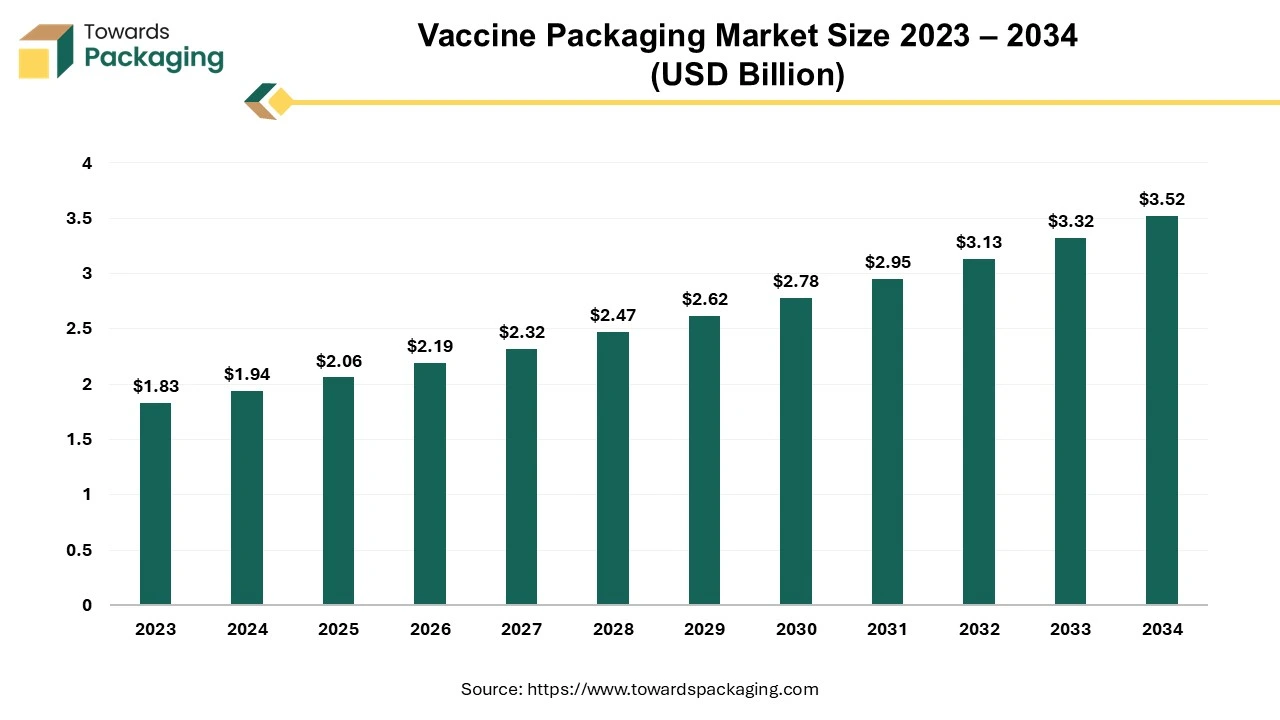

The vaccine packaging market is forecasted to expand from USD 2.19 billion in 2026 to USD 3.74 billion by 2035, growing at a CAGR of 6.14% from 2026 to 2035. This report presents detailed segments by material, type and end‑use; regional data covering North America, Europe (which held ~37.75% share in 2024), Asia Pacific (expected fastest CAGR ~8.29%), Latin America and MEA; profiles of leading companies (such as Schott AG, Gerresheimer AG, Stevanato Group, SGD Pharma); a full competitive analysis; value‑chain mapping from rawâ€materials to finished packaging; trade data on import/export flows; and detailed manufacturer & supplier insights.

The vaccine packaging market is set to expand substantially over the forecast timeline. Innovations in vaccine packaging may have an effect on user acceptance and adoption as well as the supply chain. The benefits of these innovative package designs for public health are evident in their simplicity in use, increased safety, and improved logistics of supply and uptake that creates new chances for vaccination. Furthermore, there appears to be strong user acceptance at the national level. Stakeholders worldwide are interested in two packaging innovations currently that are the dual-chamber delivery devices and the compact pre-filled auto-disable devices (CPADs).

The rising incidence of infectious diseases, such as influenza, measles and COVID-19 along with the growing global immunization programs is expected to augment the growth of the vaccine packaging market during the forecast period. Furthermore, the advancements in biotechnology as well as the expansion of the cold chain logistics sector driven by the need to transport temperature-sensitive vaccines safely are also anticipated to augment the growth of the market.

Additionally, the rising investments in healthcare infrastructure and the shift toward single-dose vaccines is increasing the demand for unit-dose packaging formats is also projected to contribute to the growth of the market in the years to come.

| Metric | Details |

| Market Size in 2025 | USD 2.06 Billion |

| Projected Market Size in 2035 | USD 3.74 Billion |

| CAGR (2026 - 2035) | 6.14% |

| Leading Region | Europe |

| Market Segmentation | By Material, By Type, By End-Use and By Region |

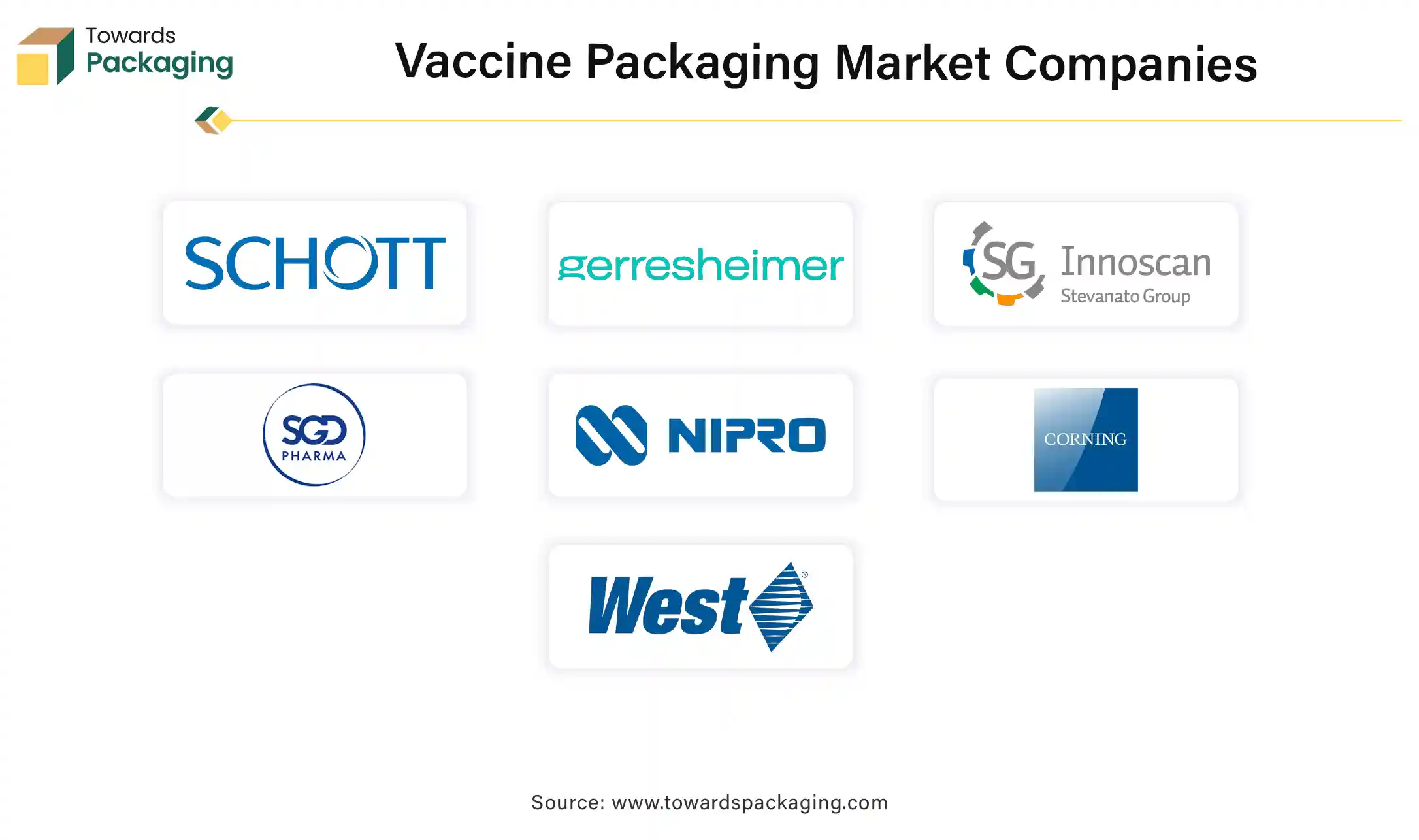

| Top Key Players | Schott AG, Gerresheimer AG, Stevanato Group, SGD Pharma |

Artificial Intelligence (AI) has already integrated itself into the healthcare and pharmaceutical industry in the last few years. It is being widely used in drug development and processing vast amounts of data to help researchers work smarter and faster. The vaccine packaging industry has been slowly finding applications for AI into their infrastructure. AI helps improves overall efficiency of operations, that helps in streamlining production processes. Consistent quality and anomaly detection can be accomplished by utilizing AI-based technologies.

With any health-related packaging, regulation compliance plays an important part. AI can ensure that all compliances are being met during the production with quality control. Supply chain optimization is crucial to conduct proper logistics as these are essential goods. AI combined with Internet of Things (IoT), can help track and optimize routes for delivery ensuring the process runs smoothly. Artificial Intelligence’s full potential is yet to be explored in the vaccine packaging industry and is anticipated to help this market’s growth during the forecast period.

The expansion of vaccine production capacities is expected to fuel the growth of the vaccine packaging market within the estimated timeframe. This is owing to the rise of infectious diseases, pandemics like COVID-19 and the need for routine immunization programs. Thus, pharmaceutical companies and governments are rapidly increasing their vaccine production capacity.

For instance,

These expansions are not just aimed to fulfill urgent demands, but also to prepare for possible future pandemics and epidemics. As manufacturing capacity increases, so does the demand for efficient, dependable and scalable packaging. The increase in production, particularly in developing countries, is likely to drive the demand for high-volume packaging materials such as vials, prefilled syringes and ampoules.

The disruptions in the global supply chain for raw materials like glass, plastics and polymers is expected to limit the growth of the market during the forecast period. Geopolitical issues such as the war in Israel, the US-China rivalry, the Russian invasion of Ukraine and elections, had a substantial impact on the global supply chain, particularly on the essential raw materials used by numerous industry verticals. Sharp price increase and the production delays across industries are being caused by constraints on the supplies of certain raw materials, mainly polypropylene (PP), polyethylene (PE) and monoethylene (MEG). These chemicals are utilized to make plastics that are found in almost every type of the product such as equipment and packaging.

Moreover, global epidemics and the possibility of new variations increasing could result in labor shortages and border closures that worsen interruptions to the packaging material supply chain. All of these factors focus on the complicated connection that exists among geopolitical stability and the seamless functioning of international supply networks in the packaging industry.

Furthermore, the daily operations of plastics manufacturing firms as well as other organizations outside the sector have been directly impacted by these issues with the raw material supply chain. This material is utilized for manufacturing a multitude of products considered essential for health and wellbeing such as gloves, syringes and medical equipment. This industry is directly and severely impacted by the disruption in the supply chain today. Additionally, the lack of resin has led to an increase in the resin costs globally. Pharmaceutical companies sometimes bear the burden of these higher costs, which may restrict their capacity to mass-produce packaging for vaccines. Consequently, the market's capacity to grow is limited by the general instability of the supply chain, especially in regions with inadequate infrastructure.

The developments and advancements in the vaccine technologies are anticipated to augment the growth of the vaccine packaging market in the near future. The landscape of vaccine production has changed due to the emergence of novel immunization techniques as viral vector and mRNA vaccines. A recent advancement incorporates the successful application of mRNA as a protective vaccination. The addition of 5' Kozak and cap sequences, 3' poly-A sequences, codon optimization, altered nucleosides to increase mRNA stability and reduce detection by innate immune cell receptors, intradermal injection to minimize the RNA degradation and the production of thermostable mRNA are some of the methods that can increase the effectiveness of mRNA vaccines.

Some of the recent developments in the new vaccines include

The packaging sector is likely to gain from the growing complexity of vaccines as they continue to develop, creating a higher need for specialized, cutting-edge, and dependable packaging options. This trend presents substantial opportunities for packaging companies to innovate and provide value-added solutions for the next generation of vaccines.

| Rank | Company | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | SCHOTT Pharma | Mainz | Germany | Global leader in pharmaceutical glass and vaccine packaging | Glass vials, syringes, cartridges |

| 2 | Gerresheimer | Düsseldorf | Germany | Leading supplier of vaccine containment solutions | Glass vials, prefilled syringes |

| 3 | Stevanato Group | Piombino Dese | Italy | Major provider of integrated drug containment systems | Vials, syringes, cartridges |

| 4 | West Pharmaceutical Services | Exton, Pennsylvania | USA | Global leader in elastomer closure systems for injectable drugs | Stoppers, seals, containment systems |

| 5 | SGD Pharma | Paris | France | Leading manufacturer of molded and tubular pharmaceutical glass | Glass vaccine vials |

| Rank | Company | Headquarters | Country | Why Relevant | Key Packaging Products/Services |

| 1 | Nipro | Osaka | Japan | Strong portfolio of pharmaceutical containers | Glass vials, syringes |

| 2 | Corning | Corning, New York | USA | Developer of pharmaceutical glass technologies | Valor Glass vials |

| 3 | Datwyler | Altdorf | Switzerland | Pharmaceutical elastomer packaging components | Rubber stoppers and seals |

| 4 | Aptar Pharma | Le Vaudreuil | France | Injectable drug delivery and packaging solutions | Closures and drug delivery systems |

| 5 | Terumo | Tokyo | Japan | Prefilled syringe systems for vaccines | Syringes and injection systems |

| Rank | Company | Headquarters | Country | Why Relevant | Key Packaging Products/Services |

| 1 | DWK Life Sciences | Mainz | Germany | Pharmaceutical glass containers | Glass vials and bottles |

| 2 | Bormioli Pharma | Parma | Italy | Primary pharmaceutical packaging | Glass and plastic packaging |

| 3 | TekniPlex Healthcare | Wayne, Pennsylvania | USA | Medical packaging components | Seals, films, packaging materials |

| 4 | Cold Chain Technologies | Franklin, Massachusetts | USA | Cold-chain vaccine shipping solutions | Thermal packaging systems |

| 5 | CSafe | Monroe, Ohio | USA | Temperature-controlled vaccine transport | Reusable insulated shipping containers |

Some of the key players in vaccine packaging market Schott AG, Gerresheimer AG, Stevanato Group, SGD Pharma, Nipro Corporation, Corning Incorporated, West Pharmaceutical Services, Inc., AptarGroup, Inc., Becton, Dickinson and Company (BD), and Catalent, Inc., among others.

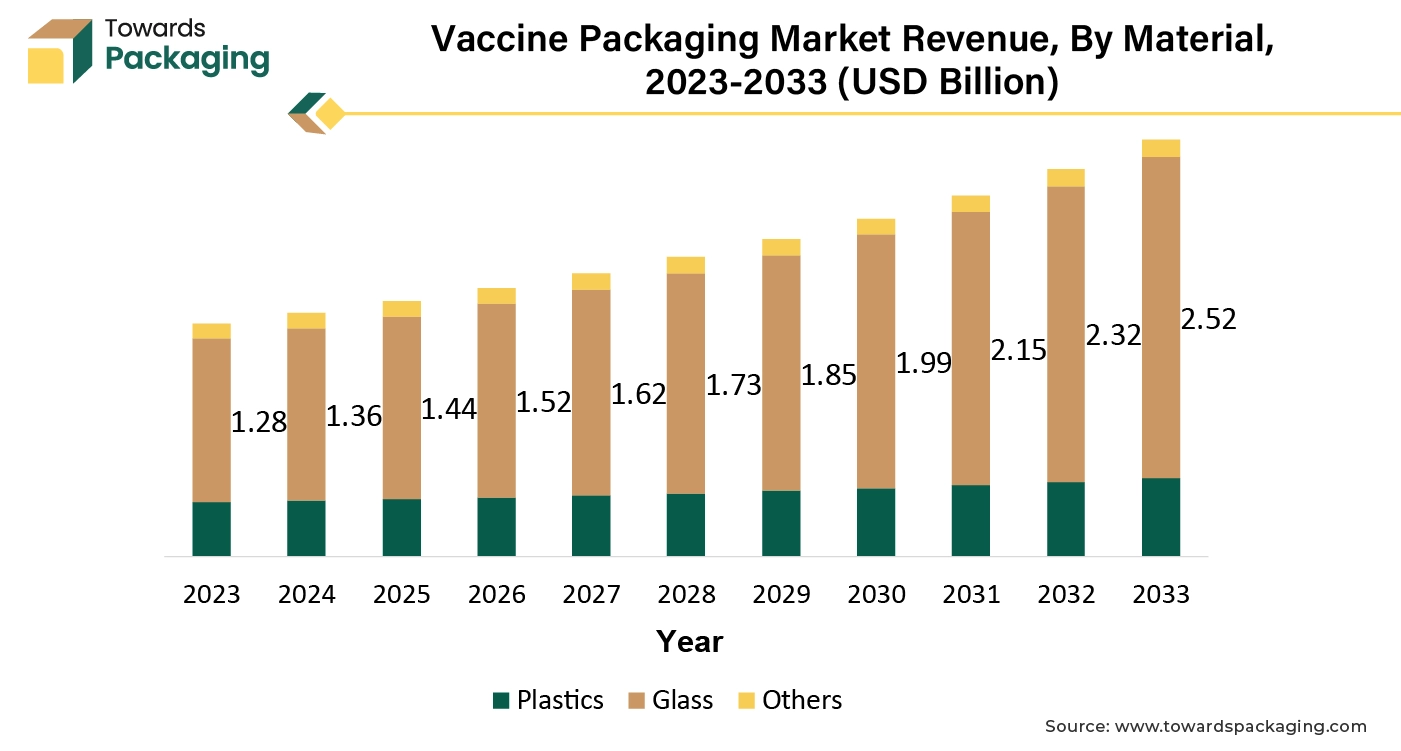

The glass segment captured largest market share in 2025. This is due to its unmatched properties that make it the preferred material for vaccine packaging. As it is inert, borosilicate glass is the most common material utilized for packaging vaccines. The ability of this unique glass to withstand chemicals as well as, in particular, heat from the outside is essential for preserving the vaccine. The vaccination within the glass bottles is therefore kept as durable and optimally protected as possible due to the glass only minimally expands in response to variations in the outside temperature.

Further, the packaging used for vaccines needs to be resilient to both the risks associated with international shipping and extremely high temperatures. As a result, glass is the material most frequently used to make vaccine vials since it is strong and can withstand high temperatures. Certain vaccine makers are likely to stick with the current packaging type, even though better packaging is still needed as COVID-19 vaccines require different storage conditions than regular glass vials.

The vials segment held the largest market share in 2025. Glass vials are preferred for their ability to preserve the stability as well as effectiveness of the vaccines over long periods. Globally, over fifty billion glass vials are made and sold for a variety of uses. SCHOTT, having 20 authorized glasses and factories worldwide, is one of the biggest producers of pharmaceutical packaging units. SCHOTT vials were utilized by three of the four vaccine studies that are undergoing the clinical testing for their vaccination campaigns. It generates approximately eleven billion glass vials annually in total.

Major participants in the pharmaceutical glass vial industry such as SCHOTT, Gerresheimer, Stevanto group, Corning and DWK Life Sciences have expanded their production capacity and quality in response to the continuous demand. Furthermore, vials also comply with the strict regulatory requirements for pharmaceutical packaging, providing the safety required for large-scale vaccination campaigns.

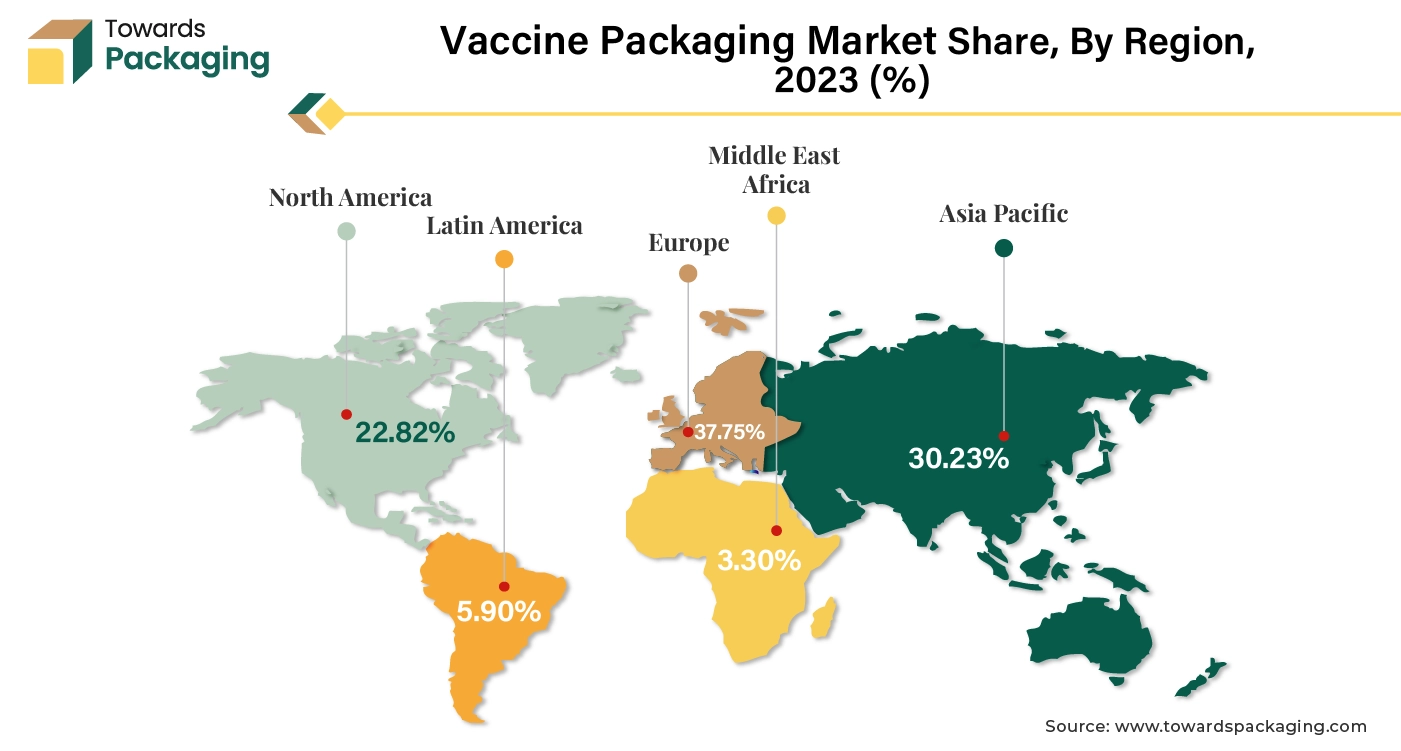

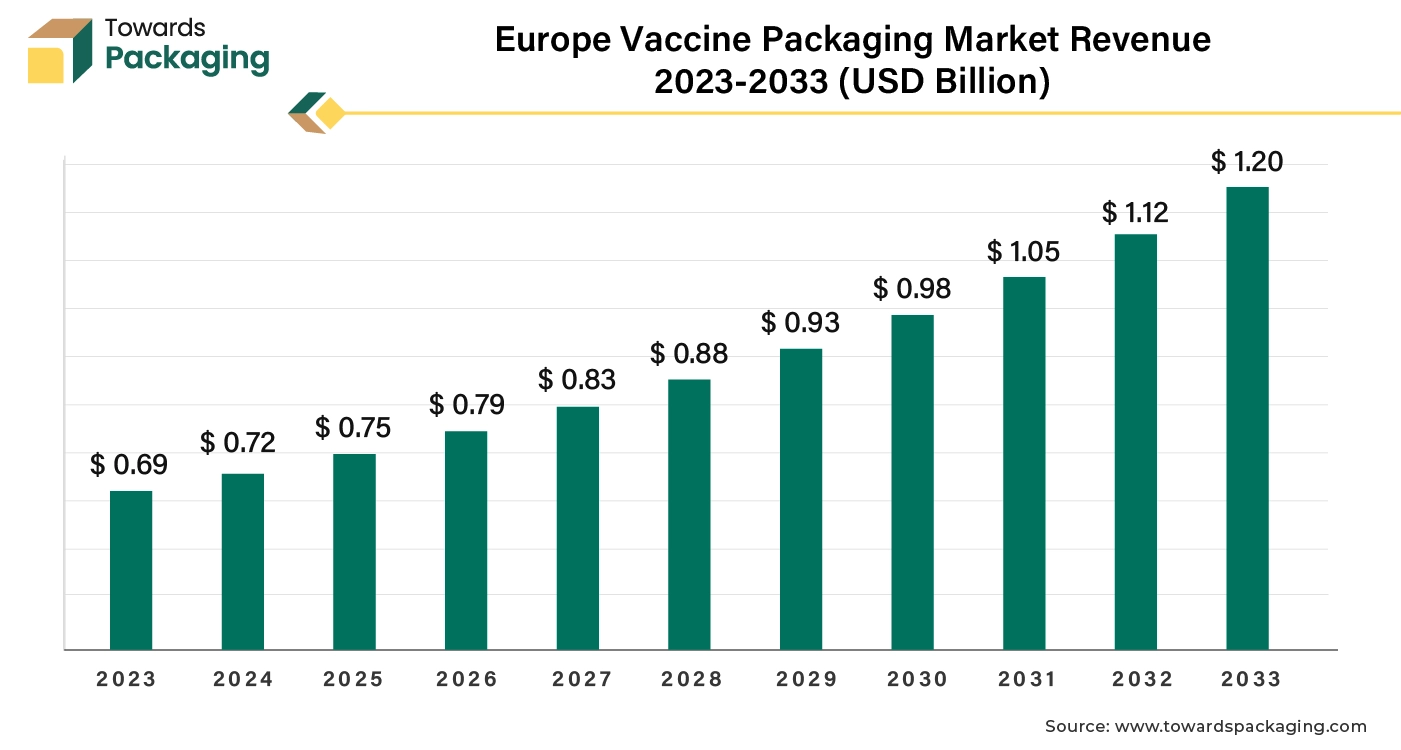

Europe held the largest market share of 37.75% in the world in 2025. This is due to the well-established and highly advanced healthcare system that supports large-scale vaccine production and distribution across the region. Furthermore, the presence of the most stringent regulatory requirements for vaccine packaging, governed by agencies like the European Medicines Agency (EMA) as well as the expansion of vaccine production capacities is also expected to contribute to the regional growth of the market.

Germany Vaccine Packaging Market Trends:

Germany is experiencing robust growth, and the growth is driven by the advancement in vaccine development, like single-dose vials and prefilled syringes reduce vaccine wastage and enhance safety, so there is a shift towards single-dose packaging. The expansion of cold chain facilities, particularly in the developing nations, is crucial for maintaining the efficacy of temperature-sensitive vaccines. These factors drive the growth of the market.

")

For instance,

Asia Pacific is likely to grow at fastest CAGR of 8.29% during the forecast period. This is owing to the increasing vaccine production in economies like China and India. As per the data by the Invest India, India has emerged as a dominant force in vaccines for diseases such as measles, Bacillus Calmette–Guérin (BCG), and Diphtheria, Tetanus and Pertussis (DPT).

Asia Pacific is poised to be the fastest expanding market for vaccine packaging in the forecast period. In India, for example, the pharmaceutical and healthcare industry expansion is on the rise. The government of India is taking constant efforts and making investments in improving the healthcare and pharmaceutical sector paving the way for new opportunities. The growing population directly increase the need for vaccines. India is leading innovation and development in drugs and medicine at a lower cost for various diseases. The country could become a growth opportunity for the vaccine packaging market in the Asia Pacific region during the forecast period.

India Vaccine Packaging Market Trends

India is seeing robust growth in the packaging market due to its rising vaccine production in the country, expanding immunization programs like the universal immunization programme are increasing vaccine uptakes, which require an increase in the supply of vaccine to different areas, and advancements in packaging technologies like innovation in packaging materials and cold chain logistics enhancing vaccine shelf life and distribution efficiency. These factors help the market to grow.

For instance,

Supported by reliable vaccination programs and robust pharmaceutical production capabilities. The region is steadily expanding due to the strong demand for glass vials, prefilled syringes, and packaging options that are compatible with cold chains. Advanced tamper-evident and traceable packaging formats are becoming more popular due to strict regulatory standards and quality requirements. Furthermore, ongoing investments in smart packaging, technological, and cold chain logistics are bolstering the region's market dominance.

The U.S. plays a critical role within the North American vaccine packaging market because of its extensive vaccine production, sophisticated healthcare systems, and robust regulatory oversight. High-quality primary and secondary packaging solutions are becoming more and more necessary as the demand for temperature-sensitive vaccines and booster programs rises. Manufacturers are being compelled by FDA regulations to improve safety, sterility, and compliance standards.

Driven by growing immunization programs and the enhancement of the infrastructure of healthcare. Growing consumer demand for cold chain-compatible packaging, glass vials, and ampoules is fueling market growth. The need for dependable and legal packaging solutions is growing as governments and healthcare institutions throughout the region bolster vaccine distribution networks.

Brazil is a key market for vaccine packaging in Latin America backed by extensive public immunization campaigns and the capacity to produce vaccines domestically. The demand for premium primary packaging like vials and prefilled syringes is rising in the nation's pharmaceutical industry. Tamper-evident and compliance-focused packaging solutions are being driven by ANVISA regulatory oversight. Furthermore, investments in healthcare infrastructure and cold chain logistics are boosting the market for vaccine packaging in Brazil.

Vaccine packaging relies on medical-grade glass, plastics, rubber stoppers, and aluminum seals to ensure sterility and product integrity. Growing vaccine production is increasing demand for high-quality, temperature-resistant, and contamination-free materials.

Key Players: Schott, Corning, Gerresheimer, West Pharmaceutical Services, AptarGroup

Cold-chain logistics are critical for vaccine packaging to maintain efficacy during storage and transport. Rising global immunization programs and temperature-sensitive vaccines are driving demand for insulated and traceable packaging solutions.

Key Players: DHL, UPS Healthcare, FedEx, Kuehne + Nagel, DB Schenker

Sustainable vaccine packaging is gaining focus to reduce medical waste and environmental impact. Manufacturers are adopting recyclable materials and safe disposal solutions for used vials and syringes.

Key Players: Veolia, Stericycle, Clean Harbors, Sharps Compliance, Daniels Health

By Material

By Type

By End-Use

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarVaccine Packaging Market