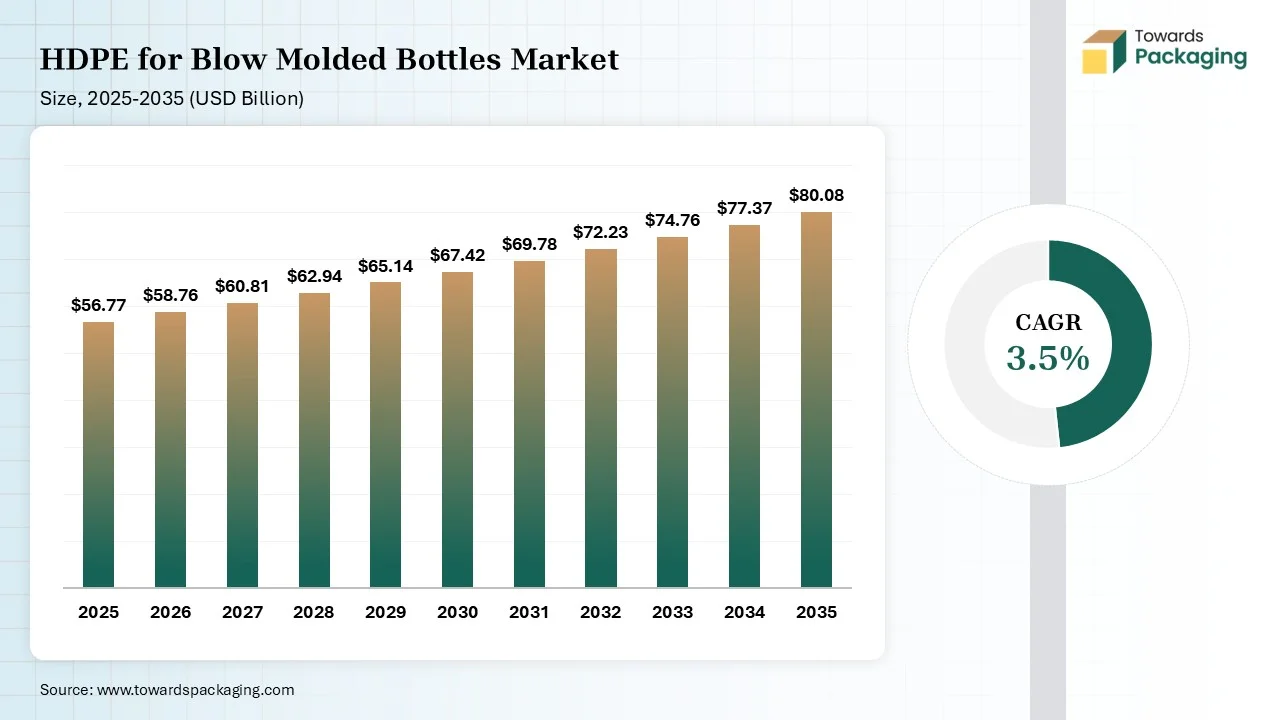

The HDPE for blow molded bottles market is projected to grow from USD 58.76 billion in 2026 to USD 80.08 billion by 2035, registering a CAGR of 3.5% during the forecast period. This report provides comprehensive coverage of market size, segment-wise data, and regional insights, along with detailed competitive analysis, company profiling, and value chain evaluation. It also includes trade data, manufacturer and supplier analysis, offering a complete view of the industry driven by rising demand across pharmaceutical, food, and chemical sectors.

HDPE for blow molded bottles is a durable and versatile thermoplastic utilised to generate chemical-resistant, rigid, and lightweight hollow containers. It is suitable for shampoo bottles, milk jugs, and chemical bottles because of its superior strength-to-weight ratio and capability to be handled through injection or extrusion blow molding.

Technological transformation in the HDPE for blow molded bottles market plays a significant role in developing high-performance packaging. These advanced technology supports in developing high-quality and durable packaging. It also helps in predicting the potential of the packaging that attract huge consumer base towards this sector. Advanced packaging technologies supports in meeting the sustainability goals of the industries.

The major raw materials utilised in this market are virgin HDPE, recycled HDPE, and HDPE granules or chips. It supports in developing cost-effective, durable, and excellent processability.

The component manufacturing in this market comprises Mold (shaping), Hopper (feeding), Die Head (forming parison), Extruder (melting), and Cooling System. These are essential steps required to develop high-quality packaging bottles.

This segment ensures high-quality production for the huge distribution of the packaging. It supports enhancing the packages to meet the demand of the consumers.

The virgin HDPE segment dominated the market with 68% share in 2025. Due to its enhanced chemical resistance, stiffness, and tensile strength. It has high-performance reliability which encourage its adoption in a wide range of industries. This is extremely used in chemical, food and beverages industries.

The recycled HDPE segment is expected to experience the fastest growth in the market with 5.6% CAGR during the forecast period. Due to the rising sustainability goals among major market players. It has high chemical resistant and weight-to-strength ratio which has pushed the demand for this sector profoundly. With the presence of strict ecological standards, the packaging industry has adopted this segment highly.

The 101 ml – 500 ml segment dominated the market with 45% share in 2025. Due to its convenience, versatility, and widespread acceptability. These are considered as standard size for the packaging of a wide range of products. The rapid expansion of personal care and pharmaceutical industry has fuelled the demand for this segment.

The above 500 ml segment held the second largest share of 32% in 2025. Due to its low permeability, durability, and fracture resistance these are widely accepted. These bottles are widely used in automotive, petrochemical, and chemical industries. These are the cost-effective solution for packaging.

The 31 ml – 100 ml segment held the third largest share of 15% in 2025. Due to its safety, durability, and chemical resistance, these are widely accepted this segment. These can be customized widely which has raised the demand of this segment. These are widely used in the pharmaceutical sector for packaging of pills, capsules, and liquids.

The less than 30 ml segment is expected to experience the fastest growth in the market with 4.5% CAGR during the forecast period. Due to its high versatility and portability has pushed the demand for this segment. It has high chemical resistant and efficacy has fuelled the demand for this segment. These are widely used in the cosmetics, food, and pharmaceutical industries.

The screw closure segment dominated the market with 40% share in 2025. Due to its cost-effectiveness, leak-proof sealing, and versatility, it has raised the demand for this segment. These are used in high-volume packaging of household chemical, food and beverages packaging. These have tamper-evident packaging which has raised its adoption in a wide range of industries.

The other closures segment is expected to experience the fastest growth in the market with 4.8% CAGR during the forecast period. Due to its child resistance, user-friendly, and tamper-evident packaging has pushed the demand for this segment. The rapid innovation in the closure sector has pushed the demand for this segment. These are extensively used in the industrial, pharmaceutical, and home care sector.

The snap closure segment held the third largest share of 15% in 2025. Due to the rising demand for hygienic and convenient packaging. These are considered as highly functional closure which has raised the demand for this sector. These are majorly used in the shampoo, lotions, and other condiments packaging. These are low-cost packaging available in this sector which has fuelled the demand for this sector.

The pushpull closure segment held the fourth largest share of 12% in 2025. Due to its secure sealing and enhanced versatility. The rising demand for home care and personal care application has pushed the demand for this segment. The rapid innovation in the push and pull solutions has raised the adoption of this segment.

The disc top closure segment held the fifth largest share of 10% in 2025. Due to the rising demand for convenience in this sector has fuelled the demand for this closure. The increasing chemical-resistant, ease of processing, and cost-effectiveness. The rising demand for lightweight solution has pushed the innovation and expansion of this segment.

The spray closure segment held the sixth largest share of 8% in 2025. Due to huge demand for superior chemical resistance has fuelled the expansion of this segment. The increasing demand for disinfectant, personal care, and home cleaner industry has boosted the demand for this segment. These are considered as consumer-friendly and it has the capacity to handle corrosive chemicals has enhanced its adoption.

The pharmaceutical & healthcare segment dominated the market with 30% share in 2025. Due to its high moisture-barrier and excellent chemical resistant potential. There is a huge demand for safe packaging in this industry which has raised the adoption of this segment. The increasing demand for lightweight packaging has pushed the adoption for this sector.

The food & beverage segment held the second largest share of 28% in 2025. Due to the rising concern towards food safety and hygienic packaging. It supports in enhancing the shelf life of the food products. These packaging are used for safety during transportation of food products.

The chemical & petrochemical segment held the third largest share of 22% in 2025. Due to its high chemical-resistant and durability quality. The rising shift towards recyclable packaging has fuelled the demand for this segment. These are considered ideal packaging option for corrosive chemicals.

The personal care & cosmetics segment held the fourth largest share of 12% in 2025. Due to its cost-effectiveness, eco-friendliness, and durability. The rising concern towards adoption of eco-friendly packaging to enhance the brand image has raised the demand for this sector. It protects products from air, light, and moisture which has raised the adoption of this segment.

The household & homecare segment is expected to experience the fastest growth in the market with 4.5% CAGR during the forecast period. Due to the increasing concern towards using sustainable packaging of the products. There is a huge demand for hygienic and convenient packaging in this sector. The presence of huge customisation option has raised the demand for this segment.

North America dominated the HDPE for blow molded bottles market with 34% share in 2025, due to the rapid expansion of pharmaceutical and food industry. The rapid shift towards sustainable packaging options has fuelled the demand for this industry. The presence of strict ecological guidelines has also raised the production of these molded bottles. The huge advancement in the manufacturing technology has raised the demand for this industry.

The U.S. HDPE for Blow Molded Bottles Market Trends

The rising integration of recycled content has fuelled the demand for the HDPE for blow molded bottles market. The increasing focus towards manufacturing process has enhanced the demand for this industry. The enhanced production capacity has raised the demand for such packaging bottles. The rising sustainability goals of the major market players has pushed the demand for this industry.

Asia Pacific expects the fastest growth in the market with 5.2% CAGR during the forecast period. The massive consumers and rapid industrialisation have fuelled the demand for this industry. The rising demand for secure and lightweight packaging has fuelled the demand for this sector. The rapid expansion of healthcare sector has pushed the adoption of this market. The increasing focus on reduction of packaging waste has enhanced the production process of this sector.

China HDPE for Blow Molded Bottles Market Trends

The increasing demand for high-performance, lightweight, and durable packaging has fuelled the demand for the HDPE for blow molded bottles market in China. There is a huge demand for sustainable packaging which has raised the manufacturing of these bottles. It has high chemical resistance, durability, and cost-efficiency which has raised its usage in a wide range of industries. The presence of huge manufacturing capacity has raised the demand for this industry and pushed its expansion.

By Resin Source

By Bottle Capacity

By Cap/Closure Type

By EndUse Industry

By Manufacturing Technology

By Distribution Channel

By Regions

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarHDPE for Blow Molded Bottles Market