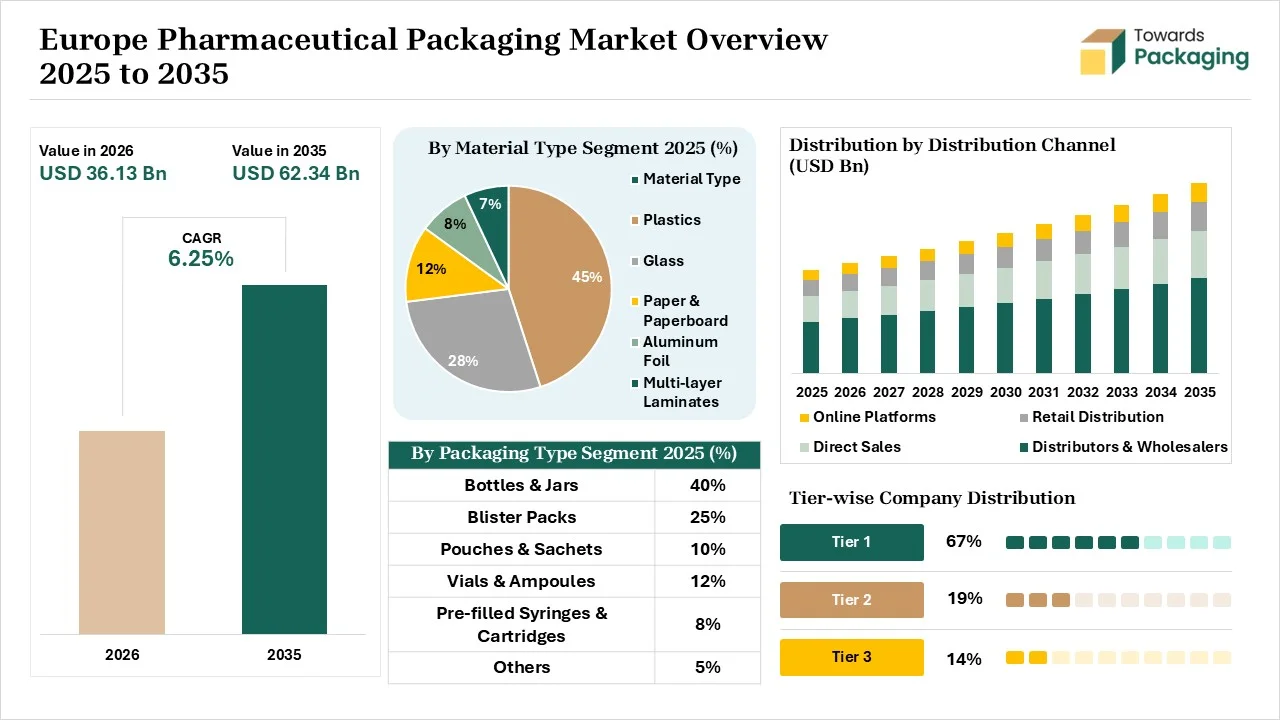

The Europe pharmaceutical packaging market is forecasted to expand from USD 36.13 billion in 2026 to USD 62.34 billion by 2035, growing at a CAGR of 6.25% from 2026 to 2035. This growth is driven by increasing demand for safe, sustainable, and innovative packaging solutions ensuring drug protection and regulatory compliance. The market includes segments such as material types (plastics, multi-layer laminates), packaging types (bottles & jars, pre-filled syringes), and dosage forms (oral solids, injectables). Key countries like Germany and the UK play pivotal roles in this market's development.

The Europe pharmaceutical packaging market is witnessing steady growth, driven by tighter regulations for drug safety, growing healthcare demands, and increased pharmaceutical production. Demand is being further fueled by the growing use of eco-friendly and sustainable packaging materials. Smart and tamper-evident packaging innovations are also improving patient convenience and product security, which is helping the market expand throughout the region. Tamper-evident packaging innovations are also enhancing patient convenience and product security.

AI is rapidly reshaping the European pharmaceutical packaging industry by improving production efficiency, regulatory compliance, patient safety, and supply-chain transparency. Smart algorithms analyze production data to reduce waste, improve recyclable packaging development, and enhance sustainability efforts, aligning with Europe’s strong environmental regulations and circular economy goals. AI-enabled predictive analysis helps maintain temperature stability and product integrity during transportation. AI-driven tracking systems, smart labels, and digital authentication tools enable pharmaceutical companies to combat counterfeit medicines and improve supply-chain visibility across Europe. AI enables monitoring manufacturing lines in real time, detecting defects instantly, and reducing packaging errors in sensitive drug products.

| Technological Shift | Description/Impact |

| Smart Packaging | Integration of RFID, OR codes, and IoT for real-time monitoring of drug authenticity, temperature, and supply chain visibility. |

| Prefilled & auto-injectable devices | Adoption of prefilled syringes, cartages, and auto injectors for biologics, vaccines, and self-administered therapies, improving dosing accuracy and patient convenience. |

| Sustainable & eco-friendly materials | Shift toward recyclable, biodegradable, and multi-layer laminate materials to reduce environmental impact and comply with EU sustainability regulations. |

| Tamper-evident & child-resistant designs | Advanced closures, seals, and blister technologies to enhance drug safety and prevent misuse. |

Pharmaceutical companies are facing pressure to reduce plastic waste and implement recyclable solutions because of Europe's strong push toward a circular economy. Reusable containers, paper-based packaging, and biodegradable plastics are becoming more popular. Growing consumer awareness of sustainability has also contributed to this change in green packaging.

Despite sustainability initiatives, plastics continue to be used in a sizable portion of pharmaceutical packaging. Obstacles include the challenge of recycling multi-layer materials and limitations on medical waste. Supply chains may be disrupted, and costly switchovers to alternatives may be necessary as pressure to phase out non-recyclable plastics grows.

")

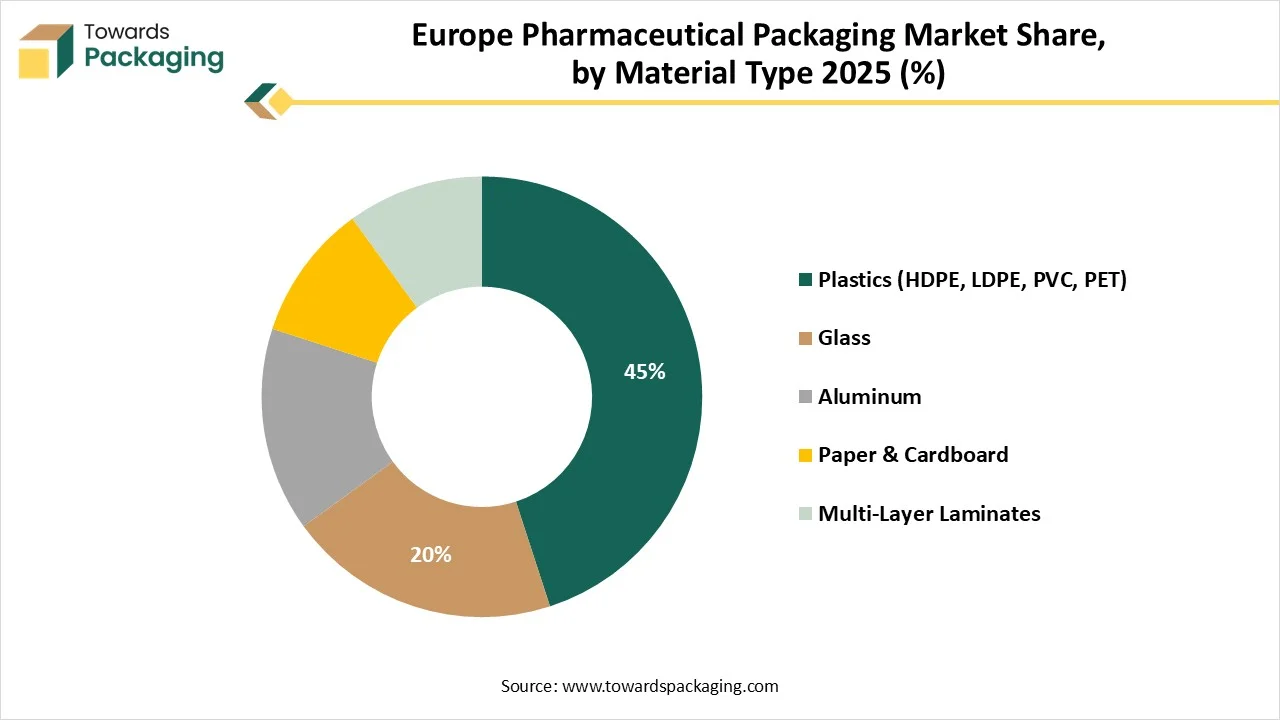

The plastics segment dominated the Europe pharmaceutical packaging market with a 45% share in 2025 because of its lightweight quality's affordability, and adaptability. It is frequently used for bottles, blister packs, vials, and caps because it is easy to make and durable. Plastics dominance in oral injectable and topical dosage forms is guaranteed by its ability to be tailored for barrier qualities, clarity, and drug compatibility.

The multi-layer laminates are expected to be the fastest in the market during the forecast period due to their superior barrier protection against light oxygen and moisture. They are being used more often in sachets, blisters, and pouches for medications that are sensitive, such as vaccines and biologics. Laminate materials quick rise in the European market, being driven by the growing need for longer shelf lives and improved drug safety, as well as sustainability advancements in laminate materials.

")

The chart shows that flexible packaging plastics use in Europe increased steadily between 2010 and 2020.

Key trends:

")

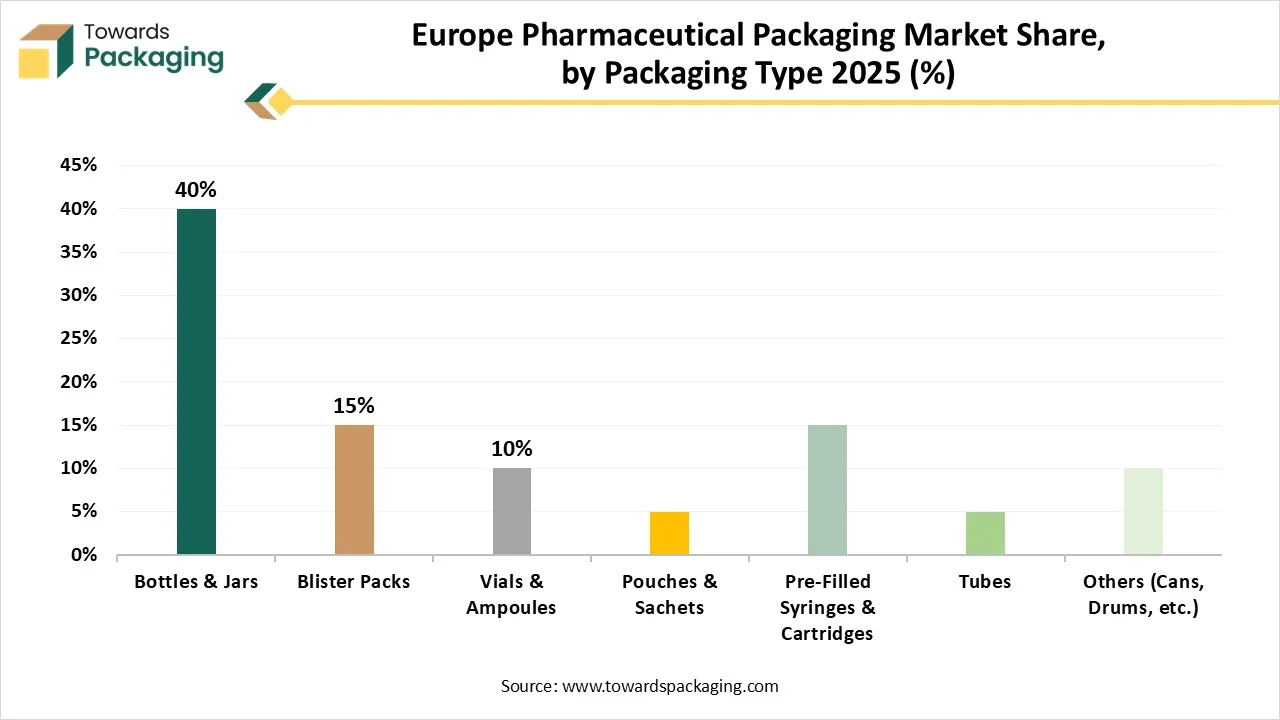

The bottles & jars segment dominated the Europe pharmaceutical packaging market with approximately 40% share in 2025, because they are frequently found in oral solids, liquids, and supplements. They are economical in large-scale manufacturing, providing strong protection and are simple to handle. Glass and plastic bottle maintain their top spot because they are still necessary for both patient convenience and regulatory compliance.

The pre-filled syringes & cartridges segment is predicted to be the fastest in the market during the forecast period. Due to the growing need for vaccines, self-administration treatments, and injectable biologics. They increased patient adherence, lowered the risk of contamination, and improved dosing accuracy. Adoption of these practical, user-friendly formats has been further accelerated by the trend toward personalized medicine and home healthcare.

The oral solid segment has dominated the market with approximately 50% share in 2025, since it accounts for the greatest portion of drug use in Europe. Blister packs, bottles, and cartons are frequently used in their packaging to ensure child safety, tamper evidence, and durability. Oral solid packaging is always in demand due to the high prevalence of chronic illnesses and preventive treatments.

The injectable segment is predicted to be the fastest growing in the market during the forecast period because of the rise in vaccines, biologics, and specialty drug treatments. To ensure sterility, stability, and precise dosing, advanced packaging options such as prefilled syringes, vials, and cartridges are crucial. The expansion of this market is also being driven by the rise in hospital-focused therapies and self-administered injectables.

")

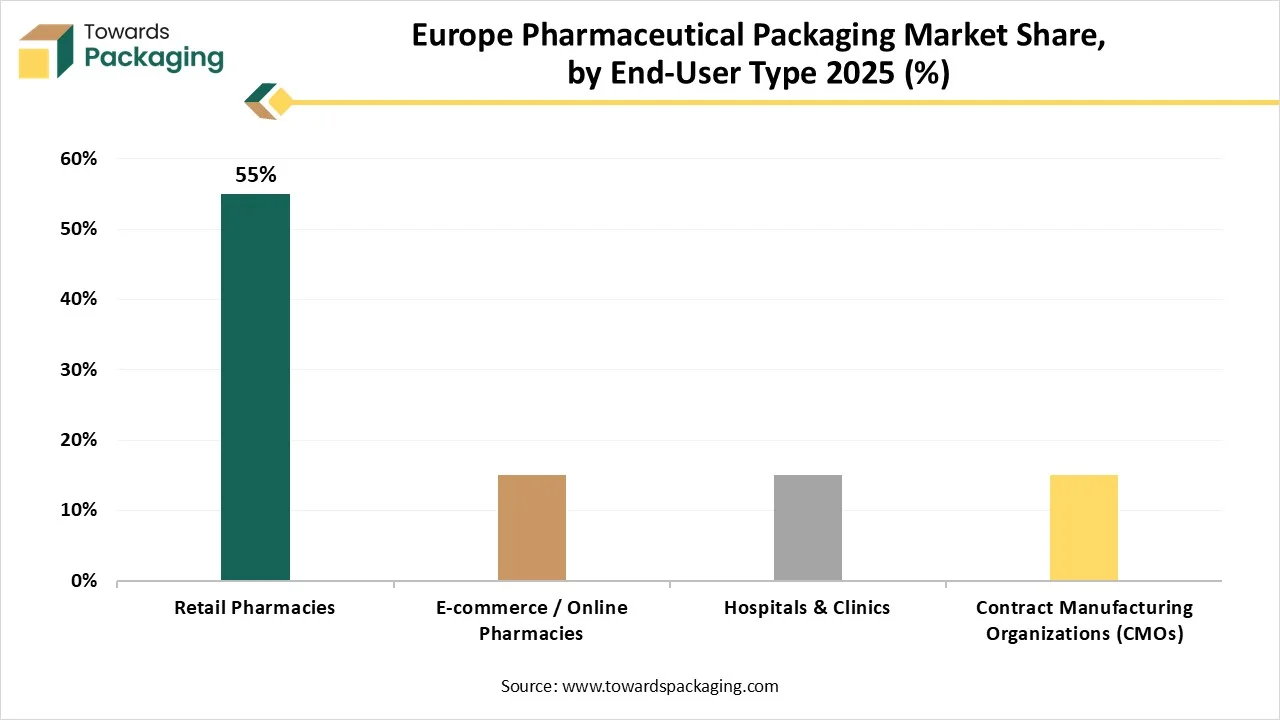

The retail pharmacies segment has dominated the market with approximately 55% in 2025 because they are where prescription and over-the-counter medications are primarily distributed. Pharmaceutical companies are a major force behind standardized formats like bottles, blisters, and cartons because packaging solutions must guarantee patient safety compliance and ease of dispensing. The demand for pharmaceutical packaging is consistently maintained by their well-established networks.

The e-commerce/online pharmacies segment is predicted to be the fastest in the market during the forecast period because of the growing popularity of pharmaceutical home delivery and online purchases. Additional protection, tamper evidence, and temperature control during transit are necessary for packaging solutions in this channel. The growth of this channel. The growth of this market is driven by consumers increasing desire for quick delivery and convenience.

The distributors & wholesalers segment dominated the market in 2025, by managing large shipments to pharmacies, hospitals, and other healthcare facilities. Their well-established networks guarantee prompt delivery of packaged medication, effective inventory control, and storage. Because of their standardized packaging and adherence to legal requirements, they are essential to the supply chain.

The online platforms are growing fastest, driven by a direct-to-consumer business model and the growing adoption of digital healthcare. The focus of this channels packaging is on secure transportation, tamper evidence, and safety. The demand for online drug delivery is being further accelerated by the expansion of telemedicine and home healthcare services.

Germany’s market is driven by its sophisticated healthcare infrastructure, robust pharmaceutical manufacturing base, and stringent regulatory requirements. High-quality, legally compliant packaging solutions that guarantee product safety and traceability are prioritized in the nation. Growing consumer demand for sustainable materials, child-resistant packaging, and blister packs is bolstering market expansion.

The UK market is driven by the growing demand for over-the-counter biologics and prescription medications. Adoption of advanced packaging formats is being boosted by a strong focus on patient safety, anti-counterfeiting measures, and serialization requirements. Growing investments in recyclable and environmentally friendly packaging options are also boosting market growth.

France pharmaceutical packaging market is driven by rising healthcare and a strong domestic pharmaceutical sector. To maintain medication integrity and patient compliance, there is an increasing need for barrier tamper-evident packaging. Government rules promoting eco-friendly materials and sustainable packaging are also impacting market expansion.

Italy’s market growth is driven by its export of pharmaceuticals and proficiency in packaging designs and machinery. Adoption is being driven by the strong demand for ampoules, vials, and blister packaging in both domestic and international markets. The market is still growing thanks to advancements in packaging technology and a focus on quality standards.

Spain’s market growth is driven by rising healthcare demand, expanding pharmaceutical production, and growing manufacturing of generic drugs. Growth is being aided by the expansion of hospital infrastructure and the need for affordable legal packaging options. The nation is also seeing an increase in the use of sustainable packaging materials.

Tier 1

Tier 2

Tier 3

By Material Type

By Packaging Type

By Dosage Form

By End-User

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarEurope Pharmaceutical Packaging Market