The adhesives for primary labelling market is growing rapidly, driven by rising demand across food & beverages, pharmaceuticals, logistics, and e-commerce industries. The market analysis covers global size projections from 2026-2035, key trends such as solvent-free and low-VOC formulations, and detailed segment data for adhesive chemistry, product form, end-use sectors, and distribution channels. Regional insights span North America, Europe, Asia Pacific, Latin America, and MEA, including APAC’s 35% share in 2025 and MEA’s projected 6% CAGR. The report includes competitive benchmarking of major players like Henkel, 3M, Sika, Avery Dennison, Covestro, and Dow, along with deep value chain mapping, trade flow analysis, pricing trends, and manufacturer-supplier ecosystem data.

Adhesives for primary labelling market refers to adhesives specially formulated and used directly on primary product containers or packs for attaching labels. These adhesives are designed to meet specific requirements such as substrate compatibility, application method, environmental resistance, regulatory compliance, and performance characteristics over shelf life.

The integration of AI technology in the adhesives for primary labelling market plays a significant role through automated quality control and predictive maintenance. It helps in controlling the quality of the adhesives with advanced formulation. AI support in the formulation of advance adhesives for stronger support to the labelling of the products. The incorporation of AI has reduced the generation of wastage and ensure the safety of the products.

Rising E-commerce and Logistics Industry Boost the Adhesives for Primary Labelling Market Demand

The rapid growth in the e-commerce and logistics industry has driven the demand for market. There is a huge demand for advancement in the adhesive technology for labelling of products in sectors such as pharmaceuticals and food & beverages. The requirement for customization and efficient branding has fuelled the development of this market. The rising trend for online ordering of products and growth of e-commerce industry has influenced the development of this market.

Rising Competition in the Market has Hindered the Adhesives for Primary Labelling Market Growth

The growing competition for introducing high-quality adhesives has raised the charges of the materials and hindered the development of the market. There is a huge demand for sustainable adhesives which require enhanced formulation of the adhesives for labelling of products. The requirement for strong performance in high temperature has influence the demand for high-quality formulation result in high charge of the adhesives restrict the development of the market.

Increasing Smart Labels and Technological Advancement Enhanced the Opportunities of the Adhesives for Primary Labelling Market

The increasing smart labels and technological advancement has raised the opportunities in the market. The major market players are developing environment-friendly adhesives such as biodegradable materials, recyclable resolutions, and water-based adhesives. The development of e-commerce and logistics industry needs durable adhesives and enhance the growth of the market. Innovation in the pressure sensitive adhesives comprising development in RFID and smart labels enhance the opportunities of the market.

")

Why Solvent-based Segment Dominated the Adhesives for Primary Labelling Market In 2025?

The solvent-based segment dominated the market in 2025 due to excellent bonding strength, chemical resistance, and durability of these adhesives. The chemical properties of these adhesives provide high-strength and quick-setting for the labelling used in the products. These are versatile and effective in several substrates such as metals. This segment is significantly accepted due to strict regulatory guidelines. These adhesives generate high strength bonds to last long.

The water-based adhesive emulsions segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is adopted by various sectors due to its eco-friendliness. It supports sustainability aim of the market players and decrease VOCs. These types of adhesives use water as base carrier for polymers such as acetate, EVA, acrylics, or vinyl. These are majorly accepted by segments such as gift wrapping, general-purpose repairs, and carton sealing.

")

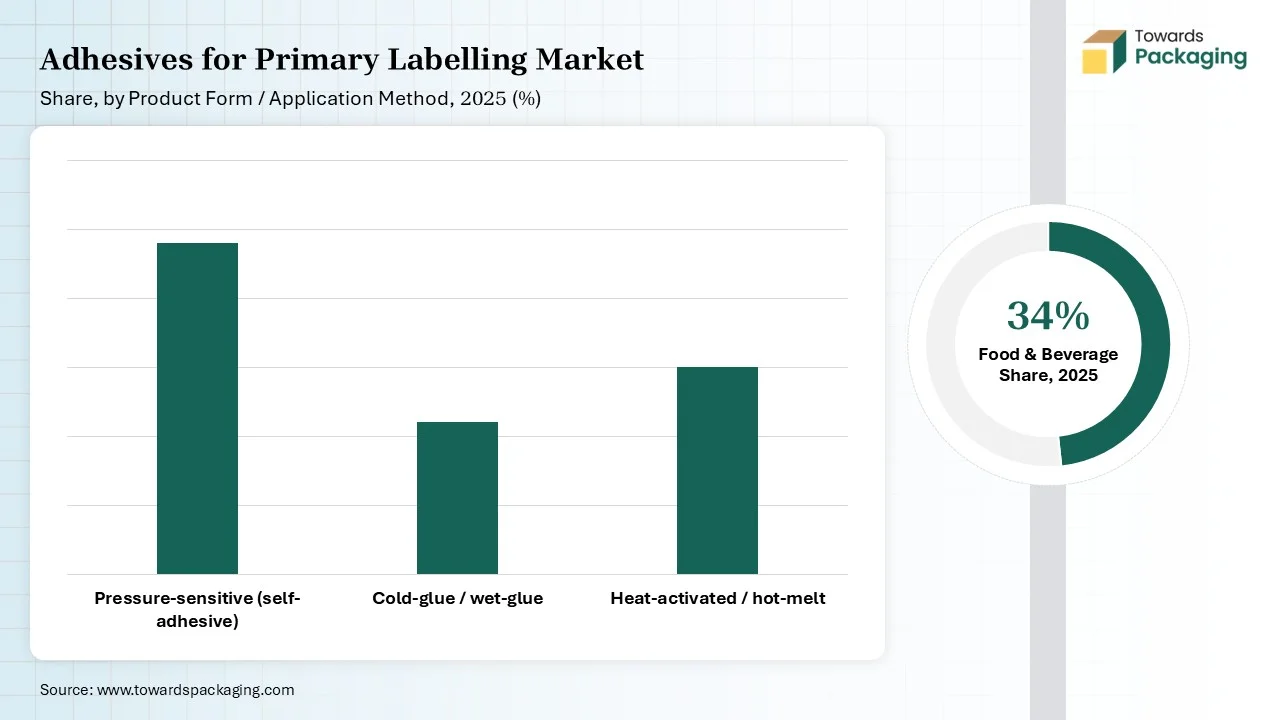

Why Pressure-sensitive Segment Dominated the Adhesives for Primary Labelling Market In 2025?

The pressure-sensitive segment held the largest share of the market in 2025 due to its versatile and convenient bonding solution. The huge ability to customize with wide finishes, high-definition graphics, and special facilities such as RFID technology. The diverse surface finishes, high-quality printing, and vivid graphics enhance the adoption of this segment in various sectors. The increasing need for detailed information of the products raised the demand for this segment adhesives for primary labelling.

The heat-activated segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is growing rapidly as this type of adhesives provide strong bonds for numerous substrates automated productions, durable labels, and enabling fast. Its formulation provides high efficiency and supply chain management. The continuous innovation in this sector provides improved bond strength and thermal stability.

Why Food & Beverage Segment Dominated the Adhesives for Primary Labelling Market In 2025?

The food & beverage held the largest share of the market in 2025 due to rising consumption of ready-to-eat food products. The rapid urbanization and changing lifestyle have encouraged the usage of packaged food which require strong adhesives for labelling important information about packaged food products. Increasing versatility and convenient in applying encouraged the adoption of such adhesives in this sector. These adhesives ensure the secure attachment of the labels and maintain its readability.

The pharmaceuticals & healthcare segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is growing rapidly due to strict guidelines of the regulatory bodies for the secure labelling of the information related to the product. Adhesives utilised in this segment must fulfil the robust regulatory needs by providing resistance to several ecological factors like chemicals, moisture, and temperature. These adhesives confirm that the primary labels stay securely and comprehensible during the lifecycle of the product, from production to consumption. The growing demand for pharmaceuticals and healthcare products worldwide is influencing the requirement for advanced adhesive resolutions that can fulfil these severe requirements.

Why Through Converters Segment Dominated the Adhesives for Primary Labelling Market In 2025?

The through converters held the largest share of the market in 2025 due to handling a wide variety of resources and processing technology. These provide expertise in selecting materials for adhesives formulation and controlling quality of the formation. It confirms the production of aesthetically attractive, high-quality, and functional labels to fulfil the requirement of several brands.

The direct-to-brand segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is growing as it comprises from production of adhesives to its distribution process. It helps in building reliability of brands over adhesive manufacturing companies by fulfilling the evolving demand of it. By eliminating middle man from distribution process, it helps to make these adhesives cost-effective.

")

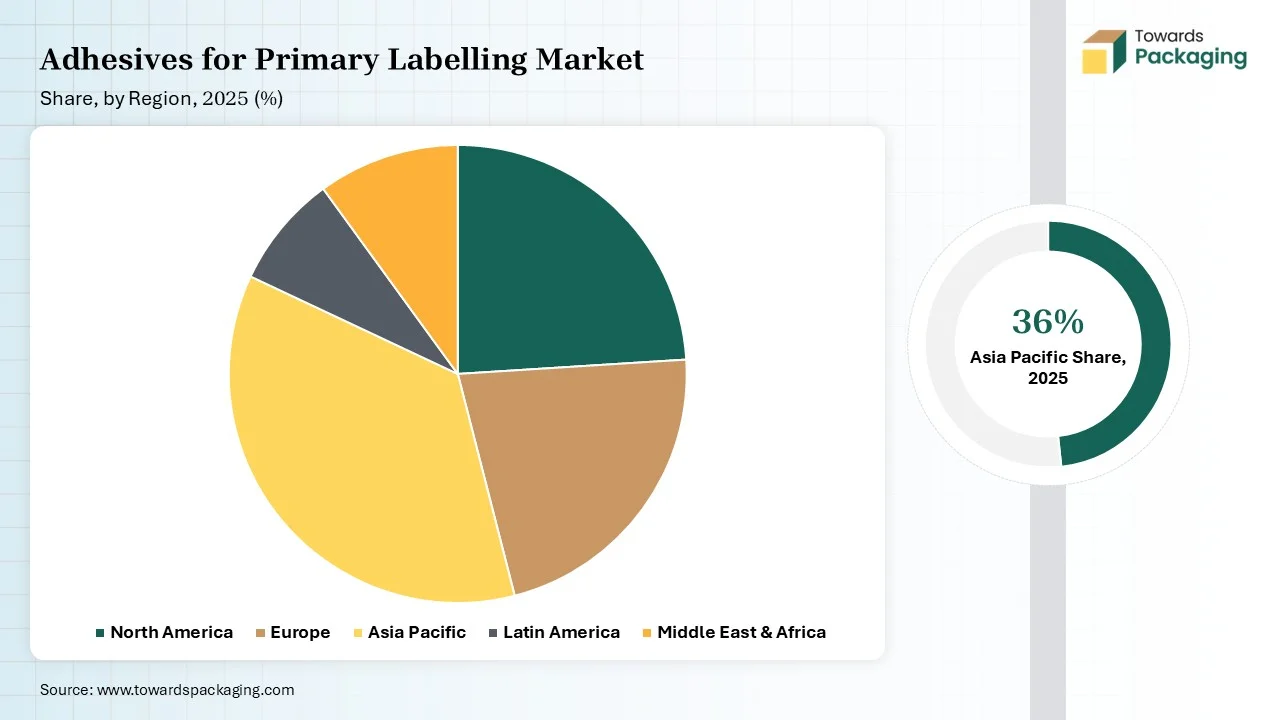

Asia Pacific held the largest share of the adhesives for primary labelling market in 2025, due to rapid industrialization and the rising expansion of e-commerce industries and growing trend of online ordering. In countries like China and India this market is growing rapidly due to increasing disposable earning among people and changing lifestyle. This changing lifestyle has influenced the demand for packaged food which require labelling with detailed information. The increasing emphasis for ecologically friendly adhesives has influence the innovation in this market.

The huge presence of companies to introduce innovation in the adhesives formulation for primary labelling has boosted the growth of the market in China. Rising consumer market encourage the development of new formulation for providing strong bonding between materials has influenced the growth of this market in this region. The continuous growth in sectors such as technological prowess, industrial base, and burgeoning customer market has raised the influence of this market.

Middle East & Africa expects the significant growth in the adhesives for primary labelling market during the forecast period. This market is growing significantly in this region due to rising economic condition, shifting customer demand, and industrialization. Rising ecological concern has influenced the demand for formulation of adhesives that can be decomposed such as bio-based and water-based adhesives. The rapid growth in automotive, construction, and several other industries has enhanced the demand for adhesives for primary labelling purpose.

This market depends upon a wide variety of raw materials which confirm cost-efficiency and stability of the adhesives.

These components play significant role in maintaining the quality of the adhesives and enhance reliability.

It is important for consumers to get right quality adhesives according to their requirements in large scale.

By Adhesive Chemistry

By Product Form / Application Method

By End-Use Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarAdhesives for Primary Labelling Market