene resins, solvent-free adhesives, and EVOH barrier additives are required.

Material processing involves the extrusion process, MDO, barrier application, and lamination. Conversion includes the lamination process, barrier integration, and sealability.

The design includes selecting MDO-PE film, integrating a barrier layer, selecting a compatible sealant web, laminating, coating, and verifying parameters. Prototyping focuses on the material structure, barrier integration, heat resistance, and real-world testing.

The LLDPE-based MDO-PE laminates segment dominated the market with 38% share in 2025. The difficulties in sorting diverse materials and the changing legislative rules increase the adoption of LLDPE-based MDO-PE laminates. The lighter films demand and the rise in cost-efficient production increase the use of LLDPE-based MDO-PE laminates. The higher demand for shelf-ready display packaging increases the use of LLDPE-based MD-PE laminates. The optimized sealability and excellent mechanical strength of LLDPE-based MD-PE laminates drive the segment growth.

The PE blend laminates segment held the 24% market share in 2025 and is expected to grow at the fastest CAGR of 10.7% during the forecast period. The increased development of PE-based packaging and printable outer webs increases the demand for PE blend laminates. The shelf life focus in beverage packaging and demand for low-temperature sealing increases the use of PE blend laminates. The difficult-to-recycle plastic replacements and the interest in eco-friendly laminates increase the use of PE blend laminates. The economic viability and optimized performance of PE blend laminates support the segment growth.

The EVOH barrier segment dominated the market with 42% share in 2025. The focus on unmatched preservation of cosmetics and the need to minimize feedstock use increase the adoption of the EVOH barrier. The highly printable packaging needs and the focus on better packaging designs increase the use of EVOH barrier. The shift away from PVDC helps with the expansion. The mechanical compatibility, high transparency, and optical synergy of the EVOH barrier drive the segment growth.

The AIOx coated barrier segment held the 13% market share in 2025 and is expected to grow at the fastest CAGR of 10.4% during the forecast period. The rise in the replacement of metallized polyester and the focus on increasing consumer visibility increase the adoption of AIOx coated barrier. The focus on minimizing laminate layers and the integration of specialized sealants increases the use of AIOx coated barrier. The expansion of converting processes helps with the growth. The high stability and encapsulated durability of AIOx coated barrier support the segment growth.

The multi-layer PE segment dominated the market with 52% share in 2025. The stringent recyclability designs and the focus on achieving superior gloss in the packaging increase the use of multi-layer PE. The need to achieve OTR in the pharmaceutical industry and the excellent moisture barrier demands in the packaged food increases the use of multi-layer PE. The increased commercialization of multi-layer PE helps with the expansion. The excellent runnability, closed-loop circularity, and high barrier performance of multi-layer PE drives the segment growth.

The single-polymer PE laminates segment held the 28% market share in 2025 and is expected to grow at the fastest CAGR of 10.9% during the forecast period. The increased use of packaging that meets recyclability standards increases the adoption of single-polymer PE laminates. The development of higher-quality recycled plastics and the eco-friendly goals increases demand for single-polymer PE laminates. The focus on replicating BOPP properties and the need to eliminate the use of expensive equipment increase the adoption of single-polymer PE laminates. The seamless line runnability of single-polymer PE laminates supports the segment growth.

The stand-up pouches segment dominated the market with 39% share in 2025. The focus on using low space on store shelves and the easy packaging trends increases the use of stand-up pouches. The focus on reducing the rupture of pouches and the prevention of oxygen transmission in the product increases the use of stand-up pouches. The need to provide a premium look to products and the increased snack production increase the use of stand-up pouches. The high space efficiency and superior stiffness of stand-up pouches drive the segment growth.

The recyclable lidding films segment held the 12% market share in 2025 and is expected to grow at the fastest CAGR of 11.4% during the forecast period. The reduction of landfill waste and the rising replacement of traditional materials increases the use of recyclable lidding films. The focus on prolonging food shelf life and the increasing lightweighting goals increase the adoption of recyclable lidding films. The need to preserve safety while maintaining RecyClass compatibility and the expansion of dairy products increases the use of recyclable lidding films, supporting the segment growth.

The 50-100 microns segment dominated the market with 44% share in 2025. The focus on preventing film tearing and the rise in holding heavier items increases the use of 50-100 microns. The need to improve moisture protection and the sealant layer integration increases the use of 50-100 microns. The expanding CPG companies and the protection of sensitive contents increase the use of 50-100 microns. The compatibility of the format with mono-material recycling streams drives the segment growth.

The above 150 microns segment held the 12% market share in 2025 and is expected to grow at the fastest CAGR of 9.9% during the forecast period. The high utilization of heavy-duty pouches and the rigorous waste reduction guidelines increase the use of above 150 microns. The expansion of high-stress applications and the production of industrial shipping sacks increases the use of above 150 microns. The protection of sensitive powder products and the shelf-life extension of medical supplies increases the use of laminates above 150 microns. The high drop resistance and enhanced moisture protection in above 150 microns support the segment growth.

The moisture barrier packaging segment dominated the market with 36% share in 2025. The prevention of the spoilage of hygroscopic powders and the need to maintain seal integrity increase the use of moisture barrier packaging. The focus on cereal weight efficiency and the need for WVTR protection increases the adoption of moisture barrier packaging. The expansion of moisture-sensitive products and the demand for product freshness increased the use of moisture barrier packaging, driving the segment growth.

The aroma barrier packaging segment held the 18% market share in 2025 and is expected to grow at the fastest CAGR of 9.7% during the forecast period. The need for excellent odor retention in food items and the focus on limiting food waste increase the use of aroma barrier packaging. The need to retain volatile flavor and the need to enhance pet care shelf life increase the use of aroma barrier packaging. The zero cardboard mess, excellent odor retention, and minimized food degradation in aroma barrier packaging support the segment growth.

The food & beverage segment dominated the market with 56% share in 2025. The aroma protection needed in the F&B products and packaging integrity in F&B increases the use of recyclable barrier MDO-PE laminates. The focus on lowering the rate of spoilage and the prevention of high EPR taxes in FMCG companies increases the adoption of recyclable barrier MDO-PE laminates. The convenient snacking demand and the zero-waste commitments increase the use of recyclable barrier MDO-PE laminates. The growing e-grocery deliveries drive the segment growth.

The personal care & cosmetics segment held the 15% market share in 2025 and is expected to grow at the fastest CAGR of 11.2% during the forecast period. The focus on structural rigidity of cosmetics packaging and the expansion of cosmetic formulations increases the use of recyclable barrier MDO-PE laminates. The expanding luxury beauty branding and the growing demand for travel-friendly cosmetic products increase the use of recyclable barrier MDO-PE laminates. The growing moisture loss in the personal care products and the premium positioning of the cosmetic products support the segment growth.

Europe dominated the market with a 34% share in 2025. The regulations, like the EU plastic strategy and the transition away from foil-based laminates, increase the adoption of recyclable barrier MDO-PE laminates. The advanced reprocessing capabilities and the consumer preference for changing their purchasing habits increase the use of recyclable barrier MDO-PE laminates. The consumer pushing brands to adapt flexible packaging helps with growth. The stringent preservation standards drive the market growth.

Asia Pacific held the 30% share of the market in 2025 and is expected to grow at the fastest CAGR of 10.8% during the forecast period. The spike in convenience food consumption and the increased replacement of unrecyclable laminates increase the adoption of recyclable barrier MDO-PE laminates. The popularity of circular economy packaging among brand owners helps with the expansion. The high purchasing of chilled goods and the well-established regional packaging converters increase the production of recyclable barrier MDO-PE laminates, supporting the market growth.

North America held the 22% market share in 2025. The shift of brands to circular models and the high demand for reusable packaging across FMCG giants increases the adoption of recyclable barrier MDO-PE laminates. The demand for high technical film performance and the transition from aluminum layer increases the use of recyclable barrier MDO-PE laminates. The continued growth in e-commerce and the growing strategic industry mergers support the overall market growth.

Latin America held the 8% market share in 2025. The growing usage of recycled content and the increased use of mono-material in food protection increase the adoption of recyclable barrier MDO-PE laminates. The spiking processed food demand and the multinational brands' eco-friendly pledges increase the use of recyclable barrier MDO-PE laminates. The thriving frozen food industry and the burgeoning protein export boost the overall market growth.

The Middle East & Africa held the 6% market share in 2025. The rising regional food producers and the thriving convenience sector increase the adoption of recyclable barrier MDO-PE laminates. The focus on saving e-commerce freight costs and the large-scale petrochemical projects increases the use of recyclable barrier MDO-PE laminates. The stringent export standards and the expanding grocery delivery infrastructure support the market growth.

| Rank | Company | Headquarters | Country | Major Contribution to Recyclable Barrier MDO-PE Laminate Market | Key Packaging Products and Services |

| 1. | Amcor plc | Zurich, Switzerland | Switzerland | The company manufactures proprietary MDO-PE products. The company offers recyclable MDO-PE solutions to the food and healthcare industry. |

|

| 2. | Constantia Flexibles | Vienna, Austria | Austria | The company invested €6.5 millions in the MDO technology, and the company incorporates BOBST Expert K5 metallizer for enhancing the barrier. |

|

| 3. | Klockner Pentaplast | Heiligenroth, Germany | Germany | The company manufactures PE-based films and offers superior processing capabilities for laminates. |

|

| 4. | TOPPAN Holdings | Bunkyo, Tokyo, Japan | Japan | The company manufactures all-PE barrier packaging for liquids and integrates GL BARRIER Film in the MDO-PE structures. |

|

| 5. | Polysack | Kibbutz Nir Yitzhak, Israel | Israel | The company focuses on high-barrier film innovation and offers the Pack N Cycle range. |

|

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarRecyclable Barrier MDO-PE Laminate Market