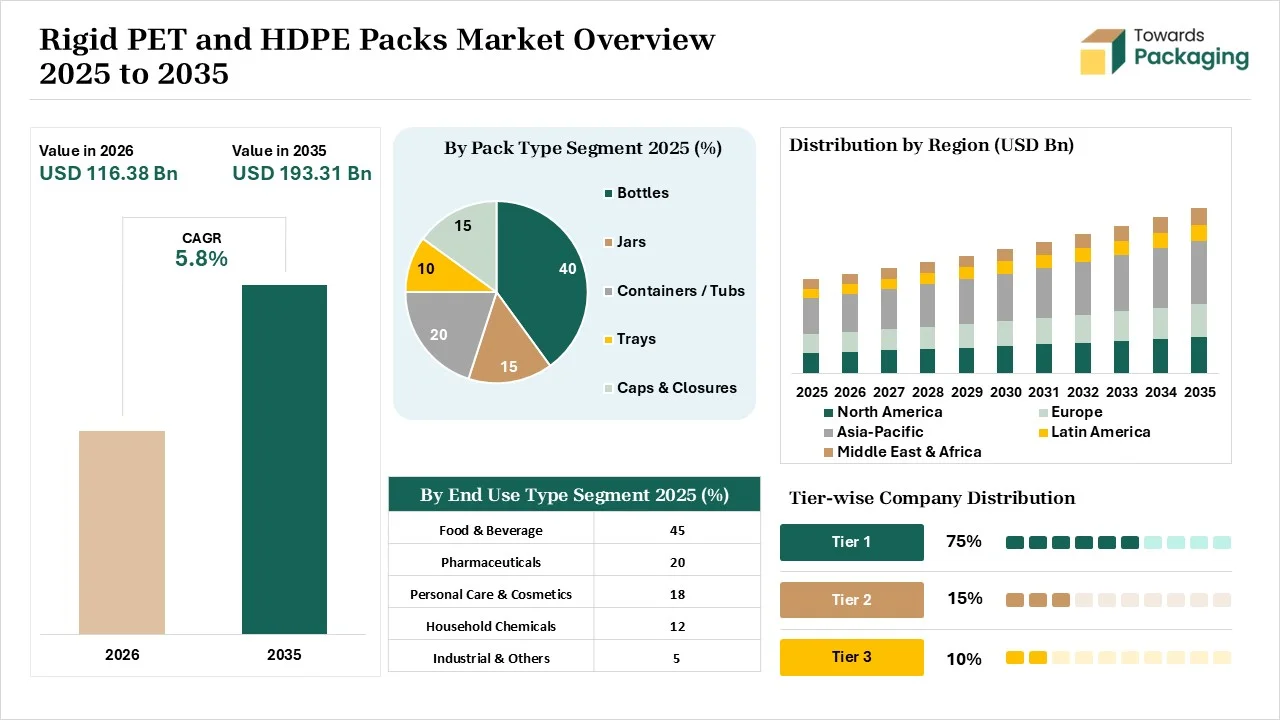

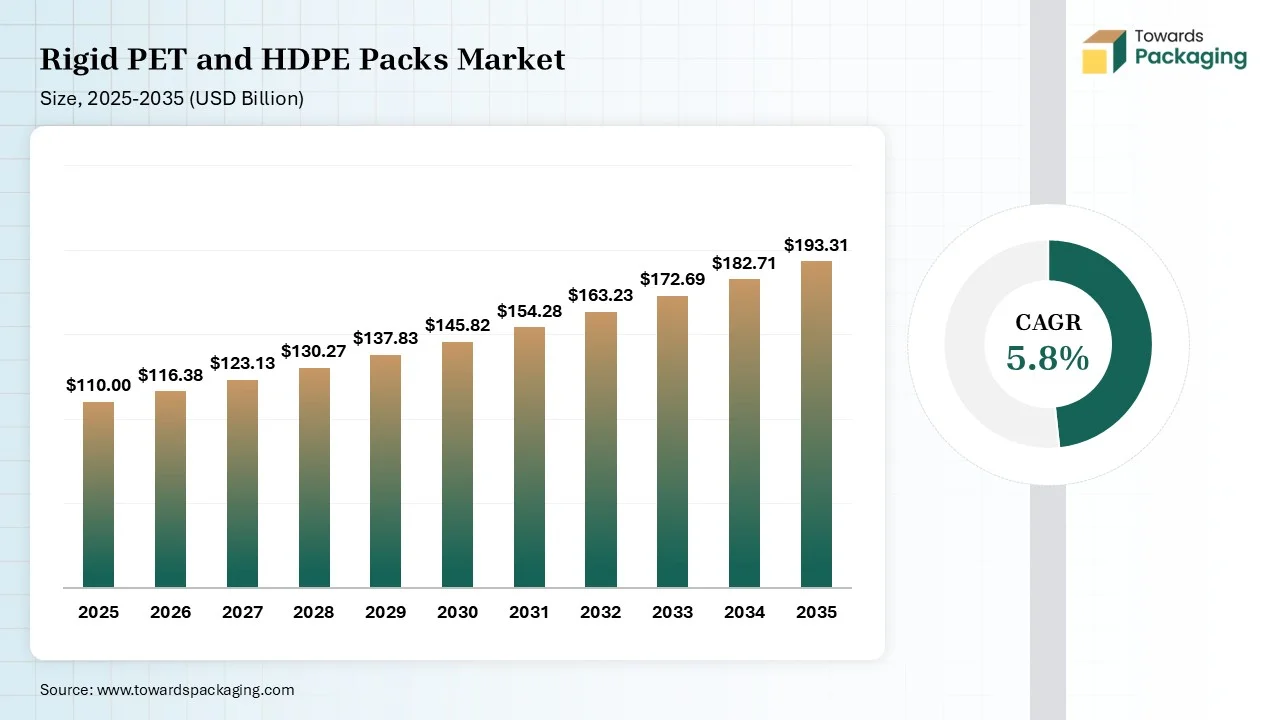

The rigid PET and HDPE packs market is projected to grow from USD 116.38 billion in 2026 to USD 193.31 billion by 2035, registering a CAGR of 5.8% during the forecast period. The market study provides comprehensive coverage of market size, share, growth drivers, opportunities, segment analysis, regional performance, competitive benchmarking, company profiles, value chain assessment, trade statistics, pricing trends, manufacturing analysis, supplier evaluation, and future industry outlook. Rising accessibility of personal care products, growing demand for food-grade resins, transportation efficiency requirements, and increasing consumption of prepared meals are supporting market expansion worldwide.

Rigid PET packs are packaging items made from rigid PET, whereas rigid HDPE packs are packaging developed using HDPE. Rigid PET packs offer features like excellent natural barrier, exceptional transparency, high impact resistance, high clarity, excellent recyclability, and glass-like finish. Rigid HDPE packs offer features like high durability, higher heat tolerance, superior chemical resistance, excellent opacity, and safety. Rigid PET and HDPE packs are widely used in bottled water, cosmetic jars, blister packs, clamshell containers, milk jugs, large chemical buckets, jerry cans, and others.

The rigid PET and HDPE packs market growth is driven by the processed food explosion, shift to recycled plastic, healthcare growth, strong focus on chemical resistance, growing logistics needs, burgeoning smaller households, preference for brand differentiation, huge pharmaceuticals demand, enhancements in recycling technologies, and the interest in lightweight materials.

In March 2026, Indorama Ventures collaborated with Genesis Power & Energy Solutions and Nigerian Breweries Plc to launch develop rPET manufacturing facility in Nigeria. The new production site is present in Lagos and the annual production capacity of food-grade rPET is 45000 tons of the facility. The collaboration helps in lowering plastic waste.

The current technological developments, like generative AI, machine learning, IoT integration, 3D simulation, and digital tracking, are happening in the rigid PET and HDPE packs. The technological developments are driven by smart manufacturing, circularity, advanced polymer engineering, and material lightweighting. The AI is a significant development in the market that helps in revolutionizing plastic waste recycling.

AI maintains consistent resin quality and monitors packaging machinery. AI detects misaligned labels and easily separates plastic waste. AI lowers excess inventory and helps in achieving food-grade purity. AI manufactures ultra-thin packages, and it prevents bloated inventories. AI analyzes market patterns and supports a cost-effective process. Overall, AI supports from resin processing to demand forecasting.

The stage acquires primary raw materials like HDPE and PET. The stage sources raw materials from recycled resins and virgin resins.

The stage includes technologies like extrusion blow molding, thermoforming, stretch blow molding, and injection molding.

Package design focuses on graphic design, structural engineering, and design for recycling. Prototyping focuses on testing rigorous properties, 3D digital modeling, and physical prototyping.

Key Players:- ALPLA, Schutz, Amcor plc, Plastipak Holdings, Inc., Berry Global Group, Inc.

The PET segment dominated the market with 55% share in 2025 due to its unbreakability and strong gas-barrier properties. The focus on protecting chemicals in pharmaceutical products and the continuous e-commerce shipping increases the use of PET. The rise in rPET mandates in several regions increases the adoption of PET. The all-around safety, design flexibility, unmatched aesthetics, transport efficiency, and high circularity of PET drive the segment growth.

The HDPE segment held the 45% market share in 2025 due to the growing use in harsh household cleaners. The increased use of motor oils and the high demand for lightweight transportation benefits increase the use of HDPE. The increased glass replacement in rigid packaging and the rise in OTC liquid drugs increase the use of HDPE. The excellent chemical protection and exceptional recyclability of HDPE support the segment growth.

The bottles segment dominated the market with 40% share in 2025 due to the huge beverage consumption globally. The increasing need for exceptional clarity in cosmetic packaging and the focus on branding aesthetics increase the use of PET and HDPE bottles. The need for UV resistance in pharmaceutical products and the growing use of dispensing lotions increase the adoption of PET and HDPE bottles. The rise in liquid prescriptions and the explosion of bottled juices drive the segment growth.

The containers/tubs segment held the 20% market share in 2025 due to the high use in premium food products. The need for premium transparency in personal care and the focus on keeping cosmetics fresh increase the use of PET containers or tubs. The growth in long-term storage of products and the focus on superior moisture protection in dry food grains enhance the use of HDPE containers or tubs. The logistical efficiency and extended shelf life of rigid PET containers or tubs support the segment growth.

The jars segment held the 15% market share in 2025 due to its utilization in the personal care industry. The higher demand for heavy-duty cleaners and the focus on eliminating breakage risks increase the use of rigid PET & HDPE jars. The burgeoning cosmetic sales and the surging buying of heavy-duty agrochemicals increase the use of rigid PET & HDPE jars. The surge in premium skincare packaging boosts the segment growth.

The caps & closures segment held the 15% market share in 2025 due to the massive manufacturing volume of bottled water. The need for moisture-tight barriers in pharmaceuticals and the shift to convenience packaging increase the use of rigid PET & HDPE caps & closures. The increased utilization of dispensing caps and the growing development of PET-based closures boost the overall segment growth.

The food & beverage segment dominated the market with 45% share in 2025 due to the focus on protecting highly perishable goods. The spoiling prevention in the food industry and the protection of beverage freshness increase the use of rigid PET and HDPE packs. The expansion of squeezable ketchups and the need to maintain the nutritional profile of food contents increase the adoption of rigid PET and HDPE packs. The exploding convenience food sector drives the segment growth.

The pharmaceuticals segment held the 20% market share in 2025 due to the heavy consumption of sensitive capsules. The patient's preference for liquid drug transparency and the rise in sustainable pharmaceutical manufacturing increase the adoption of rigid PET and HDPE packs. The growing demand for sterile containers in the pharmaceutical sector and the exploding generic medications support the segment's growth.

The personal care & cosmetics segment held the 18% market share in 2025 due to the higher demand for body washes. The increased purchasing of creams online and the need for glass-like clarity in personal care items increase the adoption of rigid PET and HDPE packs. The circular economy goals in the personal care industry help with expansion. The development of precision-dispensing pumps boosts the segment growth.

The blow molding segment dominated the market with 50% share in 2025 due to the mass-production efficiency. The manufacturers' focus on sustainability alignment and the need to reduce transportation emissions increases the adoption of blow molding. The rising container production and the massive FMCG industry increase the use of blow molding. The excellent material properties and integrated handling capabilities of blow molding drive the segment growth.

The injection molding segment held the 25% market share in 2025 due to its design complexity and high repeatability. The manufacturing waste reduction and the development of rigid closures increase the use of injection molding. The creation of tight dimensional tolerances and the focus on supply chain safety increase the use of injection molding. The burgeoning high-volume manufacturing supports the segment growth.

The stretch blow molding segment held the 15% market share in 2025 due to the lower gas permeability. The development of thinner bottles and the focus on radical weight reduction increase the use of stretch blow molding. The production of edible oil containers and mineral water bottles increases the use of stretch blow molding. The seamless fit, high output rates, biaxial orientation, and exceptional aesthetics of stretch blow molding boost the segment growth.

Asia Pacific dominated the market with a 38% share in 2025 and is expected to grow at 6.8% CAGR in the market during the forecast period due to the increased buying of convenience goods. The high accessibility of raw materials and the burgeoning online retail increase the adoption of rigid PET and HDPE packs. The focus on hygiene in the cosmetic industry and the soaring popularity of ready-to-consume drinks increase the use of rigid PET and HDPE packs. The rise in the buying of household cleaners and bottled water drives the market growth.

China

India

North America held the 22% market share in 2025 due to the surging region’s environmental consciousness. The growing consumer interest in RTE meals and the explosion of retail footprints increase the adoption of rigid PET and HDPE packs. The robustly growing e-pharmacies and the development of single-serve containers increase the adoption of rigid PET and HDPE packs. The well-established trucking sectors and the huge demand for condiments support the market growth.

United States

The high consumer spending on single-serve beverages and the robust medical industry increases the use of rigid PET and HDPE packs.

The continuous expansion of pharmaceutical capacity and the advancing packaging technology increases the adoption of rigid PET and HDPE containers.

Canada

Europe held the 20% market share in 2025 due to the availability of high-quality recycled feedstocks. The growing industrial packaging activities and the popularity of carbonated soft drinks increase the adoption of rigid PET and HDPE packs. The strong raw material collection infrastructure and the availability of HDPE feedstocks increase the production of rigid PET and HDPE packs. The growing electrical sectors support the market growth.

Germany

United Kingdom

Latin America held the 10% market share in 2025 due to the high logistical efficiency. The convenience food consumption and the expanding digital economies increase demand for rigid PET and HDPE packs. The huge dairy products consumption and the increasing global freight costs increase the use of rigid PET and HDPE packs. The rapidly expanding e-commerce market boosts the overall growth.

Brazil

Argentina

The Middle East & Africa held the 10% market share in 2025 due to the low cost of raw materials. The high presence of tourism and the rise in production of large chemical drums increase the adoption of rigid PET and HDPE packs. The transition towards convenience-oriented products and the high investment in water supply increases the use of rigid PET and HDPE packs. The increased buying of bottled drinking water supports the market growth.

Saudi Arabia

United Arab Emirates

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products and Services |

| 1. | Amcor PLC | Zurich, Switzerland | Switzerland | The company focuses on using PCR content in its packaging format and developing specialized high-barrier solutions. | Beverage Bottles, Specialty Bottles, Jerricans, Caps, Jars, Closures, and Tubes |

| 2. | Berry Global Group, Inc. | Evansville, Indiana, United States | United States | The company supplies rigid packaging solutions to CPG brands and focuses on the development of customized rigid solutions. | Pharma Bottles, Claripill Range, Optimum R-HDPE Containers, Midi Tubular Range, Chameleon Range |

| 3. | ALPLA Group | Hard, Austria | Austria |

The company operates its recycling facility and manufactures eco-bottles. The company acquired Energoplast to enhance its share in Southeast Europe. |

Bottles, Caps, Preforms, Containers, Closures |

| 4. | Silgan Holdings Inc. | Stamford, Connecticut, United States | United States | The company manufactures custom containers. The company focuses on using PCR plastics and expanding dispensing worldwide. | Wide-Mouth Jars, Tablet Containers, Roll-On Packs, PCR-Focused Jars, Bottles |

| 5. | Plastipak Holdings, Inc. | Plymouth, Michigan, United States | United States |

The company offers blow molding and injection molding manufacturing technology. The company develops customized containers for renowned B2B clients. |

PET Bottles, HDPE Bottles, Specialty Aerosols, PET Containers, Preforms, HDPE Containers |

By Material Type

By Pack Type

By End Use

By Manufacturing Technology

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarRigid PET and HDPE Packs Market