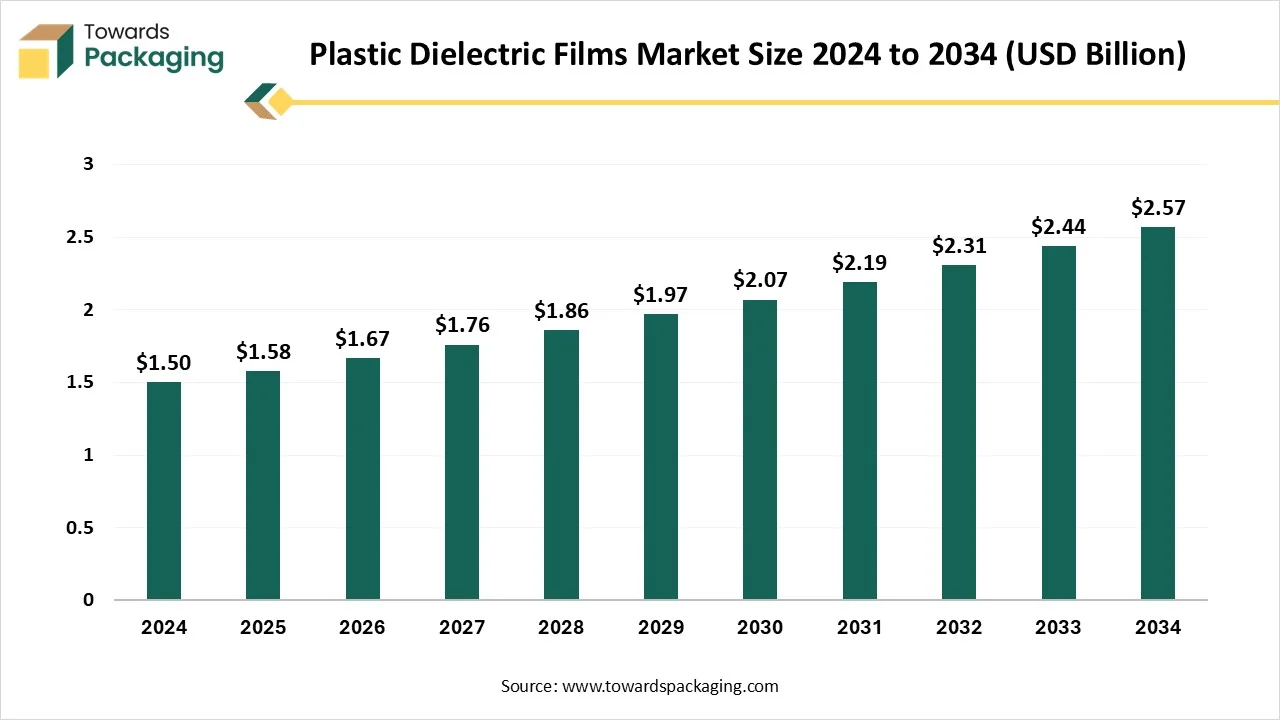

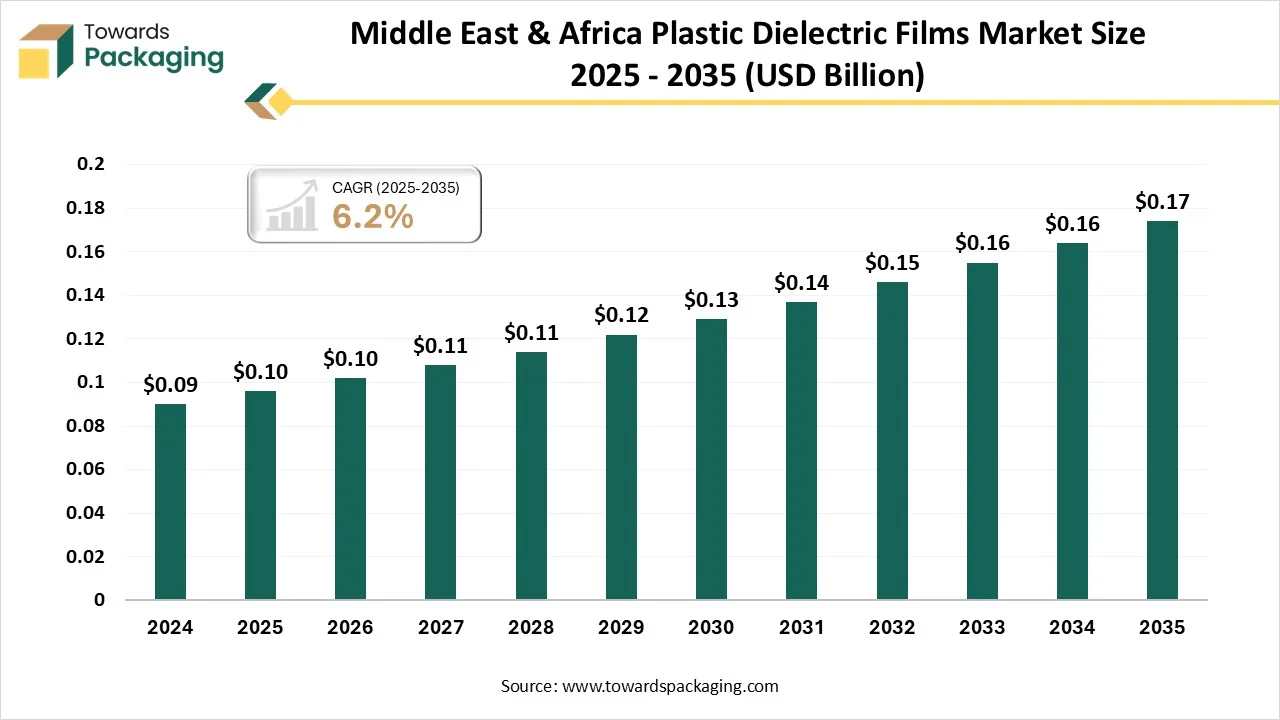

The plastic dielectric films market is forecasted to expand from USD 1.67 billion in 2026 to USD 2.71 billion by 2035, growing at a CAGR of 5.55% from 2026 to 2035. The rising demand for renewable energy sector, electric vehicles (EV), and electronics. With the continuous advancement of material science and production process the market is evolving rapidly.

The study further explores logistics and distribution networks, regional demand patterns, and technological advancements in high temperature and low loss dielectric materials. In addition, the report highlights competitive strategies of leading manufacturers, innovation in high performance polymer films, and growing applications in electrical and electronics, renewable energy systems, and automotive EV components, helping businesses understand market dynamics and identify future growth opportunities in the plastic dielectric films market.

The plastic dielectric films refer to the global industry for polymer-based thin films that provide electrical insulation (high dielectric strength, low dielectric loss) and thermal/chemical stability for use in capacitors, transformers, flexible circuits, sensors, power electronics, and other high-voltage/high-frequency applications. Key film materials include PET, PEN, PP, PTFE, PVDF, PPS and specialty blends. The market growth is driven by increasing demand from consumer electronics, electrification of vehicles, renewable energy systems, miniaturization of electronic components, and the need for energy-efficient power conversion and insulation solutions.

The incorporation of AI technology in the plastic dielectric films market plays an important role in enhancing the quality of the films, real-time data analysis, automated system, and enhanced efficacy. The continuous demand for advancement of material and designing with optimization of designing process has enhanced the demand for incorporation of AI technology. Generative AI is utilized for efficient designing of various components such as film capacitors and useful in reducing the generation of waste materials. Advanced technology is helpful in improving the recycling process.

The U.S. is growing in domestic demand and import of plastic dielectric films in insulators and capacitors.

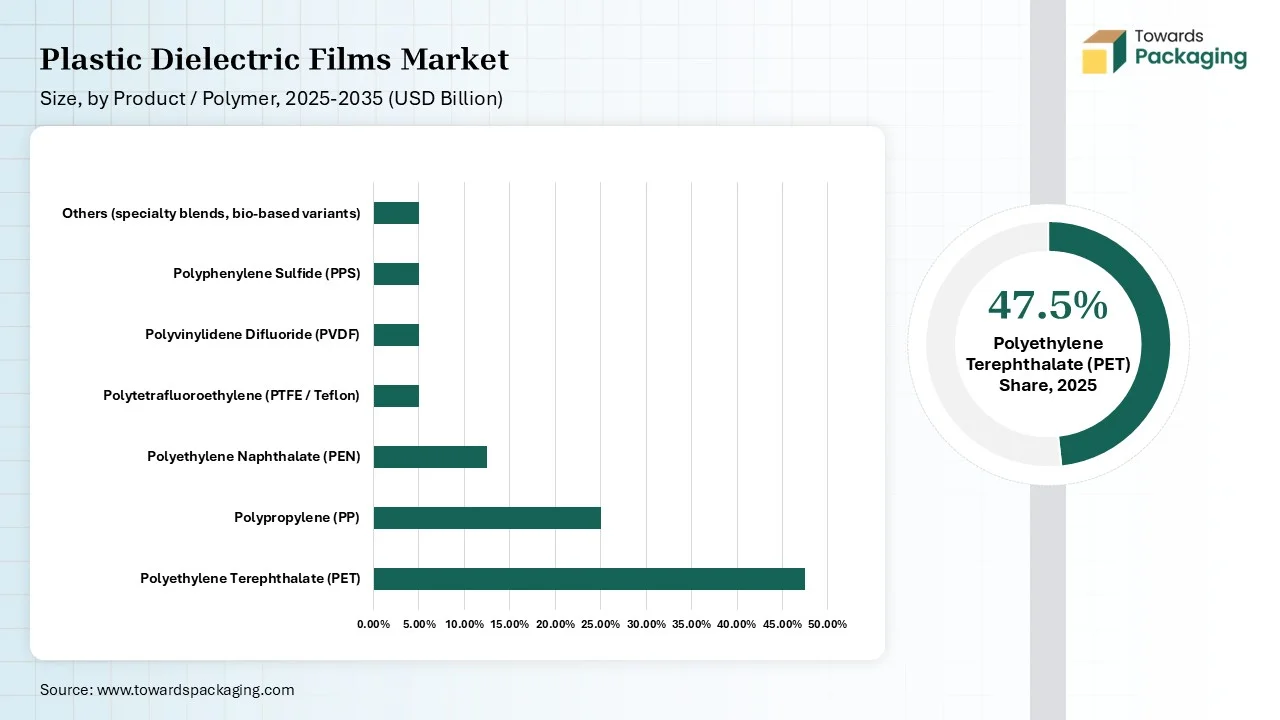

The major raw materials utilized in this market are Polytetrafluoroethylene (PTFE), Polyvinylidene Fluoride (PVDF), Polyphenylene Sulfide (PPS), Polyethylene Naphthalate (PEN), Polypropylene (PP), and Polyethylene Terephthalate (PET).

The major components used in this market are aluminum foil, paper & paperboard, polyvinyl chloride, polyethylene, and several other materials.

This segment plays an important role in interconnecting worldwide supply chain and manage handling in three steps primary, secondary, and tertiary.

| Regions/ Countries | Regulatory Bodies | Key Regulations |

| Canada | Environment and Climate Change Canada (ECCC) | EPR & single-use ban |

| Japan | Ministry of the Environment (MOEJ) | Plastic Resource Circulation Strategy |

| United States | FDA (food contact) | Prevent plastic pollution |

| India | Central Pollution Control Board | Monitor the quality of the plastics used for packaging to reduce plastic usage. |

Rising Demand for Electronic Products

The rising demand for electronics products has influenced the demand for the plastic dielectric films market. Increasing usage of devices such as laptops and smartphones has encouraged the development of this market. The rapid expansion of the renewable source of energy like wind and solar power has boosted the market to develop. Some of the major factors boosting the growth of the market are technological advancement, electronics and consumer devices, miniaturization and performance, electric vehicles, and material innovation.

Supply Chain Disruptions

Growing supply chain disruption of the dielectric films have hindered the growth of the market. Strict safety guidelines in the packaging industry have restricted the growth of this market. Huge development charges associated in this market has limited the innovation process of the industry.

High Performance Electronic Components

High performance electronic components have raised the opportunities for the market. Enhancing 5G/ IoT infrastructure, automotive sector, and consumer electronics industry has boosted innovation process in this market which resulted in widening scope. The development of 5G network and extended digital infrastructure need effective electronic components. The increasing worldwide production of flexible electronic modules has promoted several scopes in this market.

")

The polyethylene terephthalate PET segment dominated the plastic dielectric films market in 2024 due to its balanced performance and versatility. The growing consumer electronics industry, comprising wearable devices, smartphones, and tablets enhance the demand for this segment. This segment is driving the market for covering range from packing to films and fabrics to molded parts for automobiles and electronics, and others. It has enhanced thermal resistance, pushing the development of this market, thus influencing market segment for electric insulation resources.

The polyethylene naphthalate (PEN) segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing due to its chemical durability, dimensional stability, and excellent thermal resistance. This is accredited to its extensive application in film-grounded goods like optical displays, labels, flexible printed circuits, and laminates. PEN is considered as a high-performing fibre with improved hydrolytic steadiness and is mainly well-matched for things that are likely to oxidation due to its less oxygen penetrability.

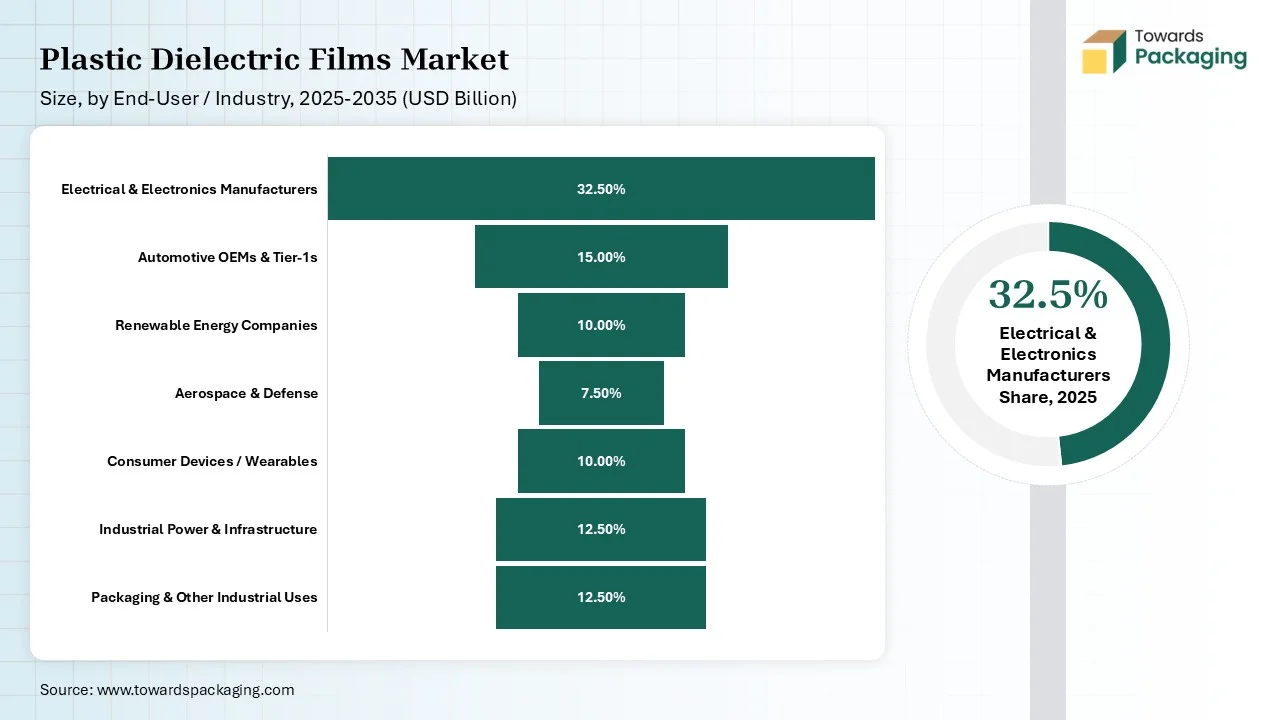

The electrical & electronics segment dominated the plastic dielectric films market in 2024 due to rising consumer electronics demand. This development is influenced by growing demand for high presentation dielectric films in circuit safety, sensors, and capacitor engineering. The ability of these packing to provide continuous insulation and excellent power and compressed electronic arrangements. Growth of customer electronics, coupled with improvements in renewable energy and electricity flexibility, has additionally enhanced practice.

The solar & wind energy systems segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing due to the insulating and energy storage potential. Necessity for the utilization of renewable sources has enhanced the demand for these films. Contribution of major market players for the development of this sector has boosted its demand.

")

The electrical & electronics manufacturers segment held the largest share of the plastic dielectric films market in 2024 due to smart electronics demand. Manufacturers majorly focus on efficiency of energy and develop insulating films. The increasing focus towards biodegradability and recyclability of the films has enhanced its demand in this market. The growing trend for miniature products has influenced the demand for this segment.

The automotive OEMs & EV applications segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing rapidly due to the rising demand for components in the automotive sector. High thermal resistance, safety features, and dielectric strength have upsurged the demand for this segment. The moldability and flexibility of the polymers facilitate integrated and complex EV designs which reduce part counts and simplify manufacturing processes.

The standard dielectric films segment held the largest share of the plastic dielectric films market in 2024 due to its cost-effectiveness and wide application in general insulation, electronics, and packaging. The upsurge in the demand of smartphones and various consumer electronics. It is cost-effective solution available in this market for safe packaging of the electronics products. The enhanced energy storage system has influenced the growth of this segment.

The high-temperature / low-loss specialty films segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing rapidly due to continuous material enhancement. The rising demand for superior insulation, high thermal resistance, and low power dissipation boost the growth for this market. The advancement in films make it lightweight and suitable for packaging a huge variety of electronic products.

")

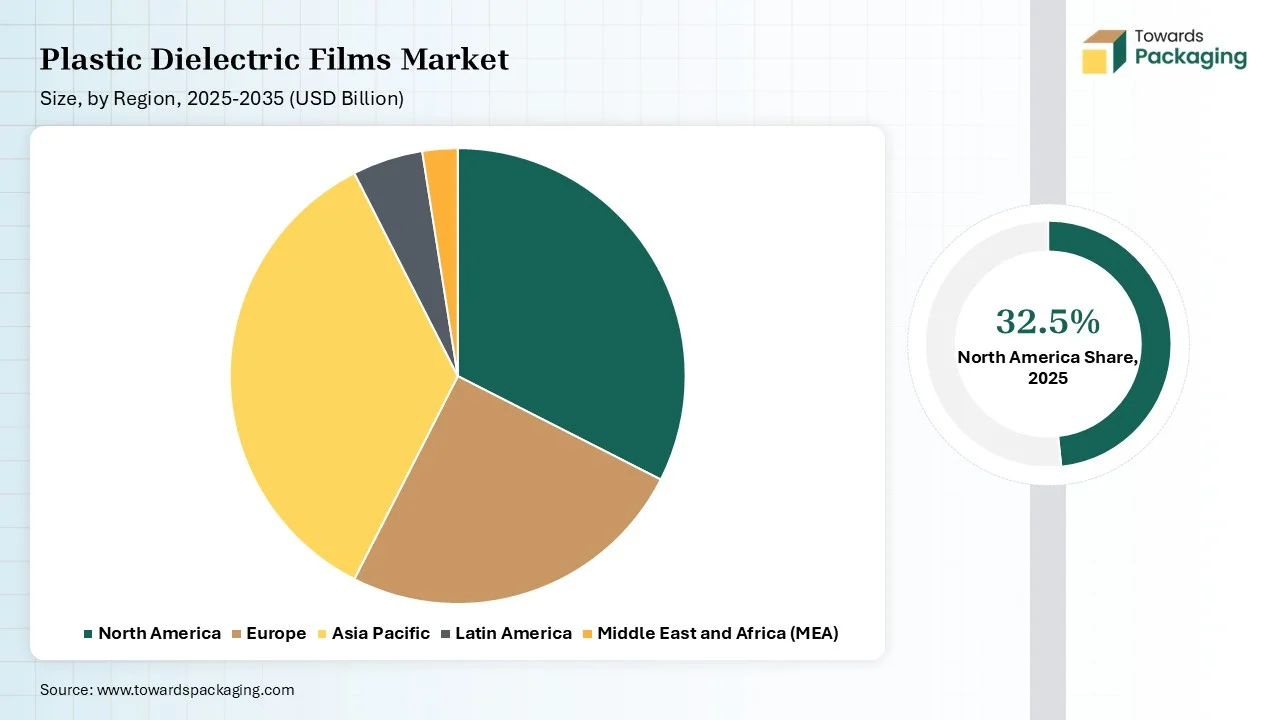

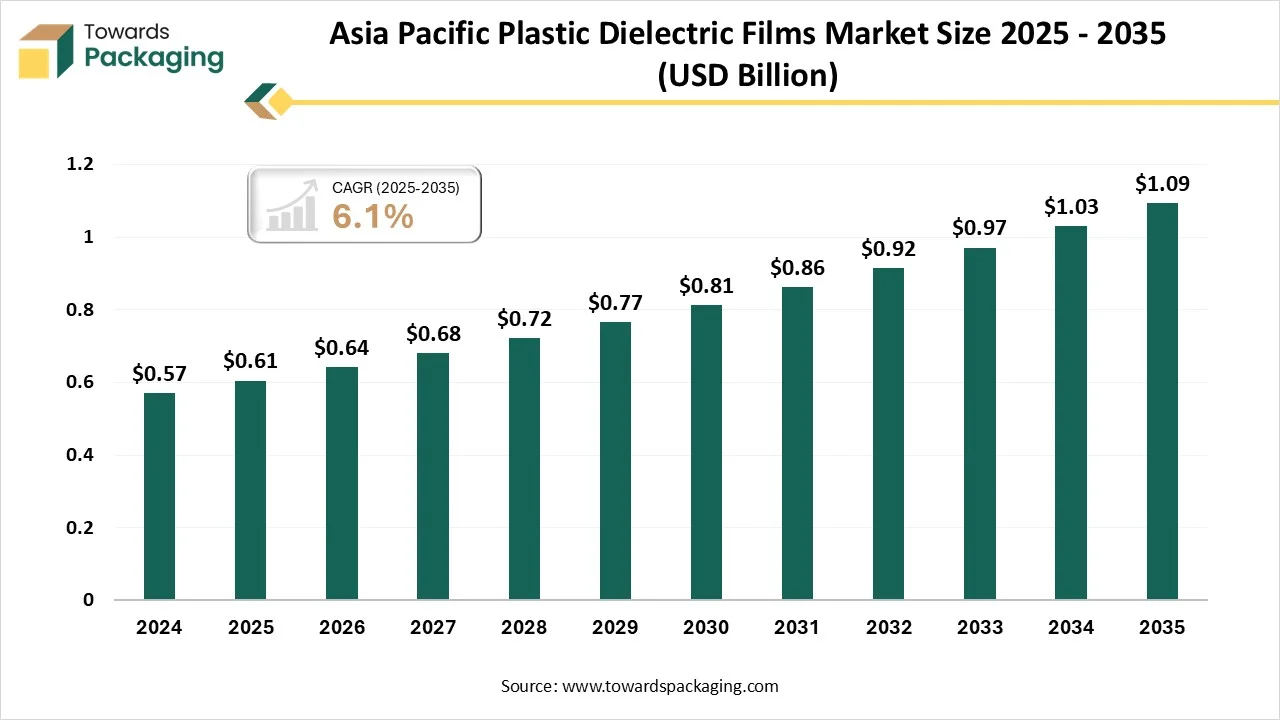

Asia Pacific held the largest share of the plastic dielectric films market in 2024, due to the presence of huge electronics companies in countries such as India, China, Japan, and several others. The well-established electronics producing ecosystem in this region, mixed with the increasing demand for energy-effectual capacitors and progressive electrical machineries, is enhancing the usage of high-presentation dielectric films. It is reinforced by flexible and automotive electronics engineering. China’s manufacture of capacitor film and innovative energy power storing approves PET dielectric film and polypropylene dielectric film, which grades top in the internal scale manufacture of the plastic dielectric films.

North America expects fastest growth in the market during the predicted period. This market is growing due to the availability of well-established industries of automotive, electronics, renewable energy, and aerospace. This region assistances from well-recognized manufacturing outline, cultured research and expansion competences, and a robust assurance to energy-effectual, high-presentation electronic arrangements. The increasing acceptance of electric vehicles, development in solar and solar energy schemes, and the placement of 5G structure are growing the demand for reliable dielectric resources in circuit and capacitors shield components.

By Product / Polymer Type

By Application / Function

By End-User / Industry

By Specification / Performance Attributes

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPlastic Dielectric Films Market