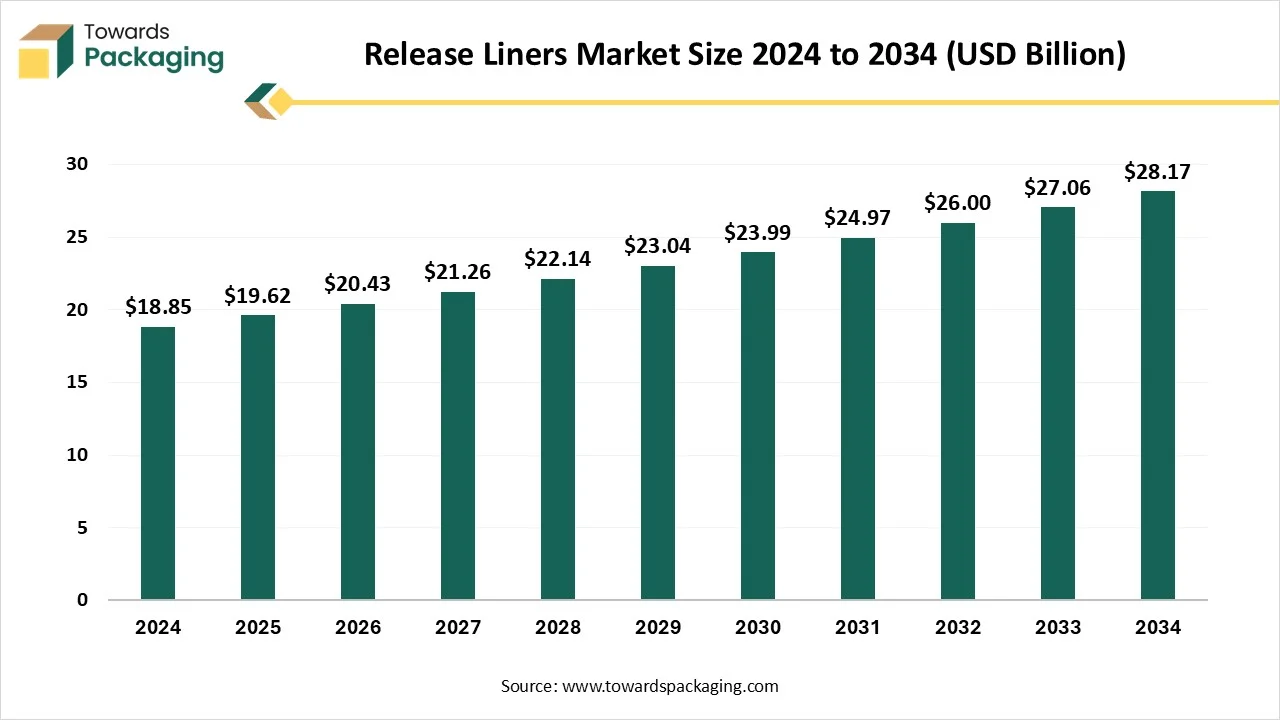

The release liners market is projected to grow from USD 19.62 billion in 2025 to USD 29.32 billion by 2035, at a CAGR of 4.1%. This growth is driven by rising demand for self-adhesive products, particularly in the packaging, labeling, and medical industries. The paper-based segment led the market in 2025, while the film-based segment is expected to grow at the fastest rate. Asia Pacific held the largest market share in 2025, with North America expected to witness notable growth during the forecast period. Innovations in silicone and non-silicone coatings are driving further advancements in the market.

The study further explores logistics and distribution networks, regional demand trends, and sustainability initiatives such as recyclable and bio-based liner materials. In addition, the report highlights competitive strategies of leading manufacturers, technological innovations in coating processes, and growing applications in medical, packaging, and industrial sectors, helping businesses understand market dynamics and identify growth opportunities in the global release liners market.

| Metric | Details |

| Market Size in 2025 | USD 19.62 Billion |

| Projected Market Size in 2035 | USD 29.32 Billion |

| CAGR (2026 - 2035) | 4.1% |

| Leading Region | Asia Pacific |

| Market Segmentation | By Material Type / Substrate, By Coating Type, By Application, By End-User Industry, By Revenue Model and By Region |

| Top Key Players | Sappi Limited, Nitto Denko Corporation, Stora Enso Oyj, Ritrama S.p.A., Flexcon Company, Inc., Yupo Corporation, Molymer (India) Pvt. Ltd., Lintec Corporation. |

The release liners market refers to the production and commercialization of sheets or films coated with a release agent that enables easy separation of pressure-sensitive adhesives (PSA) from the liner. These liners are widely used in pressure-sensitive labels, tapes, adhesive products, flexible packaging, graphics, and medical applications.

They can be paper-based, film-based, polycoated-paper-based, or even have different substrates. We can seek them in everyday uses by serving as a barrier between the pressure-sensitive adhesive and its surroundings, which protects the adhesive from sticking to surfaces before its actual usage. Without the release liner, an adhesive can become a pollutant and lose its smoothness, which then makes it challenging or impossible to use.

A procedure that integrates the usage of artificial intelligence technologies and a limited element method is constructed to track the manufacturing of a liner, specifically, the metallic shell of current high-pressure metal-composite cylinders. Costly physical experiments have been substituted by computer simulation, which made it possible to receive a big data array (BDA) in the design of tables counting the crucial technological parameters for swaging the liner neck and information about the metal flow at the time of deformation, and to disclose a tendency towards defect creation.

In the current packaging sector, release liners and release paper are rapidly driving a technological update. From regular carton labels and heat-sealed packaging to biodegradable electronic materials and composite film products, the use of release materials is constantly stretching, as kt becomes a main factor in developing packaging quality, environmental performance, and manufacturing efficiency too.

| Medical and Pharmaceutical Applications | Product Examples |

| Diagnostic & Point of Care | Diagnostic Test Strips (blood glucose, cholesterol, urinary tract infections) Point of Care / Diagnostic Devices |

| Fixation, Surgical & Wound Care | Advanced Wound Dressing (extended wear, burn treatment, MVTR, etc.) Catheter Placement Incise / Ophthalmic Incise Films IV Holders Medical Fixation Tapes Ostomy Pouches / Components Surgical & Isolation Drapery |

| Drug Delivery & Pharmaceutical Packaging | Transdermal Drug Delivery System (TDDS) Drug-Loaded Monolithic Matrix Reservoir with Rate Controlling Membrane Transdermal / Medicinal Patch Transmucosal Drug Delivery System (TMDS) Buccal Mucosal System Oral Thin Films (OTF) / Oral Strips Pharmaceutical Packaging Tapes |

| Medical Sensors & Electrodes | Disposable Electrodes ECG, EKG and TENS Pads / Electrodes Grounding Pads Oxygen Sensors |

| Process Carrier Liner | Enables Handling, Conversion & Assembly of Pharmaceutical & Medical Products |

| OTC / Consumer Healthcare | Cosmetic Patches (Face strips, acne pads, etc.) Eye Patches First Aid Bandages & Tape Hygiene Products (diapers, sanitary napkins, incontinence pads) OTC Therapeutic Patches |

Sustainability is a rising trend in the release liner sector. Organisations are increasingly discovering environmentally friendly options such as recyclable film materials and biodegradable paper substrates to align with environmental goals. These sustainable selections lower the waste and appeal to environmentally conscious consumers. Expertise organisations and industry initiatives are generating programs in order to recycle and collect used release liners. This can allow closed-loop recycling, in which high-quality fibers from paper liners are reprocessed into the latest release base papers. Producers are creating liners from recycled and alternative sources that count bio-based polymers (like corn or sugarcane) and post-consumer recycled (PCr) and plastic both.

Apart from this, the latest coatings are being made to reduce waste and develop recyclability. For instance, UV LED curable silicones are more nerdy-filled and secure to generate than regular alternatives.

The restrictions of release liners are that they are frequently discarded immediately after every use, which contributes to a large volume of waste. Due to this, they are not widely or easily recycled and end up in landfills or incineration. Standard silicone-coated release liners, which consist of a base material (paper or film) and a silicone coating, are further challenging to recycle. The silicone must be removed from the substrate in a procedure called deinking, and not every recycling facility has the compulsory machine.

")

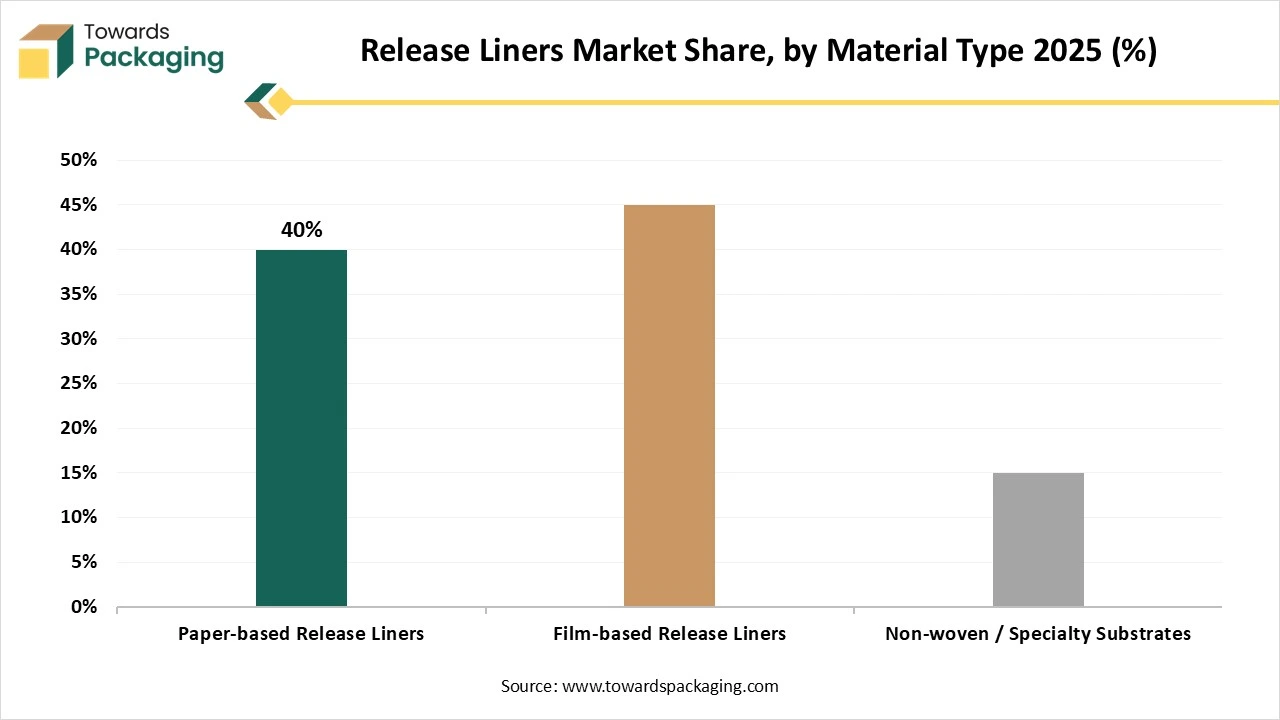

The paper-based release liner segment dominated the market in 2025, as they are greatly utilised in sectors where versatility and smoothness are the main factors. These liners are perfect for uses such as taps, labels, and graphic art. One of the benefits of paper release liners is their convenience of personalization, which enables producers to personalize them to needs. Furthermore, they have accurate moisture resistance characteristics, which ensure the integrity of the adhesive material even in humid surroundings.

Also, paper release liners provide perfect printability that enables high-quality graphics and vibrant colors. Their versatility expands to the tape sector, in which they serve as a reliable backing for different adhesive tapes, which ensure easy use and removal.

The film-based release liners segment is predicted to be the fastest in the market during the forecast period. These liners utilise polyester (PET), polyethylene (PE), and other films that are made of plastic material as the main material. The usage of films facilitates developed flexibility, strength, and opposition to surrounding factors such as moisture and heat. Film-based release liners are necessary in high-performance environments like automotive and electronics production, in which stability and accuracy are main. They also enable tighter tolerances with respect to performance and thickness, which is often complicated in big industries.

The silicon-coated segment dominated the release liners market in 2025, as silicone-release liners are necessary materials in the manufacturing and industrial sectors. These are particularly crafted sheets that protect the product from attaching collectively, which enables soft operations and improved product quality. It is made from silicone, which is well-known for its non-stick characteristics, durability, and heat resistance, as these liners play a crucial role in different production procedures.

Their personalised release characteristics enable manufacturers to choose the right release liner for applications, which adds to their versatility.

The non-silicone segment is expected to be the fastest-growing in the market during the forecast period. Non-silicone release liners serve as an alternative to regular silicone-coated liners. They search uses in situations in which silicone residues may interfere with downstream procedures in which particular adhesive characteristics need a non-silicone surface. Sectors such as medical devices and electronics often need non-silicone release liners to block pollutants or obstructions with sensitive elements. These liners serve a residue-free surface and are clean, which ensures the accurate functioning of the devices.

The pressure-sensitive labels and tapes segment dominated the market in 2025, as release liners are crucial to pressure-sensitive adhesive uses such as graphics, tapes, and medical products. Release liners are also utilised in industrial composite applications and construction uses in which sticky chemicals are being managed by the release liner till they are ready for usage. These chemicals and adhesives need protection during transport and storage.

Usually, pressure-sensitive adhesive labels and tape include three parts: the carrier, release liner, and adhesive.

The carrier is a stiffer material that assists the tape in tracking its structure and stability. The adhesive layer assists the tape in making bonds.

The medical and hygiene segment is predicted to be the fastest in the market during the forecast period. Consumer goods are a complete set of products, including release liners. These include electrodes, wound care dressings, baby care products, transdermal patches, tapes, personal hygiene, wearable devices, and feminine care, too. Release liners seek huge applications in the medical field, specifically in hygiene uses. These types of liners ensure reliable and sterile use of medical adhesives while tracking the convenience of use and product integrity.

Furthermore, release liners make it convenient for healthcare professionals to use dressings or bandages precisely and securely, which provides optimal wound care.

The labelling and packaging segment dominated the market in 2025, as labels and release liners deliver as dependable carriers of the facestock and adhesive during converting, printing, and application too. The release liners will serve as a hard surface for the die-cutting intricate shapes without enabling the die to break through the silicon layer and disturb the release performance at the time of usage. They provide a temporary carrier for the label unit till it is ready to be used on the needed substrate.

Release liner materials in film liners, paper liners, and specialty liners, too. They even make sure of ideal label performance.

The medical and healthcare segment is expected to be the fastest in the market during the forecast period. PET release liners are prevalent for wound dressings, medical tapes, and other medical adhesive products. Their reliability is to track dimensional security and oppose pollutants and moisture, which makes them perfect for sterile surroundings and complicated healthcare settings. Uses such as transdermal patches, advanced wound care, electrode fixation, and wearable devices are advantageous from PET liners as they serve a dependable and constant release, which assists in the accurate placement of medical products.

")

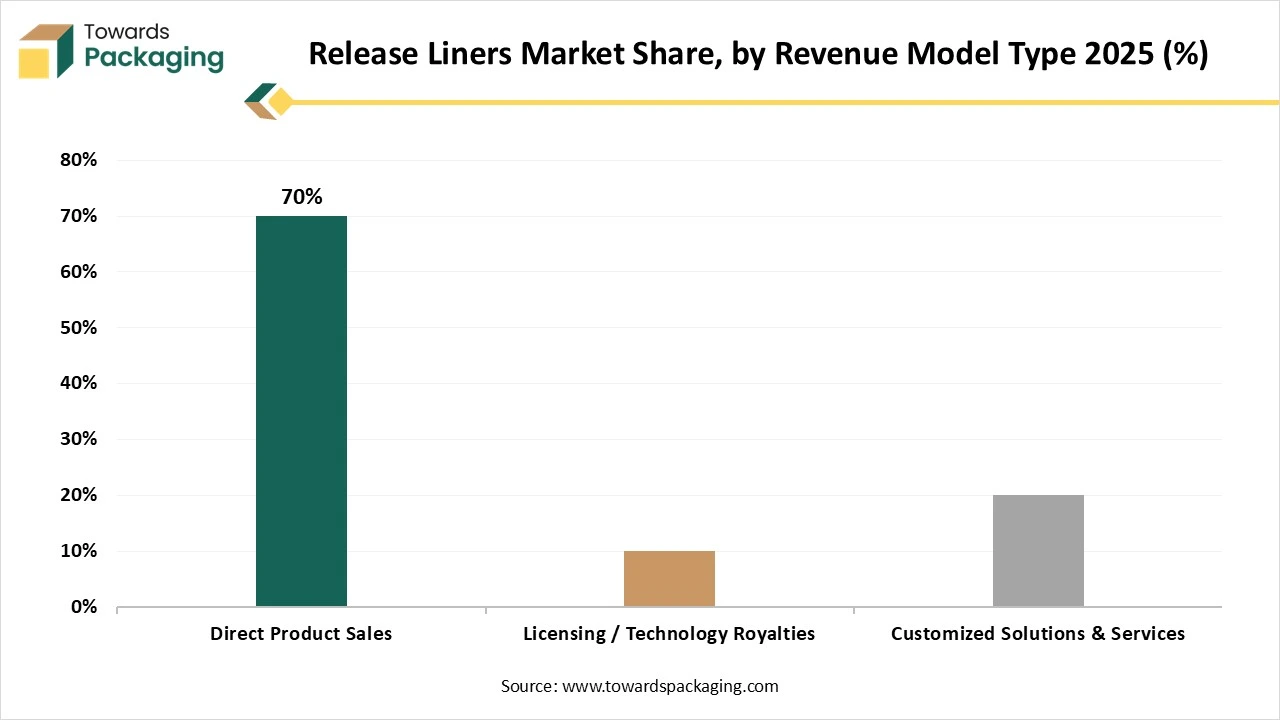

The direct product sales segment dominated the release liners market in 2025, as it is completely possible to buy release liners directly from manufacturers and their official distributors, as well as from wholesale retailers and suppliers. The accessibility depends on the volume that is demanded and the uses for the liner. For a minute, businesses or those who do not demand custom runs, distributors and wholesalers serve a more usable way to buy release liners. These organisations have stocked items from different manufacturers and sell them in minute quantities. Online marketplaces are a famous way to seek these suppliers.

The customized solutions and services segment is predicted to be the fastest in the market during the forecast period. One can easily customize various colors and release force of release liners as per the customer's demands. This is a grid release paper that we tailor for users, which mainly solves the bubbles created by users during the die-cutting procedure of electronic tape. The surface of the product has the anti-sticking of grease liners, and it also has the reliability of the exhaust, anti-slip, and is not convenient to make bubbles when the product is being linked to it. It is perfect for waste discharge and punching pads for round knife die-cutting and flat knife die-cutting.

")

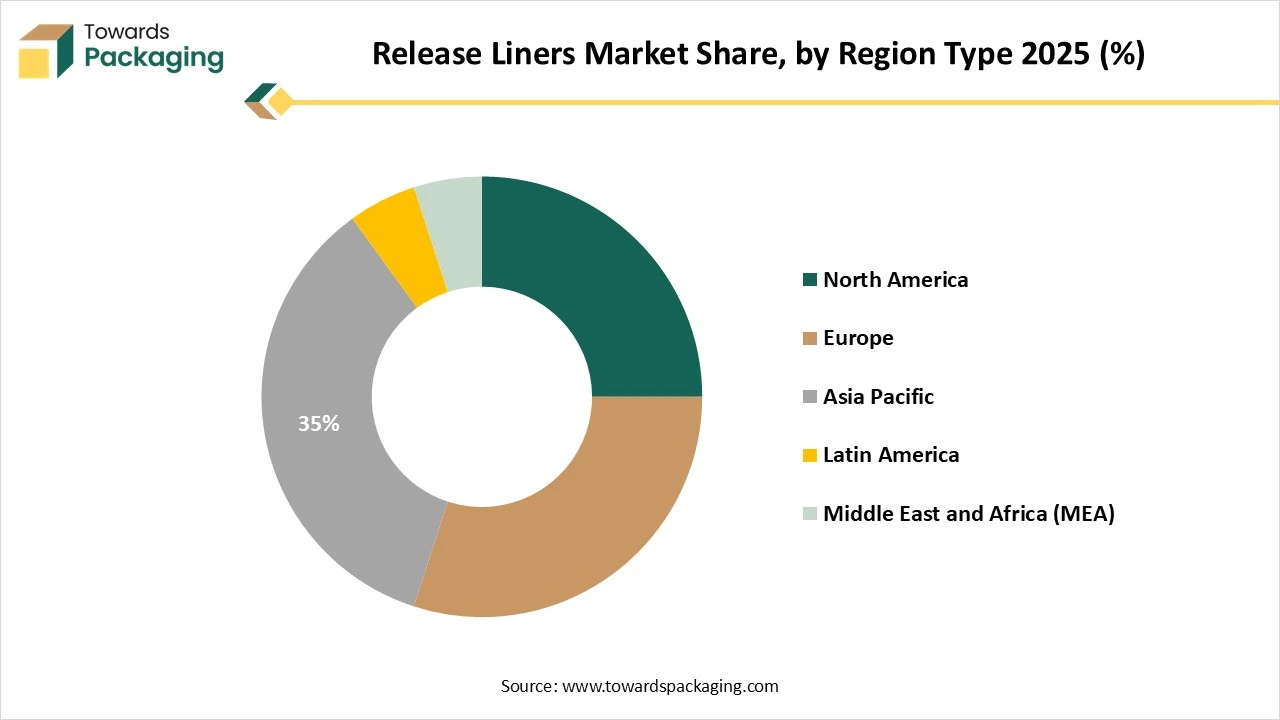

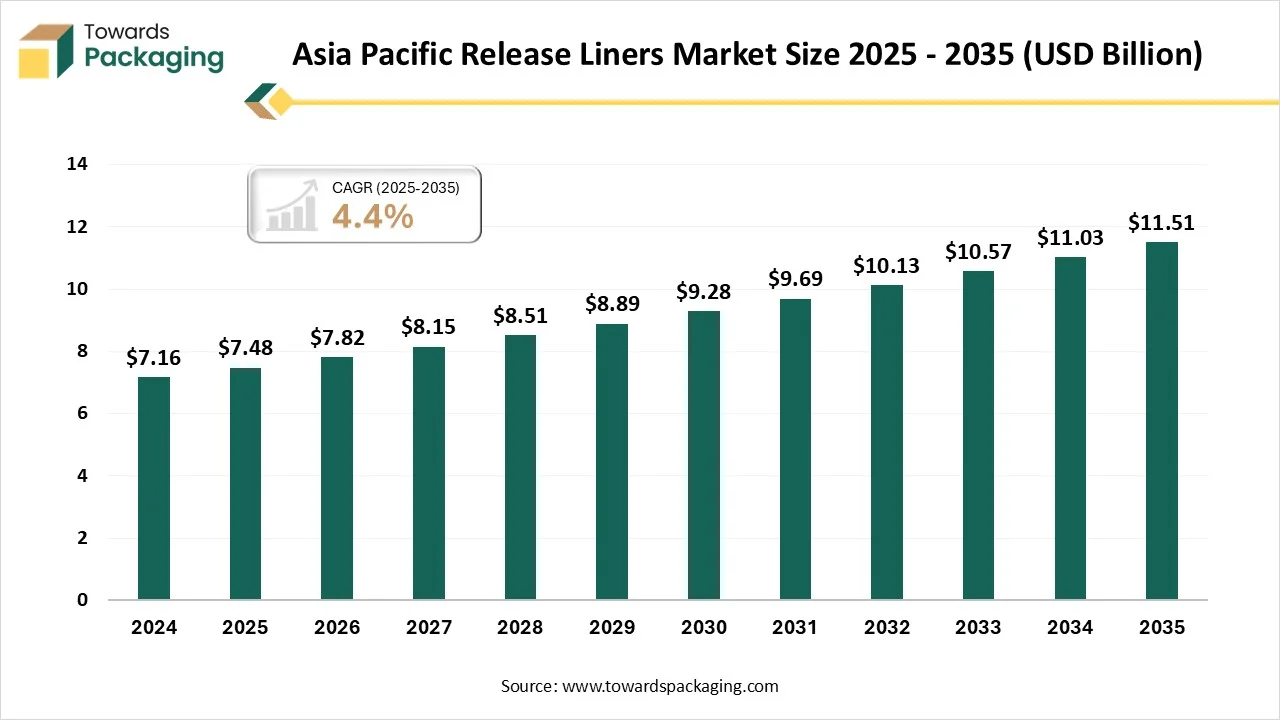

Asia Pacific dominated the release liners market in 2025 as the release liner industry is being driven by the fast industrialization, a rigid push towards sustainability, and the e-commerce sector too. The market is also finding ground demand from the main end-use industries like medical, packaging, and electronics. A growth in the packaging of consumer goods, pharmaceuticals, food, and beverages is fulfilling the urge for pressure-sensitive labels and tapes, which totally depend on release liners. Developed health consciousness and the usage of wound dressings, medical devices, and hygiene products like sanitary pads and diapers are driving the urge for high-performance release liners. The stretching of online retail has made a demand for reliable packaging materials and smoothness, mainly driving the demand for release liners for protective tapes and tables.

Release liners demand in India is due to sustainability, as rigid development on main technological advancements and end-user industries to develop performance. The Indian market is a dominant force in the huge Asia-Pacific region, which is due to growing urbanization, industrialization, and a rising consumer base. India is one of the fastest-developing regions for release liners, which is a trend that is predicted to continue. The industry will continue to be strengthened by its huge population and growing disposable incomes that drive the usage of packaged goods.

North America is expected to be the fastest growth during the forecast period. The North American market is rigid, with the United States being an initial driver because of high-level production capability and big healthcare, consumer goods, and automotive sectors. The rising demand for packaging across different industries, including food and beverage, is also boosting the market. The developing e-commerce industry is fulfilling the urge for reliable packaging solutions. Release liners are necessary for pressure-sensitive tapes and labels in shipping and logistics, which ensure that the product integrity is maintained.

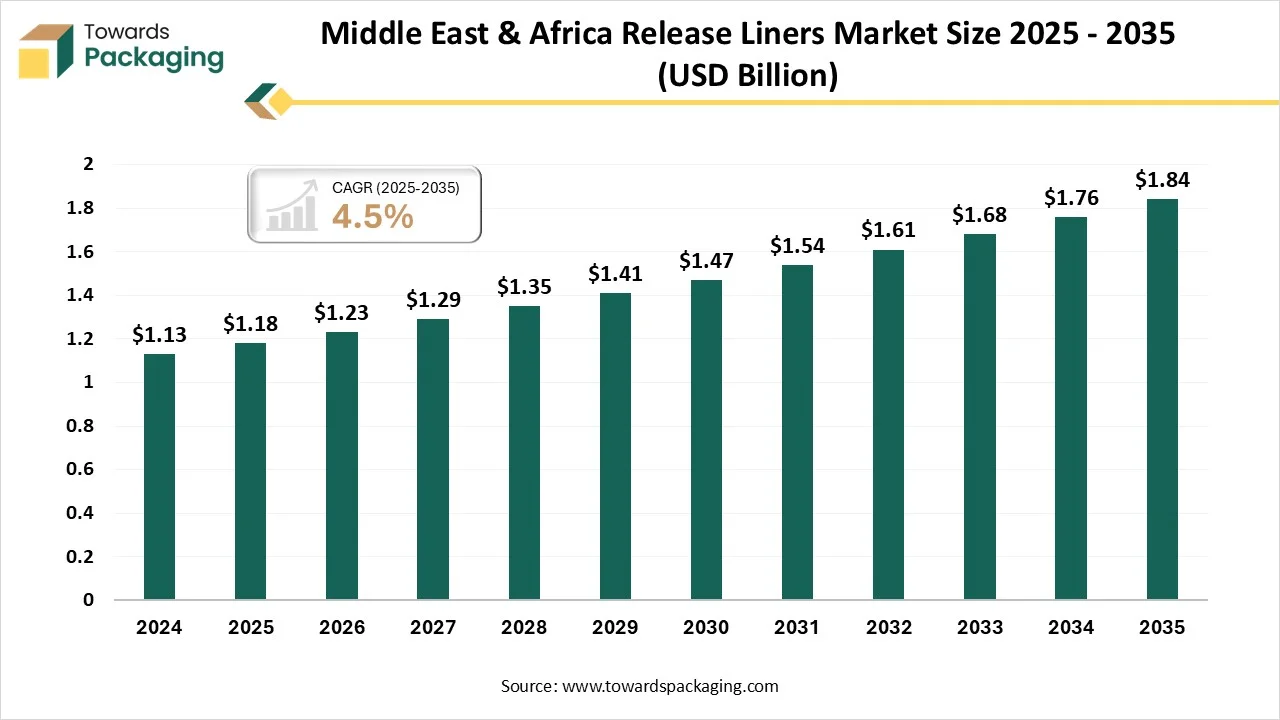

The release liners market in Canada is driven by the worldwide move towards performance, developed sustainability, and efficiency. The Canadian industry is due to the rising e-commerce industry, with high demand from the packaging and medical industries, and a rigid importance on eco-friendly solutions. User demand and strict environmental solutions. This technology, which avoids the liner completely, is gaining attention as a waste reduction and cost-saving measure that is specifically for high-volume uses in retail and food packaging, too.

Tier 1

Tier 2

Tier 3

By Material Type / Substrate

By Coating Type

By Application

By End-User Industry

By Revenue Model

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarRelease Liners Market