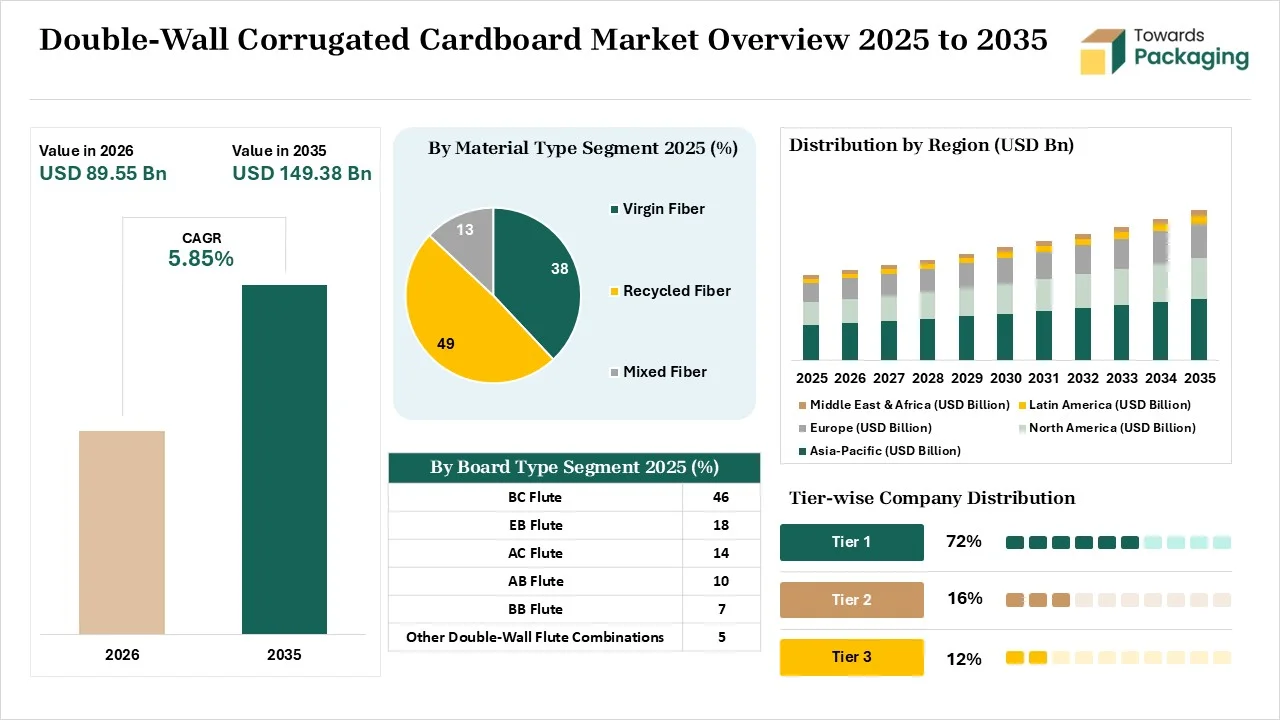

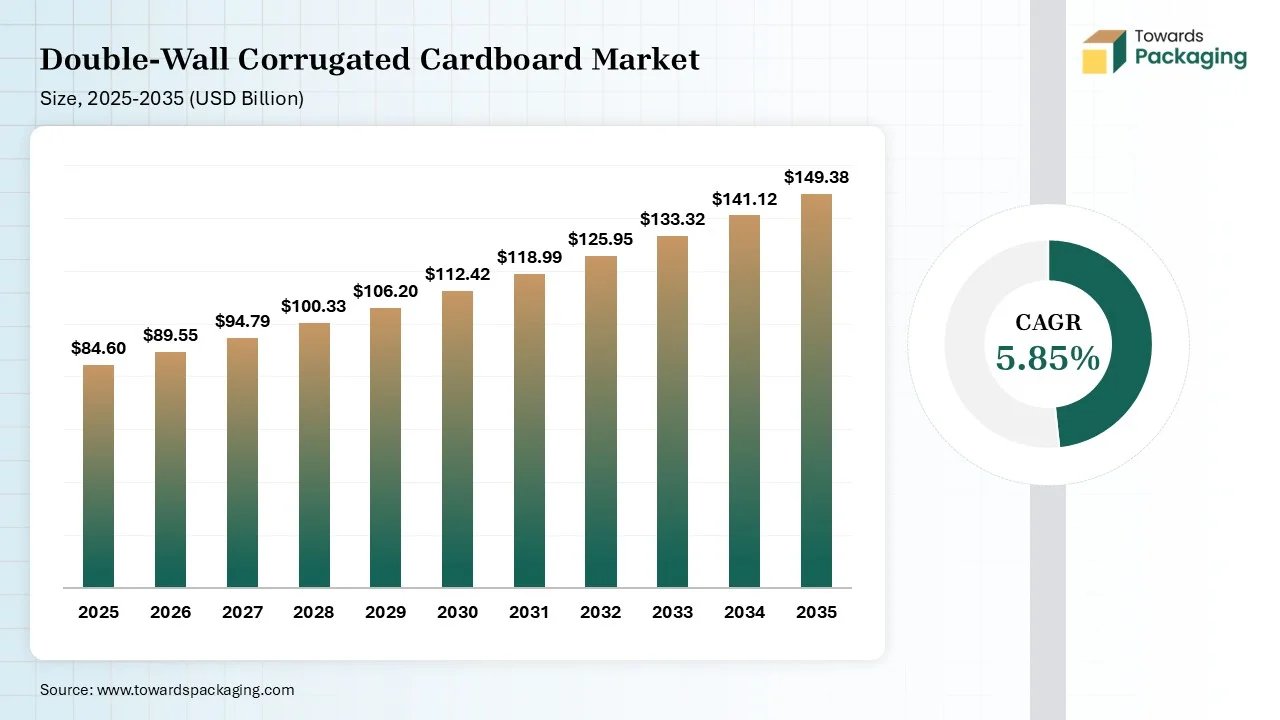

The Double-Wall Corrugated Cardboard Market is projected to grow from USD 89.55 billion in 2026 to USD 149.38 billion by 2035, registering a CAGR of 5.85% during the forecast period. The report provides comprehensive market size forecasts, segment-wise analysis by board type, flute combination, application, end-use industry, and distribution channel, along with regional and country-level insights across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. It also covers competitive benchmarking, company profiles, market share analysis, value chain assessment, import-export (trade) analysis, pricing trends, key manufacturers, suppliers, production capacity, demand-supply dynamics, and the latest industry developments influencing market growth.

Double-wall corrugated cardboard is a packaging material made up of two fluted inner mediums, two flat outer linerboards, and one flat inner linerboard. The packaging is made up of 5 layers and developed using diverse combinations of the flute. The commonly used flutes are the EB-flute and BC-flute. They include characteristics like high burst strength, excellent puncture resistance, stacking stability, heavy weight capacity, superior shock absorption, customizable thickness, and full recyclability. They offer benefits like enhanced impact protection, reusability, eco-friendliness, and optimal strength-to-weight ratio. Double-wall corrugated cardboard is widely used in heavy-duty shipping, pallet boxes, flat-pack furniture, fragile electronics packaging, and appliance packaging.

Factors like the quick commerce explosion, heavy electronics protection, rise in RTE meal transportation, innovations in printing, advancements in micro-fluting, expansion of global trade networks, growth in heavy-duty industries, higher sustainable solution demand, interest in moisture-resistant corrugated boxes, growing distribution of delicate medical devices, and the popularity of automated warehousing drive the growth of the double-wall corrugated cardboard market.

The explosion of online retail increases the use of double-wall corrugated cardboard due to the demand for preventing transit damage. Factors like affordable mobile data, personalization demand, rural internet penetration, 10-30 minutes delivery times, and accessible financing increase the penetration of online retail. The costly returns of online retail parcels and the focus on reducing the collapse of packaging boxes in the vehicle increase the use of double-wall corrugated cardboard.

The rise in ordering large appliances online and the shift away from plastic bubble wraps increase the use of double-wall corrugated cardboard. The shipping of massive items and humidity changes during online retail increase the use of double-wall corrugated cardboard. The preservation of online brand perception helps with the expansion. The expansion of online retail is a key driver for the growth of the market.

Factors like thriving worldwide e-commerce demand, port congestion, and high energy costs are responsible for the fluctuations of raw material prices. The volatility in the prices of recycling and virgin kraft pulp increases the cost of double-wall corrugated cardboard production. The high paper production demand and energy-intensive manufacturing process increase the cost. The freight bottlenecks and regional fiber shortages increase the cost.

The rise in high-strength paper imports and the high pressures on paper suppliers are responsible for price volatility. The heavy electricity use in sourcing materials and the various transportation bottlenecks increase the cost. The magnified consumption of feedstock and the growing worldwide freight charges increase the cost. The fluctuations in the feedstock prices are a major restriction on the growth of the market.

The growing technological integration in packaging helps in the fight against counterfeiting. The incorporation of complex codes, RFID sensors, and other technologies in the double-wall corrugated cardboard supports flawless application. The need for superior cargo protection and the focus on securing smart goods increase the use of smart double-wall corrugated cardboard packaging.

The monitoring location during transit and focus on product hardware safety increases the use of smart packaging. The prevention of tampering during long-haul shipping and the need to lower loss rates increase the integration of smart packaging. The creation of a memorable unboxing experience helps with the expansion. The smart packaging adoption creates an opportunity for the growth of the market.

The double-wall corrugated cardboard market is experiencing technological developments driven by demand for lightweighting, automated production, and simulation. Technological developments like CNC automation, track-and-trace integration, machine learning, nanotechnology integration, and IoT integration support real-time tracking, lowering shipping costs, and customizing box sizes. AI is the major technological transformation in the market, driven by production efficiency and minimized environmental impact.

AI tests countless flute profiles and anticipates equipment failures. AI easily spots board defects and offers greater accuracy in production. AI optimizes the shipping logistics and customizes the box dimensions. AI detects the printing misalignment and monitors the corrugator health. AI performs workflow automation and optimizes the run sequences. Overall, AI helps in structural design and predictive maintenance.

For instance, International Paper Company uses AI for optimizing board configurations and predictive maintenance of machinery.

Raw materials like kraft paper, starch-based adhesives, and corrugated medium are required for the manufacturing of double-wall corrugated cardboard.

Material processing involves steps like conditioning, fluting, gluing, and bonding. Conversion includes printing, slitting, die-cutting, and folding.

Logistics focuses on Edge Crush Test, Mullen Burst Test, and flute combinations. Distribution includes channels like distributors, converters, direct sales, and e-commerce platforms.

The BC flute segment dominated the market with 46% share in 2025. The prevention of mechanical damage in long-haul freight and the expansion of commercial moving increase the use of BC flute. The need to secure semi-fragile products and the rise in heavy-duty storage increase the adoption of BC flute. The growing export packaging and the increased stacking of boxes in warehouses increase the demand for BC flute. The excellent stacking strength, optimal thickness, excellent durability, and high crush resistance of BC flute drives the segment growth.

The other double-wall flute combinations segment held the 5% market share in 2025 and is expected to grow at the fastest CAGR of 7.20% during the forecast period. The high retail-ready demand and the need for a high-quality surface for printing purposes increase the use of other double-wall flute combinations. The development of a custom-tune box and weight-bearing standards increases the use of other double-wall flute combinations. The development of an ultra-smoother outer surface increases the use of the FE or EB flute combination. The compatibility of other double-wall flute combinations with automated packaging supports the segment growth.

The recycled fiber segment dominated the market with 49% share in 2025 and is expected to grow at the fastest CAGR of 6.90% during the forecast period. The brand's focus on satisfying sustainability-conscious consumer demand and the plastic-free mandates increases the use of recycled fiber. The high cost of virgin kraft pulp and the packaging manufacturers' focus on stable pricing increases the use of recycled fiber. The development of affordable double-wall boxes and the higher utilization of recycled-fiber corrugate increases the use of recycled fiber. The excellent material properties of recycled fiber drive the segment growth.

The virgin fiber segment held the 38% market share in 2025. The demand for better bursting strength and the prevention of fiber degradation in packaging increases the use of virgin fiber. The need to lower the box failure and the expansion of automated warehouses increase the use of virgin fiber. The demand for contaminant-free raw material and the expansion of multiple transit touchpoints increase the use of virgin fiber. The excellent tensile strength and heavy load-bearing capacity of virgin fiber support the segment growth.

The standard double-wall corrugated board segment dominated the market with 57% share in 2025. The thriving bulk transportation of food products and the complex logistic chains increase the adoption of standard double-wall corrugated board. The growing shipping of automotive components and the stricter sustainability directives increase the use of standard double-wall corrugated board. The burgeoning cross-border transition helps with the expansion. The optimal protection, cost-efficiency, and material efficiency of standard double-wall corrugated board drive the segment growth.

The moisture-resistant double-wall corrugated board segment held the 13% market share in 2025 and is expected to grow at the fastest CAGR of 7.80% during the forecast period. The higher interest in sturdy-durable packaging and the focus on protecting items from warehouse humidity increase the use of moisture-resistant double-wall corrugated board. The rising cold-storage shipping of dairy items and the shift away from wooden packs increase the adoption of moisture-resistant double-wall corrugated board. The explosion of modern automated warehouses and the rise in maritime transport have increased the use of moisture-resistant double-wall corrugated board, supporting the segment's growth.

The regular slotted containers (RSC) segment dominated the market with 42% share in 2025. The manufacturers focus on zero manufacturing waste, and the growth in automated sealing machinery increases the use of RSC. The growing demand for space-saving storage and the need for maximum crushing resistance increase the use of RSC. The increased packaging of industrial components increases the use of RSC. The double-wall durability, automation friendliness, exceptional stacking stress, and universal versatility of RSC drive the segment growth.

The bulk bins & pallet boxes segment held the 9% market share in 2025 and is expected to grow at the fastest CAGR of 7.60% during the forecast period. The focus on lowering the excessive volumetric weight of heavy industrial parts and the increased replacement of plastic bulk containers increases the adoption of bulk bins & pallet boxes. The corporate green initiatives and the expanding palletizing robots increase the production of bulk bins & pallet boxes. The bulk chemicals transportation and the reduction of warehouse footprint increase the use of bulk bins & pallet boxes, supporting the overall growth of the segment.

The food & beverages segment dominated the market with 27% share in 2025. The need for cushioning in bottled beverages and the focus on resisting condensation of dairy items increase the use of double-wall corrugated cardboard. The explosion of D2C meal kits and the high weights of canned goods increase the use of double-wall corrugated cardboard. The shipping of chilled food products and the breakage issues in F&B items increase the use of double-wall corrugated cardboard. The large fresh produce shipments drive the overall segment growth.

The e-commerce & logistics segment held the 23% market share in 2025 and is expected to grow at the fastest CAGR of 7.80% during the forecast period. The high handling rates of e-commerce parcels in diverse sorting hubs increase the adoption of double-wall corrugated cardboard. The need to lower replacement costs of e-commerce parcels and the surge in rapid deliveries increase the use of double-wall corrugated cardboard. The strong presence of micro-fulfillment hubs and unpredictable transitions in e-commerce increase the use of double-wall corrugated cardboard. The increased purchasing of electronic items through online portals supports the segment growth.

The flexographic printing segment dominated the market with 61% share in 2025. The high-volume double-wall corrugated cardboard operation and the focus on handling irregular surfaces increase the use of flexographic printing. The availability of water-based inks and the shifting away from high upfront setup increases the adoption of flexographic printing. Advancements like HD Flexo help with the expansion. The massive throughput, substrate flexibility, excellent processing speed, and inline processing capabilities of flexographic printing drive the segment growth.

The digital printing segment held the 16% market share in 2025 and is expected to grow at the fastest CAGR of 9.40% during the forecast period. The demand for small-batch production and the popularity of D2C branding increase the adoption of digital printing. The rise in variable data printing and the demand for inventory waste reduction increases the use of digital printing. The rise in mass customization of packaging and the incorporation of smart packaging increases the use of digital printing. The no setup cost, shorter drying times, photographic-quality graphics, and high customization in digital printing support the segment growth.

The direct sales segment dominated the market with 58% share in 2025. The demand for direct collaboration with clients and the massive volume of purchasing increase the adoption of direct sales. The demand for pricing negotiation and an uninterrupted supply chain increases the adoption of direct sales. The customized specifications for industrial needs and the robust quality control demand increase the adoption of direct sales. The availability of complex customization drives the segment growth.

The online sales segment held the 11% market share in 2025 and is expected to grow at the fastest CAGR of 8.50% during the forecast period. The availability of easy comparison of diverse parameters and the expansion of smaller retailers increase the use of online platforms. The high flexible sizing demand and the rise in independent brands prefer buying from online platforms. The demand for custom-printed boxes and the creation of short-run custom graphics increases the adoption of online platforms. The streamlined logistics in online platforms support the segment growth.

Asia Pacific dominated the double-wall corrugated cardboard market with a 41% share in 2025 and is expected to grow at the fastest CAGR of 7.10% during the forecast period. The high production of appliances and the rise in international shipping increase the adoption of double-wall corrugated cardboard. The exploding logistics industry and the massive export volume increase the use of double-wall corrugated cardboard. The thriving food processing in urbanized areas and the high dependence on fresh foods increase the use of double-wall corrugated cardboard. The expanding standards of parcel-drop durability drive the overall market growth.

North America held the 27% market share in 2025. The burgeoning D2C networks and the high regional production of industrial goods increase the demand for double-wall corrugated cardboard. The well-matured recycling infrastructure and the expansion of nearshoring increase the use of double-wall corrugated cardboard. The complex supply chains and the rise in relocation of electronics assembly increase the use of double-wall corrugated cardboard, supporting the overall market growth.

Europe held the 23% market share in 2025. The mandates for the replacement of plastic and the exploding online retail industry increase the use of double-wall corrugated cardboard. The fastest expansion of industrial sectors and the high interest in double-wall containers help with the expansion. The growing intra-regional trade of agricultural goods and the focus on carbon footprint optimization increase the use of double-wall corrugated cardboard, boosting the market growth.

Latin America held the 5% market share in 2025. The focus on the safe international transportation of food products and the rise in multi-item orders on e-commerce platforms increase the adoption of double-wall corrugated cardboard. The awareness about the benefits of paper-based packaging solutions and easy access to feedstocks increases the production of double-wall corrugated cardboard. The high fresh produce export and the rise in auto-parts manufacturing support the market growth.

The Middle East & Africa held the 4% market share in 2025. The expansion of digital commerce activities and the increased transportation of renewable energy equipment increases the use of double-wall corrugated cardboard. The high shipping rate of beverages and the rise in recycled fiber packaging increase the use of double-wall corrugated cardboard. The heavy-duty export and the rise in cross-border trade help with expansion. The plastic alternatives demand boosts the market growth.

| Rank | Company | Headquarters | Country | Major Contribution to Double-Wall Corrugated Cardboard Market | Key Packaging Products and Services |

| 1 | International Paper Company | Memphis, Tennessee, United States | United States | The company manufactures durable linerboard and a standardized fluting combination. In the United States, they operate a total of nine plants of the corrugated packaging sheet feeder. | Heavy-Duty Slotted Boxes, Bulk Bins, Corrugated Sheets, Telescopic & Bushel Boxes, Die-Cut Packaging |

| 2 | DS Smith Plc | London, United Kingdom | United Kingdom | The company invested €14 million to expand the production capabilities of the heavy-duty corrugated board. They manufacture pallet-based solutions. | Export Boxes, Industrial Machine & Parts Packaging, Heavy-Duty Box Pallets, Consumer Goods Transport Packaging |

| 3 | Packaging Corporation of America | Lake Forest, Illinois, United States | United States | The company focuses on heavy-duty structural engineering and operates corrugated box plants over 90. The company manufactures packaging products by utilizing sustainable forestry practices. | BulkMaster Bulk Bins, PowerPly, Grid-Lok Containers, Custom-Engineered Heavy-Duty Containers |

| 4 | Smurfit WestRock | Dublin, Ireland | Ireland | The company got a €20 million investment in Vernon for the upgradation of an advanced corrugated facility. The company received a $150 million investment for scaling production & upgrading the facility of high-performance corrugated packaging in Brazil. | Corrugated Trays, Gaylord Boxes, Double Wall Boxes, Octabins, Heavy-Duty Boxes |

| 5 | Mondi Group | Weybridge, United Kingdom, and Vienna, Austria | United Kingdom and Austria | The company offers sustainable raw materials and an advanced printing solution. The company received a €200 million investment for the upgradation of the Duino recycled containerboard mill. | Heavy-Duty Industrial Containers, Food & Agriculture Boxes, eCommerce Packaging, Retail-Ready Packaging |

By Board Type

By Material Type

By Wall Construction

By Box Type

By End-Use Industry

By Printing Technology

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarDouble-Wall Corrugated Cardboard Market