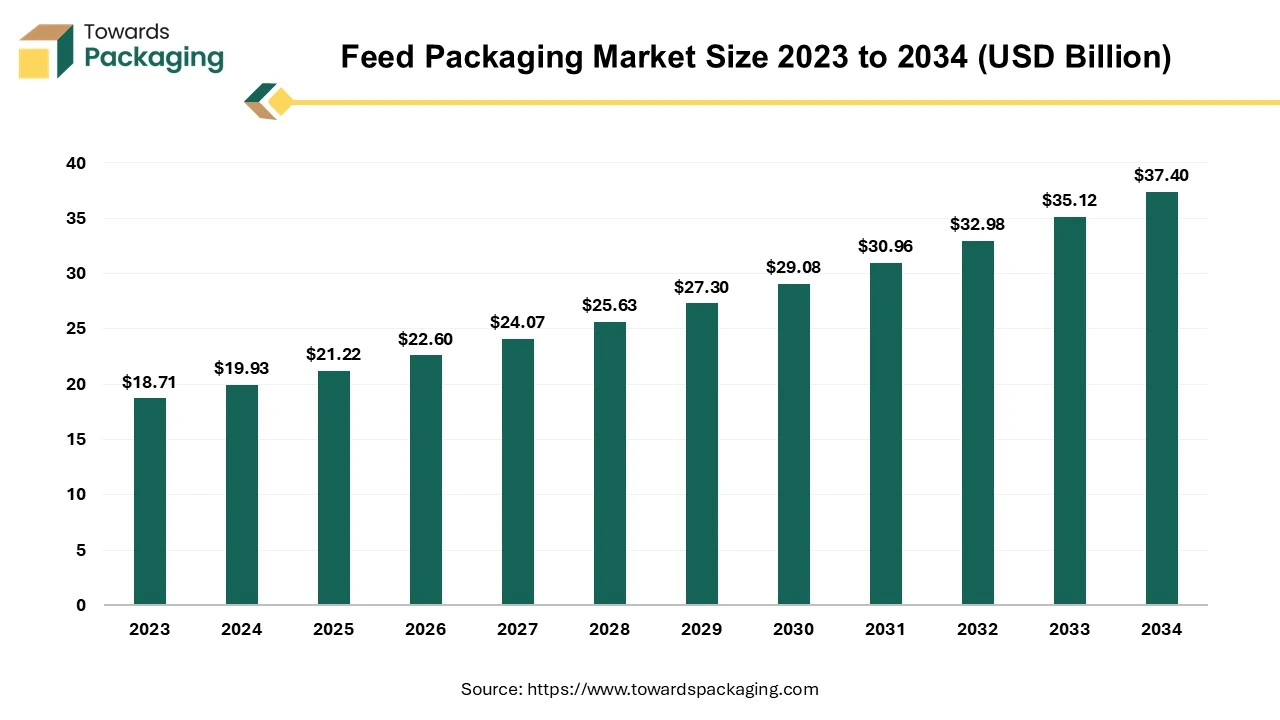

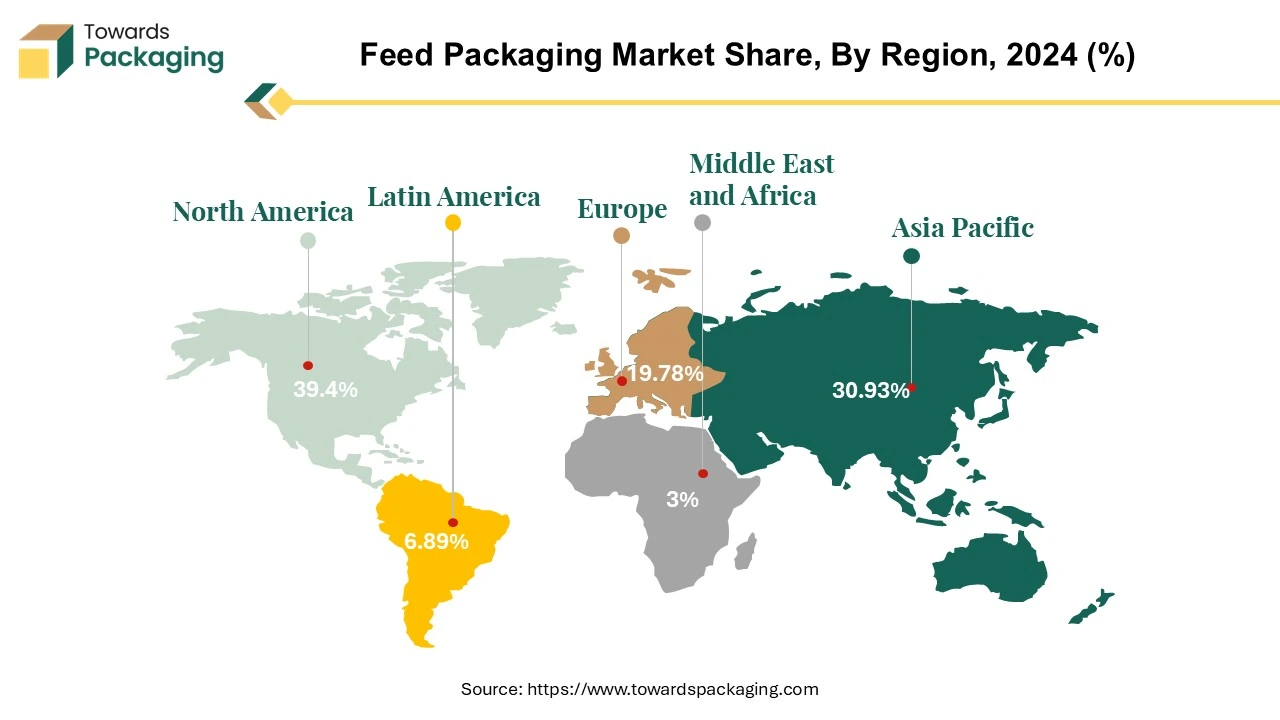

The feed packaging market is forecasted to expand from USD 22.61 billion in 2026 to USD 39.84 billion by 2035, growing at a CAGR of 6.5% from 2026 to 2035. This report delves into key market segments, including material types (paper, plastic, metal, jute, glass) and end-users (livestock, pets, aquaculture). North America dominates with a market share of 39.4%, followed by Asia-Pacific's significant role in feed packaging innovation, especially with flexible packaging solutions like laminates and films.

| Metric | Details |

| Market Size in 2025 | USD 21.23 Billion |

| Projected Market Size in 2035 | USD 39.84 Billion |

| CAGR (2026 - 2035) | 6.5% |

| Leading Region | North America |

| Market Segmentation | By Material, By End Users and By Region |

| Top Key Players | Amcor plc, Mondi, Huhtamaki, ProAmpac, El Dorado Packaging. |

Feed, being the sustenance for animals, requires packaging solutions that safeguard the product and ensure its safety for animal consumption.

The feed packaging market plays a pivotal role in ensuring animal feed products' safe and efficient distribution. As the global demand for animal feed continues to rise with the growth of the agriculture, livestock, and pet care industries, the need for reliable and innovative packaging solutions becomes increasingly crucial. Globally, the commercial feed manufacturing industry is anticipated to have a turnover and sales value of US$ 85 billion annually. To provide the industry with branded feed raw ingredients, tools, and ingredients for processing, handling and technical services around the globe.

The global compound feed production, surpassing one billion tonnes yearly, forms a robust foundation. This extensive output, combined with the commercial feed manufacturing's impressive annual turnover exceeding US $400 billion, is poised to propel substantial growth in the feed packaging market as the demand for efficient packaging solutions intensifies alongside the expanding feed production sector.

Feed packaging serves as a protective barrier, preserving the nutritional integrity of the feed while meeting regulatory standards for safety and information disclosure. This dynamic market is characterized by ongoing advancements in packaging materials and design, sustainability initiatives, and a keen focus on meeting the diverse needs of end-users in the agriculture and animal husbandry sectors.

AI is simplifying feed packaging by making precise demand forecasting and inventory control possible. Appropriate sealing, accurate weight, and contamination control are guaranteed by intelligent sensors and AI-based monitoring systems. These innovations enhance packaging dependability and lower operational losses. Additionally, supply chain coordination and warehouse management are optimized by AI-driven analytics. Automated systems preserve packaging safety regulations while increasing productivity. Purchasing raw materials is managed more effectively with the use of predictive tools. AI also lowers packaging errors by monitoring performance in real time.

The feed packaging market is characterized by intense competition among key industry players, Including Amcor plc, Mondi Huhtamaki, ProAmpac, El Dorado Packaging, LC Packaging, Plasteuropa, Winpak Ltd., ABC Packaging Direct, Constantia Flexibles. These entities are making significant investments in the manufacturing of Feed packaging solutions. Notably, industry leaders are adopting inorganic growth strategies such as acquisitions, mergers, partnerships, and collaborations to augment their product portfolios, thereby contributing to the global expansion of the feed packaging market.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Mondi | Weybridge, England | United Kingdom | Global leader in industrial and agricultural packaging with strong feed bag portfolio | Multiwall paper bags, feed packaging solutions |

| 2 | Berry Global | Evansville, Indiana | USA | Major supplier of flexible films and industrial packaging materials | Feed packaging films and bags |

| 3 | ProAmpac | Cincinnati, Ohio | USA | Strong presence in agricultural and feed flexible packaging markets | Laminated feed bags and pouches |

| 4 | LC Packaging | Waddinxveen, South Holland | Netherlands | Global supplier of FIBCs and agricultural packaging products | Bulk feed bags and FIBCs |

| 5 | NNZ Group | Groningen | Netherlands | Specialized agricultural packaging supplier with strong feed market exposure | Feed sacks, agricultural packaging |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Bischof+Klein | Lengerich, North Rhine-Westphalia | Germany | Major producer of heavy-duty industrial packaging films | Feed and agricultural packaging |

| 2 | Coveris | Vienna | Austria | Provides durable flexible packaging solutions for agricultural applications | Feed packaging films |

| 3 | Sonoco Products Company | Hartsville, South Carolina | USA | Industrial packaging supplier serving agricultural markets | Multiwall bags and industrial packaging |

| 4 | Greif | Delaware, Ohio | USA | Strong industrial bulk packaging portfolio | Bulk feed packaging solutions |

| 5 | Billerud | Solna, Stockholm County | Sweden | Leading supplier of sack paper for feed packaging applications | Kraft and sack paper solutions |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Muscat Polymers | Muscat | Oman | Specialist manufacturer of woven PP feed bags | Woven feed sacks |

| 2 | United Bags | Aylesbury, England | United Kingdom | Focused supplier of agricultural and feed packaging bags | Feed and agricultural sacks |

| 3 | Shalimar Group | Kolkata, West Bengal | India | Producer of woven PP feed and fertilizer packaging | Feed bags and woven sacks |

| 4 | Emmbi Industries | Mumbai, Maharashtra | India | Supplier of woven industrial and agricultural packaging | Feed and bulk packaging |

| 5 | Anduro Manufacturing | Morgan Hill, California | USA | Producer of industrial paper-based feed packaging | Multiwall feed bags |

| Trends | |

| Technological Advancements in Packaging Materials |

|

| Sustainability Initiatives |

|

| Customization for Branding and Information |

|

| Globalization and Market Expansion |

|

North America stands out as a prominent leader in the feed packaging market. Fuelled by the Vigor of its expansive agriculture and livestock industries, the region has become a focal point for advancements in packaging methodologies and a vanguard for sustainable practices.

Manufacturers in North America are spearheading the adoption of cutting-edge packaging technologies, setting a high standard for innovation within the industry. This proactive approach reflects a commitment to staying ahead of the curve and underscores the region's dedication to meeting the evolving needs of the agriculture and animal husbandry sectors. Approximately 284 million tonnes of animal feed were eaten in the United States, which is supported by the packaging, helping to grow the feed packaging market, which supplies the packaging to animal feed producers.

A key aspect of North America's dominance in the feed packaging arena lies in the strategic utilization of leading materials. High-density polyethene (HDPE) and polypropylene (PP) emerge as the region's primary choices for packaging solutions. The selection of these materials is driven by their exceptional properties, including durability, moisture resistance, and the capacity to endure diverse environmental conditions.

HDPE, known for its robustness and resistance to wear and tear, ensures that feed products remain securely packaged throughout the supply chain. Its resilience makes it particularly adept at safeguarding the nutritional integrity of the feed, a critical consideration in the overall quality assurance process. Meanwhile, polypropylene brings advantages, offering a combination of strength and flexibility that enhances the packaging's ability to withstand external pressures, maintaining the feed's safety and freshness.

Moreover, deploying HDPE and polypropylene aligns with the stringent regulatory standards prevalent in North America, ensuring that packaged feed meets and exceeds safety requirements. This commitment to compliance enhances consumer confidence and reinforces the region's reputation for delivering high-quality feed packaging solutions.

In essence, North America in the feed packaging market is not only a witness to its robust agricultural foundation but also a result of its proactive stance in embracing technological advancements and sustainable practices. The strategic use of materials like HDPE and polypropylene underscores a commitment to product integrity and safety, establishing the region as a trendsetter in the evolving landscape of feed packaging. As the market continues to evolve, North America's role as a regional leader is likely to persist, driven by its dedication to excellence and responsiveness to industry dynamics.

Canada Feed Packaging Market Trends:

Most of the business owners and customers choose feed packaging option for luxury products and high-end products. Vancouver premium packaging could also assist in solving Canada's most challenging environmental challenges. Nearly half of the wastage in Toronto comes from Single-family homes as most dismissed fruits and vegetables, specifically those without specific containers spoiled before consumption. But within the fruits and vegetables kind as whole produce lead to maximum majority with lettuce , bananas by being the most commonly disappeared.

Asia-Pacific has emerged as a significant regional leader, propelled by the rapid growth of its aquaculture and poultry industries. This surge in demand for animal feed has positioned the region as a critical player in the global feed packaging sector. One of the distinguishing features driving Asia-Pacific's prominence is the widespread adoption of flexible packaging materials. Laminates and films, in particular, have become integral components of the packaging ecosystem in this region. Their popularity is attributed to their cost-effectiveness and remarkable adaptability to diverse packaging formats. The flexibility of these materials not only facilitates efficient packaging processes but also ensures the preservation of feed quality throughout the supply chain.

Exploring bio-based plastics in feed packaging aligns with the broader industry trend towards sustainability. By incorporating these innovative materials, Asia-Pacific manufacturers are addressing environmental concerns and positioning themselves as leaders in meeting regulatory standards. This proactive stance enhances the region's reputation for adopting cutting-edge solutions and places it at the forefront of the evolving global feed packaging market. As Asia-Pacific continues to navigate the intersection of growth, innovation, and sustainability, its role as a second regional leader is poised to strengthen, contributing significantly to the overarching narrative of the feed packaging industry.

Europe’s packaging industry is on a steady growth trajectory which is filled by urge from industries such as food and beverage, pharmaceuticals and automotive .Countries such as France,spain and Italy are finding significant growth driven by both local and worldwide pressures to accept sustainable practices. Sustainability is the main trend in Europe packaging solutions as Denmark and Belgium have paved the way for innovative deposit systems and high recycling rates which sets the benchmark for other nations. Countries like the Netherlands are pushing boundaries with ambition for entirely recyclable and fossil -free packaging too.

The selection of materials for feed packaging plays a pivotal role in determining the quality and longevity of the products. Polyethylene (PE) and polypropylene (PP) stand out as predominant choices, maintaining their dominance owing to their versatile properties, inherent strength, and moisture resistance. These materials collectively form a robust barrier, shielding the feed from external elements and preserving its nutritional content.

Polyethylene, known for its durability and resistance to wear and tear, provides a secure and protective packaging solution. Its strength ensures the safe transportation and handling of feed products throughout the supply chain, contributing to the overall quality assurance process. Simultaneously, polypropylene brings its unique combination of strength and flexibility to the forefront, enhancing the packaging's ability to endure external pressures and preserving the safety and freshness of the feed.

In response to the growing emphasis on sustainability, there is a noticeable shift towards alternative packaging materials. Paper-based packaging is gaining significant traction, particularly in regions with a heightened focus on eco-conscious practices. Utilizing paper bags and cardboard boxes is becoming a preferred choice due to their recyclability and environmentally friendly attributes. Additionally, the feed packaging industry is witnessing a surge in the use of bio-based plastics derived from renewable sources. This shift reflects a collective commitment within the industry to mitigate its environmental impact, aligning with global efforts to promote sustainability and reduce the ecological footprint of packaging materials.

The diverse landscape of feed packaging end users encompasses various sectors within agriculture and animal husbandry. Livestock farming, including cattle, poultry, and swine, stands as a primary end user, driving the demand for bulk packaging solutions tailored to the specific needs of each segment. The pet food industry represents another crucial end user, with an increasing focus on packaging formats that enhance pet owners' convenience while preserving the products' freshness and nutritional quality.

The aquaculture sector, experiencing substantial growth globally, has distinct packaging requirements to address the unique challenges associated with aquatic feed. This includes considerations for water resistance, durability, and efficient storage and transportation.

Dynamic trends, regional variations, and a commitment to sustainability characterize the feed packaging market. As the industry evolves, stakeholders are challenged to balance innovation with regulatory compliance and environmental responsibility. The choice of packaging materials, technological advancements, and customization for branding are critical factors shaping the market. At the same time, the global expansion of crucial players reflects the industry's responsiveness to diverse regional needs. As the demand for high-quality animal feed persists, the feed packaging market is poised for continued growth and transformation.

Feed packaging uses polypropylene, polyethylene, and multi-layer paper for durability and moisture protection. Suppliers prioritize contamination-free materials.

Key Players: Mondi Group, Berry Global

Strong distribution networks deliver bulk packaging to livestock and agricultural producers. Efficient transport reduces damage and spoilage risks.

Key Players: Maersk, DB Schenker

The market is adopting recyclable and biodegradable feed bags. Sustainability goals are to reduce plastic dependency.

Key Players: Republic Services, Remondis

In January 2026, Mondi announced it has received nine WorldStar Packaging Awards for 2026, highlighting excellence in sustainable and circular design. The winning, fiber-based solutions, including the recyclable re/cycle HiProtex Paper, focus on replacing non-recyclable plastics to enhance shelf-life. These awards emphasize Mondi's commitment to innovation in both food and industrial packaging sectors.

In February 2026, Huhtamaki and Xampla announced the launch of a plastic-free, grease-resistant barrier coating for food and feed applications. The coating uses Morro plant-protein technology and is designed to be fully recyclable and home-compostable. This innovation provides a sustainable alternative to traditional coatings, complying with the EU Single-Use Plastics Directive.

By Material

By End Users

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarFeed Packaging Market