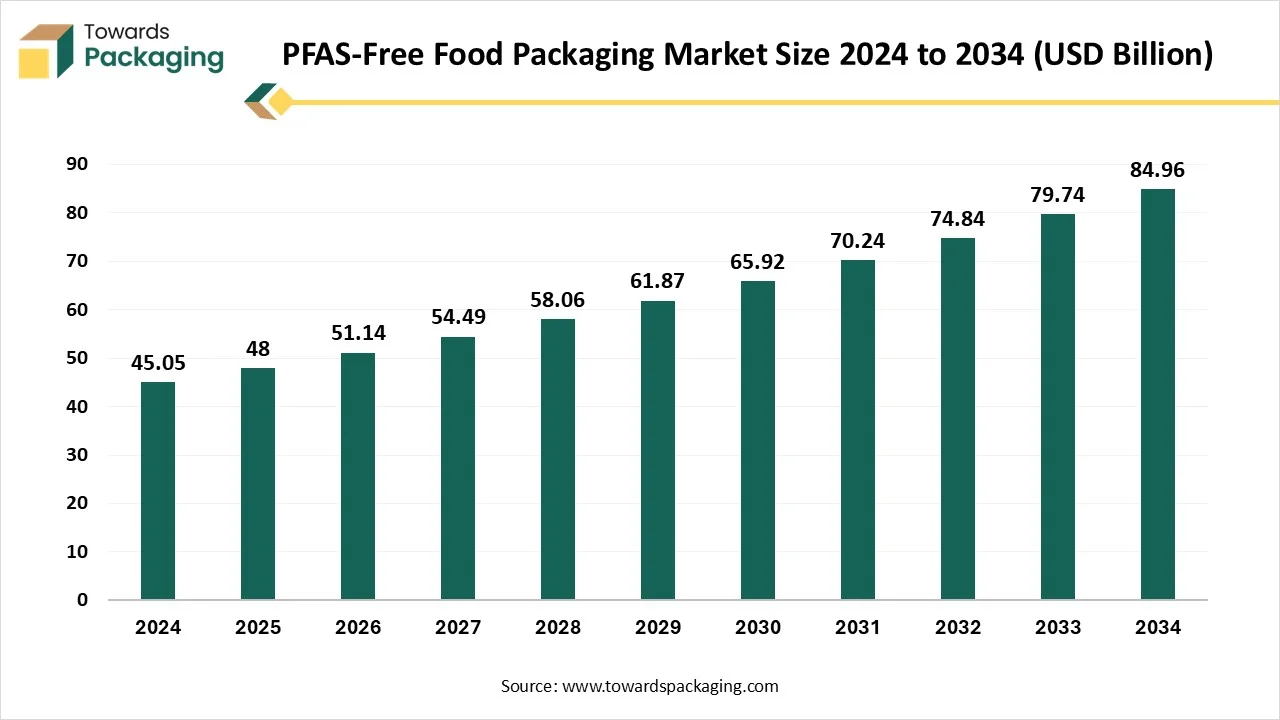

The PFAS-Free Food Packaging market is forecasted to expand from USD 51.14 billion in 2026 to USD 90.53 billion by 2035, growing at a CAGR of 6.55% from 2026 to 2035. This report provides comprehensive insights into market trends, segmentation by packaging type, material, and end-use sector, and detailed regional analysis covering North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Key players such as Huhtamaki, Footprint, Georgia-Pacific, Stora Enso, Vegware, and Sabert Corporation are profiled with information on their products, market presence, and strategies.Competitive analysis, trade flows, and value chain dynamics are also discussed to guide manufacturers and suppliers in identifying growth opportunities.

Over the years, sustainability has gained significant traction, with prominent market players increasingly focusing to leverage leveraging their expertise in sustainable packaging solutions to strengthen their market presence. Additionally, the market is expanding in various emerging economies. North America is expected to dominate the region, fuelled by growing awareness regarding the health risks associated with PFAS compounds and a stringent government framework.

PFAS-free food packaging refers to food-contact packaging materials that do not contain per- and polyfluoroalkyl substances (PFAS), a group of synthetic chemicals widely used for their grease, oil, and water-resistant properties. Due to growing health concerns, regulatory bans, and consumer demand, PFAS-free alternatives are being rapidly adopted across packaging applications.

| Metric | Details |

| Market Size in 2025 | USD 48.00 Billion |

| Projected Market Size in 2035 | USD 90.53 Billion |

| CAGR (2026 - 2035) | 6.55% |

| Leading Region | North America |

| Market Segmentation | By Packaging Type, By Material Type, By End-Use Sector and By Region |

| Top Key Players | Huhtamaki, Footprint, Georgia-Pacific, Stora Enso, Vegware, Sabert Corporation |

In today's rapidly evolving technological landscape, AI integration emerges as a game-changer and holds the potential to revolutionize PFAS-free food packaging by enhancing sustainability, reducing wastage, and streamlining operations. Artificial integration-driven solutions significantly increase the use of multiple materials or components within the packaging to improve functionality and boost sustainability. In the packaging industry, AI is widely being adopted by businesses to achieve unprecedented efficiency and innovation. Machine learning (ML) algorithms can effectively analyze the data related to material properties, environmental impact, and production processes, as well as predict valuable insights to increase overall productivity through efficient resource allocation.

How is the Rising Consumer Awareness of the Harmful Effects of PFAS Impacting the Market’s Growth?

The increasing consumer awareness of the harmful effects of PFAS on human health is expected to drive market growth during the forecast period in the packaging industry. PFAS-free food packaging plays an integral role in the safety of consumers. Per- and polyfluoroalkyl substances are a group of man-made chemicals that have been commonly linked to chronic health issues such as immune disorders, cancer, rising cholesterol levels, hormonal imbalance, developmental effects in children, and others. As consumers are becoming more aware of the potential health risks associated with PFAS has led to an increasing demand for safer and PFAS-free alternatives, compelling food service industries to adopt PFAS-free options.

High Costs

The high costs associated with PFAS-free alternatives are anticipated to hamper the market's growth. PFAS-free alternatives with high-performance abilities are significantly more expensive than conventional PFAS-containing packaging, which can adversely impact the affordability of food items, particularly for budget-conscious consumers. Moreover, the need for rigorous testing and certification to ensure safety is likely to limit the expansion of the global PFAS-free food packaging market.

Stringent Government Regulations

The stringent government regulations are projected to offer lucrative growth opportunities to the PFAS-free food packaging market during the forecast period. Several governments around the world continue to tighten the ban or restrictions on these harmful chemicals. Regulatory bodies such as the U.S. Food and Drug Administration (FDA), Canadian Food Inspection Agency (CFIA), and European Union (EU) have implemented their own PFAS regulations to address health concerns and provide additional protection to consumers. Such stringent policies are compelling manufacturers operating in the food packaging industry to adopt safer and eco-friendly alternatives as well as increase their investment in research and development (R&D) to ensure compliance.

The quick-service restaurants (QSR) segment holds a dominant presence as PFAS is the most widely utilised to create grease-proof and water-resistant barriers. These harmful chemicals can be commonly found in products such as fast-food wrappers, pizza boxes, bakery papers, and others. The growth of the segment is mainly driven by the rising awareness regarding food safety to prevent serious health issues associated with PFAS food packaging and stringent regulatory compliance. Quick-service restaurant businesses require meeting regulatory requirements for product packaging to stay ahead and meet evolving consumers' desires.

On the other hand, the retail and supermarket segment is expected to grow at a notable rate. PFAS-free packaging solutions are increasingly being adopted in retail and supermarkets to address growing consumer concerns about food safety and sustainable alternatives. Food items such as frozen foods, beverages, ready-to-eat meals, snacks, and others require protective packaging to prevent contamination and maintain integrity as well as freshness. In addition, stringent regulatory frameworks are encouraging retail and supermarkets to align with sustainability and adopt non-toxic packaging materials.

The paper and paperboard (PFAS-free coated) segment dominated the market with the largest share in 2024, owing to the rising investment of key market players for innovations in barrier coating and increasing use of these materials in packaging formats such as boxes, cartons, wraps, and trays. In the food packaging industry, PFAS-free coated paper and paperboard are widely adopted to ensure health compliance with food safety standards and prevent the risk of health disorders associated with PFAS exposure. Paper and paperboard serve as sustainable packaging alternatives owing to its due to their biodegradable nature and becoming more prevalent in response to meet the eco-conscious consumer demand.

On the other hand, the bioplastics are anticipated to grow at the fastest CAGR, owing to the rising concerns about the environmental and health impacts of PFAS chemicals. Bioplastics are gaining immense popularity as PFAS-free alternatives in the food packaging sector owing to their versatility, durability, lightweight, and excellent protection properties against moisture and oxygen, which also makes them ideal for various applications, including wraps, containers, and pouches.

The wraps and liners segment registered its dominance over the global PFAS-free food packaging market in 2024, owing to the rising adoption of PFAS-free wraps and liners to reduce the potential environmental and health risks associated with "forever chemicals" or PFAS. In the food packaging industry, PFAS-free wraps and liners are widely utilized for wrapping sandwiches, hamburgers, cheeses, and other food items to prevent cross-contamination. PFAS-free wraps and liners also serve as an eco-friendly alternative to plastic as they use plant-based coatings and barrier materials while maintaining recyclability and compostability.

On the other hand, the clamshells and hinged containers are expected to witness remarkable growth during the forecast period. Clamshell and hinged containers are widely used in the food packaging industry, mainly for takeout and to-go meals. These PFAS-free containers are often biodegradable or compostable, breaking down naturally as well as eliminating the risk of harmful chemicals leaching into food. These containers are generally being produced using PFAS-free materials like bagasse and other plant-based fibers, offering an eco-friendlier alternative to conventional plastics.

In the year 2025, the Asia Pacific region is predicted to witness a major evolution in its chemical tracking frameworks, including the acceptance of the Globally Harmonized System, enhanced control of pre-and polyfluoroalkyl substances, and heavily stringent regulations, which are designed after the usage of the EU’s Registration, Authorization, Evaluation and Restrictions of Chemicals systems, among others. The APAC region is leading the globe in chemical manufacturing, with the most current data displaying the integrated countries selling approximately USD 3 trillion of chemicals in 2023. As nations in the region accept more rigid measures, the concentration on toxic chemicals is changing with a notable move towards restricting or banning materials that showcase significant risk.

North America, especially the U.S. and Canada, has a well-established presence of the food and beverage industry, which spurs the demand for PFAS-free food packaging as a safe and sustainable packaging solution. Factors such as stringent government standards, growing emphasis on sustainability, increasing adoption of non-toxic packaging materials, surging consumer demand for safe food packaging, and rapid technological innovation are expected to drive the growth of the PFAS-free food packaging market during the forecast period. In addition, numerous key players in the region are heavily investing in innovative barrier technologies, such as bio-based polymers, plant-based coatings, and water-based alternatives, to gain a competitive edge and meet the evolving consumer demand for safer food packaging options.

On the other hand, the growth of the European market is mainly attributed to the implementation of stringent regulatory compliance by the authorized bodies like the EU, rapid technological improvement in bio-based packaging materials and green packaging, rising awareness of the harmful effects of per- and polyfluoroalkyl substances (PFAS), and increasing consumer inclination for safer and sustainable packaging solutions. Europe's stringent environmental regulations have created a strong market presence for the PFAS-free food packaging market. Moreover, the rapid expansion of the food and beverage industry has led to an increasing demand for PFAS-free food packaging to address potential health issues with the use of harmful chemicals and improve environmental sustainability by replacing conventional plastics.

By Packaging Type

By Material Type

By End-Use Sector

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPFAS-Free Food Packaging Market