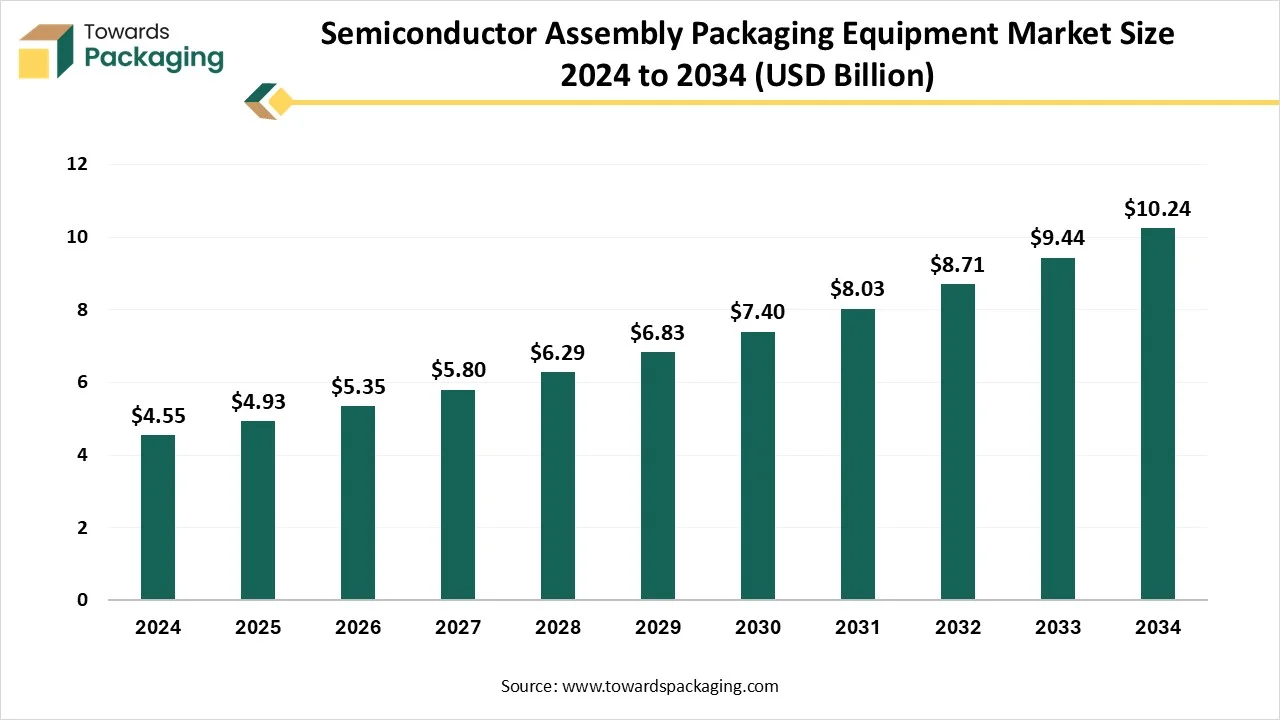

The semiconductor assembly packaging equipment market is expected to grow from USD 5.35 billion in 2026 to USD 11.11 billion by 2035, at a CAGR of 8.45% during the forecast period. This market is segmented by equipment type, packaging type, application, and end-user.

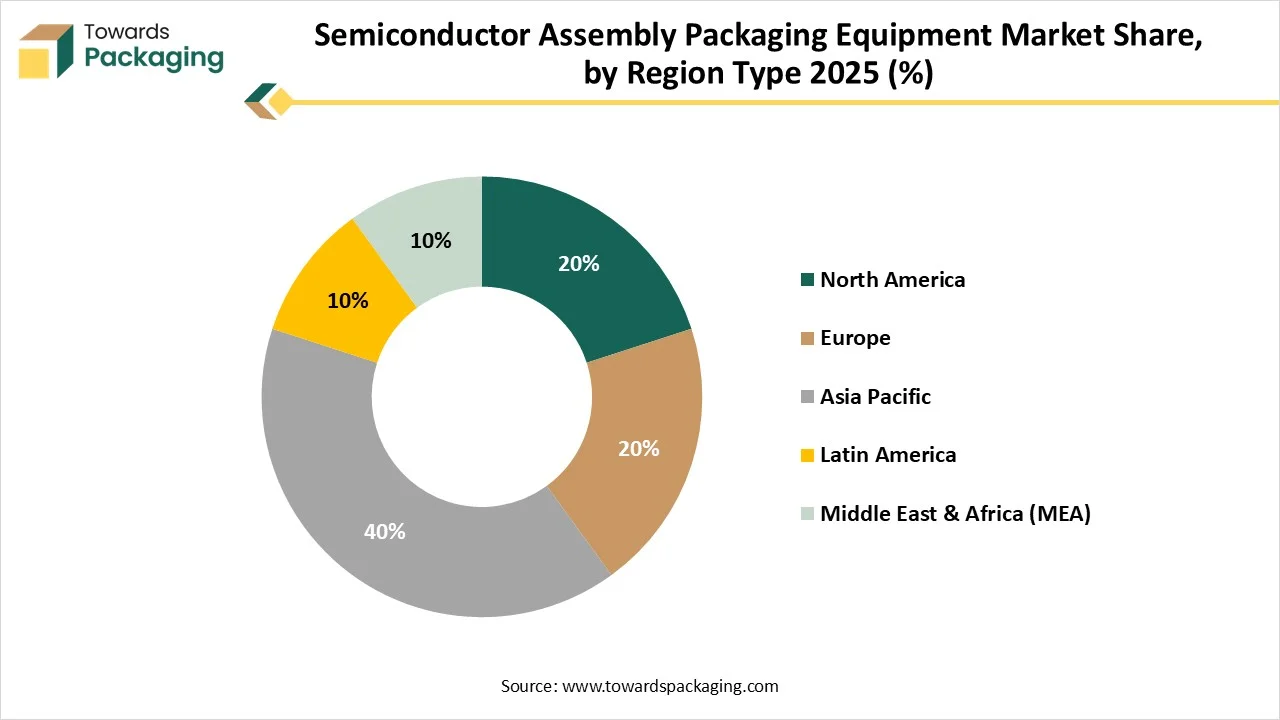

The major regions contributing to market growth include Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa. Asia Pacific led the market in 2025, owing to the presence of major OSAT companies and government support in countries like China, Japan, and South Korea. North America is projected to grow at a notable CAGR due to strong market players such as Lam Research and Applied Materials.

The study further reviews supply chain dynamics, raw material sourcing, and logistics networks supporting semiconductor manufacturing, along with regional demand trends and government investments shaping the industry. In addition, the report highlights competitive strategies of major equipment manufacturers, innovation in advanced packaging technologies, and the role of OSAT companies and foundries, helping businesses understand market dynamics and identify future growth opportunities in the semiconductor assembly packaging equipment market.

Semiconductor assembly packaging equipment are process utilized for assembling, interconnecting, encapsulating, and testing semiconductor devices after wafer fabrication. The prime aim is to generate durable goods that can associated to their equipment while protecting the fragile chip from damage. Major functions and processes involved in this industry die bonding, encapsulation/molding, wire bonding, and testing. These equipment’s are operated precisely to connect and handle microscopic components. Advanced automation, AI, and robotics are utilized to enhance throughput and reduce errors at the time of high-production.

The semiconductor assembly packaging equipment market is experiencing major technological shift due to enhanced wafer-level packaging (WLP), 3D packaging, and system-in-package (SiP). The market is experiencing enhanced investment in packaging technologies by companies and government initiatives. Rapid advancement in the medical devices and electric vehicles has boosted the growth of the packaging industry. The development is fuelled by the increasing advancement of AI technology in the 5G technology, consumer electronics, portable devices, and electric vehicle.

The major raw materials utilized in this market are gallium arsenide, silicon, and several other metals.

The major components used in this market are wafer mounting, dicing, plating and inspection, bonding, and encapsulation/molding.

This segment comprises managing transportation, customs clearance, and warehousing.

")

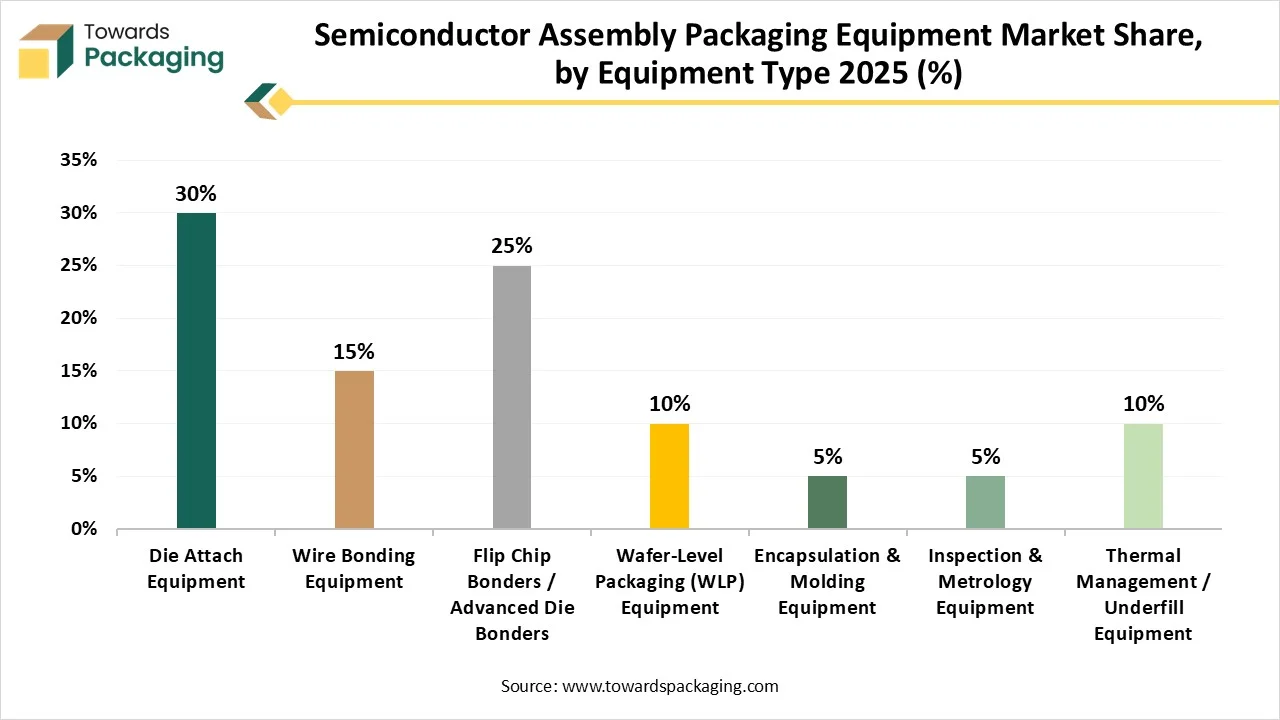

The die attach equipment segment dominated the market with highest share in 2025 due to increasing demand of the technologies such as die bonder, hybrid bonding, and various other. Enhancement in miniaturization technology has encouraged the growth of this segment. This industry boosts the development of smaller yet powerful chips which enhance the utilization of die attach. Encouragement to the domestic semiconductor manufacturer with bulk investment has supported the growth of this segment. The rapid expansion of photonics, IoT, and medical electronics.

The flip chip bonders / advanced die bonders segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to increasing demand for performance and miniaturization. The rapid growth in the electronics, telecommunication, and automotive industry has raised the utilization of this segment. It is widely used for complex packaging architecture like 3D stacking, multi-chip packaging, and chiplet architectures.

| By Packaging Type Segments | Market Share 2025 (%) |

| Wire Bond Packaging | 40% |

| Flip Chip Packaging | 30% |

| Wafer-Level Packaging (WLP) | 10% |

| 3D Integrated Circuits (3D-ICs) | 20% |

The wire bond packaging segment dominated the market with highest share in 2025 due to its affordability, maturity, and reliability. It is widely used due to rising complexity in the electronic devices and high-performance equipment. Continuous innovation in the wire and automation has raised the demand for such packaging segment. This technology is suitable to meet the huge production demand. These are used in semi-automatic as well as fully automatic machines.

The flip chip packaging segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to the huge demand for high-performance application such as consumer electronics, AI, and 5G. The advance packaging process includes mounting a chip face down for enhanced thermal dissipation, shorter electrical path, and more interconnections. This segment helps in high density connections in comparison to wire bonding. It has better thermal management capacity which promote the expansion of this segment.

")

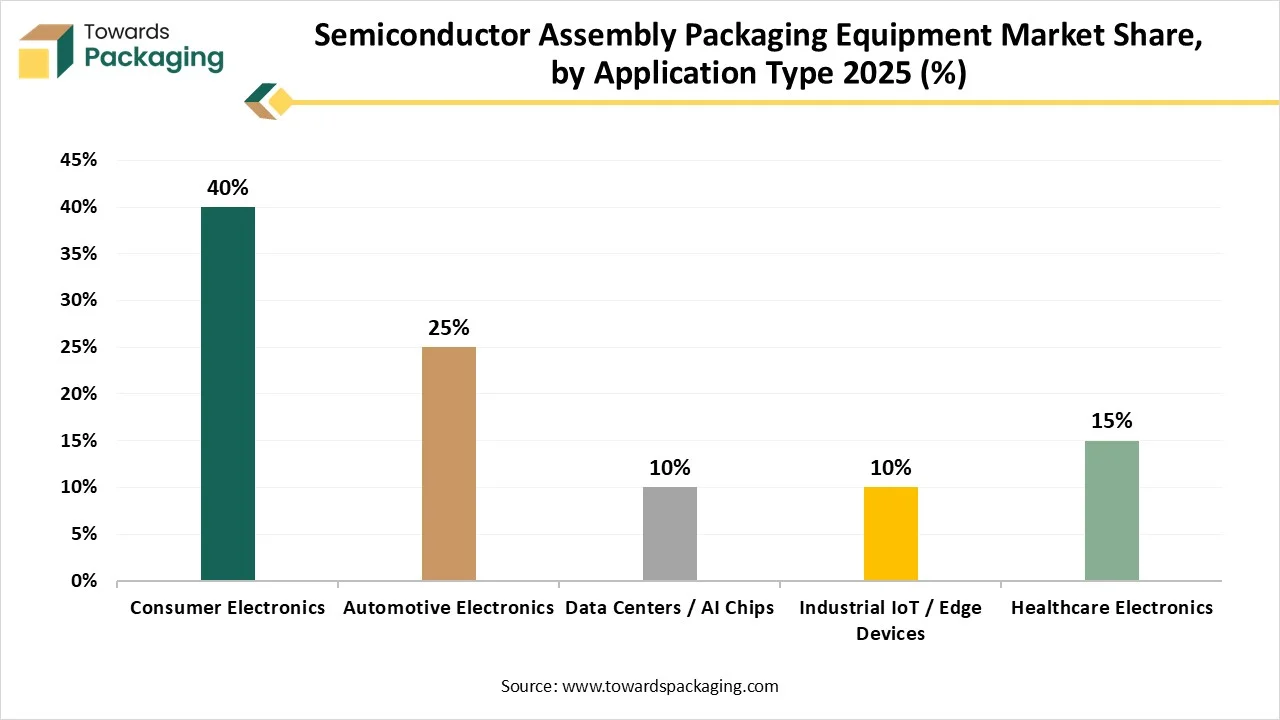

The consumer electronics segment dominated the market with highest share in 2025 due to huge demand for products such as smart home devices, smartphones, and wearables. This demand is further influenced by the requirement for equipment which help in the development of high density, high performance, and compact chips. Huge investment towards developing electronics to meet the expectations of the consumers has boost the growth of the market.

The automotive electronics segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to growing electric vehicles adoption with integrated Advanced Driver-Assistance Systems (ADAS). The increasing demand for wafer-level and flip-chip bonding to ensure the durability and thermal performance required for harsh automotive surrounding. The industry needs precise bonding, assembly equipment, and encapsulation to manage the precise necessity of automotive industry.

| By End-User Segments | Market Share 2025 (%) |

| OSAT Companies | 45% |

| IDMs | 25% |

| Foundries | 30% |

The OSAT companies (outsourced semiconductor assembly and test) segment dominated the market with highest share in 2025 due to testing service and chip assembly. These companies are providing a wide diversity of services such as traditional to advanced level packaging. The continuous expansion of electronics sector boosts the demand for advanced semiconductor devices. Enhanced usage of EVs and medical devices has raised the demand for this segment profoundly. Outsourcing help companies to get latest innovative semiconductors at an affordable range.

The foundries segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to rising demand for enhanced semiconductors. These are used for automotive, AI, IoT, and 5G because of ongoing trend for consumer electronics and miniaturization. This segment comprises a wide range of devices from wafer level device such as bonding and dancing.

")

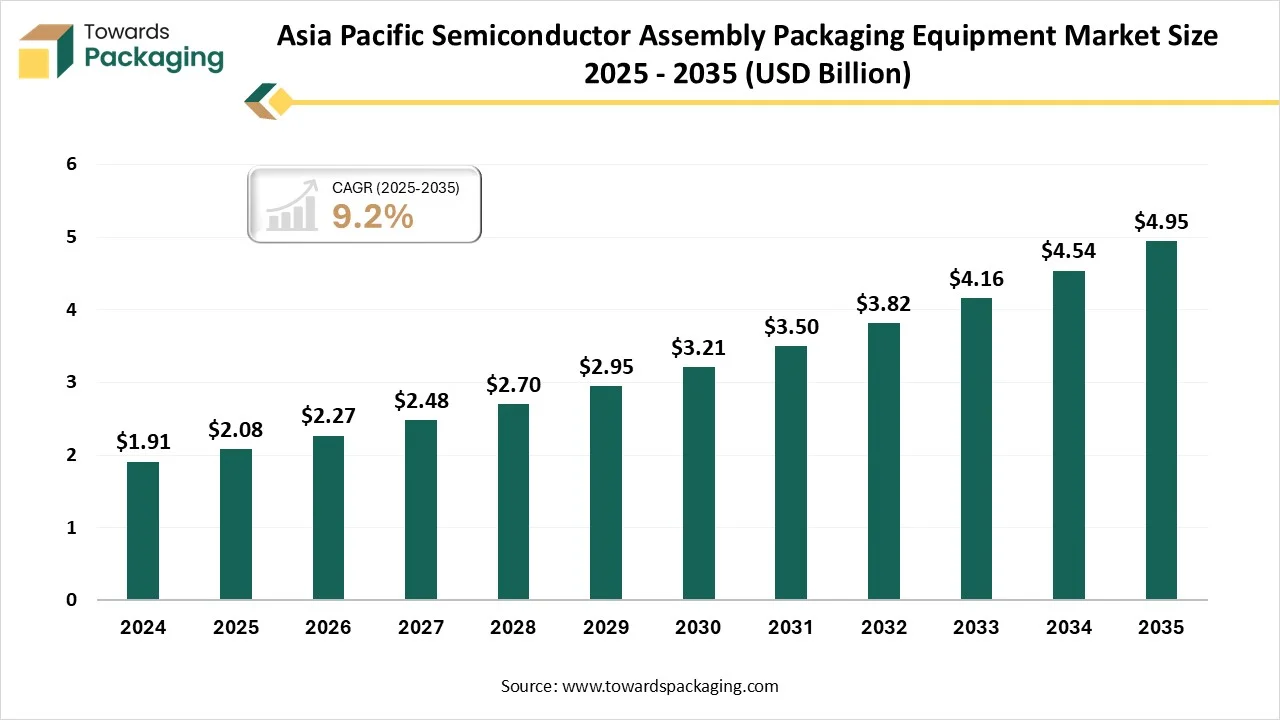

Asia Pacific held the largest share in the market in 2025. This market is growing due to increasing manufacturing ecosystem. This region is centre of OSAT companies and component suppliers making a huge ecosystem and influencing high-demand for packaging and assembling equipment. Moreover, fast digital alteration, regional government funding for semiconductor self-dependance, and growing demand for customer electronics are influencing capacity extensions and technological advancements. Huge investment towards advancement in packaging sector has raised the demand for this market.

India has a huge semiconductor assembly packaging equipment market due to continuous support provided by the government through funding and promoting its advantages. Growing government-backed creativities goaled at emerging a contained semiconductor ecosystem. Increasing interest from worldwide companies, growing domestic electronics usage, and developing fundings in semiconductor sector are contributory to the necessity for current assemblage and packing tools. India’s emphasis on becoming an engineering and design center is additionally fast-tracking the acceptance of progressive device in the back-end semiconductor distribution.

North America expects the significant growth in market during the forecast period due to rising investment of the government towards this industry. Continuous investments in upcoming-generation semiconductors, attached with rising demand for superior-performance computation, AI, and broadcastings infrastructure, are influencing the requirement for refined packing resolutions. Moreover, the existence of main market players and research organizations, accompanied by kind policy creativities expected at consolidation domestic chip construction, is improving apparatus demand and founding this region as a centre for semiconductor progression.

U.S. is dominating in the market in North America region due to the presence of major market players such as KLA Corporation, Teradyne, Inc., Lam Research, Onto Innovation, and several others. The primary focus of the country is on enhanced-performance computation, AI-determined, and aerospace electronics applications has influenced constant funding in progressive packing technologies. Moreover, helpful national strategies and planned initiatives goaled at improving domestic chip construction have reinforced demand for apparatus across major services.

Europe is notably growing due to strong demand for consumer electronics and automotive industry has influenced the demand of market. Growing regional hard work to improve semiconductor enhancement and growing advanced chip engineering proficiencies. Europe is endorsing invention in semiconductor packing skills, mainly for automotive, telecom, and industrial applications, as fragment of wider planned creativities. The drive toward emerging excellent-performance, energy-effectual electronic apparatuses is encouraging investments in packaging of tools and modern assembly.

Strong Industrial Base in Germany Promote the Semiconductor Assembly Packaging Equipment Market Growth

Germany has a huge market due to the presence of strong industrial base. Strong automotive sector of this country has promoted the demand for enhanced quality packaging. The primary focus is on incorporating the progressive technologies, like autonomous driving has amplified the necessity for advanced chip packing resolutions. Additionally, sustained funds in high-tech organization and manufacturing superiority have enhanced the acceptance of upcoming-generation semiconductor assembly and packaging equipment industry.

By Equipment Type

By Packaging Type

By Application

By End User

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarSemiconductor Assembly Packaging Equipment Market