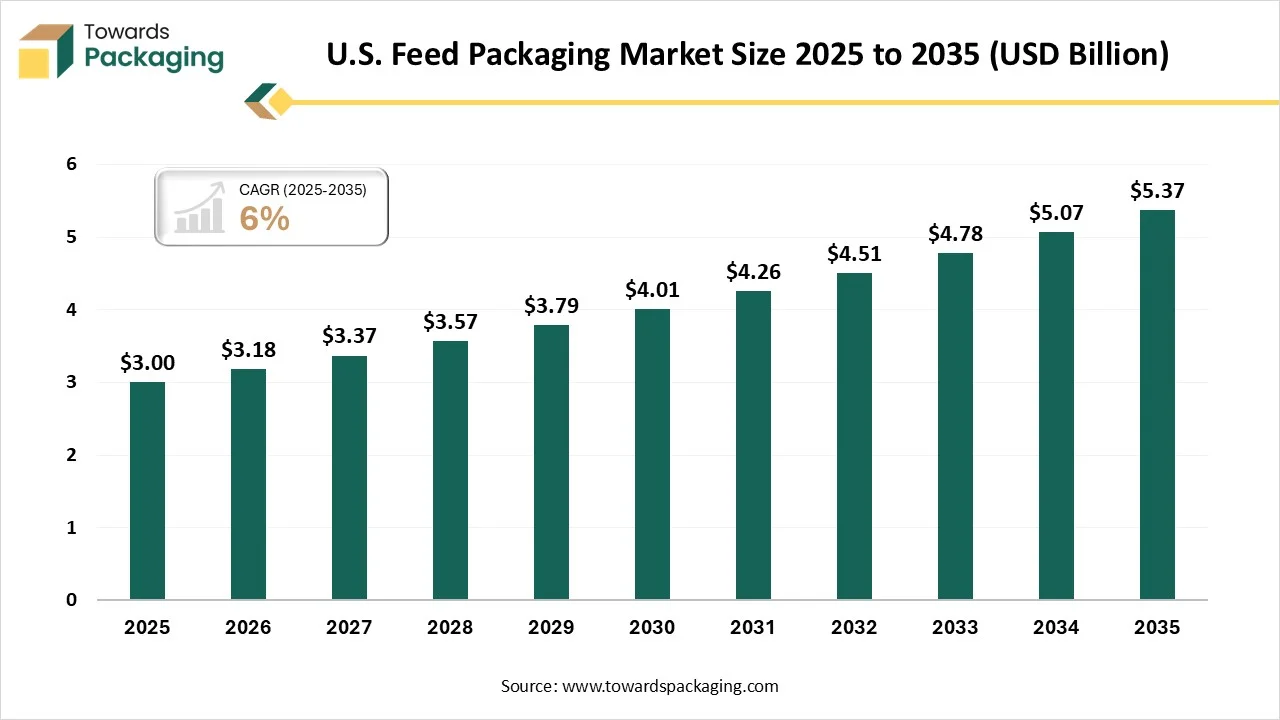

The U.S. feed packaging market is expected to grow from USD 3.18 billion in 2026 to USD 5.37 billion by 2035, expanding at a CAGR of 6% during 2026-2035. The market study provides detailed insights into market size, segment performance, regional trends, and demand patterns across the United States. It also highlights the growing demand from the pet food, livestock, and poultry industries, which is driving the need for durable, flexible, and sustainable packaging solutions for longer storage periods. The report further covers competitive analysis, company profiles, manufacturers and suppliers data, value chain analysis, and trade statistics, offering a complete view of the industry landscape.

U.S. feed packaging states to the focused resources and vessels mainly multi-wall paper, woven polypropylene (BOPP) bags, and plastic vessels utilized to protect, store, and transport pet food and animal feed from spoilage, moisture, and contamination. BOPP bags (biaxially-oriented polypropylene) are highly preferred for being moisture-barrier, robust, and printable. Several other types include bulk bags, multi-wall paper bags, plastic tubs and totes for liquids.

Technological transformation in the U.S. seed packaging market plays a significant role by developing mono-material flexible packaging films. Presence of strict ecological guidelines has fuelled the development of sustainable packaging solution. Enhanced technology such as sensors, antimicrobial agents, and moisture regulator has pushed this market to develop active and smart packaging for food storage and transportation. Incorporation of automation in this industry has reduced labour charge which has resulted in the production of cost-effective packaging solution. Modified atmosphere packaging technology lowers the growth of microbes and support in maintaining the integrity of the food products.

The major raw materials utilized in this market are polypropylene, polyethylene, paperboard, paper, bio-based materials, lignin, and cellulose. Post-consumer recycled plastics has raised the adoption of eco-friendly packaging.

The component manufacturing in this market comprises woven polypropylene sacks, liners and component, pouches and flexible films, flexible intermediate bulk containers, and multi-wall paper bags.

This segment ensures enhanced supply chain traceability with advanced coding technologies. It supports advancement in traceability, compliance, and distribution technique.

The plastic segment dominated the market with highest share in 2025 due to superior protective barriers, durability and cost-effective solution. Plastic offers an important barrier against oxygen, external contaminants, moisture, and UV rays. This is important for preserving the dietary value and stopping degeneration of animal feed which is stored for longer periods or shipped long distances. The lightweight plastic arrangements support decrease fuel ingesting and logistics expenditures, which is important in this industry handling bulk supplies.

The paper & paperboard segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to its recyclability, sustainability, and renewability. These are versatility, cost-effectiveness, and huge durability for both livestock sacks and pet food coagulated this market management. The urgent requirement for environment-friendly, recyclable, and biodegradable sustainable to plastic influence the change in the direction of paperboard. Paperboard provides excellent printability for branding, cost-effectiveness, and advanced coatings which is necessary for moisture resistance.

The flexible segment dominated the market with highest share in 2025 due to high-performance barrier properties, cost-efficiency, and lightweight nature. It provides high-barrier possessions, preventing feed from light, moisture, and oxygen, thus confirming longer shelf life. Acceptance of environment-friendly, bio-based, and recyclable plastics permits producers to fulfil strict sustainability guidelines. These are mono-material, high-barrier, and recyclable pouches planned to decrease ecological impact.

The rigid feed packaging segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to structural integrity and superior durability. It is influenced by both trade-scale livestock processes necessitating durable storage and customers looking for premium as well as safe packaging for pets.  It is crucial for products necessitating maximum fortification and shelf-life constancy. These containers are structured to endure the inflexibilities of logistics and distribution chains, preserving product quality and protecting from damage.

The livestock feed segment dominated the market with highest share in 2025 due to increasing requirement for bulk production process. Long supply chains and heavy weight starting from feed mills till the farms, it needs durable as well as high-capacity packaging. Bulk containers and large-format bags provide the most inexpensive way of packaging and allocate feedstuff at scale. Hygiene have boosted the producers to accept tamper-proof, advanced, and moisture-barrier packaging to stop contamination and confirm feed quality.

The aquatic feed packaging segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to rapid aquaculture growth and specialized preservation requirement. It is increasing significantly to fulfil the growing seafood demand as it is considered as sustainable source for protein. Aquatic feeds sometimes contain specialized nutrients and high protein. It has raised the demand for finest, high-digestibleness feeds that need focused packaging. It influences the requirement for new, advanced packaging arrangements to confirm product quality.

The bags segment dominated the market with highest share in 2025 due to its compatibility and cost-effectiveness. Bags are chosen for handling, storage, and transportation of commercial farms which is offering high-volume capacity and durability. They offer an economical option that preserves product quality, comprising moisture resistances to defend against ecological factors. Producers are improving bags with sturdier seals, enhanced stacking potentials, and better printing choices for branding. They provide to both huge-scale profitable livestock and refined formats, the rising pet food sector.

The pouches/pockets segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to its convenience, reusability, and luxury packaging potential. The rapid growth of online retail sector for pet foods demands packing that is durable, cost-effective and lightweight for transportation. Pouches are stretchy, decreasing transportation charges and storing space which is making them a favored option for producers looking to decrease their carbon footprint. Current pouches include features such as tear notches, spouts, and zippers which enhance user suitability, and progressive barrier packaging films that enhance shelf life.

The dry feed segment dominated the market with highest share in 2025 due to its cost-efficiency, stability and convenience. It is convenient to transit, handle, and store which is making it the ideal option for both pet owners and commercial livestock. It is commonly more affordable to yield and purchase over wet feed substitute. The need to keep dry feed innocuous from contamination and moisture requires particular packaging, mainly woven polypropylene sacks and multi-layer paper bags.

The chilled & frozen segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to protective, sustainable, and specialized packaging. Enhanced the demand for raw-meat-based pet diets or high-end, fresh, requires progressive packaging that preserves nutritional worth and freshness. The acceptance of flexible, sustainable packaging option offers excellent protection, decreases waste, and improves shelf appeal. Customers are deeply demanding environment-friendly, sustainable, and recyclable packaging which is forcing producers to invent in the frozen and chilled industries.

U.S. witnessing rapid growth in the feed packaging market, due to its sustainability and technological innovation. Producers are causing the sustainable packaging, utilizing flexible, high-resistance, and durable resources to defend feed from contamination and moisture. Industries are concentrating on bulk packing for agricultural efficacy and dedicated, advanced packing for the rising pet food sector. Huge demand for, suitability, and durable packing for long distribution chains from farms and feed mills.

By Material

By End Use

By Packaging Format

By Feed Type

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarU.S. Feed Packaging Market