U.S. Packaging Market Size, Trends, Share and Innovations

The U.S. packaging market is forecast to grow at a CAGR of 4.01%, from USD 223.96 billion in 2026 to USD 319.04 billion by 2035, over the forecast period from 2026 to 2035. Market growth is driven by strong consumer goods demand, rapid expansion of e-commerce and omnichannel retail, increasing focus on sustainable and recyclable packaging, regulatory pressure on single-use plastics, and innovation in smart and lightweight packaging solutions.

The study further examines transportation and logistics performance such as shipping costs, handling time, and distribution efficiency, along with consumer demand patterns, regional preferences, and regulatory compliance related to sustainability and waste management. In addition, it includes competitive analysis of key companies, packaging innovation, and technology adoption such as automation, AI, and smart packaging, helping businesses understand market dynamics and identify growth opportunities in the U.S. packaging market.

Major Key Insights of the U.S. Packaging Market

- In terms of revenue, the market is valued at USD 223.96 billion in 2026.

- The market is projected to reach USD 319.04 billion by 2035.

- Rapid growth at a CAGR of 4.01% will be observed in the period between 2026 and 2035.

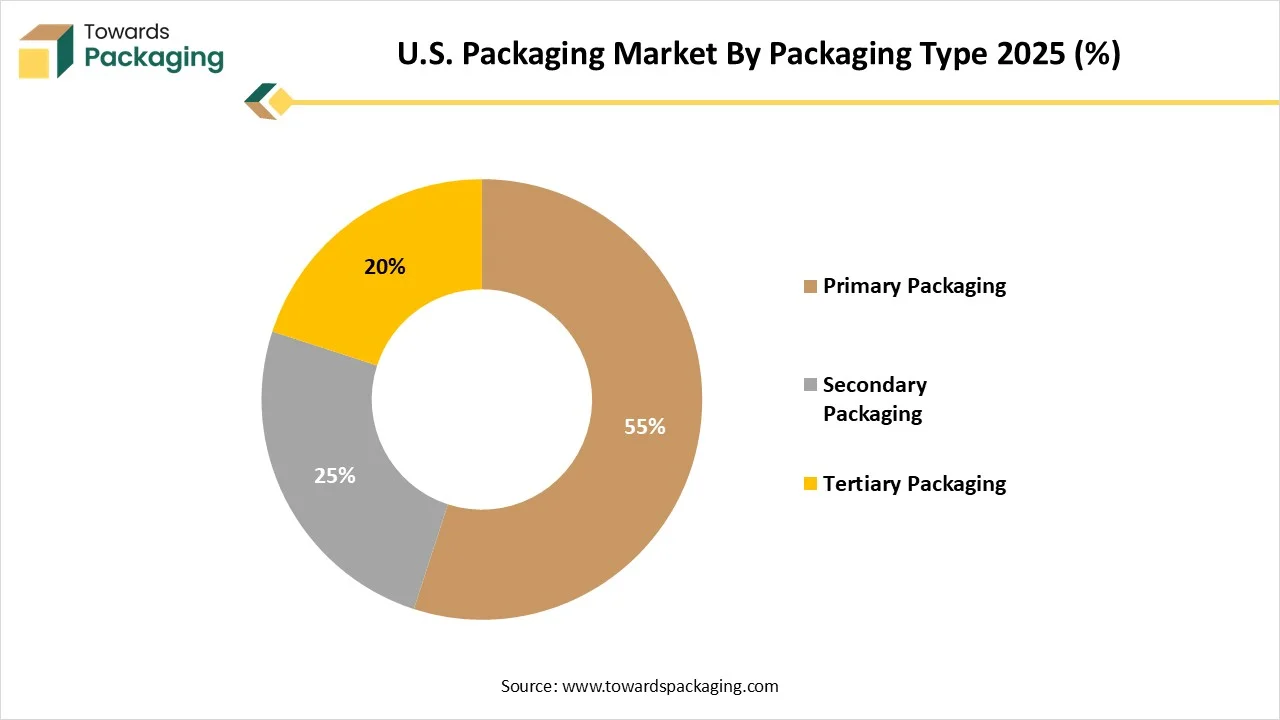

- By packaging type, the primary packaging segment has invested the biggest market share of approximately 55% in 2025.

- By packaging type, the secondary packaging segment will be expanding at a significant CAGR between 2026 and 2035.

- By material type, the paper & paperboard segment has contributed to the largest market share of approximately 40% share in 2025.

- By material type, the biodegradable/bio-based materials segment will be growing at a main CAGR between 2026 and 2035.

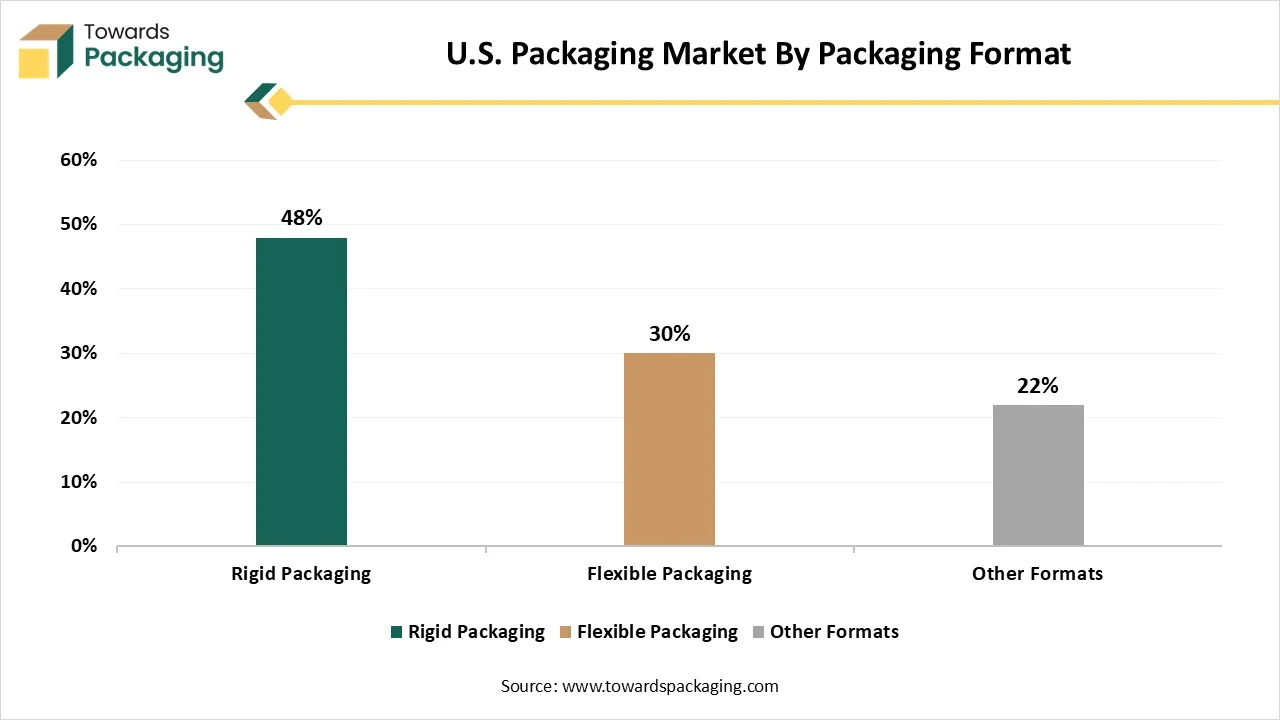

- By packaging format, the rigid packaging segment dominated with the biggest market share of approximately 48% in 2025.

- By packaging format, the flexible packaging segment will be expanding at a main CAGR between 2026 and 2035.

- By end-use industry, the food & beverages segment has contributed to the largest market share of approximately 38% in 2025.

- By end-use industry, the e-commerce & retail segment will be growing at a main CAGR between 2026 and 2035.

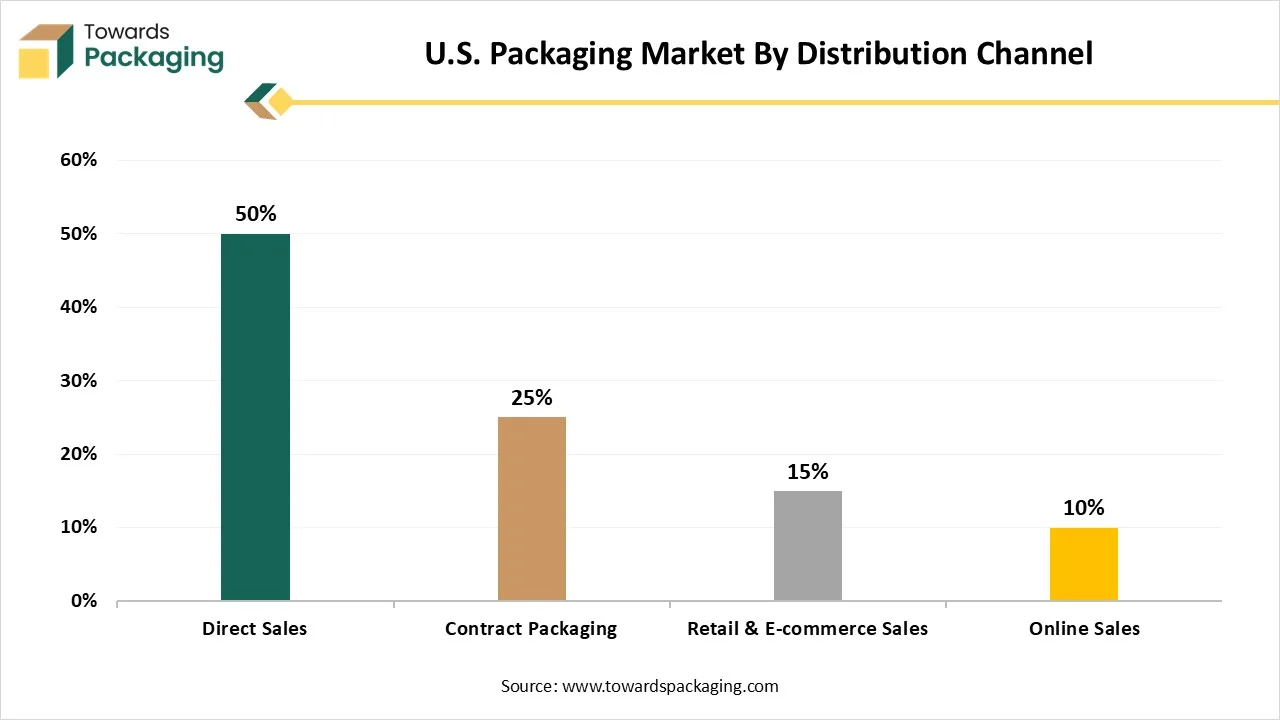

- By distribution channel, the direct sales segment has invested in the biggest market share of approximately 50% in 2025.

- By distribution channel, the contract packaging segment will be developing at a main CAGR between 2026 and 2035.

Market Overview

The U.S. packaging market encompasses materials, products, technologies, and services used to contain, protect, transport, store, and market goods across food & beverages, pharmaceuticals, consumer goods, industrial products, e-commerce, and healthcare sectors. The market includes primary, secondary, and tertiary packaging solutions made from paper & paperboard, plastics, metals, glass, and emerging sustainable materials

Trends in the U.S. Packaging Market

- Robotics and AMRS are developing productivity: Robotic technologies which counts autonomous mobile roots (AMR0 are fastly becoming more common in the packaging sector. Synch powerful solutions are crafted to develop productivity and lower the manual labor needed in the packaging procedure.

- Artificial Intelligence is developing data to update the packaging procedure: Artificial Intelligence is updating the path that brands request packaging. AI algorithms can manage a huge amount of data in order to update the packaging procedure, which makes it more smooth and lower the waste. Furthermore, AI can be utilised to manage and track the quality of the packaging procedure that make sure every products are being packaged to the decided standard.

- Smart Packaging uses and exploits real-time tracking data to ensure high quality: Smart packaging, which is also known as intelligent packaging, applies sensors and remaining technology in order to track and develop the packaging procedure. This counts the actual-time monitoring of the product quality, excessively accurate managing of the shipments of goods and the temperature management for sensitive items.

- Digital Transformation: Digital transformation is another common pattern that has a major effect on the packaging sector. By using the technologies, organizations can optimize and update their packaging procedure, by lowering the manual labor and improving the smoothness. This counts the usage of digital stages like to track shipments, manage orders and monitor the quality of the packaging process.

- Industry 4.0: Industry 4.0 linked to the fourth industrial update, that is being classified by the usage of technology to update and automate industrial procedures. The packaging sector is not left behind, and Industry 4.0 is changing the way that packaging organizations run.

- Sustainability: Sustainability is becoming crucial in the packaging sector and companies are seeking for different approaches in order to lower down the environmental effect. Automation can assist companies receive this by lowering waste, which updates the usage of materials and developing the smoothness of the packaging procedure.

- Market Growth Overview: The U.S packaging industry is stretching because of growing e-commerce, developing user demand for convenience and the sustainable options like paper/cardboard, also a demand in the food and beverages industry that has encouraged the new regulations for the eco-friendly materials.

- Global Expansion: The worldwide expansion of the U.S. packaging sector is being classified by strong cross-border partnerships, a strategic move towards the development that grows the industry and management at a high level, sustainable, and “smart’ packaging technologies.

- Major Market Players: The main market players in the U.S. packaging sector are Ball Corporation, Berry Global, C-P Flexible Packaging and Georgia-Pacific LLC too.

- Startup Ecosystem: The U.S. packaging startup ecosystem is a developed but excessively inventive scenario that has over 177 focused packaging tech startups and a huge link of 21,180 startups which invest to the overall sector. The ecosystem is initially dominated by a move towards automation, sustainability and the smart technology too.

Technological Developments of the U.S. Packaging Market

The advantages of smart technology are various such as expanding shelf life, to develop product security and polishing user engagement and loyalty too. Technology not only develops the consumer experience, but also serves insightful data to the organizations for product development and marketing. Smart packaging transformations and updates count elements that deliver consumers with quick permission to promotional events, product information, and more. Furthermore, smart packaging includes tracking numbers and barcodes to assist developed inventory management and the supply chain transparency. These factors help the organizations manage their items with the assistance of distribution procedure, whose aim is to precisely deliver and to lessen the overall loss.

Trade Analysis of U.S. Packaging Market: Import & Export Statistics

- Worldwide, the leading three importers of the US Packaging are Colombia, Vietnam and Russia.

- Vietnam has topped the globe in the US packaging which has imported with 3,092,064 shipments , which is being followed by Colombia that has 384,049 shipments and the Russia who has taken the third position with 203,304 shipments.

- As per the global data, the globe has imported 2,281,783 shipments of US packaging during the period June 2024 to May 2025. Such imports were being supplied by 106,534 exporters to 82,720 worldwide buyers, which has marked an overall development rate of 40% as compared to the leading twelve months.

- In May 2025 alone, the globe imported 188,809 US Packaging shipments.

U.S. Packaging Market - Value Chain Analysis:

Raw Material Sourcing:

Packaging raw materials play an important role in the production of a huge series of items. By completely understanding the characteristics and applications of prevalent plastic raw materials like polypropylene, polyethylene, polystyrene, and PVC, producers can make informed decisions regarding the materials they use in their products.

- Key Players: Huhtmaki Oyj, Graphic Packaging Holding Company, and Packaging Corporation of America.

Component Manufacturing:

Manufacturers take extreme care in the production of packaging materials.This incudes everything right from selection and acquisition of the raw elements to the growth of final packaging items that make sure product safety. Additionally, another complicated factor that manufacturers include into their packages is hazard warning. Such labels play an crucial role in user awareness by alarm consumers about any capable risks linked with the product integrated inside the package.

- Key Players: Sonoco Products Company, Mondi Group and WestRock Company.

Logistics and Distribution:

The logistics sector is continuously developing, with the packaging materials that has players an important role in making the future of commerce. Organizations that include sustainable packaging solutions can lower down the eco-friendly effect, that develops brand reputation, and develop customer commitment. The progress of packaging materials in current logistics displays a latest era of partnerships and inventions, which is driven by a loyalty to smoothness and sustainability.

- Key Players: Silgan Holdings Inc., O-I Glass Inc., and Printpack, Inc

Packaging Type Insights

")

Why the Primary Packaging Segment Dominated the U.S. Packaging Market In 2025?

The primary packaging segment has dominated the market with approximately 55% share in 2025, as primary packaging, which is also known as retail or user packaging, links to the primary layer of the packaging that directly meets the product. The main aim of primary packaging is to secure the product from impairment white protecting its quality. It also plays a main role in serving necessary details like expiration dates., ingredients , usage instructions and lastly product identification.

The secondary packaging segment is expected to experience the fastest CAGR during the forecast period. This kind of packaging encircles and has one or more primary packages, which may not touch the product directly, but they play an important role in terms of bundling, branding, and distribution, too. It grants in stocking, handling and retail display too. Its initial function is to organize and include several primary packages, which makes them convenient to handle, transport, and showcase. For instance, enhanced protection, retail display, visual branding and product grouping too.

Material Type Insights

| By Material Type Segments |

Market Share 2025(%) |

| Paper & Paperboard |

40% |

| Plastics |

30% |

| Metals |

15% |

| Biodegradable/Bio-based Materials |

10% |

| Other Materials |

5% |

Why the Paper & Paperboard Segment Dominated the U.S. Packaging Market In 2025?

The paper & paperboard segment has dominated the market with approximately 40% share in 2025, It delivers the aim of protecting, containing , transporting and showcasing the products. Apart from being a simple outer layer, paper packaging is becoming a mark of green lifestyle and sustainable usage trends. Paperboard is a lightweight and rigid packaging material that is made of wood pulp or recycled paper pulp. It is thicker than regular paper but not as bulky as cardboard, which makes it perfect for packaging ignitor products or making more complex unboxing experiences.

- In October 2024, Southwest Airlines substituted its serving plastic cups, which were utilized to give cold beverages at the time of flights, with the latest cups created with a pulp mixture of 75% bamboo and 25% paper.

The biodegradable & bio-based materials segment is predicted to witness the fastest CAGR during the forecast period. Biodegradable packaging is a kind of packaging created from natural, renewable materials which can decompose securely in the surrounding. Biodegradable packaging materials are being crafted to be broke down by micro-organisms into the natural elements like as carbon dioxide, water and organic matter. There are 10 types of biodegradable materials, such as polylactic acid, cellulose-based films, starch-based bioplastics, mushroom mycelium packaging, chitosan, etc. On the other hand, bio-based materials are completely, or half made from biological resources instead of fossil based raw materials.

- In May 2025, Futamura, which is a flexible packaging transformer Repaq and machine generator GK Sondermaschinenbau that has partnered to generate a compostable packaging cover for the liquid sachet segment. This laminate is totally dependent on NatureFlex technology and can pack ingredients like mustard or ketchup , hand cream or cooking sauces too.

Why Rigid Packaging Segment Dominated the U.S. Packaging Market In 2025?

The rigid packaging segment has dominated the market with approximately 48% share in 2025 as this packaging has still maintained its form and shape, which exhibits no or restricted elastic deformation, and is usually self-assisting and separate too. Rigid plastics are most greatly used in food and beverage packaging uses. This developing urge rigidly depends on growing usage that is owed to the rising population and demographic changes. Also, transforming demographics such as urbanization, the acceptance of sedentary lifestyle and growing single-income households markets the usage of easy packaging in small-serve packages.

The flexible packaging segment is predicted to witness the fastest CAGR during the forecast period. This packaging points to any packaging created of plastic or flexible materials. The initial leading element of the flexible packaging is its adaptability. Additives like polyvinyl chloride (PVC), ethylene vinyl alcohol, and aluminium foil can be used as flexible packaging materials. This flexibility means that it can be utilized for a huge range of products, right from food packaging to medical goods. Also, from pet food to personal care items and household items, flexible packages can be personalized to align with an organization's branding or functional design as well as practical demands, which makes these items attention-grabbing at the point of purchase.

- In May 2025, Oroville Flexible Packaging LLC, which is also an RE: CIRCLE Solutions organization and a leader in terms of flexible plastics and the packaging solutions for foodservice and retail customers, revealed that the official launch of “Oroflex” is a sustainable flexible plastics, recycling, and packaging machine.

End-User Insights

| By End-Use Industry Segments |

Market Share 2025(%) |

| Food & Beverages |

38% |

| Pharmaceuticals |

18% |

| Personal Care & Cosmetics |

15% |

| Household Goods |

10% |

| E-commerce & Retail |

12% |

| Industrial & Chemicals |

7% |

Why the Food & Beverages Segment Dominated the U.S. Packaging Market In 2025?

The food & beverages segment has dominated the market with approximately 38 % share in 2025. Lines should make sure flexibility, food safety and constant manufacturing that accepts fast to latest designs and developing sustainable materials. Bioplastics, compost solutions and high-performance papers are extensively substituting regular selections. Also, predictive monitoring software, which is assisted by sensors and real-time data analysis, allows companies to detect failures, lessen waste and energy usage, and update performance too.

- In May 2025, KIND snacks, a brand known for its nutritious and tasty snacks, launched its primary curbside recyclable paper cover pilot in the U.S.

The e-commerce & retail segment is predicted to witness the fastest CAGR during the forecast period. The US remains the second biggest e-commerce market globally, after China. This huge valuation displays a developed but still growing sector with a huge spread of internet entry, digital payment acceptance, and smartphone usage, too. Additionally, online sales have shown approximately 20% of all retail transactions, as this ratio has jumped rapidly over recent years, exacerbated by the COVID-19 pandemic, which has constantly shifted several shoppers' choices to online channels. The move towards digital shopping is no longer a core competency but crucial, with each one in five retail dollars being spent online.

Distribution Channel Insights

Why Direct Sales Segment Dominated the U.S. Packaging Market In 2025?

The direct sales segment has dominated the market with approximately 50% share in 2025 as producers are heavily serving tailored e-commerce solutions like high-barrier films and the tailored mailers to assist the expanding DTC industry. Regular sales designs are experiencing pressure, so organizations are shifting away from “order-taking” in the direction of insight-driven selling to reconstruct buyer loyalty. Brand owners now have long-term sustainability that concentrates directly in their procurement activities.

The contract packaging segment is predicted to witness the fastest CAGR during the forecast period. There are very strict laws like the Drug Supply Chain Security Act (DSCSA) for the pharma and latest FDA which is front-of-pack labelling rules in terms of food drive which is a constant demand for expert serialization and relabelling services. Also, the demand in online retail has passed the urge for updated logistics and secondary packaging too.

Country-Level Insights

As sustainability becomes an issue across the world, the U.S. packaging sector is witnessing a transformative shift. With growing user alertness, rigid environmental regulations, and fast invention, sustainable packaging is not only one of the but a crucial industry in current landscape. Sustainable packaging links to packaging solutions that dismiss the eco-friendly effect by using materials that are biodegradable, recyclable, or compostable, which are created from renewable sources.

Conventional materials count HDPE plastics and recyclable PET, cardboard, paper, PLA ( a starch-based polymer), and cellulose. Hence, federal agencies like the U.S. Environmental Protection Agency (EPA) which are entering in with policies to reduce the single-use plastics and market sustainable alternatives. Such efforts are assisting producers accept green packaging solutions without embracing the complete financial load.

- In December 2025, Tjopack, which is a contract packaging company, disclosed that it has expanded its packaging services and the operational footprint in the United States, with the latest 170,000 sq. ft availability to be constructed next to the company’s current site in Clinton, Tenn.

Partnerships and Deals in the U.S. Packaging Market

- In October 2025, Emerald Packaging, the biggest supplier of retail flexible packaging for the product sector, in collaboration with Wada Farms, Idaho Package, and Walmart, revealed the primary 30% Post-Consumer Recycled (PCR) in food contract with respect to the potato category.

- In July 2025, a private equity company that is in growth equity funding in the healthcare industry and life sciences is named Ampersand Capital. It has revealed the partnership of CurTec Group B.V., a Netherlands-based producer of high-performance plastic packaging options for specialty chemical uses and pharmaceutical chemical uses, in collaboration with the management of Bencis Capital Partners.

Recent Developments

- In December 2025, FUJIFLM Corporation disclosed ZEMATES, which is the latest brand of photosensitive insulating materials in terms of semiconductor back-end procedure, with a center point on the polyimide.

- In December 2025, UPM disclosed UPM Circular Renewable BlackTM, which is an innovative invention that updates the role of black as a color in terms of sustainable packaging. It is the globe‘s first bio-based, carbon-negative, and infrared detectable material that allows luxury packaging solutions that integrate design perfection with complete recyclability and rigid sustainability performance.

- In December 2025, Demeter's Pantry will disclose the revelation of many user favourites in terms of Metalogic stage with the latest sustainable packaging and developed micro-nutrient labels. Every item is created from scratch, in-house, right from the sauces and proteins to beans and grains, by only using the clean-label products.

Top Companies in the U.S. Packaging Market

- International Paper: International Paper is one of the top biggest and top fiber-based packaging sectors. Its headquarters are 6400 Poplar Ave, Memphis, TN 38197, USA. The organization is a top leader in user packaging, protective packaging, and industrial products, and the displays, too.

- Elite Custom Boxes: Elite Custom Boxes is one of the huge industrial packaging organization in the globe. The main goal of this packaging is its users satisfaction as they are heavily dependent to their creative packaging making that aligns well with each demand of customers.

- Avery Dennison Corporation: Avery Dennison Corporation has an big history in terms of success and invention. They are in the top position in terms of pressure-sensitive adhesive materials and the apparel branding solutions that have over 200 locations around the globe.

- Amcor: Amcor is a top packaging server that producers and distributors have a big range of products and services. Their services count rigid plastic containers, closures, flexible packaging materials , specialty cratons and the services like as labelling, printing and shrink sleeve uses too.

- Packaging Corporation of America: Packaging Corporation of America is one of the top manufacturers of corrugated packaging items in the United States. They deliver a huge range of products and services, which range from regular corrugated boxes to complicated shipping containers for industrial uses.

- Vertiv Corporation: This organization serves an overall array of paper, packaging, and facility solutions. They allow their users to stand firmly in the current competitive business environment.

- Graphic Packaging International: Graphic Packaging International is one of the leading companies in the packaging sector. It is the perfect solution giver with a big network of service centres throughout North America as well as overall expansion in Europe, South America and Asia too.

- Urgent Boxes: Urgent Boxes is located in the U.S. and offers tailored initial-rate custom packaging solutions with a concentration on fast shift and reliability, too. It serves a huge range of packaging types, which includes cosmetics, food, e-commerce, and retail, too.

- Eagle Flexible Packaging: Eagle flexible packaging is a professional in innovative flexible packaging solutions, such as roll-fed film, pre-designed pouches, and laminate structures.

- Good Start Packaging: They are an sustainable packaging solution company who are specialists in environment-friendly unchangeable packaging for a variety of industries. The company also concentrates on environmental and innovation responsibility, which serves goods produced from biodegradable, compostable, and recyclable materials.

U.S. Packaging Market Segments Covered

By Packaging Type

- Primary Packaging

- Secondary Packaging

- Tertiary / Transport Packaging

By Material Type

- Paper & Paperboard

- Plastics

- Metals

- Glass

- Biodegradable / Bio-based Materials

By Packaging Format

- Rigid Packaging

- Bottles & Jars

- Cans & Containers

- Flexible Packaging

- Pouches

- Films & Wraps

- Semi-Rigid Packaging

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Consumer Goods & Personal Care

- Industrial & Chemicals

- E-Commerce & Retail

- Electronics

By Distribution Channel

- Direct Sales (Brand Owners / Manufacturers)

- Packaging Distributors

- Contract Packaging (Co-Packers)

- Online / E-Procurement Platforms